Beer Processing Market Synopsis

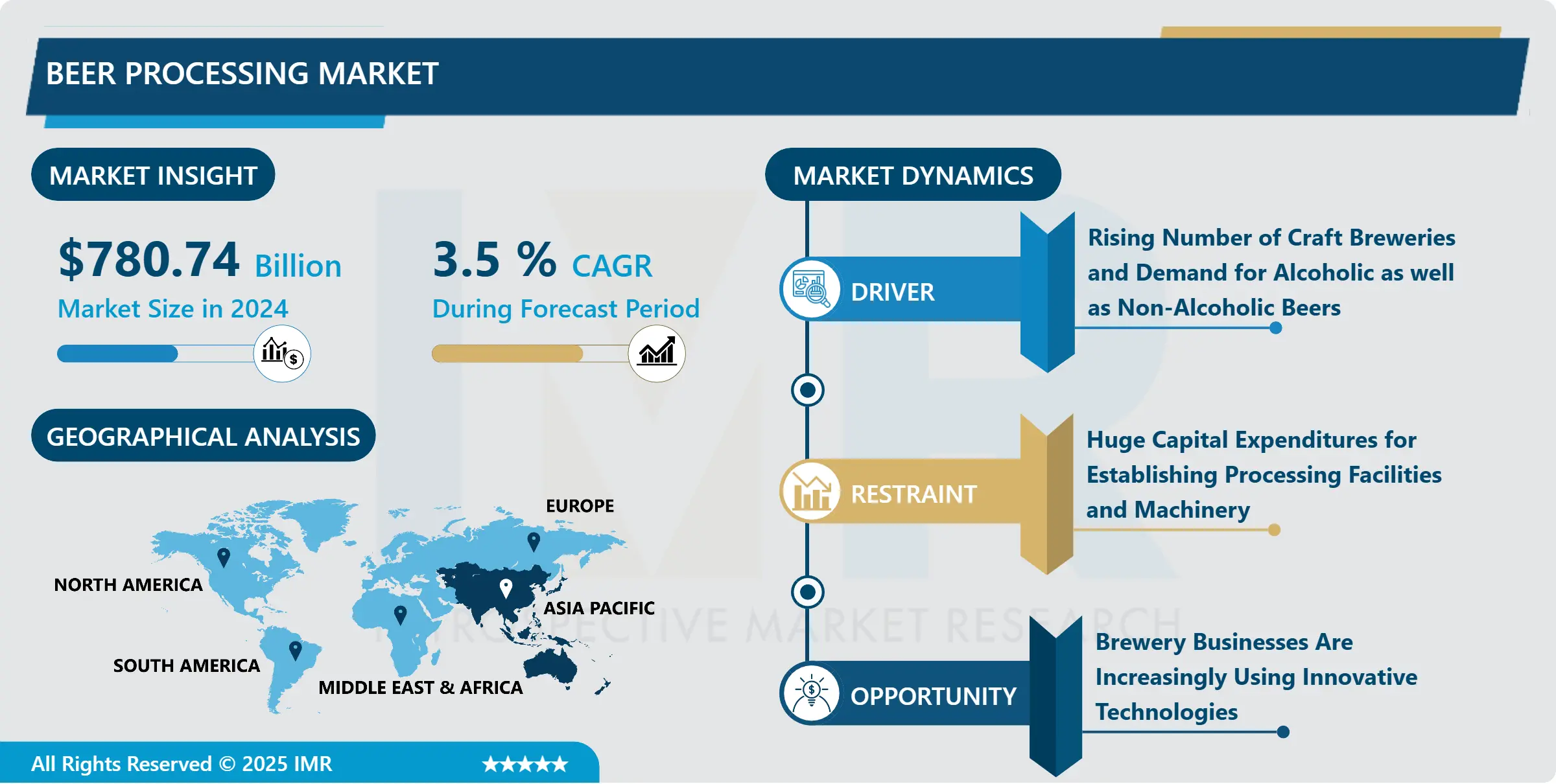

Beer Processing Market Size Was Valued at USD 780.74 Billion in 2024 and is Projected to Reach USD 1028.09 Billion by 2032, Growing at a CAGR of 4.1 % From 2025-2032.

