Hospital Beds Market Synopsis:

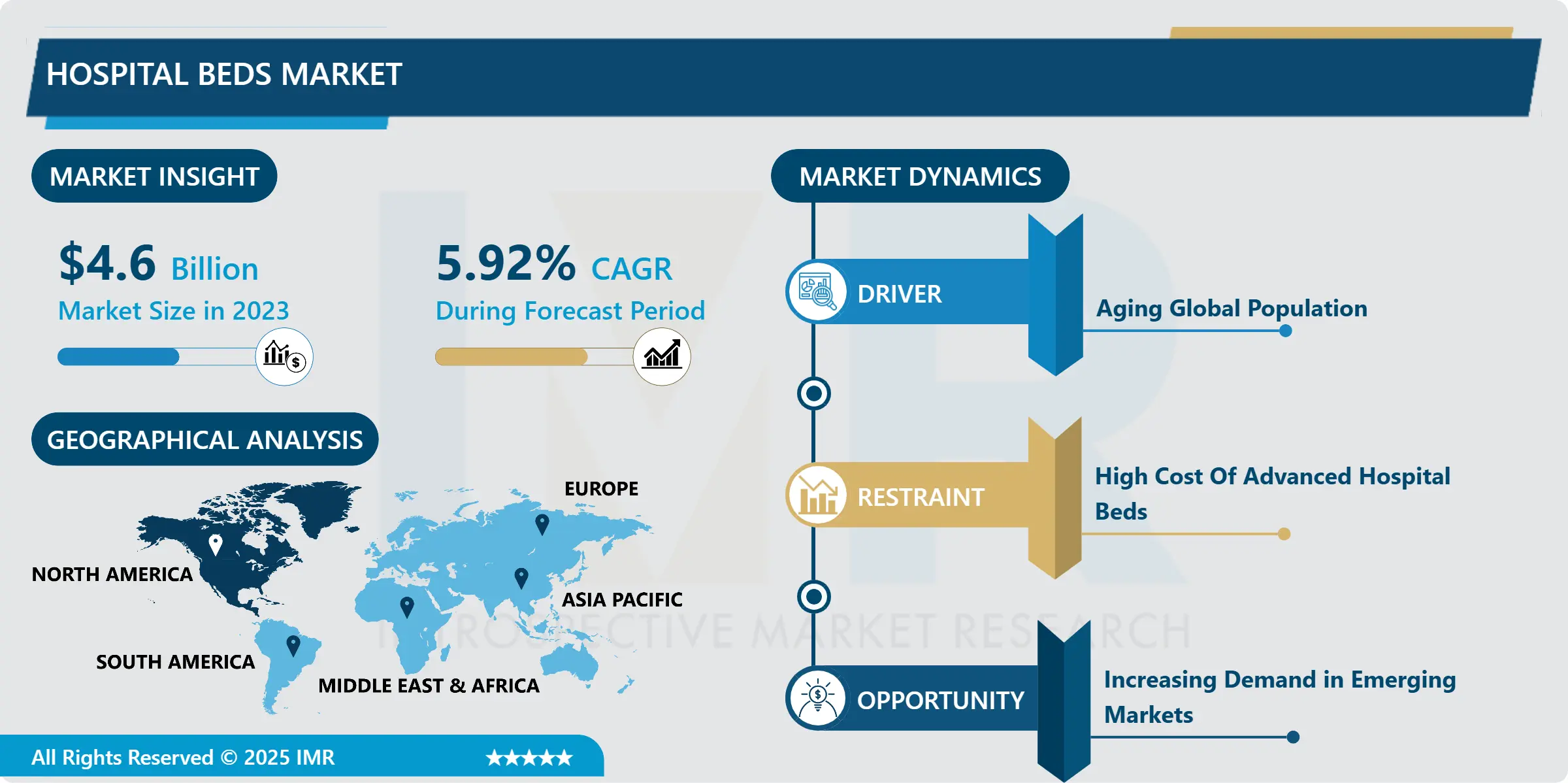

Hospital Beds Market Size Was Valued at USD 4.6 Billion in 2023, and is Projected to Reach USD 7.7 Billion by 2032, Growing at a CAGR of 5.92% From 2024-2032.

