Hyaluronic Acid-based Dermal Fillers Market Overview

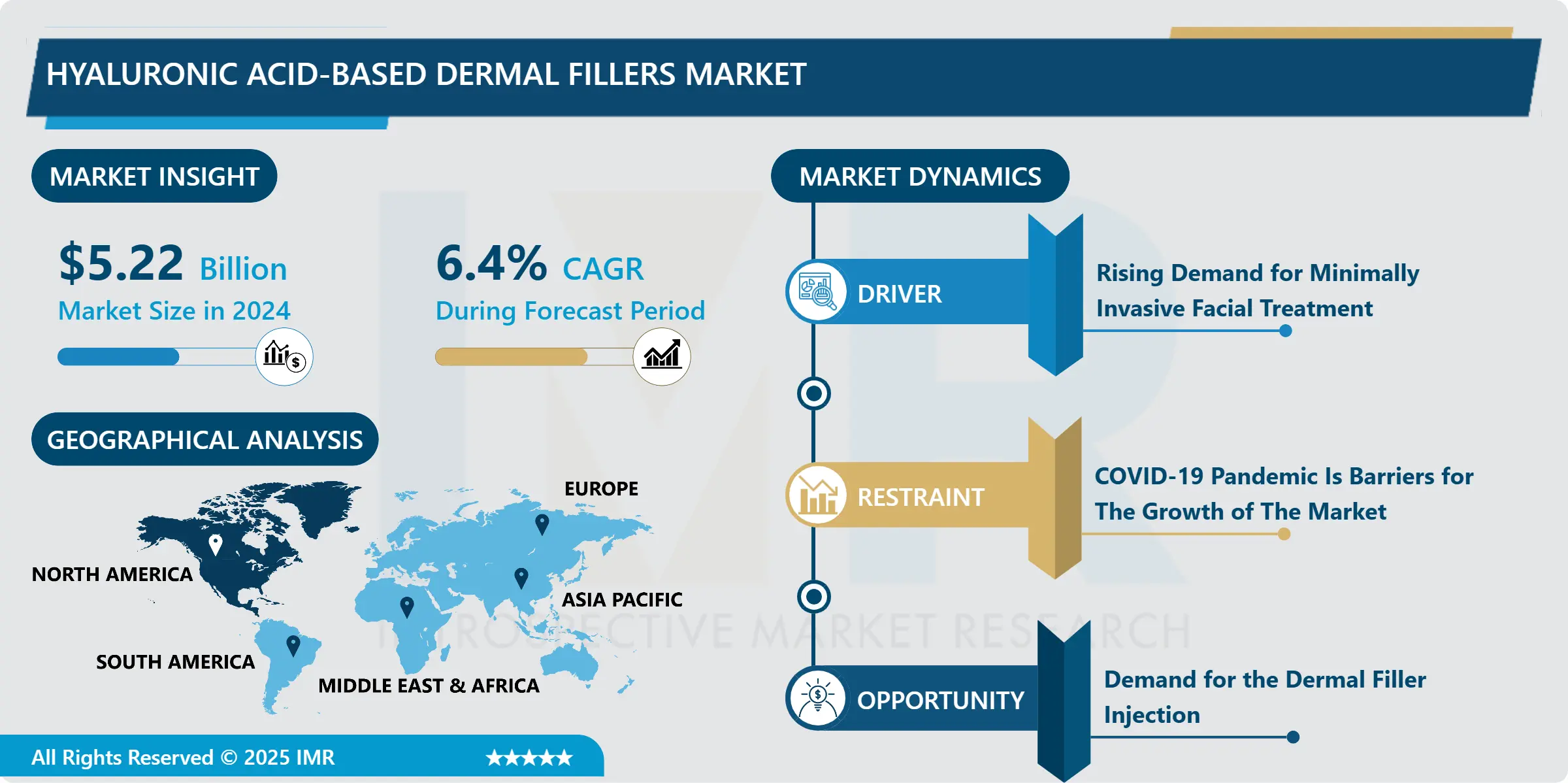

Global Hyaluronic Acid-based Dermal Fillers Market Size Was Valued at USD 5.22 Billion in 2024 and is Projected to Reach USD 10.33 Billion by 2035, Growing at A CAGR of 6.4 % From 2025 to 2035.

