Implantable Medical Devices Market Synopsis:

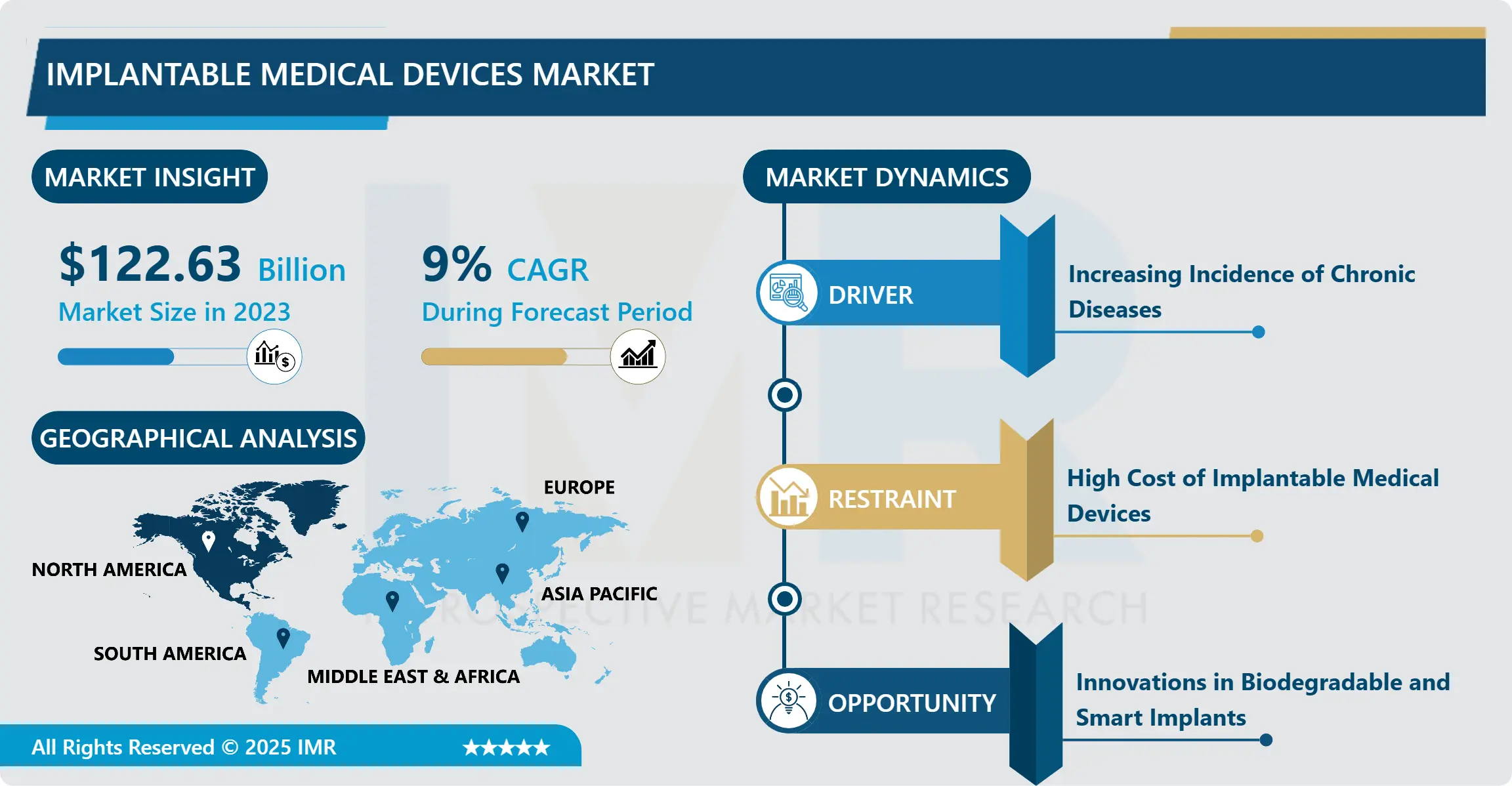

Implantable Medical Devices Market Size Was Valued at USD 122.63 Billion in 2023, and is Projected to Reach USD 266.33 Billion by 2032, Growing at a CAGR of 9.00% From 2024-2032.

Implantable medical devices can therefore be defined as the part of market that involves the creation, production and sale of devices made for use in human body for specific purposes of diagnosis or therapy. These devices are for instance pacemakers, defibrillators, orthopedic implants, dental implants, neurostimulators and others. This market is fuelled by technology, rising incidence of chronic diseases, rising elderly population and the need for less invasive surgeries. During transition in the healthcare industry, implantable medical devices become indispensable tools to bring better and quality life, involvements in lessen the burden of diseases.

