Healthcare Simulators Market Synopsis:

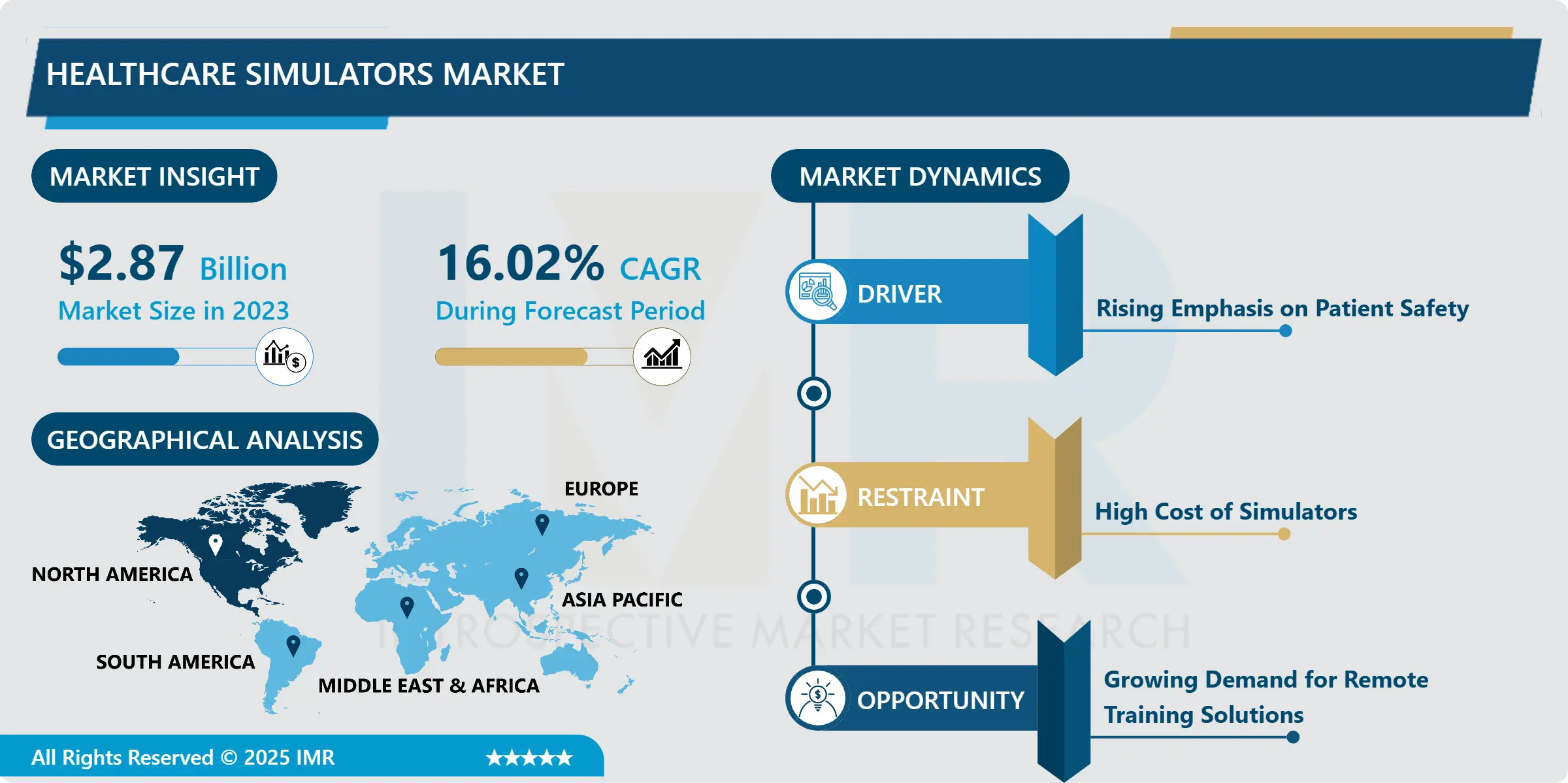

Healthcare Simulators Market Size Was Valued at USD 2.87 Billion in 2023, and is Projected to Reach USD 10.93 Billion by 2032, Growing at a CAGR of 16.02% From 2024-2032.

