Cephalosporin Drugs Market Synopsis:

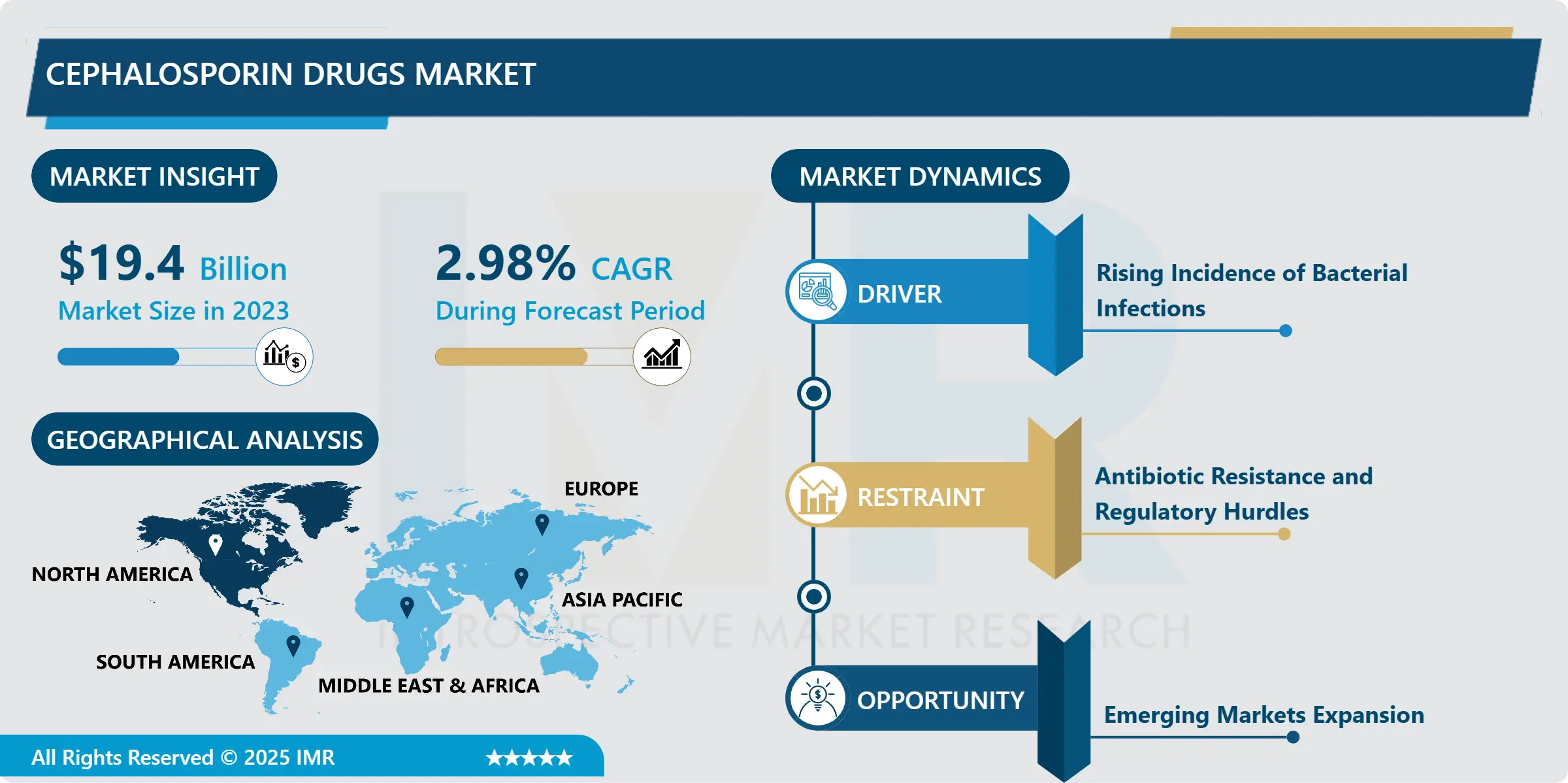

Cephalosporin Drugs Market Size Was Valued at USD 19.40 Billion in 2023, and is Projected to Reach USD 25.27 Billion by 2032, Growing at a CAGR of 2.98% From 2024-2032.

