Key Market Highlights

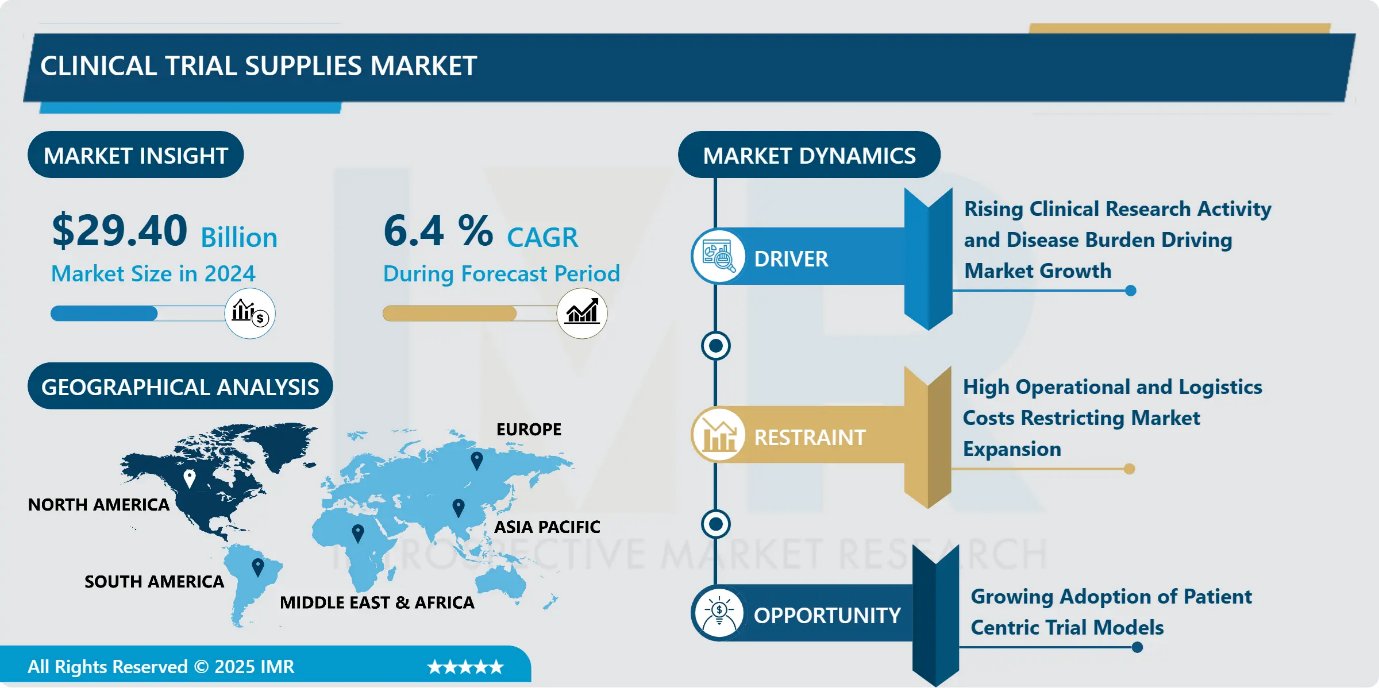

Clinical Trial Supplies Market Size Was Valued at USD 29.40 Billion in 2024, and is Projected to Reach USD 58.17 Billion by 2035, Growing at a CAGR of 6.4% from 2025-2035.

- Market Size in 2024: USD 29.40 Billion

- Projected Market Size by 2035: USD 58.17 Billion

- CAGR (2025–2035): 6.4%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By End User: The biotechnology companies segment is anticipated to lead the market by accounting for 30.3% of the market share throughout the forecast period.

- By Therapeutic Area: The oncology segment is expected to capture 27.4% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 33.2% of the market share during the forecast period.

- Active Players: Almac Group (United Kingdom), Biocair (United Kingdom), BioNTech (Germany), Catalent Inc. (United States), CureVac (Germany), and Other Active Players.

Clinical Trial Supplies Market Synopsis:

The Clinical Trial Supplies Market refers to the specialized ecosystem that supports the planning, production, management, and distribution of materials required for the effective execution of clinical trials across all development phases. It includes investigational drugs, comparators, placebos, and ancillary supplies, along with critical services such as packaging, labeling, storage, and global logistics. The market is shaped by increasing clinical trial complexity, the rise of biologics and personalized medicine, and the expansion of trials into emerging regions. Strict regulatory compliance, temperature-controlled supply chains, and real-time visibility are essential market conditions. Growing outsourcing, digitalization, and decentralized trial models further reinforce the need for reliable, flexible, and compliant clinical trial supply solutions.

