Global Orthodontic Services Market Synopsis:

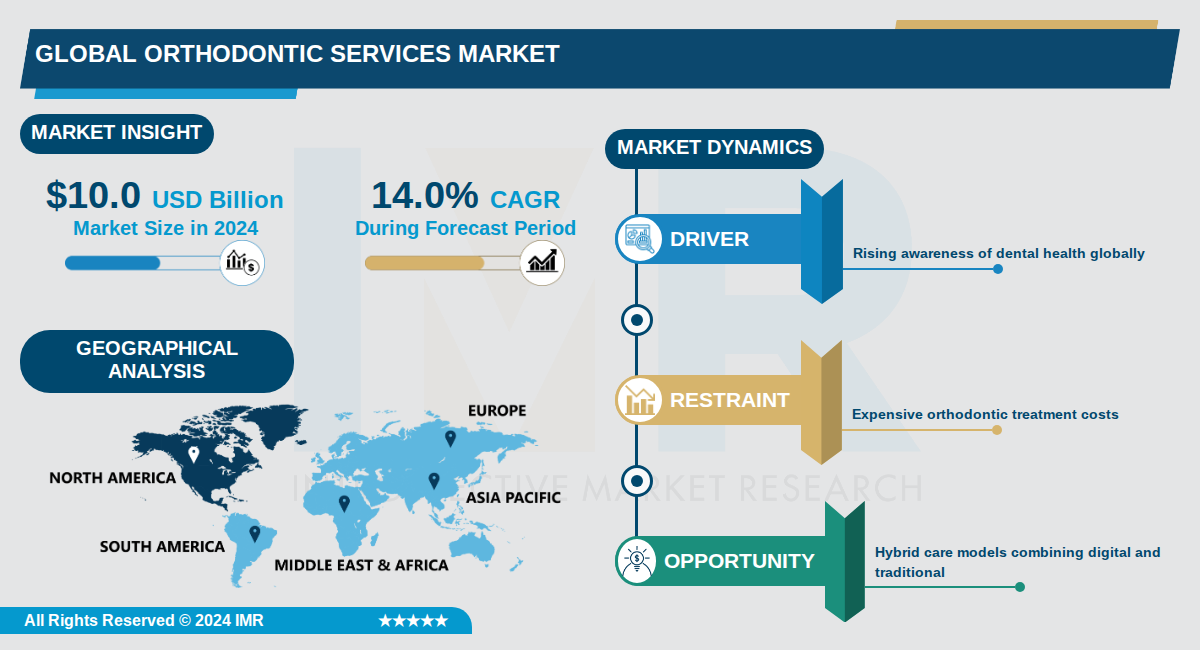

Global Orthodontic Services Market Size Was Valued at USD 10.0 Billion in 2024, and is Projected to Reach USD 38.0 Billion by 2035, Growing at a CAGR of 14.0% From 2024-2035.

The Global Orthodontic Services Market, valued at $10.0 billion in 2024, is projected to reach $38.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 14.0%. This robust expansion reflects increasing demand for orthodontic treatments driven by aesthetic preferences and advancements in dental technologies.

North America currently dominates the market, holding the largest revenue share due to advanced healthcare infrastructure, high disposable incomes, and widespread adoption of innovative solutions like clear aligners and digital treatment planning. The region benefits from a high concentration of skilled orthodontists and favorable reimbursement policies.

Asia-Pacific is poised for the fastest growth, fueled by rapid urbanization, rising middle-class populations, increasing awareness of oral health, and growing investments in dental infrastructure. Countries like China are leading with high adoption of modern orthodontic solutions amid rising malocclusion cases.

Global Orthodontic Services Market Trend Analysis:

Digitalization and AI-Powered Treatment Planning

- Orthodontic practices are rapidly adopting digital workflows that incorporate 3D intraoral scanners, AI-assisted treatment planning, and CAD/CAM software to enhance precision and efficiency. These technologies enable orthodontists to analyze 3D scans and X-rays for highly accurate, customized treatment simulations that optimize force application and reduce mid-treatment refinements. The global digital dental diagnosis and treatment service market was valued at US$1.4 billion in 2025 and is projected to grow to US$1.57 billion in 2026.