The Implantable Medical Devices industry has been experiencing growth over the last few years, having broadened its technology, the rise in chronic diseases, together with the aging population. These include pacemakers, defibrillators, neurostimulators and orthopedic implants; these devices are very important in complimenting patients care in order to achieve desirable outcomes that would by and large augment their quality of life. Other factors driving the market progress consist of increased demand for less invasive surgeries and companies that create intelligent and networked devices. In particular, self-powered implantable devices, incorporating artificial intelligence, machine learning and other multifunctional technologies will remain high on the global healthcare agenda as more organizations shift towards patient-centric care.

In addition, more demand is placed on current and future legislation in regards to approval and commercialization of these devices, which means that their safety and efficacy would be of a better quality. The regions such as North America and Europe have large market shares due to having sound health facilities coupled with higher per capita income and rising R & D spending. But the fastest growth is expected in the Asia/Pacific region primarily due to enhanced focus on healthcare spending, better access to healthcare along with enhancing awareness of more sophisticated technologies in healthcare.

However, the market comes with its unique challenges such as high costs in implantable devices, regulatory hurdles, and risks or complications that emanate from the implantation of devices. Due to these challenges, the manufacturer is concentrating on Research and Development and differentiation of products to suit the various consumers within the health sector. There are also growing multiparty collaborations between the medical device industry and healthcare organizations to create better and easy to use implantable medical devices.

Therefore, the implantable medical devices market has a strong growth outlook since the factors include advancement in technology and evolution in the population demographics along with emphasis on patient-centricity. Despite these phenomena, such as the changing legislation and the rising costs, there are certain opportunities that may be useful for market members and strengthen the sphere of healthcare.

Implantable Medical Devices Market Trend Analysis:

Growing Demand and Technological Advancements Drive the Implantable Medical Devices Market

-

Implantable medical devices are being sought after due to their ability to cure heart related issues, symptoms of neurological diseases, and certain musculoskeletal abnormalities.. Heart pacemakers, implants, aesthetic surgery and joint replacements are a few examples of devices that help people with chronic diseases and conditions while improving their quality of life and the quality of their future health throughout their lifespan. Furthermore, the increasing global population and the pre-dominance of the aging population, especially in the developed countries have added to this demand since implantable devices are helpful in handling most of the age related conditions. Developing markets are also experiencing a similar trend as there is both awareness and, equally importantly, the development of networks to cater for the provision of such devices to potentially enhanced quality life shifts for various health conditions.• Furthermore, modern trends in minimally invasive surgeries which comprise a major segment have fuelled the implantable device market. disorders, and orthopedic conditions. Devices like pacemakers, defibrillators, and joint replacements are essential in managing these chronic health issues, offering patients improved quality of life and enhanced long-term health outcomes. The aging global population, especially in developed regions, has further fueled this demand as implantable devices play a crucial role in addressing age-related health concerns. Emerging economies are also witnessing a surge in demand for these devices due to increased awareness and improved healthcare infrastructure, making life-changing medical solutions more accessible to a broader population.

- Additionally, advances in minimally invasive surgical techniques have contributed significantly to the growth of the implantable devices market. Technological advancements that present new minimally invasive approaches to surgery and recovery are also increasing the appeal of implantable devices among both physicians and patients. Positive changes in the patients’ status, faster healing and less strict post-operative complications have turned into major reasons as to why these devices are being introduced. Since the trend towards using less invasive procedures in most cases, the implantable medical devices market is forecasted to remain on an uptrend, supported by a combination of innovative technology and patient satisfaction.

Growing Demand for Minimally Invasive Implantable Medical Devices

-

The overall growth in the implantable medical devices market driven by the greater focus towards less invasive techniques, including pacemakers, neurostimulators and orthopedic implants. People including the patient and doctor are in constant search of better treatment methods to minimize the likelihood of surgery and the time required for rehabilitation, leading to a high demand for enhanced implantable technology. Such devices which are made to reduce trauma and enhance the comfort of the patient fall under the chip technologies in health care facilities. Microtechnological innovations are also taking central part, enabling people to develop appliances that are more compatible with human tissues. This minimizes immune rejection impacts and boosts the functionality of implants making them useful in treating more variety of patients with long term needs.