Cephalosporin drugs are antibiotics which are produced from the fungus Acremonium (earlier called Cephalosporium). They are mostly prescribed for bacterial infections because they limit the formation of bacterial cell wall. There are several classifications of the cephalosporins which distinguish the antibiotics according to their activity against different types of bacteria – generations. It is used primarily with respiratory tract infections and Urinary tract infections, skin infections and other many.

The global Cephalosporin drugs market is propelled by the increasing rate of bacterial infections and antibiotics consumption in different segments. They are now one of most important therapeutic tools in patients’ management in hospitals and clinics worldwide. There are five generations of Cephalosporins and each of them contains different antimicrobial efficacy. The global market for cephalosporins is growing because bacterial resistance remains a constant issue and new generations of antibiotics are being sought.

The market is shifted further by the current and constant research and development activities to make cephalosporins more effective and safer. As the formulations in drug were improving, and as the introduction of new generations of cephalosporins, this group of drug plays an essential role to manage bacterial infections. Further, the development of the healthcare industry and improved access to some priority chemicals in developing countries has contributed to the need for cephalosporins.

Despite the high demand of these products, the market is faced with problems of excessive use of antibiotics, resistance to which is a major concern called antimicrobial resistance (AMR). We are now seeing attempts to combat AMR become a major force in deciding on new regulation and the creation of novel antibiotic treatments. In addition, market players are shifting their focus to the stakeholders consolidating their capacities with strategic partnerships, mergers, and acquisitions to get a broader product range and secured market position in the global geochemistry market.

Cephalosporin market has good prognosis, there is a well-established market need for broad-spectrum antibiotics and for the development of new treatments. However, competition from regulatory authorities and from generic drugs may pose some constraints to growth of branded cephalosporins. The nature and unpredictable growth of the market can heavily rely on changes in drug formulations and distribution channels over the course of the five years.

Cephalosporin Drugs Market Trend Analysis:

Increase in Antibiotic Resistance

-

One of the emerging trends across the world health arena is antibiotic resistance with special emphasis being put on bacterial resistance to cephalosporins. One of the most important factors explaining the growth of requirements for new generations of cephalosporins is the growth of the number of cases with multi-drug-resistant organisms (MDROs). This is mainly due to the misuse and over prescription of antibiotics that has been made and dosed in health facilities and outpatient departments. The major cause is the rising resistance of bacteria to these drugs and thus reduced efficacy of older generation cephalosporins hence expansion of use of advanced-generation cephalosporins.

- The pharmaceutical companies are opting for the development of unconventional cephalosporins having better resistance profiles. This also cover agents that are developed to invert existing resistance including beta-lactamase inhibitors with ceaphalosporins that restores antibiotics effectiveness. Moreover, awareness of antibiotic use has increased there is pressure from healthcare facilities and governments that call for better use of antibiotic. Such actions are required for maintaining the effectiveness of the cephalosporin drugs in eradicating bacteria related diseases.

Emerging Markets Expansion

-

Asia-Pacific, Latin America, Africa, and other emerging markets holds great potential for the growth of cephalosporin drugs market. There is high incidence of bacterial infections in these areas due to population boost, increasing urbanization and shift in lifestyles which calls for high use of antibiotics. These factors include investment in the enhancement of healthcare system and increased access to some primary health care needs such as essential drugs, and recreation of ceaphalosporins.

- The management of cephalosporin royalties by pharmaceutical companies has reached these emerging markets through affordable formulations and extended networks. As the populace has become more conscious about their health it’s manifested in greater antibiotic usage and eruptions in infection management hence a huge potential for these markets. In addition, governments of these regions are also upping their efforts on organisation of health care and increasing the availability of critical antibiotics, such as cephalosporins, among people.

Cephalosporin Drugs Market Segment Analysis:

Cephalosporin Drugs Market is Segmented on the basis of Generation, Route of Administration, Distribution Channel, Application, End User, and Region.

By Generation, First Generation segment is expected to dominate the market during the forecast period

-

According to the antibacterial activity cephalosporin drugs market has been classified into generations Second Generation Cephalosporin Orally Active Drugs, Third Generation Cephalosporin Orally Active Drugs, Fourth Generation Cephalosporin Orally Active Drugs and Fifth Generation Cephalosporin Orally Active Drugs. First generation cephalosporin includes cephalexin which exhibit major activity against gram-positive bacteria and is usually employed to manage a mild to moderate infections. The second includes a wider range of activity, including gram-negative bacteria, and is used for such diseases as respiratory tract infections and sinusitis.