Beer, the oldest and most widely consumed alcoholic beverage, is crafted through the extraction and fermentation of raw materials, primarily malted cereal grains, and hops. The brewing process, crucial to shaping the beer's variety and flavor, involves manipulating key variables. Across the globe, laws often define beer production standards, emphasizing ingredients like malt, hops, and yeast.

The landscape of beer processing underwent a transformative shift during the Industrial Revolution, introducing mechanization that provided enhanced control over the brewing process. Innovations such as the thermometer and saccharometer played pivotal roles. Originating in Britain, beer production techniques spread worldwide, and advancements in refrigeration technology in the late 19th century facilitated the brewing of lager beers even in summer.

The beer processing journey encompasses several sequential steps, including malting, milling, mashing, lautering, wort boiling, wort clarification, fermentation, storage, filtration, and filling. As the beer industry evolves, new trends emerge, leading to the creation of non-alcoholic and fruit-based beer varieties. Today, these innovations are highly favored in the market.

According to Statista, approximately 41% of alcohol consumers cite beer as their preferred beverage, surpassing a diverse range of wines, spirits, and liquors. The growing popularity of beer, attributed to its diverse flavors and widespread adoption in social settings, is driving increased demand for the Beer Processing Industry.

Beer Processing Market Trend Analysis

Beer Processing Market Drivers- Rising Number of Craft Breweries and Demand for Alcoholic as well as Non-Alcoholic Beers

- In recent years, the dynamics of beer supply and consumption have undergone significant transformations to meet the escalating demand from traditional, craft, and microbreweries. Craft breweries, characterized by their use of traditional ingredients and methods, as well as microbreweries, known for lower-volume production, have emerged as influential players in sustaining market expansion.

- These newer brewery models specialize in offering premium and innovatively flavored beers tailored to consumer preferences. Despite being relatively more expensive than conventional beers, the market is witnessing growth driven by the heightened demand for these distinctive brews, thereby boosting overall revenue. Notably, in 2020, over 100 new flavored beers were introduced for retail sales, constituting 40% of total launches in the flavored alcohol category.

- Craft beer enthusiasts have showcased their affinity for exploring novel and intricate flavor profiles, exemplified by choices like Avocado Honey Ale or Coconut Curry Hefeweizen in the past year. This inclination reflects a clear market demand for unique and innovative flavored beers, propelling the market share of microbreweries and craft breweries.

Beer Processing Market Opportunities- Brewery Businesses Are Increasingly Using Innovative Technologies Like Automation, Artificial Intelligence, and the Internet of Things (IoT)

- The most changes have been made to the beer industry than to any other alcoholic beverage over the past three decades as the world has quickly moved toward the future.

- The industry did, however, undergo significant changes in distribution, process management, and digitization. The methods of processing beer have been entirely improved by the adoption of cutting-edge technologies. Internet of Things (IoT)-based technologies are expected to have a positive impact on beer distribution and processing, including delivery and consumption. Smaller and craft breweries are now adopting similar digital upgrades that were initially introduced by larger brewers.

- These improvements are probably the result of the growth of smaller brew houses and craft breweries around the globe. These brewers also don't mind starting trends in the industry by sharing knowledge, which presents small breweries with a great chance to become more efficient through the use of technology.

- Furthermore, quality and product differentiation are crucial in providing consumers with the beer styles they want, which will support the industry's growth in the coming years.

Beer Processing Market Segment Analysis:

The beer Processing Market is Segmented on the basis of Beer Type, Brewery Type, and Price Category.