Hospital beds industry is defined by the market of a wide range of types of products used in medical institutions including hospitals, nursing homes and rehabilitation centers. These beds have been developed to enhance the delivery of patient care by depth, safety and functionality when receiving medical treatment or recovering. Specialised general, pediatric, birthing, bariatric and pressure relief beds meet various patient requirements.

Many factors have contributed to this growth; they include; the increasing health care expenditure across the global, increased incidence of chronic diseases, and the ageing population across the globe. Standard hospital beds: These are what most patients expect in a healthcare facility today given the improvement of health care technology to cater for every patient’s comfort and safety, hospital beds can be adjusted to different heights and tilts with pressure reducing surfaces for easy mobility. Other innovations that concern smart hospital beds with sensors incorporated making a significant contribution in the market.

The growth in lifestyle diseases, coupled with the rise in the number of hospitals, healthcare facilities, and long-term care centers world over has also contributed to the rise of demand for hospital beds. As for the factors, the menace of the rise in various diseases has lead to a need for specialized care especially in such field as bariatrics, pediatrics and maternity. Furthermore, growing obesity rates have boosted the bariatric patients and pressure relief beds needed for bed-ridden patients in drive the market. The Covid 19 need for beds that particular year saw a rise due to the pandemic increasing the short term demand for both general and ICU beds.

Hospital Beds Market Trend Analysis:

Smart Hospital Beds

-

The most remarkable market trend has been the ability of smart technology to be incorporated in hospital beds. These high enhance bed has sensor, monitoring system, and IoT perspectives with the aim to enhance the patient care and even hospital. There are specific intelligent hospital beds, which can monitor the patient’s vital signs and his shifts through the night and report them to the healthcare givers in real time if anything abnormal was noted. What the smart beds produce are data that can be easily fed into the EHRs to give a picture of a patient’s health and progress. It increases efficiency of patient’s flow, decreases possibilities of mistakes and brings the benefit to patients.

- Another important factor of this trend is the utilization of the hospital bed to improve comfort and solve hospital associated complications. For example, electrical pressure mattresses help to decrease the chances of pressure sores for the immobile patients. Moreover, adjustable beds can offer, for instance, patients the opportunity to get into different positions within the human body which would help in their healing process hence better recovery is expected. This move toward smart and connected hospital beds is expected to gain further momentum because several connected health systems are already being developed.

Increasing Demand in Emerging Markets

-

One such strategic opportunity highly relevant for the hospital beds market is the need for escalation of the healthcare industries, particularly in the developing nations. Asia-Pacific, Latin American and African countries largely relate to the improved economic condition and realizing healthcare requirements with increased consumption on healthcare sector. So, when these regions develop more establishments of hospitals and health care facilities, the need for hospital beds is expected to increase greatly. National and other stakeholders in these regions are putting up more resources to expand health care services to the population and this include hospital beds.

- In addition to the problem presented by the growing emergent market healthcare requirements, it is not simply about the demand for more beds, but also for pediatric, maternity and bariatric specific beds among others – making it a dynamic market. These changes are seen as a major opportunity in the sense that manufacturers can improve their portfolios and target the healthcare needs of those areas. Companies can achieve additional growth by offering new markets cost effective and high quality hospital beds specifically designed for those markets.

Hospital Beds Market Segment Analysis:

Hospital Beds Market is Segmented on the basis of Type, Usage, Application, End User, and Region.

By Type, General Beds segment is expected to dominate the market during the forecast period

-

The hospital beds can be segmented based on the type, which includes a particular type of hospital bed for particular patients. Open or general beds are the most common types of used in the hospitals for patients who may not need intensive care. These are reclining beds with adjustable positions to allow comfort all through for treatment. Individualized beds are specialized for children with lesser dimensions and characteristics that are safeguarding and comfortable for children during treatment. Maternity beds, also known as birth or delivery beds, are designed for use in obstetrical wards as patients’ comfort during labor and delivery is important and beds can be adjusted for ease of use by both patient and health care attendant.