Dermal fillers based on hyaluronic acid, also known as hyaluronan, are made from a clear material produced naturally in the human body. Hyaluronic acid is a form of sugar (polysaccharide) found in bodily tissues like skin and cartilage. When in gel form, it can react with water and swell, giving it a smoothing/filling effect. Bacteria or rooster combs are two sources of hyaluronic acid utilized in dermal fillers (avian). Hyaluronic acid used in dermal fillers is sometimes chemically changed (crosslinked) to extend its life in the body. This material's effects last for about 6 to 12 months. This acid is also a humectant, which means it may retain moisture: In water, it can bind up to 1,000 times its volume. Its capacity to pull in and retain water enhances the volumizing impact while also adding hydration, making it a tempting treatment as a dermal filler. To restore lost volume, smooth wrinkles and fine lines, and increase volume and plumpness, hyaluronic acid fillers are injected into the skin with a needle or cannula. The effects of the treatment might be seen right away.

Dermal fillers are injectable procedures that help reduce the appearance of lines, wrinkles, and furrows caused by aging. They can also revitalize the face by adding volume to the lips, cheeks, chin, and other areas. Because of its adaptability, efficacy, and lack of side effects, hyaluronic acid is a preferred choice among injectable fillers. Existing market players are focused on constant innovation and up-gradation of their product portfolio with new and efficient product offerings to provide patients with better and more accurate aesthetic outcomes. The increasing desire for aesthetic beauty, driven by the less-invasive nature of the treatments and the increasing efficiency of hyaluronic acid-based dermal fillers, is one of the key factors driving the global hyaluronic acid-based dermal fillers market.

Market Dynamics And Factors For Hyaluronic Acid-based Dermal Fillers Market

Drivers:

Rising Demand for Minimally Invasive Facial Treatment

- Considering the developments in cosmetic treatments, a growing number of consumers are opting for operations that are less invasive and less unpleasant. In comparison to Botox, which lasts three to six months, the effects of hyaluronic acid dermal fillers can last for six to twelve months. Consumers prefer hyaluronic acid fillers to alternative injectables for cosmetic and aesthetic treatments because they have fewer side effects and last longer. Facial rejuvenation treatments have come a long way from equipment-based procedures, from minimally invasive injectables to non-invasive topical skin treatments, further complementing the growing adoption of facial rejuvenation treatments among patients with specific cosmetic concerns, the most common of which is anti-aging.

Growing Infrastructure Development Across Developing Countries

- During the projected period, the market for Hyaluronic Acid-based Dermal Fillers will be supported by an expanding network of healthcare institutions that provide advanced aesthetic treatments and improved infrastructure. In recent years, both industrialized and developing countries have seen a considerable increase in the number of facilities such as clinics, medical spas, and rejuvenation centers. As a result, the business will increase due to the fast adoption of various non-invasive therapies given by these facilities, which have advantages such as cost-effectiveness and shorter treatment times. Furthermore, the growing number of trained experts, such as dermatologists, will help the business grow even faster.

Restraints:

COVID-19 Pandemic Is Barriers for The Growth of The Market

- Due to restrictions on movement and lockdown in the majority of locations around the world, the pandemic has had a stronger influence on aesthetic medicine and cosmetic dermatology. Furthermore, as economies have slowed, discretionary spending has decreased, limiting customers' ability to undergo costly aesthetic operations. The market for Hyaluronic Acid-based Dermal Fillers have been constrained since the number of cosmetic treatments has decreased. However, market recovery will be aided by high demand and accompanying drop of COVID-19 instances.