- The third generation comprises even more effective Cephalsporin that work well against gram negative organisms appropriate for use in conditions such as meningitis and sepsis. The fourth generation further expands the coverage by incorporating features that neutralise beta-lactamase enzymes making them even more effective against resistant bacteria. The newest generation that is the fifth generation offers activity against resistant strains such as MRSA (Methicillin-resistant Staphylococcus aureus). These generations provide different efficacy to bacterial resistance, making a valuable tool for healthcare practitioners.

By Application, Hospital Use segment expected to held the largest share

-

The cephalosporins market is categorized into three primary applications: hospital, outpatient and retail prescription users. The largest business segment of use is still hospitals, since cephalosporins are often prescribed for serious or complex bacterial infections which require IV or other forms of clinical therapy. These antibiotics are generally employed in case management of infections caused by bacteria that are resistant to other forms of antibiotics which are often part of an overall strategy to contain an institutional spread of the bacteria.

- Outpatient use and retail pharmacies are also expanding seasonal segments because of growing availability of oral cephalosporin formulations. These drugs are used more frequently for mild infections in ambulatory patients . When the healthcare status in various areas is changing for the better, the request for cephalosporins in outpatient clinics and chemist’s shops remains rather high, which leads to these segments’ boosting importance in the greater market.

Cephalosporin Drugs Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

The largest share contributed to the North American region based on the developed healthcare framework, increasing prevalence of bacteria, and sound healthcare infrastructure. The United States specifically contributes significantly to market size owing to its extensive holding of the healthcare facilities, higher demand for antibiotics testing, and improvement in medical research consistently. The area also enjoys good health policies due to the attainment of essential medicines like the cephalosporins.

- Similar to the European market, the North American market for cephalosporins is fuelled by the increasing prevalence of antibiotic-resistant infections. This has encouraged both public and private health care provider to opt for the effective antibiotics such as cephalosporin. The increase in investment related to new R&D in the segment of pharmaceuticals for Cephalosporins along with the government policies of this region enforces North America to remain as the market leader.

Active Key Players in the Cephalosporin Drugs Market:

- F. Hoffmann-La Roche – (Switzerland)

- GlaxoSmithKline – (United Kingdom)

- Pfizer – (United States)

- Merck & Co. – (United States)

- Johnson & Johnson – (United States)

- Sanofi – (France)

- Novartis – (Switzerland)

- Eli Lilly – (United States)

- Bayer Healthcare – (Germany)

- AstraZeneca – (United Kingdom)

- Teva Pharmaceuticals – (Israel)

- Amgen – (United States)

- Other Active Players

Key Industry Developments in the Cephalosporin Drugs Market:

-

In April 2024, Zevtera (ceftobiprole medocaril sodium for injection) by the Basilea Pharmaceutical International Ltd. got the approval by the U.S. Food and Drug Administration (FDA) for the treatment of the serious bacterial infections in the pediatrics, and adults.

- In April 2024, the Mumbai-based Lupin, the pharmaceutical company granted the approval from the US Food and Drug Administration (USFDA) for launching the Mirabegron extended-release tablets (25 mg) in the United States market. The used of the Mirabegron extended tablets are for the treatment of bladder problems including the overactive bladder.

- In April 2024, Lupin a global major pharma company launched the generic version of Oracea (Doxycycline Capsules, 40 mg), after approval by the United States Food and Drug Administration (U.S. FDA) in the U.S. market.

|

Global Cephalosporin Drugs Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 19.40 Billion |

|

Forecast Period 2024-32 CAGR: |

2.98% |

Market Size in 2032: |

USD 25.27 Billion |

|

Segments Covered: |

By Generation |

|

|

|

By Application |

|

||

|

By Route of Administration |

|

||

|

By End-User |

|

||

|

By Distribution |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Cephalosporin Drugs Market by Generation

4.1 Cephalosporin Drugs Market Snapshot and Growth Engine

4.2 Cephalosporin Drugs Market Overview

4.3 First Generation

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 First Generation: Geographic Segmentation Analysis