The Healthcare Simulators Market refers to the technologies and devices for mimicking real-life medical practice settings for training, education, and assessment. It provides healthcare professionals and students with an environment in which procedures and decision-making skills can be practiced without risk to improve competency and the quality of care given to patients.

This market for Healthcare Simulators has experienced massive growth in the last few years and is based on a growing need for quality healthcare education coupled with concern over rampant medical error rates. These simulators are used highly in medical schools, nursing institutions, and hospitals to simulate real-life healthcare scenarios such as surgical procedures, patient interactions, and diagnostic processes. It covers a wide expanse of healthcare domains including patient care, surgery, emergency response, and diagnostics.

With the increasing intricacy of health-care procedures and rapid changes in technological advances within medicine, institutions have been challenged to incorporate simulation-based learning. Simulations expose professionals to hands-on practice without putting a patient's safety at risk. In medical education, simulators in healthcare provide students and practitioners with the chance to hone their skills in the absence of a direct interaction with the patients. This is especially so because healthcare systems all over the world keep demanding more patient safety and better quality of care delivery.

The market is also very highly technologically innovative. It has the new high-fidelity patient mannequin, 3D visualization tools, and augmented/virtual reality capabilities. These allow them to experience real-like scenarios and handle complex medical cases. The other breakthrough has come in the form of the inclusion of AI in simulators, which enables tailoring to a user's performance. Though growing promisingly, it also presents some challenges in the form of high costs of simulators and the specific training instructors for effective sessions.

Healthcare Simulators Market Trend Analysis:

Integration of Virtual Reality (VR) and Augmented Reality (AR)

- One of the main trends within the Healthcare Simulators Market involves integration of virtual and augmented reality within the learning process. Such technologies are successful in encouraging an immersive experience: for instance, trainees could interact with virtual patients, anatomical models, or real-time feedback while in a controlled environment. Indeed, VR and AR simulators allow for real-life medical scenarios, therefore allowing professionals the chance to gain practical experience without running any physical risks.

- It is with the potential of making possible the imitation of complex surgical operations and medical interventions that the use of VR and AR is fast expanding. For instance, a surgeon can utilize AR glasses to put on the body of a patient overlays of anatomical structures that will guide him or her to conduct complex surgeries. Medical students have the advantage of using VR headsets for training in diagnostics or surgery on a virtual "real" environment. This will change the face of medical training delivery and bring about more engagement in more efficient learning.

Growing Demand for Remote Training Solutions

- Offering remote training solutions has been a huge opportunity for the Healthcare Simulators Market. Geographical and logistical challenges associated with healthcare institutions and medical schools result in a need for effective training that can be delivered from a distance. Indeed, this need has escalated during and subsequent to the COVID-19 pandemic, where online education became critical to ensure that medical training could continue uninterrupted.

- New, cloud-based platforms and virtual training environments offer institutions the possibility to train beyond traditional classroom settings through remote healthcare simulators. Because there is already advanced simulation technology-the virtual reality and interactive learning platform-healthcare professionals can be trained practically from anywhere. That opens up new opportunities for companies that offer these solutions to expand to a wider customer base and increase their market share.

Healthcare Simulators Market Segment Analysis:

Healthcare Simulators Market is Segmented on the basis of Product type, Technology, Application, End User, and Region

By Product Type, Patient Simulators segment is expected to dominate the market during the forecast period

- This market is categorized based on product type into patient simulators, surgical simulators, dental simulators, ultrasound simulators, and eye simulators. The patient simulators hold the largest market share because this system is increasingly used in most healthcare training setups. Starting from simple mannequins to high-fidelity systems with capabilities to simulate real physiological activities, patient simulators are versatile to be used in any medical setting.