Opportunities:

Demand for the Dermal Filler Injection

- The unique location is the number one reason patients seek dermal filler injections, according to a recent assessment by plastic surgeons. Puffiness and darker skin beneath the eyes make us appear exhausted, and no amount of pricey lotions or serums will usually help. Hyaluronic Acid-based Dermal Fillers, on the other hand, can help provide volume to depressed eye regions and alleviate puffiness. The results are natural-looking, long-lasting, and instantaneous, as with other dermal filler injections.

- Dermal Fillers based on hyaluronic acid have always been popular for cheeks, but today's popular cheek fillers are far more natural-looking. Patients wanting cheek dermal filler injections are more likely to request a subtle look, such as filling in parts of the cheeks that have flattened with time or giving the appearance of higher cheekbones. Dermal filler injections, a relatively new kid on the block, are gaining favor among patients wishing to sculpt their faces with modest modifications. Dermal Fillers based on Hyaluronic Acid are highly successful at making modest alterations in the angularity of the jawline for a sophisticated style that's gaining popularity.

Segmentation Analysis of Hyaluronic Acid-based Dermal Fillers Market

- By Product, the single-phase fillers segment is anticipated to observe profitable growth due to different applications in skin and facial aesthetic procedures, comparatively fewer side effects, and rapid technological development for emerging new fillers. Dermatologists and customers favor single-phase solutions for the treatment of soft tissue facial abnormalities because the uncross-linked HA promotes elastin and collagen production, giving the face a youthful and healthy-looking shine. Single-phase goods do not go through the sizing technique, which breaks down the gel, throughout the production process. In the production of single-phase dermal fillers like Juvederm Ultra, Hylacross technology is used, resulting in product life and desirable effects.

- By Application, the lip augmentation segment is anticipated to hold the largest Hyaluronic Acid-based Dermal Fillers market share throughout the forecast period. Dermal Fillers based on hyaluronic acid are widely utilized for lip augmentation operations around the world. It should be noted that hyaluronic acid aids in the volume increase of the lips. First-time filler patients are frequently prescribed hyaluronic acid-based dermal fillers. The duration of these fillers is usually 6 to 18 months. Hyaluronic Acid fillers also provide the lips form, volume, and structure, which is why they are so popular. During the projection period, such factors are expected to boost the segment's expansion.

- By End-User, Specialty & Dermatology Clinics segment is expected to dominate the Hyaluronic Acid-based Dermal Fillers market over the forecast period. Over the projected period, advancements in hyaluronic acid-based dermal filler technologies for wrinkle treatment, together with rising spending on cosmetic operations, are expected to drive market expansion.

Regional Analysis of Hyaluronic Acid-based Dermal Fillers Market

- With its well-established healthcare infrastructure, favorable policies, and the growing number of plastic surgery treatments, North America is expected to have a considerable market share. The United States has the biggest number of plastic surgeons (7,009) in the world, according to the International Society of Aesthetic Plastic Surgery. In 2018, 17.7 million surgical and minimally invasive plastic surgery procedures were performed in the United States, according to the American Society of Plastic Surgeons. Furthermore, the widespread use of plastic surgery and minimally invasive plastic surgery methods is predicted to stimulate regional development.

- The rise in awareness of hyaluronic acid-based dermal fillers and the increasing demand for aesthetics in emerging nations such as India and China are propelling growth in the hyaluronic acid-based dermal fillers market in Asia Pacific region during the forecast period. New goods are being launched in nations like China and India as a result of the methods utilized by important market leaders. Due to the availability of sophisticated hyaluronic acid-based dermal fillers and the high proportion of the senior population in Japan, there is a significant demand for these dermal fillers.

- Factors such as a rapidly aging population and increased public knowledge of advanced aesthetic procedures are driving the European industry. The Russian dermal fillers market is being boosted by increased demand for minimally invasive procedures, the rising use of non-surgical dermal fillers, and the commercialization of novel interventional solutions. Over the projection period, the Russian market is expected to rise steadily. The country's sales are predicted to grow because of an aging population and the widespread use of hyaluronic acid-based dermal fillers. Growth in the German market has been enabled by the introduction of new products and the development of distribution.