- Advanced AI solutions are enabling remote consultations and tele-dentistry, significantly expanding patient access to care beyond traditional in-office visits. Teens are increasingly using smartphone apps to scan their teeth remotely, allowing orthodontists to monitor progress virtually and reduce the need for frequent in-person appointments. This shift is transforming clinical workflows and enabling practices to serve larger patient populations with improved operational efficiency.

- Innovations in 3D printing technology are revolutionizing appliance manufacturing, with examples including LightForce 3D-printed brackets offering precision and low-profile treatment, and Ghost PU Aligner Sheets with optimized thermoplastics that improve durability, force retention, and stain resistance. The supplies segment, comprising brackets, archwires, and aligners alongside digital innovations, held the largest revenue share of the market in 2024 and continues to drive technological advancement.

Clear Aligner Dominance Among Adult Patients

- There is a pronounced shift toward clear aligners as the preferred treatment option for adult patients, driven by increased awareness of dental aesthetics and the convenience of removable appliances. The dentist and orthodontist-owned practices segment, which dominated the market with the highest share in 2025, has benefited from the easy availability of custom aligners in clinics and partnerships between manufacturers and service providers. This segment is anticipated to capture 89.5% of the market share in 2026.

- North America generated USD 3.66 billion in orthodontics revenue in 2026, with a significant portion driven by growing numbers of adult individuals opting for orthodontic procedures, particularly clear aligners. Asia-Pacific markets, including China (USD 0.74 billion in 2026) and India (USD 0.39 billion in 2026), are experiencing rising awareness of dental aesthetics among young adults and professionals, fueling demand for modern aligner solutions supported by increasing disposable incomes.

- In the future, aligners are expected to dominate new adult cases globally, while traditional braces will remain essential for complex dental corrections. The trend reflects broader patient preferences for aesthetic, convenient treatment options that align with modern lifestyle expectations and digital-first healthcare approaches.

Expansion of Orthodontic Services in Emerging Markets

- Asia-Pacific is anticipated to be the fastest-growing region and the second-largest orthodontics market, projected to hold USD 2.45 billion in 2026. The rapid growth is driven by the widening awareness of dental aesthetics, the expanding number of dental practices, high prevalence of dental ailments, and strategic initiatives by market operators. Key cities including Tokyo, Seoul, and Beijing are bolstering advanced dental clinics, while Thailand and India are encouraging medical tourism to accelerate accessibility to orthodontic care.

- India and China represent particularly significant growth opportunities, with India's market poised to reach USD 0.39 billion and China's expanding market set to reach USD 0.74 billion in 2026. In India, rising awareness of dental aesthetics and preventive care is fueling demand for clear aligners, supported by technology adoption like 3D scanning in clinics. In May 2025, Align Technology received regulatory approval to roll out its 3D-printed Invisalign Palatal Expander System in China in the second half of 2025.

- The global orthodontics market is projected to grow from approximately USD 9.50 billion in 2026 to USD 38.43 billion by 2034, representing a compound annual growth rate of 19.10%. This explosive growth is substantially driven by emerging markets adopting advanced technologies and increasing patient populations seeking orthodontic treatment, positioning providers in these regions for substantial revenue expansion.