- Other popular masses are being achieved through surgical simulators. Advances in minimal invasive surgeries, complex procedures, and the need for safe simulation tools for training medical professionals require surgical simulators. These simulators help surgeons cultivate skills before conducting real surgeries, which leads to reducing complications and error.

By Application, Diagnostics segment expected to held the largest share

- The Healthcare Simulators Market is classified on the basis of product type as patient simulators, surgical simulators, dental simulators, ultrasound simulators, and eye simulators. Of these, patient simulators are the dominating ones as they find applications in nearly all types of healthcare training environments. Ranging from the most simple mannequins to ultra-complex systems mimicking real physiological response, patient simulators can be said to be highly versatile in their use for healthcare education purposes.

- Surgical simulators are also gaining considerable mileage. The advancement in minimally invasive surgeries and complicated procedures underscores the demand for surgical simulation tools to be used in training medical professionals in controlled and safe environments. It allows the surgeon to hone his skills through practice before conducting actual operations, reducing the risks of complications and errors.

Healthcare Simulators Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- The healthcare simulators' current market leader is North America, primarily because of the advanced healthcare setup in the region as well as a strong education focus related to medical science. As simulation-based training was highly adopted by many medical schools and healthcare institutions in the region, this position was held by the United States ever since.

- The region has been motivated by the local presence of major healthcare simulators manufacturers and access to advanced technologies, including virtual reality and AI-based simulation tools. North America's interest in patient safety and the need to minimize errors in healthcare has increased demands for developing high-fidelity simulators to enhance healthcare programs.

Active Key Players in the Healthcare Simulators Market:

- Laerdal Medical (Norway)

- CAE Healthcare (Canada)

- Gaumard Scientific (USA)

- 3D Systems (USA)

- Simulab Corporation (USA)

- Mentice AB (Sweden)

- Kyoto Kagaku (Japan)

- Limbs & Things (UK)

- SynBone AG (Switzerland)

- Surgical Science Sweden AB (Sweden)

- Intelligent Ultrasound (UK)

- Medaphor Group (UK)

- Other Active Players

|

Global Healthcare Simulators Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.87 Billion |

|

Forecast Period 2024-32 CAGR: |

16.02% |

Market Size in 2032: |

USD 10.93 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Technology |

|

||

|

By End User |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Healthcare Simulators Market by Product Type

4.1 Healthcare Simulators Market Snapshot and Growth Engine

4.2 Healthcare Simulators Market Overview

4.3 Patient Simulators

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Patient Simulators: Geographic Segmentation Analysis

4.4 Surgical Simulators

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Surgical Simulators: Geographic Segmentation Analysis

4.5 Dental Simulators

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Dental Simulators: Geographic Segmentation Analysis

4.6 Ultrasound Simulators

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Ultrasound Simulators: Geographic Segmentation Analysis

4.7 Eye Simulators

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Eye Simulators: Geographic Segmentation Analysis

Chapter 5: Healthcare Simulators Market by Technology

5.1 Healthcare Simulators Market Snapshot and Growth Engine

5.2 Healthcare Simulators Market Overview

5.3 Low-Fidelity Simulators

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Low-Fidelity Simulators: Geographic Segmentation Analysis

5.4 Medium-Fidelity Simulators

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Medium-Fidelity Simulators: Geographic Segmentation Analysis

5.5 High-Fidelity Simulators

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 High-Fidelity Simulators: Geographic Segmentation Analysis

5.6 Web-Based Simulators

5.6.1 Introduction and Market Overview

5.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.6.3 Key Market Trends, Growth Factors and Opportunities

5.6.4 Web-Based Simulators: Geographic Segmentation Analysis

Chapter 6: Healthcare Simulators Market by End User

6.1 Healthcare Simulators Market Snapshot and Growth Engine

6.2 Healthcare Simulators Market Overview

6.3 Academic & Research Institutions

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Academic & Research Institutions: Geographic Segmentation Analysis