Clinical Trial Supplies Market Dynamics and Trend Analysis:

Clinical Trial Supplies Market Growth Driver

Rising Clinical Research Activity and Disease Burden Driving Market Growth

-

The steady increase in global clinical trial activity is a major driver of the clinical trial supplies market, supported by expanding drug development pipelines and ongoing innovation across therapeutic areas. Pharmaceutical and biotechnology companies require a growing volume of investigational products, ancillary materials, specialized packaging, and reliable logistics to support complex trials.

- In parallel, the rising prevalence of chronic and rare diseases continues to intensify research efforts aimed at developing effective therapies. These conditions demand advanced and often customized trial materials, including specialized delivery systems and patient-specific dosing. Together, expanding clinical research programs and the growing disease burden are sustaining long-term demand for efficient, compliant, and specialized clinical trial supply solutions.

Clinical Trial Supplies Market Limiting Factor

High Operational and Logistics Costs Restricting Market Expansion

- The clinical trial supplies market faces a major restraint due to the high costs associated with the manufacturing handling and distribution of trial materials. Expenses extend beyond basic sourcing and are driven by specialized packaging country specific labeling and extensive documentation requirements for blinding and randomization.

- The growing use of biologics further intensifies cost pressures as these products require advanced cold chain infrastructure temperature controlled storage validated shipping systems and continuous monitoring. These complex operational demands significantly increase overall trial budgets placing financial strain on sponsors and limiting the number scale and geographic reach of clinical studies thereby constraining broader market growth.

Clinical Trial Supplies Market Expansion Opportunity

Growing Adoption of Patient Centric Trial Models

- The increasing emphasis on patient centric clinical trial designs is creating significant opportunities within the clinical trial supply and logistics market. Sponsors are prioritizing patient convenience and engagement to improve recruitment and retention outcomes. This shift is accelerating the adoption of decentralized and hybrid trial models that require direct to patient delivery of investigational products and trial materials. As a result logistics providers are developing flexible distribution networks temperature controlled shipping and real time tracking solutions tailored to individual patient needs. The expansion of these patient focused approaches broadens trial accessibility and drives demand for innovative responsive and scalable supply chain services supporting continued market growth.

Clinical Trial Supplies Market Challenge and Risk

Regulatory Fragmentation and Comparator Supply Constraints as Key Market Challenges

- The clinical trial supplies market faces significant challenges due to complex and fragmented regulatory requirements across regions. Variations in rules governing packaging labeling documentation and import export procedures increase operational complexity and demand extensive compliance expertise. These regulatory differences often slow supply chain execution and raise overall trial costs.

- In addition sourcing comparator drugs for control arms remains a persistent challenge particularly for head to head studies. Limited availability commercial restrictions and geographic supply barriers complicate procurement and delay trial initiation. Together regulatory fragmentation and constrained comparator access create planning uncertainties increase costs and act as critical bottlenecks for efficient clinical trial execution.

Clinical Trial Supplies Market Trend

Rising Demand for Complex Biologics and Technology Driven Supply Chains

- The clinical trial supply and logistics market is increasingly influenced by the growing focus on biologics and personalized medicine trials. These therapies require stringent cold chain management specialized storage conditions and advanced biomarker driven workflows to maintain product integrity.

- At the same time precision medicine is elevating the use of data intensive approaches including AI enabled patient matching and real world data integration supported by initiatives from organizations such as the NIH. In parallel rapid advancements in supply chain technologies such as artificial intelligence blockchain and real time analytics are transforming inventory control forecasting accuracy and operational transparency. This convergence of complex therapeutics and digital innovation is reshaping supply strategies and driving market evolution.

Clinical Trial Supplies Market Segment Analysis:

Clinical Trial Supplies Market is segmented based on Therapeutic Area, Phase, Product Type, Services, End User, and Region.

By End User, Biotechnology companies segment is expected to dominate the market with around 30.3% share during the forecast period.

- Biotechnology companies are emerging as the fastest-growing end-user segment in the clinical trial supplies market, supported by expanding development pipelines and limited internal operational infrastructure. Strong venture funding activity, illustrated by capital raises from firms such as SpliceBio, is accelerating reliance on outsourced clinical supply partners.