4.4 Second Generation

4.4.1 Introduction and Market Overview

4.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.4.3 Key Market Trends, Growth Factors and Opportunities

4.4.4 Second Generation: Geographic Segmentation Analysis

4.5 Third Generation

4.5.1 Introduction and Market Overview

4.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.5.3 Key Market Trends, Growth Factors and Opportunities

4.5.4 Third Generation: Geographic Segmentation Analysis

4.6 Fourth Generation

4.6.1 Introduction and Market Overview

4.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.6.3 Key Market Trends, Growth Factors and Opportunities

4.6.4 Fourth Generation: Geographic Segmentation Analysis

4.7 Fifth Generation

4.7.1 Introduction and Market Overview

4.7.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.7.3 Key Market Trends, Growth Factors and Opportunities

4.7.4 Fifth Generation: Geographic Segmentation Analysis

Chapter 5: Cephalosporin Drugs Market by Application

5.1 Cephalosporin Drugs Market Snapshot and Growth Engine

5.2 Cephalosporin Drugs Market Overview

5.3 Hospital Use

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Hospital Use: Geographic Segmentation Analysis

5.4 Outpatient Use

5.4.1 Introduction and Market Overview

5.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.4.3 Key Market Trends, Growth Factors and Opportunities

5.4.4 Outpatient Use: Geographic Segmentation Analysis

5.5 Retail Pharmacies

5.5.1 Introduction and Market Overview

5.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.5.3 Key Market Trends, Growth Factors and Opportunities

5.5.4 Retail Pharmacies: Geographic Segmentation Analysis

Chapter 6: Cephalosporin Drugs Market by Route of Administration

6.1 Cephalosporin Drugs Market Snapshot and Growth Engine

6.2 Cephalosporin Drugs Market Overview

6.3 Oral

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Oral: Geographic Segmentation Analysis

6.4 Parenteral

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Parenteral: Geographic Segmentation Analysis

Chapter 7: Cephalosporin Drugs Market by End-User

7.1 Cephalosporin Drugs Market Snapshot and Growth Engine

7.2 Cephalosporin Drugs Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.3.3 Key Market Trends, Growth Factors and Opportunities

7.3.4 Hospitals: Geographic Segmentation Analysis

7.4 Clinics

7.4.1 Introduction and Market Overview

7.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.4.3 Key Market Trends, Growth Factors and Opportunities

7.4.4 Clinics: Geographic Segmentation Analysis

7.5 Homecare

7.5.1 Introduction and Market Overview

7.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.5.3 Key Market Trends, Growth Factors and Opportunities

7.5.4 Homecare: Geographic Segmentation Analysis

7.6 Others

7.6.1 Introduction and Market Overview

7.6.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

7.6.3 Key Market Trends, Growth Factors and Opportunities

7.6.4 Others: Geographic Segmentation Analysis

Chapter 8: Cephalosporin Drugs Market by Distribution Channel

8.1 Cephalosporin Drugs Market Snapshot and Growth Engine

8.2 Cephalosporin Drugs Market Overview

8.3 Hospital Pharmacies

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

8.3.3 Key Market Trends, Growth Factors and Opportunities

8.3.4 Hospital Pharmacies: Geographic Segmentation Analysis

8.4 Retail Pharmacies

8.4.1 Introduction and Market Overview

8.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

8.4.3 Key Market Trends, Growth Factors and Opportunities

8.4.4 Retail Pharmacies: Geographic Segmentation Analysis

8.5 Online Pharmacies

8.5.1 Introduction and Market Overview

8.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

8.5.3 Key Market Trends, Growth Factors and Opportunities

8.5.4 Online Pharmacies: Geographic Segmentation Analysis

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Cephalosporin Drugs Market Share by Manufacturer (2023)

9.1.3 Industry BCG Matrix

9.1.4 Heat Map Analysis

9.1.5 Mergers and Acquisitions

9.2 F. HOFFMANN-LA ROCHE – (SWITZERLAND)

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Key Strategic Moves and Recent Developments