6.4 Hospitals

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Hospitals: Geographic Segmentation Analysis

6.5 Military Organizations

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Military Organizations: Geographic Segmentation Analysis

6.6 Others

6.6.1 Introduction and Market Overview

6.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.6.3 Key Market Trends, Growth Factors and Opportunities

6.6.4 Others: Geographic Segmentation Analysis

Chapter 7: Healthcare Simulators Market by Application

7.1 Healthcare Simulators Market Snapshot and Growth Engine

7.2 Healthcare Simulators Market Overview

7.3 Education & Training

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.3.3 Key Market Trends, Growth Factors and Opportunities

7.3.4 Education & Training: Geographic Segmentation Analysis

7.4 Diagnostics

7.4.1 Introduction and Market Overview

7.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.4.3 Key Market Trends, Growth Factors and Opportunities

7.4.4 Diagnostics: Geographic Segmentation Analysis

7.5 Therapy & Surgery

7.5.1 Introduction and Market Overview

7.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.5.3 Key Market Trends, Growth Factors and Opportunities

7.5.4 Therapy & Surgery: Geographic Segmentation Analysis

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Healthcare Simulators Market Share by Manufacturer (2023)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 LAERDAL MEDICAL (NORWAY)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 CAE HEALTHCARE (CANADA)

8.4 GAUMARD SCIENTIFIC (USA)

8.5 3D SYSTEMS (USA)

8.6 SIMULAB CORPORATION (USA)

8.7 MENTICE AB (SWEDEN)

8.8 KYOTO KAGAKU (JAPAN)

8.9 LIMBS & THINGS (UK)

8.10 SYNBONE AG (SWITZERLAND)

8.11 SURGICAL SCIENCE SWEDEN AB (SWEDEN)

8.12 INTELLIGENT ULTRASOUND (UK)

8.13 MEDAPHOR GROUP (UK)

8.14 .

8.15 OTHER ACTIVE PLAYERS

Chapter 9: Global Healthcare Simulators Market By Region

9.1 Overview

9.2. North America Healthcare Simulators Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size By Product Type

9.2.4.1 Patient Simulators

9.2.4.2 Surgical Simulators

9.2.4.3 Dental Simulators

9.2.4.4 Ultrasound Simulators

9.2.4.5 Eye Simulators

9.2.5 Historic and Forecasted Market Size By Technology

9.2.5.1 Low-Fidelity Simulators

9.2.5.2 Medium-Fidelity Simulators

9.2.5.3 High-Fidelity Simulators

9.2.5.4 Web-Based Simulators

9.2.6 Historic and Forecasted Market Size By End User

9.2.6.1 Academic & Research Institutions

9.2.6.2 Hospitals

9.2.6.3 Military Organizations

9.2.6.4 Others

9.2.7 Historic and Forecasted Market Size By Application

9.2.7.1 Education & Training

9.2.7.2 Diagnostics

9.2.7.3 Therapy & Surgery

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Healthcare Simulators Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size By Product Type

9.3.4.1 Patient Simulators

9.3.4.2 Surgical Simulators

9.3.4.3 Dental Simulators

9.3.4.4 Ultrasound Simulators

9.3.4.5 Eye Simulators

9.3.5 Historic and Forecasted Market Size By Technology

9.3.5.1 Low-Fidelity Simulators

9.3.5.2 Medium-Fidelity Simulators

9.3.5.3 High-Fidelity Simulators

9.3.5.4 Web-Based Simulators

9.3.6 Historic and Forecasted Market Size By End User

9.3.6.1 Academic & Research Institutions

9.3.6.2 Hospitals

9.3.6.3 Military Organizations

9.3.6.4 Others

9.3.7 Historic and Forecasted Market Size By Application

9.3.7.1 Education & Training

9.3.7.2 Diagnostics

9.3.7.3 Therapy & Surgery

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Healthcare Simulators Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size By Product Type

