Cane Sugar Market Synopsis:

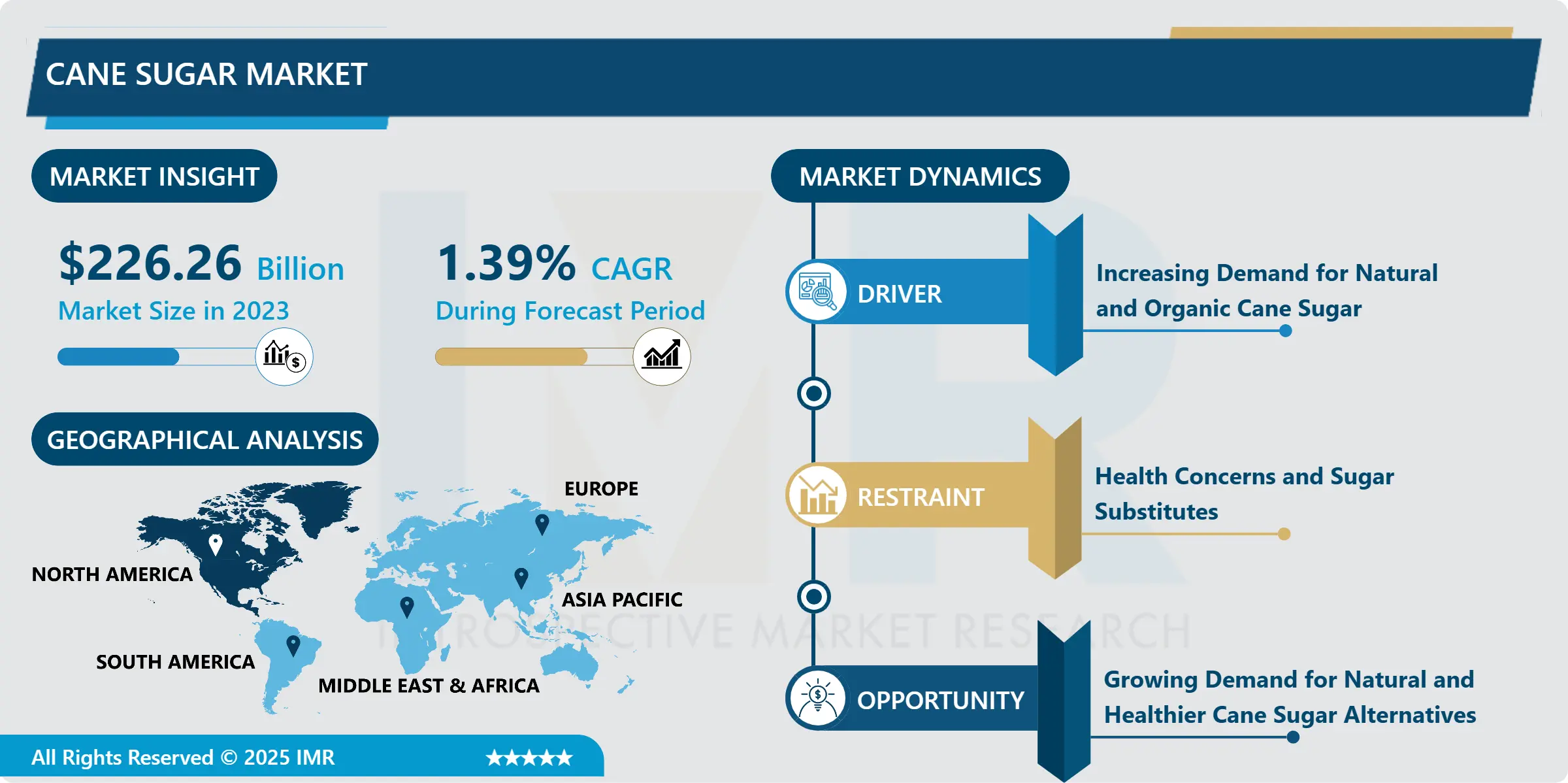

Cane Sugar Market Was Valued at USD 226.26 Billion in 2023 and is projected to reach USD 256.19 Billion by 2032, growing at a CAGR of 1.39 % from 2024 to 2032.

Cane sugar market is an umbrella ter salt that combines all the activities of providing raw material, processing, marketing and consumption of sugar produced from sugarcane, a warm climate grown plant. Tabel sugar also known as cane sugar can also be widely used in industries that are not related to foods and beverages like production of bio fuel and in pharmaceutical industries. This market entails products that are processed from raw raw sugar and it depends on factors such as agricultural production, climate, and government of policies and consumer pull towards organic sugar. Cane sugar has a paramount market importance in the global market and the leaders in the production of cane sugar are Brazil, India and China.