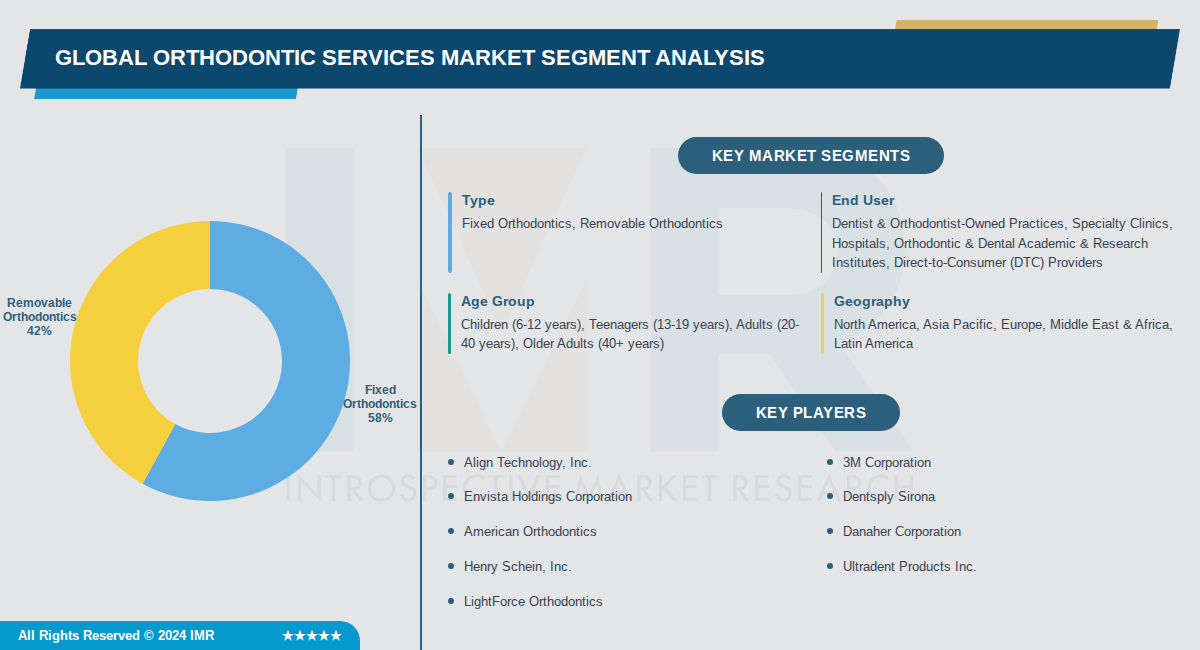

Global Orthodontic Services Market Segment Analysis:

Global Orthodontic Services Market is Segmented on the basis of By Type, By End User, By Age Group

By Type, Fixed Orthodontics segment is expected to dominate the market during the forecast period

- Fixed orthodontics dominates the market as it provides superior treatment outcomes with better control over tooth movement and alignment precision compared to removable appliances.

- Fixed appliances including braces and fixed aligners are preferred by orthodontists for complex malocclusion cases, driving higher adoption rates across dental practices globally.

By End User, Dentist & Orthodontist-Owned Practices segment is expected to dominate the market during the forecast period

- Dentist and orthodontist-owned practices dominate with nearly 50% market share because they serve as primary treatment providers offering comprehensive diagnostic, treatment planning, and follow-up care services.

- These private practices benefit from patient loyalty, easier access to advanced technologies like 3D imaging and digital scanning, and favorable reimbursement policies that enhance their competitive advantage.

By Age Group, Teenagers (13-19 years) segment is expected to dominate the market during the forecast period

- Teenagers represent the largest segment at 38% share due to optimal timing for orthodontic treatment when permanent teeth are still developing and the jawbone is more responsive to correction.

- This age group has strong parental support for aesthetic dental procedures and higher tolerance for extended treatment durations, making them the most receptive patient population for orthodontic services.

By Geography, North America segment is expected to dominate the market during the forecast period

- North America dominates with 43% market share due to its robust healthcare infrastructure, high concentration of skilled orthodontists, advanced clinic facilities, comprehensive insurance coverage, and cultural emphasis on dental aesthetics.

- Asia Pacific is the fastest-growing region driven by rapid urbanization, rising disposable incomes, increasing awareness of dental health, growing middle-class population, and expanding adoption of advanced technologies like clear aligners at cost-effective price points.

Global Orthodontic Services Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the global orthodontics market due to its highest revenue share, generating USD 3.66 billion in 2025 and maintaining the leading position in 2026. The U.S. holds the largest share within the region at USD 3.25 billion in 2025, supported by a high number of orthodontists, with 10,904 reported in 2023, concentrated in states like California, New York, and Texas. This regional leadership is further bolstered by growing adult adoption of orthodontic procedures, particularly clear aligners.

- The region benefits from well-established healthcare infrastructure, high prevalence of dental disorders, and rapid adoption of advanced technologies like 3D printing, AI-assisted treatment planning, and oral scanners. Favorable regulations and government investments in R&D for orthodontic products enhance market growth. Increasing awareness of dental aesthetics and a large patient pool with malocclusion drive sustained demand.