- One trend of advancement in this area is the use of BIOMER with an ability to dissolve in the body and support implantation naturally. This advance technology means no further surgeries are required to remove an implant therefore improving patient results and cutting general health care bills. However resorbable biopolymers are continuously being improved and health conditions subject to implantation can now be addressed more accurately with few side effects on the implantable devices. The trend towards such innovations is now one of the primary areas where companies can fund new research and development in order to meet the continually growing need for higher performance and improved safety of implantable devices. They help drive market growth while at the same time developing opportunities for firms that initiate the use of the advancements.

Implantable Medical Devices Market Segment Analysis:

Implantable Medical Devices Market is Segmented on the basis of Product Type, Biomaterial, End Use, and Region

By Product Type, Cardiovascular Implants segment is expected to dominate the market during the forecast period

-

Cardiovascular implants are used for treating heart and blood vessel diseases and include pacemakers, stents and artificial heart valves. These implants help patients receive help for irregular heartbeat, blood circulation, and issues such as arrhythmias, heart valve diseases or arterial blockages. There is for instance pacemakers that control irregular heartbeats and stents that prevent arteries from being blocked and that provide regular blood circulation especially after events like heart attacks. These devices have played a very critical role in extending lifespan and quality life of the clients, thus making them crucial tools in the management of cardiovascular diseases with a market demand in the international market.

- This is even more so when considered against the backdrop of an increasing incidence of cardiovascular diseases all over the world particularly among the ageing population and areas with tidal waves of obesity and diabetes. New innovative technologies enabling fundamental and safety enhancement of the implantation procedures have also contributed to patient recovery from technology implantation. Advances in device biocompatibility and service life are increasing the use rate in developed countries, because patients need replacements more often. At the same time, cardiovascular implant demand is rising in such countries due to improved health care and the growth of health care facilities that make life-saving procedures available to a greater number of people.

By End Use, Hospitals segment expected to held the largest share

-

Hospitals are the key consumers of the medical implants because they not only provide medical services, including well-equipped facilities and well-trained personnel for the implant operations, but also, they offer the other surgical procedures that may be necessary in light of a patient’s medical condition. It should be noted that in complex implant surgeries, such as cardiovascular and neurological implantation, only hospitals are prepared for high risk and emergencies. Because most hospitals have advanced clinicians and equipment, they are the best option in picking the required sophisticated and close attention more than patients. The cases of chronic diseases and geriatric population are on the rise and so the hospitals are seeing a demand for durable and value-added implants that relate to such conditions.

- Additionally, the technology applied to medical implants is expanding over the years, the success rate of surgeries and recovery periods of patients are improving, thus, it can be said that hospitals are an important factor in implant procedures. Techniques used, imaging and the materials used in implantation help in improving on the probability and hasten the days clients have to spend in the hospital making the operations more convenient. The role of hospitals is expected to persist as a reference market for implant surgeries, given the current and future trends of hospitals’ development that implies a focus on the confrontation of the growing demand for healthcare services worldwide, particularly in countries with the aging population and increased rate of different diseases.

Implantable Medical Devices Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

The market for Implantable Medical Devices in North America holds the largest market share and is erupting at a high rate due to increased healthcare consciousness, good healthcare facilities, and significant funding towards medical device innovation. The region also enjoys stable and sustainable regulatory environment and reimbursable policies that rehearsal latest medical technologies. Specifically, the role of the U.S. was very important and it has a large contribution to the growth of the market. The general status of healthcare across the country can be considered to be rather high and the following development of the tendencies can be seen: The approach to healthcare all over the country can be viewed as rather progressive due to the introduction of implantable devices by a large number of representatives of the healthcare sector. Market favourites including pacemakers, orthopedic implants and neurostimulators to offer a measure of support to this view indicating that the region holds a strong thirst for top notch medical aid.

- Another factor explaining the growth of implantable medical devices market is an overall rising aging population in North America, with a particular focus on the U.S. With the aging population there is an increase in common geriatric diseases like cardiovascular diseases, orthopedics and neurological diseases for which implantation services are required. Also, pathogens including diabetes, hypertension and obesity, which have continued to increase in prevalence, creates demand for devices that provide long term cure. Owing to the increase of minimally invasive surgeries and advanced technologies of the implantable medical devices, this market also experienced significant improvement in the revenue growth in North America.