- Bariatric beds are further constructed to be used for the fatty people; these are built to have more weight capacity as well as wider structures to hold inappropriate sizes of bed sizes other than the usual bed sizes. Pressure relief beds, on the other hand, are those beds that are useful for patients who are confined to their bed for most of their time in order to avoid development of pressure ulcers also called bedsores. These beds have components such as the surface adjustability and aeration to minimize load on the body. The usage of each variant is directly proportional to the age, gender, and chronic illnesses of the patient population and the need of the healthcare facility.

By Application, Acute Care segment expected to held the largest share

-

The hospital beds can also be split by the application which encompasses being used in general medical care, Intensive care, maternity and bariatric care among others. In general medical care, hospital beds involve admission of patients of diverse nature with different ailments that need to receive treatment. These beds are basic or self-adjustable with position altering options for the comfort and support of the patient. Related to any Intensive Care Units (ICU), the use of electric or fully adjustable beds are necessary to give special care to patents with complicated health conditions. The features that come with these beds include alarm systems, which help nurse monitor their comfort, and modify the positions frequently as needed.

- In segments of care such as maternity and pediatrics, beds are designed to have certain factors such as birthing positions, or something child friendly about them to allow for comfort and safety. Bariatric beds on the other hand are used in hospitals and other care centers serving the massively sized obese patients and consists of wider frames and much higher weight bearing abilities. Pressure relief beds are also utilised within long-term care or palliative care to allow the patient to be comfortable, especially those with reduced mobility or those who are at high risk for pressure ulcers.

Hospital Beds Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

The geographical segment analysis of the global hospital beds market identifies North America to be experiencing high growth, mainly due to the well-developed healthcare system, healthy spending on healthcare sectors and increasing demand for other than standard beds. Due to the region’s improving healthcare standards especially in United States, ongoing innovation to meet elderly demands create demand for hospitals and related technologies including smart, bariatric, and pressure relief beds. Also, many industry stakeholders are located in the region, and they invest in technology and innovation that enhance development in the region, particularly North America.

- Additionally, increasing focus on policies and governmental governance in the successful delivery of health services has also led to market growth in North America. Focus on quality care, comfort and safety of patients, and diminishing healthcare related risks have inclined more usage of advanced technologies in hospital bed. Considering the dynamics of development of the healthcare industry in North America, it is further predicted that it will continue to dominate the market of hospital beds throughout the world.

Active Key Players in the Hospital Beds Market:

-

Stryker Corporation (USA)

- Hill-Rom Holdings, Inc. (USA)

- Invacare Corporation (USA)

- Arjo AB (Sweden)

- Linet spol. s r.o. (Czech Republic)

- Paramount Bed Holdings Co. Ltd. (Japan)

- Medtronic (Ireland)

- SAMMONS PRESTON (USA)

- KAWASAKI (Japan)

- Gendron Inc. (USA)

- Merits Health Products Inc. (USA)

- Drive DeVilbiss Healthcare (USA)

- Other Active Players

Key Industry Developments in the Hospital Beds Market:

-

June 2024: Noida International Institute of Medical Sciences (NIIMS) Hospital revealed a significant expansion of its hospital bed capacity within the past year, from 450 to over 750. This remarkable achievement will enhance accessibility to healthcare services for both urban and rural populations. The hospital aims to provide affordable and comprehensive medical care to all patients.

- February 2023: GMG Medical Equipment in San Diego supported hospitals by providing commercial-grade medical beds for outpatient care and people coming out of the hospital.

|

Global Hospital Beds Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 4.6 Billion |

|

Forecast Period 2024-32 CAGR: |

5.92% |

Market Size in 2032: |

USD 7.7 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Usage |

|

||

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Hospital Beds Market by Type

4.1 Hospital Beds Market Snapshot and Growth Engine

4.2 Hospital Beds Market Overview

4.3 General Beds

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 General Beds: Geographic Segmentation Analysis

4.4 Pediatric Beds

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Pediatric Beds: Geographic Segmentation Analysis

4.5 Birthing Beds

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Birthing Beds: Geographic Segmentation Analysis