9.2.10 SWOT Analysis

9.3 GLAXOSMITHKLINE – (UNITED KINGDOM)

9.4 PFIZER – (UNITED STATES)

9.5 MERCK & CO. – (UNITED STATES)

9.6 JOHNSON & JOHNSON – (UNITED STATES)

9.7 SANOFI – (FRANCE)

9.8 NOVARTIS – (SWITZERLAND)

9.9 ELI LILLY – (UNITED STATES)

9.10 BAYER HEALTHCARE – (GERMANY)

9.11 ASTRAZENECA – (UNITED KINGDOM)

9.12 TEVA PHARMACEUTICALS – (ISRAEL)

9.13 AMGEN – (UNITED STATES)

9.14 OTHER ACTIVE PLAYERS

Chapter 10: Global Cephalosporin Drugs Market By Region

10.1 Overview

10.2. North America Cephalosporin Drugs Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecasted Market Size By Generation

10.2.4.1 First Generation

10.2.4.2 Second Generation

10.2.4.3 Third Generation

10.2.4.4 Fourth Generation

10.2.4.5 Fifth Generation

10.2.5 Historic and Forecasted Market Size By Application

10.2.5.1 Hospital Use

10.2.5.2 Outpatient Use

10.2.5.3 Retail Pharmacies

10.2.6 Historic and Forecasted Market Size By Route of Administration

10.2.6.1 Oral

10.2.6.2 Parenteral

10.2.7 Historic and Forecasted Market Size By End-User

10.2.7.1 Hospitals

10.2.7.2 Clinics

10.2.7.3 Homecare

10.2.7.4 Others

10.2.8 Historic and Forecasted Market Size By Distribution Channel

10.2.8.1 Hospital Pharmacies

10.2.8.2 Retail Pharmacies

10.2.8.3 Online Pharmacies

10.2.9 Historic and Forecast Market Size by Country

10.2.9.1 US

10.2.9.2 Canada

10.2.9.3 Mexico

10.3. Eastern Europe Cephalosporin Drugs Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecasted Market Size By Generation

10.3.4.1 First Generation

10.3.4.2 Second Generation

10.3.4.3 Third Generation

10.3.4.4 Fourth Generation

10.3.4.5 Fifth Generation

10.3.5 Historic and Forecasted Market Size By Application

10.3.5.1 Hospital Use

10.3.5.2 Outpatient Use

10.3.5.3 Retail Pharmacies

10.3.6 Historic and Forecasted Market Size By Route of Administration

10.3.6.1 Oral

10.3.6.2 Parenteral

10.3.7 Historic and Forecasted Market Size By End-User

10.3.7.1 Hospitals

10.3.7.2 Clinics

10.3.7.3 Homecare

10.3.7.4 Others

10.3.8 Historic and Forecasted Market Size By Distribution Channel

10.3.8.1 Hospital Pharmacies

10.3.8.2 Retail Pharmacies

10.3.8.3 Online Pharmacies

10.3.9 Historic and Forecast Market Size by Country

10.3.9.1 Russia

10.3.9.2 Bulgaria

10.3.9.3 The Czech Republic

10.3.9.4 Hungary

10.3.9.5 Poland

10.3.9.6 Romania

10.3.9.7 Rest of Eastern Europe

10.4. Western Europe Cephalosporin Drugs Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecasted Market Size By Generation

10.4.4.1 First Generation

10.4.4.2 Second Generation

10.4.4.3 Third Generation

10.4.4.4 Fourth Generation

10.4.4.5 Fifth Generation

10.4.5 Historic and Forecasted Market Size By Application

10.4.5.1 Hospital Use

10.4.5.2 Outpatient Use

10.4.5.3 Retail Pharmacies

10.4.6 Historic and Forecasted Market Size By Route of Administration

10.4.6.1 Oral

10.4.6.2 Parenteral

10.4.7 Historic and Forecasted Market Size By End-User

10.4.7.1 Hospitals

10.4.7.2 Clinics

10.4.7.3 Homecare

10.4.7.4 Others

10.4.8 Historic and Forecasted Market Size By Distribution Channel

10.4.8.1 Hospital Pharmacies

10.4.8.2 Retail Pharmacies

10.4.8.3 Online Pharmacies

10.4.9 Historic and Forecast Market Size by Country

10.4.9.1 Germany

10.4.9.2 UK

10.4.9.3 France

10.4.9.4 The Netherlands

10.4.9.5 Italy

10.4.9.6 Spain

10.4.9.7 Rest of Western Europe

10.5. Asia Pacific Cephalosporin Drugs Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecasted Market Size By Generation