By Brewery Type, the Craft Brewery segment is expected to dominate the market during the forecast period

- Craft beer is not a new concept; it has been growing steadily for more than ten years, and its popularity has been increasing globally, allowing craft breweries to meet this growing demand. The majority of communities and neighborhoods adore craft breweries because they provide new venues for locals and tourists to congregate and savor a taste of their traditional beer.

- Even though demand for craft beer has decreased over the last few years, the category is still growing extremely popular despite its slower rate of expansion. To put it another way, the United States alone saw an 8% increase in craft brewer volume sales last year, while overall beer volume sales increased by 1%. This suggests that the proportion of small and independent brewers in the nation is increasing.

- Additionally, Craft Breweries, with their alluring advantages, contribute significantly to a nation's economy, which is a major factor in the segment's growth. The craft beer market is predicted to grow steadily in the upcoming years due to its contributions to the tax base, employment, and emphasis on flavor rather than intoxication.

By Beer Type, the Lager segment held the largest share in 2024

- Lager stands as the undisputed giant in the beer processing market, commanding a substantial 57.5% share, making it the preeminent player in the industry. Its dominance can be attributed to a confluence of factors that have collectively propelled Lager to the forefront of the market. With roots tracing back centuries to Germany and Central Europe, Lager boasts a rich history, establishing itself as a globally beloved beverage. Renowned for its clean, crisp, and refreshing taste achieved through a meticulous bottom-fermentation process, Lager appeals to a diverse consumer base.

- One of Lager's key strengths lies in its mass production efficiency, resulting in lower production costs and more affordable pricing, a factor that has significantly contributed to its widespread popularity. Furthermore, Lager's global appeal spans continents, from Europe and North America to Asia and South America, solidifying its dominant market position. The Lager segment's diversity, encompassing sub-styles such as Pilsners, Helles, Dunkel, Bock, and Vienna Lager, further strengthens its market standing by catering to various taste preferences.

- The growing trend toward premium Laggers, brewed with high-quality ingredients and offering a more complex flavor profile, attests to Lager's adaptability and ability to cater to evolving consumer preferences. In essence, Lager's multifaceted appeal, historical significance, and adaptability have collectively positioned it as the unparalleled leader in the beer processing market, likely to maintain its dominance well into the foreseeable future.

Beer Processing Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast Period

- The market is dominated by Asia Pacific, and this trend is anticipated to continue throughout the forecast period. In addition to having the largest general market in the world, Asia is also home to the world's fastest-growing beer market and the most intelligent breweries. Due to their vast customer base, developing economies, and modernization, these breweries are seizing incredible opportunities.

- Around 50% of the world's beer consumption currently occurs in the Asia Pacific region, with the remaining 17.1% coming from Europe and the remaining 8.7% from North America. As a result, APAC has higher beer sales than any other region, which benefits the region's beer processing companies as well.

- The Asia-Pacific region is poised to dominate the Beer Processing market over the forecast period, driven by robust export performances of major players like China and Thailand. China, with beer exports nearing 327 million U.S. dollars in 2022, leads the market, followed closely by Thailand, contributing over 111.5 million U.S. dollars. This trend underscores the region's significant role in the global beer market, with sustained growth anticipated in the coming years.

Beer Processing Market Top Key Players:

- Boston Beer Company Inc. (USA)

- New Belgium Brewing Company (USA)

- Sierra Nevada Brewing Company (USA)

- D.G. Yuengling & Son, Inc. (USA)

- Constellation Brands, Inc. (USA)

- Molson Coors Beverage Company (USA)

- Stone Brewing (USA)

- Dogfish Head Craft Brewery (USA)

- Brooklyn Brewery (USA)

- Bell's Brewery (USA)

- Brewster's Brewery (Canada)

- Grupo Modelo(Mexico)

- Anheuser-Busch InBev (Belgium)

- Heineken N.V. (Netherlands)

- Duvel Moortgat (Belgium)

- Carlsberg Group (Denmark)

- Diageo PLC (UK)

- BrewDog (UK)

- Pilsner Urquell (Czech Republic)

- China Resources Snow Breweries (China)

- Asahi Group Holdings, Ltd. (Japan)

- Tsingtao Brewery Co., Ltd. (China)

- Kirin Holdings Company, Limited (Japan)

- BGI-Shenzhen (China) and Other Active players.