9.4.4.1 Patient Simulators

9.4.4.2 Surgical Simulators

9.4.4.3 Dental Simulators

9.4.4.4 Ultrasound Simulators

9.4.4.5 Eye Simulators

9.4.5 Historic and Forecasted Market Size By Technology

9.4.5.1 Low-Fidelity Simulators

9.4.5.2 Medium-Fidelity Simulators

9.4.5.3 High-Fidelity Simulators

9.4.5.4 Web-Based Simulators

9.4.6 Historic and Forecasted Market Size By End User

9.4.6.1 Academic & Research Institutions

9.4.6.2 Hospitals

9.4.6.3 Military Organizations

9.4.6.4 Others

9.4.7 Historic and Forecasted Market Size By Application

9.4.7.1 Education & Training

9.4.7.2 Diagnostics

9.4.7.3 Therapy & Surgery

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Healthcare Simulators Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size By Product Type

9.5.4.1 Patient Simulators

9.5.4.2 Surgical Simulators

9.5.4.3 Dental Simulators

9.5.4.4 Ultrasound Simulators

9.5.4.5 Eye Simulators

9.5.5 Historic and Forecasted Market Size By Technology

9.5.5.1 Low-Fidelity Simulators

9.5.5.2 Medium-Fidelity Simulators

9.5.5.3 High-Fidelity Simulators

9.5.5.4 Web-Based Simulators

9.5.6 Historic and Forecasted Market Size By End User

9.5.6.1 Academic & Research Institutions

9.5.6.2 Hospitals

9.5.6.3 Military Organizations

9.5.6.4 Others

9.5.7 Historic and Forecasted Market Size By Application

9.5.7.1 Education & Training

9.5.7.2 Diagnostics

9.5.7.3 Therapy & Surgery

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Healthcare Simulators Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size By Product Type

9.6.4.1 Patient Simulators

9.6.4.2 Surgical Simulators

9.6.4.3 Dental Simulators

9.6.4.4 Ultrasound Simulators

9.6.4.5 Eye Simulators

9.6.5 Historic and Forecasted Market Size By Technology

9.6.5.1 Low-Fidelity Simulators

9.6.5.2 Medium-Fidelity Simulators

9.6.5.3 High-Fidelity Simulators

9.6.5.4 Web-Based Simulators

9.6.6 Historic and Forecasted Market Size By End User

9.6.6.1 Academic & Research Institutions

9.6.6.2 Hospitals

9.6.6.3 Military Organizations

9.6.6.4 Others

9.6.7 Historic and Forecasted Market Size By Application

9.6.7.1 Education & Training

9.6.7.2 Diagnostics

9.6.7.3 Therapy & Surgery

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Healthcare Simulators Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size By Product Type

9.7.4.1 Patient Simulators

9.7.4.2 Surgical Simulators

9.7.4.3 Dental Simulators

9.7.4.4 Ultrasound Simulators

9.7.4.5 Eye Simulators

9.7.5 Historic and Forecasted Market Size By Technology

9.7.5.1 Low-Fidelity Simulators

9.7.5.2 Medium-Fidelity Simulators

9.7.5.3 High-Fidelity Simulators

9.7.5.4 Web-Based Simulators

9.7.6 Historic and Forecasted Market Size By End User

9.7.6.1 Academic & Research Institutions

9.7.6.2 Hospitals

9.7.6.3 Military Organizations

9.7.6.4 Others

9.7.7 Historic and Forecasted Market Size By Application

9.7.7.1 Education & Training

9.7.7.2 Diagnostics

9.7.7.3 Therapy & Surgery

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Healthcare Simulators Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.87 Billion |

|

Forecast Period 2024-32 CAGR: |

16.02% |

Market Size in 2032: |

USD 10.93 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Technology |

|

||

|

By End User |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||