4.6 Bariatric Beds

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Bariatric Beds: Geographic Segmentation Analysis

4.7 Pressure Relief Beds

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Pressure Relief Beds: Geographic Segmentation Analysis

Chapter 5: Hospital Beds Market by Application

5.1 Hospital Beds Market Snapshot and Growth Engine

5.2 Hospital Beds Market Overview

5.3 Acute Care

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Acute Care: Geographic Segmentation Analysis

5.4 Long-term Care

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Long-term Care: Geographic Segmentation Analysis

5.5 Critical Care

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Critical Care: Geographic Segmentation Analysis

Chapter 6: Hospital Beds Market by Usage

6.1 Hospital Beds Market Snapshot and Growth Engine

6.2 Hospital Beds Market Overview

6.3 Electric Beds

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Electric Beds: Geographic Segmentation Analysis

6.4 Semi-electric Beds

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Semi-electric Beds: Geographic Segmentation Analysis

6.5 Manual Beds

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Manual Beds: Geographic Segmentation Analysis

Chapter 7: Hospital Beds Market by End User

7.1 Hospital Beds Market Snapshot and Growth Engine

7.2 Hospital Beds Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.3.3 Key Market Trends, Growth Factors and Opportunities

7.3.4 Hospitals: Geographic Segmentation Analysis

7.4 Home Care Settings

7.4.1 Introduction and Market Overview

7.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.4.3 Key Market Trends, Growth Factors and Opportunities

7.4.4 Home Care Settings: Geographic Segmentation Analysis

7.5 Elderly Care Facilities

7.5.1 Introduction and Market Overview

7.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.5.3 Key Market Trends, Growth Factors and Opportunities

7.5.4 Elderly Care Facilities: Geographic Segmentation Analysis

7.6 Ambulatory Surgical Centers (ASCs))

7.6.1 Introduction and Market Overview

7.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.6.3 Key Market Trends, Growth Factors and Opportunities

7.6.4 Ambulatory Surgical Centers (ASCs)) : Geographic Segmentation Analysis

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Hospital Beds Market Share by Manufacturer (2023)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 STRYKER CORPORATION (USA)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 HILL-ROM HOLDINGS INC. (USA)

8.4 INVACARE CORPORATION (USA)

8.5 ARJO AB (SWEDEN)

8.6 LINET SPOL. S R.O. (CZECH REPUBLIC)

8.7 PARAMOUNT BED HOLDINGS CO. LTD. (JAPAN)

8.8 MEDTRONIC (IRELAND)

8.9 SAMMONS PRESTON (USA)

8.10 KAWASAKI (JAPAN)

8.11 GENDRON INC. (USA)

8.12 MERITS HEALTH PRODUCTS INC. (USA)

8.13 DRIVE DEVILBISS HEALTHCARE (USA)

8.14 OTHER ACTIVE PLAYERS

Chapter 9: Global Hospital Beds Market By Region

9.1 Overview

9.2. North America Hospital Beds Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size By Type

9.2.4.1 General Beds

9.2.4.2 Pediatric Beds

9.2.4.3 Birthing Beds

9.2.4.4 Bariatric Beds

9.2.4.5 Pressure Relief Beds

9.2.5 Historic and Forecasted Market Size By Application

9.2.5.1 Acute Care

9.2.5.2 Long-term Care

9.2.5.3 Critical Care

9.2.6 Historic and Forecasted Market Size By Usage

9.2.6.1 Electric Beds

9.2.6.2 Semi-electric Beds

9.2.6.3 Manual Beds

9.2.7 Historic and Forecasted Market Size By End User

9.2.7.1 Hospitals

9.2.7.2 Home Care Settings

9.2.7.3 Elderly Care Facilities

9.2.7.4 Ambulatory Surgical Centers (ASCs))

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Hospital Beds Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size By Type