The cane sugar market has seen consistent growth over the years because of the many industries it applies to starting with food and drinks. Cane sugar is one of the most used sweeteners globally, and it is the best option when it comes to value for a host of products. The demand is triggered by the fact that cane sugar is a basic raw material requirements in food processing industries such as bakery, beverages, confectionaries as well as breweries and wineries. There has been a rising demand for consumption in processed foods and also increasing demand of natural products for sweeteners hence making cane sugar and important category in many consumer goods.

The cane sugar market has a number of risks, including, fluctuating prices of the raw materials, environmental issues by sugarcane farming, rise in the price of substitutes like high fructose corn syrup. Growth in customer concern about their health and increased awareness of the ill effects of using excessive sugar are also spurring the call for more low calorie sweeteners, organic and natural products as well as stevia or monk fruit. Consequently, such trends can affect the prospects for the development of the marketplace for the ordinary cane sugar, particularly in the developed world. However, Asia Pacific, Latin America and Africa market remains highly signed for expansion due to the increasing population, disposable income per capita and westernized diet.

Modernization is also evident in technologies of manufacturing and processing enabling market efficiencies and sustainability of cane sugar business. The companies are more concerned with strategies like using environmentally friendly practices, global accreditation of higher standard trade, and minimizing the impact of the effects of sugarcane farming on the environment. Added to this, consumers are become more environmentally conscious and are willing to purchase products from companies who follow socially responsible principles. With these dynamics, the global cane sugar market is expected to sustain its growth in the forecast period though the growth rate may differ in some regions because of tastes, economic and policies.

Cane Sugar Market Trend Analysis:

Increasing Demand for Natural and Organic Cane Sugar

-

The rise of natural and organic products is another trend outstanding in the cane sugar business. Since consumers are becoming more conscious with the kind of foods that they eat, they lose their taste for food with refined sugars since they know that it causes obesity, diabetes and heart disease. This change in the consumer attitude has forced people to develop a consumer pull towards natural sweeteners that are regarded as healthier products. Cane sugar in its relatively ‘natural’ forms is rapidly being regarded as superior to the more refined alternatives. Also, cane sugar is not as processed as the other types of sugars, therefore retains most, if not all of the nutrients which makes it ideal for purists in the food and drinks industry.

- Rising demand for organic cane sugar is also a reflection of the clean label products, where consumers seek minimally processed products with easily understood ingredients sourcing. Organic foods and beverages are increasingly in demand and this has called for manufactures to incorporate organic cane sugar in their foods and beverages. This trend is currently popular and mostly expressed in the food and beverages industry where customers are more likely to purchase foods produced from organic and sustainability sources. Equally, labels such as Fair Trade and Non-GMO have emerged as new selling propositions for the cane sugar, as such brands represent added quality for consumers interested in healthy lifestyles and environmental friendly products.

Growing Demand for Natural and Healthier Cane Sugar Alternatives

-

Some of the benefits found in the cane sugar market can be derived from the increasing global trends in natural and healthier products. The health conscious consumer is in fashion and products with little or no processing and additives are dominating the market. Cane sugar being more nature Friendly compared to refined sugar or any other artificial products in the market is used as a preference. This demand correlates with the general global concern for the quantity of artificial additives, chemicals in foods, thus playing into the hands of health conscious food and beverage factories to embrace natural sources of inputs. They also highlighted that cane sugar has better chances of finding a market among “ clean label ” products, where manufacturers promote the product’s origin, and transparent supply chain.

- Changes in consumers’ preferences are becoming key in shaping innovation for the global cane sugar market particularly in the low calorie and organic products. There is some innovation on more natural products like organic cane sugar for those consumers who are avoiding synthetic additives as they try to make healthier choices while not skipping sweeteners. It also means that cane sugar producer has an opportunity to address the call for healthier options while also creating new products that will bring in a new customer base. A continuing trend towards organic and morally sourced product also supports the cane sugar trend as a naturally favourable additive for both consumers and manufacturers.

Cane Sugar Market Segment Analysis:

Cane Sugar Market is Segmented on the basis of Category, Form, Application, and Region.