Active Key Players in the Implantable Medical Devices Market:

-

Medtronic

- Abbott Laboratories

- Johnson and Johnson

- Boston Scientific Corporation

- Smith & Nephew plc

- Stryker

- Cochlear Limited

- Integra LifeSciences

- LivaNova PLC

- Biotronik SE and Co. KG

- Other Active Players

Key Industry Developments in the Implantable Medical Devices Market:

-

In June 2024, BioHorizons, a dental implant company launched Tapered Pro Conical, which utilizes a tapered body and thread to provide stability. In addition, this implant can be used for single tooth and full arch dental implants

- In June 2024, Royal Philips implanted the Duo Venous Stent System, an advanced medical device crafted to address symptomatic venous outflow obstruction in individuals suffering from chronic venous insufficiency. This achievement follows the device's premarket approval by the U.S. Food and Drug Administration, marking a significant advancement in treatment options for affected patients

- In November 2023, Medtronic received FDA approval for its Symplicity Spyral renal denervation system, for treating hypertension. The minimally invasive procedure uses radiofrequency energy to calm overactive kidney nerves, which can contribute to high blood pressure

|

Implantable Medical Devices Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 122.63 Billion |

|

Forecast Period 2024-32 CAGR: |

9.00% |

Market Size in 2032: |

USD 266.33 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Biomaterial |

|

||

|

By End Use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Active Implantable Medical Devices Market by Product Type

4.1 Active Implantable Medical Devices Market Snapshot and Growth Engine

4.2 Active Implantable Medical Devices Market Overview

4.3 Pacemakers

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Pacemakers: Geographic Segmentation Analysis

4.4 Implantable Cardioverter Defibrillators (ICDs)

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Implantable Cardioverter Defibrillators (ICDs): Geographic Segmentation Analysis

4.5 Neurostimulators

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Neurostimulators: Geographic Segmentation Analysis

4.6 Ventricular Assist Devices (VADs)

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Ventricular Assist Devices (VADs): Geographic Segmentation Analysis

4.7 Implantable Hearing Devices

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Implantable Hearing Devices: Geographic Segmentation Analysis

4.8 Other

4.8.1 Introduction and Market Overview

4.8.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.8.3 Key Market Trends, Growth Factors and Opportunities

4.8.4 Other: Geographic Segmentation Analysis

Chapter 5: Active Implantable Medical Devices Market by Application

5.1 Active Implantable Medical Devices Market Snapshot and Growth Engine

5.2 Active Implantable Medical Devices Market Overview

5.3 Cardiac

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Cardiac: Geographic Segmentation Analysis

5.4 Neurological

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Neurological: Geographic Segmentation Analysis

5.5 Hearing Impairment

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Hearing Impairment: Geographic Segmentation Analysis

5.6 Others

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Others: Geographic Segmentation Analysis

Chapter 6: Active Implantable Medical Devices Market by End User

6.1 Active Implantable Medical Devices Market Snapshot and Growth Engine

6.2 Active Implantable Medical Devices Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Hospitals: Geographic Segmentation Analysis

6.4 Ambulatory Surgical Centers (ASCs)

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Ambulatory Surgical Centers (ASCs): Geographic Segmentation Analysis

6.5 Specialized Clinics

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Specialized Clinics: Geographic Segmentation Analysis

6.6 Others

6.6.1 Introduction and Market Overview

6.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.6.3 Key Market Trends, Growth Factors and Opportunities

6.6.4 Others: Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Active Implantable Medical Devices Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 MEDTRONIC (IRELAND)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 ABBOTT LABORATORIES (USA)

7.4 BOSTON SCIENTIFIC (USA)

7.5 COCHLEAR LTD. (AUSTRALIA)

7.6 SONOVA HOLDING AG (SWITZERLAND)

7.7 LIVANOVA PLC (UK)

7.8 BIOTRONIK SE & CO. KG (GERMANY)

7.9 NUROTRON BIOTECHNOLOGY CO. LTD. (CHINA)

7.10 NEVRO CORP. (USA)

7.11 AXONICS INC. (USA)

7.12 MICROPORT SCIENTIFIC CORPORATION (CHINA)

7.13 STRYKER CORPORATION (USA)

7.14 OTHER ACTIVE PLAYERS

Chapter 8: Global Active Implantable Medical Devices Market By Region

8.1 Overview

8.2. North America Active Implantable Medical Devices Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By Product Type