9.3.4.1 General Beds

9.3.4.2 Pediatric Beds

9.3.4.3 Birthing Beds

9.3.4.4 Bariatric Beds

9.3.4.5 Pressure Relief Beds

9.3.5 Historic and Forecasted Market Size By Application

9.3.5.1 Acute Care

9.3.5.2 Long-term Care

9.3.5.3 Critical Care

9.3.6 Historic and Forecasted Market Size By Usage

9.3.6.1 Electric Beds

9.3.6.2 Semi-electric Beds

9.3.6.3 Manual Beds

9.3.7 Historic and Forecasted Market Size By End User

9.3.7.1 Hospitals

9.3.7.2 Home Care Settings

9.3.7.3 Elderly Care Facilities

9.3.7.4 Ambulatory Surgical Centers (ASCs))

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Hospital Beds Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size By Type

9.4.4.1 General Beds

9.4.4.2 Pediatric Beds

9.4.4.3 Birthing Beds

9.4.4.4 Bariatric Beds

9.4.4.5 Pressure Relief Beds

9.4.5 Historic and Forecasted Market Size By Application

9.4.5.1 Acute Care

9.4.5.2 Long-term Care

9.4.5.3 Critical Care

9.4.6 Historic and Forecasted Market Size By Usage

9.4.6.1 Electric Beds

9.4.6.2 Semi-electric Beds

9.4.6.3 Manual Beds

9.4.7 Historic and Forecasted Market Size By End User

9.4.7.1 Hospitals

9.4.7.2 Home Care Settings

9.4.7.3 Elderly Care Facilities

9.4.7.4 Ambulatory Surgical Centers (ASCs))

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Hospital Beds Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size By Type

9.5.4.1 General Beds

9.5.4.2 Pediatric Beds

9.5.4.3 Birthing Beds

9.5.4.4 Bariatric Beds

9.5.4.5 Pressure Relief Beds

9.5.5 Historic and Forecasted Market Size By Application

9.5.5.1 Acute Care

9.5.5.2 Long-term Care

9.5.5.3 Critical Care

9.5.6 Historic and Forecasted Market Size By Usage

9.5.6.1 Electric Beds

9.5.6.2 Semi-electric Beds

9.5.6.3 Manual Beds

9.5.7 Historic and Forecasted Market Size By End User

9.5.7.1 Hospitals

9.5.7.2 Home Care Settings

9.5.7.3 Elderly Care Facilities

9.5.7.4 Ambulatory Surgical Centers (ASCs))

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Hospital Beds Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size By Type

9.6.4.1 General Beds

9.6.4.2 Pediatric Beds

9.6.4.3 Birthing Beds

9.6.4.4 Bariatric Beds

9.6.4.5 Pressure Relief Beds

9.6.5 Historic and Forecasted Market Size By Application

9.6.5.1 Acute Care

9.6.5.2 Long-term Care

9.6.5.3 Critical Care

9.6.6 Historic and Forecasted Market Size By Usage

9.6.6.1 Electric Beds

9.6.6.2 Semi-electric Beds

9.6.6.3 Manual Beds

9.6.7 Historic and Forecasted Market Size By End User

9.6.7.1 Hospitals

9.6.7.2 Home Care Settings

9.6.7.3 Elderly Care Facilities

9.6.7.4 Ambulatory Surgical Centers (ASCs))

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Hospital Beds Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size By Type

9.7.4.1 General Beds

9.7.4.2 Pediatric Beds

9.7.4.3 Birthing Beds

9.7.4.4 Bariatric Beds

9.7.4.5 Pressure Relief Beds

9.7.5 Historic and Forecasted Market Size By Application

9.7.5.1 Acute Care

9.7.5.2 Long-term Care

9.7.5.3 Critical Care

9.7.6 Historic and Forecasted Market Size By Usage

9.7.6.1 Electric Beds

9.7.6.2 Semi-electric Beds

9.7.6.3 Manual Beds

9.7.7 Historic and Forecasted Market Size By End User

9.7.7.1 Hospitals

9.7.7.2 Home Care Settings

9.7.7.3 Elderly Care Facilities

9.7.7.4 Ambulatory Surgical Centers (ASCs))

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Hospital Beds Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 4.6 Billion |

|

Forecast Period 2024-32 CAGR: |

5.92% |

Market Size in 2032: |

USD 7.7 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Usage |

|

||

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||