Key Industry Developments in the Beer Processing Market:

- In August 2023, Tilray Brands, Inc. a leading global cannabis-lifestyle and consumer packaged goods company, announced that the Company has entered into a definitive agreement to acquire eight beer and beverage brands from Anheuser-Busch (NYSE: BUD). Upon satisfaction of customary closing conditions, Tilray will acquire Shock Top, Breckenridge Brewery, Blue Point Brewing Company, 10 Barrel Brewing Company, Redhook Brewery, Widmer Brothers Brewing, Square Mile Cider Company, and HiBall Energy. The transaction includes current employees, breweries, and brewpubs associated with these brands.

- In April 2023, IFF announced the launch of its new enzymatic solution that allows breweries to maintain the clarity of beer with a smarter, simplified process. By using BCLEAR™, breweries can achieve a more cost-efficient and robust stabilization process, compared to other enzymatic solutions. When switching to BCLEAR™ from traditional methods of stabilization, breweries can simplify the beer-making process, whilst increasing their energy and water savings. Additionally, unlike non-enzymatic solutions, BCLEAR™ improves foam stability in the beer and reduces gluten content.

|

Beer Processing Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 780.74 Billion. |

|

Forecast Period 2024-32 CAGR: |

3.5 % |

Market Size in 2032: |

USD 1082.99 Billion. |

|

Segments Covered: |

By Beer Type |

|

|

|

By Application |

|

||

|

By Price Category |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Beer Processing Market by Beer Type (2018-2032)

4.1 Beer Processing Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Ale & Stout

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Lager

4.5 Porter

4.6 Specialty Beers

4.7 Others

Chapter 5: Beer Processing Market by Application (2018-2032)

5.1 Beer Processing Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Macrobrewery

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Microbrewery

5.5 Craft Brewery

5.6 Brew Pubs

5.7 Others

Chapter 6: Beer Processing Market by Price Category (2018-2032)

6.1 Beer Processing Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Standard

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Premium

6.5 Super-Premium

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Beer Processing Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 CONSTELLATION BRANDS (US)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 MOLSON COORS BEVERAGE COMPANY (US)