By Category, Organic segment is expected to dominate the market during the forecast period

-

Organic sugar and syrup products as a market segment are products derived from crops grown without the application of synthetic pesticides, fertilizers or genetically modified organisms. This segment is currently on the rise due to the people’s increasing concern with their health and the environment. Organic sugar and syrup are mostly considered healthier because they relatively undergo minimal processing, have no dangerous chemicals undergoing use. People consume organically produced foods not just because they want to avoid chemical processing of foods but also have become conscious of the harm done to environment by such production techniques.

- For some time now, consumers are choosing to buy environmentally friendly products and ingredients, and thus, the consumption of organic sugar and syrup will expand at a fast pace. This rise in demand is attributed to clean eating and a continuous enhancing of the market by retail and food service sectors of organic products. Traditionally, customers have sought goods that reflect their ideology, with the latest trend being organics and sustainable agriculture that promote health soil, buffer stock, and ecosystem. That is why the organic sugar and syrup segment is reaping from the said shift in consumer preferences, and it currently stands as one of the most vibrant and rapidly expanding segments of the sweetener industry.

By Application, Bakery & Confectionery segment expected to held the largest share

-

For any bakery and confectionery business, sugar and syrup only matter in terms of their functionality in a product as they are crucial for the product appeal and taste. In bakeries sugars are used for sweetness as well as the textural and moistening roles in cakes, cookies and pastry products. Sugar aids caramelization thus giving baked products their gold and tempting color, in addition to making them tender and light. Thirdly, sugar facilitates freshness by protecting these foods from spoiling; it also increases their longevity. The confectionery that includes candies and chocolates and gummies in particular, also uses sugar and syrup in them because of their sweet taste, gloss and uniformity that comes with it.

- Cake and sweet biscuit subsector has experienced a positive growth due to increased global consumption of confectionery products. Specifically, countries with developed snacking habits both during the daytime and at night time, that is North America, Europe and some parts of Asia are to be blamed for fuelling this growth because consumers are looking for indulgence yet convenience. Increased rate of indulgent snacking accompanied by growth in availability of new and interesting baked goods and confectionery products, contributed to increase consumption of sugar-based products. Over time, customers’ preferences for bakery products transition from standard to distinctive and gourmet, which elevates the need for better quality sugar and syrup for preparing these products.

Cane Sugar Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

-

North America has the biggest demand for cane sugar where it is used in the US especially in the food and beverages. While the newer and more appealing sugars such as the high-fructose corn syrup (HFCS) are common on the market, cane sugar remains on high demand by most people due to the natural assumption it comes with. New awareness regarding fresh sugar consumption due to growing obesity and diabetic concerns has resulted in higher codes and policies against sugar, thereby creating tribulations for the cane sugar market. However, there are many barriers that have not made bulk sugar derived from sugarcane irrelevant in product applications especially in drinks, bakery products and confectionery as taste and body are fundamental. Further, consumers are reading labels more and going for cleaner labels or products that feel more natural which also serves to drive consumption of cane sugar over other processed sugars.

- There are spot opportunities such as the current focused shift toward organic and non-GMO products in the USA market, which could help the cane sugar to foster new growth. Recent trends reveal that consumers are examining sweeteners according to their ideas of sustainability and health, and organic cane sugar is a growing component of this market. Trade relations and shifts in supply base and chains, especially with Latin America countries that are large producers of cane sugar similarly shape market. These overseas cane sugar supply agreements combined with changes in global production levels affect the prices and availabilities we see for cane sugar and further its competitiveness in North American markets. These are some key issues affecting the industry and as the world changes its preference for organic cane sugar, and regulates the use of sugar through policies, it creates the future market of the industry in the region.

Active Key Players in the Cane Sugar Market:

- Global Organics, Ltd.

- DO-IT Food Ingredients BV

- Louis Dreyfus Company B.V.

- Wilmar Sugar Australia Limited

- ASR Group International, Inc.

- Tate & Lyle plc

- Biosev S.A.