10.5.4.1 First Generation

10.5.4.2 Second Generation

10.5.4.3 Third Generation

10.5.4.4 Fourth Generation

10.5.4.5 Fifth Generation

10.5.5 Historic and Forecasted Market Size By Application

10.5.5.1 Hospital Use

10.5.5.2 Outpatient Use

10.5.5.3 Retail Pharmacies

10.5.6 Historic and Forecasted Market Size By Route of Administration

10.5.6.1 Oral

10.5.6.2 Parenteral

10.5.7 Historic and Forecasted Market Size By End-User

10.5.7.1 Hospitals

10.5.7.2 Clinics

10.5.7.3 Homecare

10.5.7.4 Others

10.5.8 Historic and Forecasted Market Size By Distribution Channel

10.5.8.1 Hospital Pharmacies

10.5.8.2 Retail Pharmacies

10.5.8.3 Online Pharmacies

10.5.9 Historic and Forecast Market Size by Country

10.5.9.1 China

10.5.9.2 India

10.5.9.3 Japan

10.5.9.4 South Korea

10.5.9.5 Malaysia

10.5.9.6 Thailand

10.5.9.7 Vietnam

10.5.9.8 The Philippines

10.5.9.9 Australia

10.5.9.10 New Zealand

10.5.9.11 Rest of APAC

10.6. Middle East & Africa Cephalosporin Drugs Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecasted Market Size By Generation

10.6.4.1 First Generation

10.6.4.2 Second Generation

10.6.4.3 Third Generation

10.6.4.4 Fourth Generation

10.6.4.5 Fifth Generation

10.6.5 Historic and Forecasted Market Size By Application

10.6.5.1 Hospital Use

10.6.5.2 Outpatient Use

10.6.5.3 Retail Pharmacies

10.6.6 Historic and Forecasted Market Size By Route of Administration

10.6.6.1 Oral

10.6.6.2 Parenteral

10.6.7 Historic and Forecasted Market Size By End-User

10.6.7.1 Hospitals

10.6.7.2 Clinics

10.6.7.3 Homecare

10.6.7.4 Others

10.6.8 Historic and Forecasted Market Size By Distribution Channel

10.6.8.1 Hospital Pharmacies

10.6.8.2 Retail Pharmacies

10.6.8.3 Online Pharmacies

10.6.9 Historic and Forecast Market Size by Country

10.6.9.1 Turkiye

10.6.9.2 Bahrain

10.6.9.3 Kuwait

10.6.9.4 Saudi Arabia

10.6.9.5 Qatar

10.6.9.6 UAE

10.6.9.7 Israel

10.6.9.8 South Africa

10.7. South America Cephalosporin Drugs Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecasted Market Size By Generation

10.7.4.1 First Generation

10.7.4.2 Second Generation

10.7.4.3 Third Generation

10.7.4.4 Fourth Generation

10.7.4.5 Fifth Generation

10.7.5 Historic and Forecasted Market Size By Application

10.7.5.1 Hospital Use

10.7.5.2 Outpatient Use

10.7.5.3 Retail Pharmacies

10.7.6 Historic and Forecasted Market Size By Route of Administration

10.7.6.1 Oral

10.7.6.2 Parenteral

10.7.7 Historic and Forecasted Market Size By End-User

10.7.7.1 Hospitals

10.7.7.2 Clinics

10.7.7.3 Homecare

10.7.7.4 Others

10.7.8 Historic and Forecasted Market Size By Distribution Channel

10.7.8.1 Hospital Pharmacies

10.7.8.2 Retail Pharmacies

10.7.8.3 Online Pharmacies

10.7.9 Historic and Forecast Market Size by Country

10.7.9.1 Brazil

10.7.9.2 Argentina

10.7.9.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

11.1 Recommendations and Concluding Analysis

11.2 Potential Market Strategies

Chapter 12 Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

|

Global Cephalosporin Drugs Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 19.40 Billion |

|

Forecast Period 2024-32 CAGR: |

2.98% |

Market Size in 2032: |

USD 25.27 Billion |

|

Segments Covered: |

By Generation |

|

|

|

By Application |

|

||

|

By Route of Administration |

|

||

|

By End-User |

|

||

|

By Distribution |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||