8.2.4.1 Pacemakers

8.2.4.2 Implantable Cardioverter Defibrillators (ICDs)

8.2.4.3 Neurostimulators

8.2.4.4 Ventricular Assist Devices (VADs)

8.2.4.5 Implantable Hearing Devices

8.2.4.6 Other

8.2.5 Historic and Forecasted Market Size By Application

8.2.5.1 Cardiac

8.2.5.2 Neurological

8.2.5.3 Hearing Impairment

8.2.5.4 Others

8.2.6 Historic and Forecasted Market Size By End User

8.2.6.1 Hospitals

8.2.6.2 Ambulatory Surgical Centers (ASCs)

8.2.6.3 Specialized Clinics

8.2.6.4 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Active Implantable Medical Devices Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By Product Type

8.3.4.1 Pacemakers

8.3.4.2 Implantable Cardioverter Defibrillators (ICDs)

8.3.4.3 Neurostimulators

8.3.4.4 Ventricular Assist Devices (VADs)

8.3.4.5 Implantable Hearing Devices

8.3.4.6 Other

8.3.5 Historic and Forecasted Market Size By Application

8.3.5.1 Cardiac

8.3.5.2 Neurological

8.3.5.3 Hearing Impairment

8.3.5.4 Others

8.3.6 Historic and Forecasted Market Size By End User

8.3.6.1 Hospitals

8.3.6.2 Ambulatory Surgical Centers (ASCs)

8.3.6.3 Specialized Clinics

8.3.6.4 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Active Implantable Medical Devices Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By Product Type

8.4.4.1 Pacemakers

8.4.4.2 Implantable Cardioverter Defibrillators (ICDs)

8.4.4.3 Neurostimulators

8.4.4.4 Ventricular Assist Devices (VADs)

8.4.4.5 Implantable Hearing Devices

8.4.4.6 Other

8.4.5 Historic and Forecasted Market Size By Application

8.4.5.1 Cardiac

8.4.5.2 Neurological

8.4.5.3 Hearing Impairment

8.4.5.4 Others

8.4.6 Historic and Forecasted Market Size By End User

8.4.6.1 Hospitals

8.4.6.2 Ambulatory Surgical Centers (ASCs)

8.4.6.3 Specialized Clinics

8.4.6.4 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Active Implantable Medical Devices Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By Product Type

8.5.4.1 Pacemakers

8.5.4.2 Implantable Cardioverter Defibrillators (ICDs)

8.5.4.3 Neurostimulators

8.5.4.4 Ventricular Assist Devices (VADs)

8.5.4.5 Implantable Hearing Devices

8.5.4.6 Other

8.5.5 Historic and Forecasted Market Size By Application

8.5.5.1 Cardiac

8.5.5.2 Neurological

8.5.5.3 Hearing Impairment

8.5.5.4 Others

8.5.6 Historic and Forecasted Market Size By End User

8.5.6.1 Hospitals

8.5.6.2 Ambulatory Surgical Centers (ASCs)

8.5.6.3 Specialized Clinics

8.5.6.4 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Active Implantable Medical Devices Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By Product Type

8.6.4.1 Pacemakers

8.6.4.2 Implantable Cardioverter Defibrillators (ICDs)

8.6.4.3 Neurostimulators

8.6.4.4 Ventricular Assist Devices (VADs)

8.6.4.5 Implantable Hearing Devices

8.6.4.6 Other

8.6.5 Historic and Forecasted Market Size By Application

8.6.5.1 Cardiac

8.6.5.2 Neurological

8.6.5.3 Hearing Impairment

8.6.5.4 Others

8.6.6 Historic and Forecasted Market Size By End User

8.6.6.1 Hospitals

8.6.6.2 Ambulatory Surgical Centers (ASCs)

8.6.6.3 Specialized Clinics

8.6.6.4 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Active Implantable Medical Devices Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By Product Type

8.7.4.1 Pacemakers

8.7.4.2 Implantable Cardioverter Defibrillators (ICDs)

8.7.4.3 Neurostimulators

8.7.4.4 Ventricular Assist Devices (VADs)

8.7.4.5 Implantable Hearing Devices

8.7.4.6 Other

8.7.5 Historic and Forecasted Market Size By Application

8.7.5.1 Cardiac

8.7.5.2 Neurological

8.7.5.3 Hearing Impairment

8.7.5.4 Others

8.7.6 Historic and Forecasted Market Size By End User

8.7.6.1 Hospitals

8.7.6.2 Ambulatory Surgical Centers (ASCs)

8.7.6.3 Specialized Clinics

8.7.6.4 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Implantable Medical Devices Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 122.63 Billion |

|

Forecast Period 2024-32 CAGR: |

9.00% |

Market Size in 2032: |

USD 266.33 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Biomaterial |

|

||

|

By End Use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||