- 6.3.8 Nanning Sugar Industry

- Bunge Limited

- Raizen and Other Active Players

|

Global Cane Sugar Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 226.26 Billion |

|

Forecast Period 2024-32 CAGR: |

1.39% |

Market Size in 2032: |

USD 256.19 Billion |

|

Segments Covered: |

By Category |

|

|

|

By Form |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Cane Sugar Market by Category

4.1 Cane Sugar Market Snapshot and Growth Engine

4.2 Cane Sugar Market Overview

4.3 Organic and Conventional

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

4.3.3 Key Market Trends, Growth Factors and Opportunities

4.3.4 Organic and Conventional: Geographic Segmentation Analysis

Chapter 5: Cane Sugar Market by Form

5.1 Cane Sugar Market Snapshot and Growth Engine

5.2 Cane Sugar Market Overview

5.3 Crystallized sugar and Liquid syrup

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

5.3.3 Key Market Trends, Growth Factors and Opportunities

5.3.4 Crystallized sugar and Liquid syrup: Geographic Segmentation Analysis

Chapter 6: Cane Sugar Market by Application

6.1 Cane Sugar Market Snapshot and Growth Engine

6.2 Cane Sugar Market Overview

6.3 Bakery & Confectionery

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.3.3 Key Market Trends, Growth Factors and Opportunities

6.3.4 Bakery & Confectionery: Geographic Segmentation Analysis

6.4 Dairy

6.4.1 Introduction and Market Overview

6.4.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.4.3 Key Market Trends, Growth Factors and Opportunities

6.4.4 Dairy: Geographic Segmentation Analysis

6.5 Beverages and Other Applications

6.5.1 Introduction and Market Overview

6.5.2 Historic and Forecasted Market Size in Value USD and Volume Units (2017-2032F)

6.5.3 Key Market Trends, Growth Factors and Opportunities

6.5.4 Beverages and Other Applications: Geographic Segmentation Analysis

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Cane Sugar Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 GLOBAL ORGANICS

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 LTD.

7.4 DO-IT FOOD INGREDIENTS BV

7.5 LOUIS DREYFUS COMPANY B.V.

7.6 WILMAR SUGAR AUSTRALIA LIMITED

7.7 ASR GROUP INTERNATIONAL INC.

7.8 TATE & LYLE PLC

7.9 BIOSEV S.A.

7.10 6.3.8 NANNING SUGAR INDUSTRY

7.11 BUNGE LIMITED

7.12 RAIZEN

7.13 OTHER ACTIVE PLAYERS

Chapter 8: Global Cane Sugar Market By Region

8.1 Overview

8.2. North America Cane Sugar Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size By Category

8.2.4.1 Organic and Conventional

8.2.5 Historic and Forecasted Market Size By Form

8.2.5.1 Crystallized sugar and Liquid syrup

8.2.6 Historic and Forecasted Market Size By Application

8.2.6.1 Bakery & Confectionery

8.2.6.2 Dairy

8.2.6.3 Beverages and Other Applications

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Cane Sugar Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size By Category

8.3.4.1 Organic and Conventional

8.3.5 Historic and Forecasted Market Size By Form

8.3.5.1 Crystallized sugar and Liquid syrup

8.3.6 Historic and Forecasted Market Size By Application

8.3.6.1 Bakery & Confectionery

8.3.6.2 Dairy

8.3.6.3 Beverages and Other Applications

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Cane Sugar Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size By Category

8.4.4.1 Organic and Conventional

8.4.5 Historic and Forecasted Market Size By Form

8.4.5.1 Crystallized sugar and Liquid syrup

8.4.6 Historic and Forecasted Market Size By Application

8.4.6.1 Bakery & Confectionery

8.4.6.2 Dairy

8.4.6.3 Beverages and Other Applications

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Cane Sugar Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size By Category

8.5.4.1 Organic and Conventional

8.5.5 Historic and Forecasted Market Size By Form

8.5.5.1 Crystallized sugar and Liquid syrup

8.5.6 Historic and Forecasted Market Size By Application

8.5.6.1 Bakery & Confectionery

8.5.6.2 Dairy

8.5.6.3 Beverages and Other Applications

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Cane Sugar Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size By Category

8.6.4.1 Organic and Conventional

8.6.5 Historic and Forecasted Market Size By Form

8.6.5.1 Crystallized sugar and Liquid syrup

8.6.6 Historic and Forecasted Market Size By Application

8.6.6.1 Bakery & Confectionery

8.6.6.2 Dairy

8.6.6.3 Beverages and Other Applications

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Cane Sugar Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size By Category

8.7.4.1 Organic and Conventional

8.7.5 Historic and Forecasted Market Size By Form

8.7.5.1 Crystallized sugar and Liquid syrup

8.7.6 Historic and Forecasted Market Size By Application

8.7.6.1 Bakery & Confectionery

8.7.6.2 Dairy

8.7.6.3 Beverages and Other Applications

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Cane Sugar Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 226.26 Billion |

|

Forecast Period 2024-32 CAGR: |

1.39% |

Market Size in 2032: |

USD 256.19 Billion |

|

Segments Covered: |

By Category |

|

|

|

By Form |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||