- Brazil, Mexico, Argentina, Colombia, Chile, Peru, and the Rest of South America make up the market for hyaluronic acid-based dermal fillers in South America. Over the projection period, the market in Brazil is expected to hold the greatest market share among these nations. The increasing availability of diverse filler choices, as well as the increased desire for non-surgical procedures, can be contributed to the market's rise in the country. Furthermore, the increased awareness of skin tightening procedures among the country's aging population is expected to add to the market's growth in Brazil. According to World Bank figures, the number of people aged 65 and more in the country climbed from 9,175,089 in 2000 to 19,525,475 in 2019.

Players Covered in Hyaluronic Acid-based Dermal Fillers Market are

- Sinclair Pharma (UK)

- ALLERGAN (Ireland)

- Merz Pharma (Germany)

- Suneva Medical (US)

- Galderma Laboratories (Canada)

- BioPlus Co.Ltd. (South Korea)

- Revance Therapeutics Inc (US)

- Bioxis pharmaceuticals (France)

- DR. Korman (Israel)

- Prollenium Medical Technologies (Canada)

- Anika Therapeutics Inc (US)

- SCULPT Luxury Dermal Fillers LTD (Czechia Republic)

- CANDELA CORPORATION (US)and other major players.

Key Industry Developments In Hyaluronic Acid-based Dermal Fillers Market

- In January 2023, Allergan Aesthetics (AbbVie, Inc.) announced the FDA approval of JUVÉDERM VOLBELLA XC in adults over the age of 21 to improve infraorbital hollows. With this approval, the company continues the expansion of its treatment portfolio to effectively address the needs of patients.

|

Global Hyaluronic Acid-based Dermal Fillers Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 5.22 Bn. |

|

Forecast Period 2025-35 CAGR: |

6.4 % |

Market Size in 2035: |

USD 10.33 Bn. |

|

Segments Covered: |

By Product |

|

|

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Hyaluronic Acid-Based Dermal Fillers Market by Product (2018-2035)

4.1 Hyaluronic Acid-Based Dermal Fillers Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Single Phase

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Duplex

Chapter 5: Hyaluronic Acid-Based Dermal Fillers Market by Application (2018-2035)

5.1 Hyaluronic Acid-Based Dermal Fillers Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cheek Augmentation

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Lip Augmentation

5.5 Wrinkle Correction

5.6 Nasolabial Folds

5.7 Scar Treatment

5.8 Restoration of Volume

5.9 Others

Chapter 6: Hyaluronic Acid-Based Dermal Fillers Market by End-User (2018-2035)

6.1 Hyaluronic Acid-Based Dermal Fillers Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Specialty & Dermatology Clinics

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Hospitals

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Hyaluronic Acid-Based Dermal Fillers Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ASCOM HOLDINGS

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 BAXTER INTERNATIONAL INC

7.4 BERNOULLI ENTERPRISE INC

7.5 CAPSULE TECHNOLOGIE (SUBSIDIARY OF QUALCOMM LIFE INC.)

7.6 CONNEXALL

7.7 DRAGERWERK AG

7.8 EXTENSION HEALTHCARE

7.9 GE HEALTHCARE

7.10 KONINKLIJKE PHILIPS N.V

7.11 MASIMO

7.12 MEDTRONIC

7.13 MINDRAY MEDICAL INTERNATIONAL LIMITED

7.14 MOBILE HEARTBEAT (SUBSIDIARY OF HOSPITAL CORPORATION OF AMERICA)

7.15 SPOK INC. (SUBSIDIARY OF SPOK HOLDINGS INC.)

7.16 VOCERA COMMUNICATIONS

Chapter 8: Global Hyaluronic Acid-Based Dermal Fillers Market By Region

8.1 Overview

8.2. North America Hyaluronic Acid-Based Dermal Fillers Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Product

8.2.4.1 Single Phase

8.2.4.2 Duplex

8.2.5 Historic and Forecasted Market Size by Application

8.2.5.1 Cheek Augmentation

8.2.5.2 Lip Augmentation

8.2.5.3 Wrinkle Correction

8.2.5.4 Nasolabial Folds

8.2.5.5 Scar Treatment

8.2.5.6 Restoration of Volume

8.2.5.7 Others

8.2.6 Historic and Forecasted Market Size by End-User

8.2.6.1 Specialty & Dermatology Clinics

8.2.6.2 Hospitals

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Hyaluronic Acid-Based Dermal Fillers Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Product