- These sponsors prioritize speed and efficiency, seeking vendors capable of compressing timelines through digital documentation, centralized feasibility assessments, and agile logistics models. While pharmaceutical companies continue to represent the largest customer base due to large-scale global programs and long-term service agreements, the biotech segment is dominant in growth as innovation intensity and outsourcing dependence remain structurally high.

By Therapeutic Area, Oncology is expected to dominate with close to 27.4% market share during the forecast period.

- Oncology represents the most dominant therapeutic area within the clinical trial supplies market due to the consistently high volume and complexity of cancer-related trials. Continuous innovation in targeted and personalized oncology therapies significantly increases supply chain demands, including cold chain management, short shelf-life handling, and flexible resupply strategies. Oncology studies frequently involve adaptive designs, multi-arm protocols, and global trial sites, all of which raise requirements for forecasting accuracy, blinding, and secure distribution. High regulatory scrutiny and the elevated value of oncology investigational products further intensify logistics needs. These factors collectively position oncology as the primary driver of demand, making it the most influential segment in shaping clinical trial supply strategies.

Clinical Trial Supplies Market Regional Insights:

North America region is estimated to lead the market with around 33.2% share during the forecast period.

- North America continues to lead the clinical trial support services and clinical trial supplies market driven by a strong pharmaceutical and biotechnology ecosystem high clinical trial activity and advanced logistics infrastructure. Structured regulatory guidance and feedback mechanisms from the FDA support efficient trial execution while a dense network of investigators and CROs sustains demand for outsourced services.

- The region’s dominance is further reinforced by rapid adoption of decentralized trials AI enabled supply chain solutions and digital compliance tools. Although rising labor costs and workforce fatigue pose challenges ongoing innovation robust government funding and sustained R&D investments particularly in the United States ensure North America remains the most influential and mature market globally.

Clinical Trial Supplies Market Active Players:

- Almac Group (United Kingdom)

- Biocair (United Kingdom)

- BioNTech (Germany)

- Catalent Inc. (United States)

- CureVac (Germany)

- KLIFO (Denmark)

- Marken (United States)

- Movianto (France)

- Myonex (United States)

- NVIDIA (United States)

- Parexel International Corporation (United States)

- PCI Pharma Services (United States)

- Piramal Pharma Solutions (India)

- Sharp Services, LLC (United States)

- Thermo Fisher Scientific Inc. (United States)

- UPS Healthcare (United States)

- World Courier (United States)

- Other Active Players

Key Industry Developments in the Clinical Trial Supplies Market:

- In June 2025: BioNTech completed the acquisition of CureVac to strengthen its mRNA-based oncology pipeline. The transaction allows BioNTech to expand cancer-focused research capabilities. CureVac’s research operations in Tübingen will continue to operate under the new ownership.

- In June 2025: NVIDIA expanded its presence in healthcare by deepening collaborations with Novo Nordisk and DCAI. The partnerships leverage the Gefion supercomputer to support advanced AI-driven drug discovery. These initiatives aim to accelerate clinical development workflows and computational research efficiency.

Advanced Technical Infrastructure and Regulatory-Driven Supply Chain Framework of the Global Clinical Trial Supplies Market

- The Clinical Trial Supplies Market encompasses the specialized systems, products, and services required to manage investigational materials throughout the lifecycle of a clinical study. It includes the sourcing, manufacturing, packaging, labeling, storage, and distribution of investigational medicinal products, comparators, placebos, and ancillary supplies. Operations are governed by stringent regulatory frameworks such as Good Manufacturing Practice and Good Distribution Practice enforced by authorities including the FDA and aligned with international guidelines.

- Technically, the market relies on validated cold chain infrastructure, serialization and tracking systems, and Interactive Response Technology platforms for inventory control and randomization. Increasingly, digital tools such as AI-driven demand forecasting, real-time temperature monitoring, and blockchain-enabled traceability are integrated to ensure compliance, minimize wastage, and maintain product integrity. These technical capabilities are essential to supporting complex global and decentralized clinical trial designs.

|

Clinical Trial Supplies Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 29.40 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.4 % |

Market Size in 2035: |

USD 58.17 Bn. |

|

Segments Covered: |

By Therapeutic Area |

|

|

|

By Phase

|

|

||

|

By Product Type |

|

||

|

By Services |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Clinical Trial Supplies Market by Therapeutic Area (2018-2035)