- Major players focus on North America with frequent advanced product launches, such as innovative clear aligners and digital workflows. Recent developments include rising startup investments and strategic initiatives by companies to expand orthodontic services. The presence of a strong network of dental clinics and hospitals further supports market expansion in the U.S. and Canada.

Active Key Players in the Global Orthodontic Services Market:

- Align Technology, Inc. (USA)

- 3M Corporation (USA)

- Envista Holdings Corporation (USA)

- Dentsply Sirona (USA)

- American Orthodontics (USA)

- Danaher Corporation (USA)

- Henry Schein, Inc. (USA)

- Ultradent Products Inc. (USA)

- LightForce Orthodontics (USA)

- TP Orthodontics, Inc. (USA)

- Rocky Mountain Orthodontics, Inc. (USA)

- Institut Straumann AG (Switzerland)

- Dentaurum GmbH & Co. KG (Germany)

- Forestadent Bernhard Förster GmbH (Germany)

- DB Orthodontics Ltd. (United Kingdom)

- Leone S.p.A. (Italy)

- GC Orthodontics (Japan)

- Angelalign Technology Inc. (China)

- Shanghai Smartee Dental Technology Co. Ltd. (China)

- Medit (South Korea)

- Other Active Players

|

Global Orthodontic Services Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 10.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

14.0 % |

Market Size in 2035: |

USD 38.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By End User |

|

||

|

By Age Group |

|

||

|

By Geography |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Global Orthodontic Services Market by Type (2017-2035)

4.1 Global Orthodontic Services Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Fixed Orthodontics

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Removable Orthodontics

Chapter 5: Global Orthodontic Services Market by End User (2017-2035)

5.1 Global Orthodontic Services Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Dentist & Orthodontist-Owned Practices

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Specialty Clinics

5.5 Hospitals

5.6 Orthodontic & Dental Academic & Research Institutes

5.7 Direct-to-Consumer (DTC) Providers

Chapter 6: Global Orthodontic Services Market by Age Group (2017-2035)

6.1 Global Orthodontic Services Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Children (6-12 years)

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Teenagers (13-19 years)

6.5 Adults (20-40 years)

6.6 Older Adults (40+ years)

Chapter 7: Global Orthodontic Services Market by Geography (2017-2035)

7.1 Global Orthodontic Services Market Snapshot and Growth Engine

7.2 Market Overview

7.3 North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Asia Pacific

7.5 Europe

7.6 Middle East & Africa

7.7 Latin America

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Global Orthodontic Services Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 ALIGN TECHNOLOGY

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 INC.

8.4 3M CORPORATION

8.5 ENVISTA HOLDINGS CORPORATION

8.6 DENTSPLY SIRONA

8.7 AMERICAN ORTHODONTICS

8.8 DANAHER CORPORATION

8.9 HENRY SCHEIN

8.10 INC.

8.11 ULTRADENT PRODUCTS INC.

8.12 LIGHTFORCE ORTHODONTICS

8.13 TP ORTHODONTICS

8.14 INC.

8.15 ROCKY MOUNTAIN ORTHODONTICS

8.16 INC.

8.17 INSTITUT STRAUMANN AG

8.18 DENTAURUM GMBH & CO. KG

8.19 FORESTADENT BERNHARD FÖRSTER GMBH

8.20 DB ORTHODONTICS LTD.

8.21 LEONE S.P.A.

8.22 GC ORTHODONTICS

8.23 ANGELALIGN TECHNOLOGY INC.

8.24 SHANGHAI SMARTEE DENTAL TECHNOLOGY CO. LTD.

8.25 MEDIT

Chapter 9: Global Global Orthodontic Services Market By Region

9.1 Overview

9.2. North America Global Orthodontic Services Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Global Orthodontic Services Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Global Orthodontic Services Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Global Orthodontic Services Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Global Orthodontic Services Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Global Orthodontic Services Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Global Orthodontic Services Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 10.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

14.0 % |

Market Size in 2035: |

USD 38.0 Billion |

|

Segments Covered: |

By Type |

|

|

|

By End User |

|

||

|

By Age Group |

|

||

|

By Geography |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||