8.3.4.1 Single Phase

8.3.4.2 Duplex

8.3.5 Historic and Forecasted Market Size by Application

8.3.5.1 Cheek Augmentation

8.3.5.2 Lip Augmentation

8.3.5.3 Wrinkle Correction

8.3.5.4 Nasolabial Folds

8.3.5.5 Scar Treatment

8.3.5.6 Restoration of Volume

8.3.5.7 Others

8.3.6 Historic and Forecasted Market Size by End-User

8.3.6.1 Specialty & Dermatology Clinics

8.3.6.2 Hospitals

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Hyaluronic Acid-Based Dermal Fillers Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Product

8.4.4.1 Single Phase

8.4.4.2 Duplex

8.4.5 Historic and Forecasted Market Size by Application

8.4.5.1 Cheek Augmentation

8.4.5.2 Lip Augmentation

8.4.5.3 Wrinkle Correction

8.4.5.4 Nasolabial Folds

8.4.5.5 Scar Treatment

8.4.5.6 Restoration of Volume

8.4.5.7 Others

8.4.6 Historic and Forecasted Market Size by End-User

8.4.6.1 Specialty & Dermatology Clinics

8.4.6.2 Hospitals

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Hyaluronic Acid-Based Dermal Fillers Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Product

8.5.4.1 Single Phase

8.5.4.2 Duplex

8.5.5 Historic and Forecasted Market Size by Application

8.5.5.1 Cheek Augmentation

8.5.5.2 Lip Augmentation

8.5.5.3 Wrinkle Correction

8.5.5.4 Nasolabial Folds

8.5.5.5 Scar Treatment

8.5.5.6 Restoration of Volume

8.5.5.7 Others

8.5.6 Historic and Forecasted Market Size by End-User

8.5.6.1 Specialty & Dermatology Clinics

8.5.6.2 Hospitals

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Hyaluronic Acid-Based Dermal Fillers Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Product

8.6.4.1 Single Phase

8.6.4.2 Duplex

8.6.5 Historic and Forecasted Market Size by Application

8.6.5.1 Cheek Augmentation

8.6.5.2 Lip Augmentation

8.6.5.3 Wrinkle Correction

8.6.5.4 Nasolabial Folds

8.6.5.5 Scar Treatment

8.6.5.6 Restoration of Volume

8.6.5.7 Others

8.6.6 Historic and Forecasted Market Size by End-User

8.6.6.1 Specialty & Dermatology Clinics

8.6.6.2 Hospitals

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Hyaluronic Acid-Based Dermal Fillers Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Product

8.7.4.1 Single Phase

8.7.4.2 Duplex

8.7.5 Historic and Forecasted Market Size by Application

8.7.5.1 Cheek Augmentation

8.7.5.2 Lip Augmentation

8.7.5.3 Wrinkle Correction

8.7.5.4 Nasolabial Folds

8.7.5.5 Scar Treatment

8.7.5.6 Restoration of Volume

8.7.5.7 Others

8.7.6 Historic and Forecasted Market Size by End-User

8.7.6.1 Specialty & Dermatology Clinics

8.7.6.2 Hospitals

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Hyaluronic Acid-based Dermal Fillers Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 5.22 Bn. |

|

Forecast Period 2025-35 CAGR: |

6.4 % |

Market Size in 2035: |

USD 10.33 Bn. |

|

Segments Covered: |

By Product |

|

|

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||