4.1 Clinical Trial Supplies Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Oncology

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Gynecology

4.5 Neurology

4.6 Gastroenterology

4.7 Immunology

4.8 and Others

Chapter 5: Clinical Trial Supplies Market by Phase (2018-2035)

5.1 Clinical Trial Supplies Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Phase I

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Phase II

5.5 and Others

Chapter 6: Clinical Trial Supplies Market by Product Type (2018-2035)

6.1 Clinical Trial Supplies Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Packaging Materials

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Patient Kits

6.5 Medical Devices

6.6 and Ancillary Supplies

Chapter 7: Clinical Trial Supplies Market by Services (2018-2035)

7.1 Clinical Trial Supplies Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Clinical Trial Packaging and Labeling

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Storage and Distribution

7.5 Logistics and Supply Chain Management

7.6 and Clinical Trial Support Services

Chapter 8: Clinical Trial Supplies Market by End User (2018-2035)

8.1 Clinical Trial Supplies Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Biotechnology Companies

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Contract Research Organizations

8.5 Academic and Research Institutions

8.6 and Clinical Research Sites

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Clinical Trial Supplies Market Share by Manufacturer/Service Provider(2024)

9.1.3 Industry BCG Matrix

9.1.4 PArtnerships, Mergers & Acquisitions

9.2 ALMAC GROUP (UNITED KINGDOM)

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 BIOCAIR (UNITED KINGDOM)

9.4 BIONTECH (GERMANY)

9.5 CATALENT INC. (UNITED STATES)

9.6 CUREVAC (GERMANY)

9.7 KLIFO (DENMARK)

9.8 MARKEN (UNITED STATES)

9.9 MOVIANTO (FRANCE)

9.10 MYONEX (UNITED STATES)

9.11 NVIDIA (UNITED STATES)

9.12 PAREXEL INTERNATIONAL CORPORATION (UNITED STATES)

9.13 PCI PHARMA SERVICES (UNITED STATES)

9.14 PIRAMAL PHARMA SOLUTIONS (INDIA)

9.15 SHARP SERVICES

9.16 LLC (UNITED STATES)

9.17 THERMO FISHER SCIENTIFIC INC. (UNITED STATES)

9.18 UPS HEALTHCARE (UNITED STATES)

9.19 WORLD COURIER (UNITED STATES)

9.20 AND OTHER ACTIVE PLAYERS.

Chapter 10: Global Clinical Trial Supplies Market By Region

10.1 Overview

10.2. North America Clinical Trial Supplies Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.2.4.1 US

10.2.4.2 Canada

10.2.4.3 Mexico

10.3. Eastern Europe Clinical Trial Supplies Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.3.4.1 Russia

10.3.4.2 Bulgaria

10.3.4.3 The Czech Republic

10.3.4.4 Hungary

10.3.4.5 Poland

10.3.4.6 Romania

10.3.4.7 Rest of Eastern Europe

10.4. Western Europe Clinical Trial Supplies Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.4.4.1 Germany

10.4.4.2 UK

10.4.4.3 France

10.4.4.4 The Netherlands

10.4.4.5 Italy

10.4.4.6 Spain

10.4.4.7 Rest of Western Europe

10.5. Asia Pacific Clinical Trial Supplies Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.5.4.1 China

10.5.4.2 India

10.5.4.3 Japan

10.5.4.4 South Korea

10.5.4.5 Malaysia

10.5.4.6 Thailand

10.5.4.7 Vietnam

10.5.4.8 The Philippines

10.5.4.9 Australia

10.5.4.10 New Zealand

10.5.4.11 Rest of APAC

10.6. Middle East & Africa Clinical Trial Supplies Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.6.4.1 Turkiye

10.6.4.2 Bahrain

10.6.4.3 Kuwait

10.6.4.4 Saudi Arabia

10.6.4.5 Qatar

10.6.4.6 UAE

10.6.4.7 Israel

10.6.4.8 South Africa

10.7. South America Clinical Trial Supplies Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

10.7.4.1 Brazil

10.7.4.2 Argentina

10.7.4.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

Chapter 12 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 13 Case Study

Chapter 14 Appendix

12.1 Sources

12.2 List of Tables and figures

12.3 Short Forms and Citations

12.4 Assumption and Conversion

12.5 Disclaimer

|

Clinical Trial Supplies Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 29.40 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.4 % |

Market Size in 2035: |

USD 58.17 Bn. |

|

Segments Covered: |

By Therapeutic Area |

|

|

|

By Phase

|

|

||

|

By Product Type |

|

||

|

By Services |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||