7.4 CANNABINIERS (US)

7.5 DIXIE BRANDS INC. (US)

7.6 CANNABINOID CREATIONS (US)

7.7 COALITION BREWING CO. (US)

7.8 CERIA BEVERAGES (US)

7.9 TWO ROOTS BREWING CO. (US)

7.10 LAGUNITAS BREWING COMPANY (HEINEKEN-OWNED) (US)

7.11 KEITH VILLA'S CERIA BREWING CO. (US)

7.12 EVERGREEN HERBAL (US)

7.13 REBEL COAST WINERY (US)

7.14 MIRTH PROVISIONS (US)

7.15 LEAFBUYER TECHNOLOGIES INC. (US)

7.16 GREEN THUMB INDUSTRIES INC. (US)

7.17 CANOPY GROWTH CORPORATION (CANADA)

7.18 CANOPY RIVERS INC. (CANADA)

7.19 TILRAY INC. (CANADA)

7.20 THE SUPREME CANNABIS COMPANY (CANADA)

7.21 CANNTRUST HOLDINGS INC. (CANADA)

7.22 PROVINCE BRANDS OF CANADA (CANADA)

7.23 AURORA CANNABIS INC. (CANADA)

7.24 THE GREEN ORGANIC DUTCHMAN HOLDINGS LTD. (TGOD) (CANADA)

7.25 HEXO CORP (CANADA)

7.26 BLAZE LIFE HOLDINGS (BLH) (CALIFORNIA)

7.27 HEINEKEN (NETHERLANDS)

7.28

Chapter 8: Global Beer Processing Market By Region

8.1 Overview

8.2. North America Beer Processing Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Beer Type

8.2.4.1 Ale & Stout

8.2.4.2 Lager

8.2.4.3 Porter

8.2.4.4 Specialty Beers

8.2.4.5 Others

8.2.5 Historic and Forecasted Market Size by Application

8.2.5.1 Macrobrewery

8.2.5.2 Microbrewery

8.2.5.3 Craft Brewery

8.2.5.4 Brew Pubs

8.2.5.5 Others

8.2.6 Historic and Forecasted Market Size by Price Category

8.2.6.1 Standard

8.2.6.2 Premium

8.2.6.3 Super-Premium

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Beer Processing Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Beer Type

8.3.4.1 Ale & Stout

8.3.4.2 Lager

8.3.4.3 Porter

8.3.4.4 Specialty Beers

8.3.4.5 Others

8.3.5 Historic and Forecasted Market Size by Application

8.3.5.1 Macrobrewery

8.3.5.2 Microbrewery

8.3.5.3 Craft Brewery

8.3.5.4 Brew Pubs

8.3.5.5 Others

8.3.6 Historic and Forecasted Market Size by Price Category

8.3.6.1 Standard

8.3.6.2 Premium

8.3.6.3 Super-Premium

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Beer Processing Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Beer Type

8.4.4.1 Ale & Stout

8.4.4.2 Lager

8.4.4.3 Porter

8.4.4.4 Specialty Beers

8.4.4.5 Others

8.4.5 Historic and Forecasted Market Size by Application

8.4.5.1 Macrobrewery

8.4.5.2 Microbrewery

8.4.5.3 Craft Brewery

8.4.5.4 Brew Pubs

8.4.5.5 Others

8.4.6 Historic and Forecasted Market Size by Price Category

8.4.6.1 Standard

8.4.6.2 Premium

8.4.6.3 Super-Premium

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Beer Processing Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Beer Type

8.5.4.1 Ale & Stout

8.5.4.2 Lager

8.5.4.3 Porter

8.5.4.4 Specialty Beers

8.5.4.5 Others

8.5.5 Historic and Forecasted Market Size by Application

8.5.5.1 Macrobrewery

8.5.5.2 Microbrewery

8.5.5.3 Craft Brewery

8.5.5.4 Brew Pubs

8.5.5.5 Others

8.5.6 Historic and Forecasted Market Size by Price Category

8.5.6.1 Standard

8.5.6.2 Premium

8.5.6.3 Super-Premium

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Beer Processing Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Beer Type

8.6.4.1 Ale & Stout

8.6.4.2 Lager

8.6.4.3 Porter

8.6.4.4 Specialty Beers

8.6.4.5 Others

8.6.5 Historic and Forecasted Market Size by Application

8.6.5.1 Macrobrewery

8.6.5.2 Microbrewery

8.6.5.3 Craft Brewery

8.6.5.4 Brew Pubs

8.6.5.5 Others

8.6.6 Historic and Forecasted Market Size by Price Category

8.6.6.1 Standard

8.6.6.2 Premium

8.6.6.3 Super-Premium

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Beer Processing Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Beer Type

8.7.4.1 Ale & Stout

8.7.4.2 Lager

8.7.4.3 Porter

8.7.4.4 Specialty Beers

8.7.4.5 Others

8.7.5 Historic and Forecasted Market Size by Application

8.7.5.1 Macrobrewery

8.7.5.2 Microbrewery

8.7.5.3 Craft Brewery

8.7.5.4 Brew Pubs

8.7.5.5 Others

8.7.6 Historic and Forecasted Market Size by Price Category

8.7.6.1 Standard

8.7.6.2 Premium

8.7.6.3 Super-Premium

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Beer Processing Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 780.74 Billion. |

|

Forecast Period 2024-32 CAGR: |

3.5 % |

Market Size in 2032: |

USD 1082.99 Billion. |

|

Segments Covered: |

By Beer Type |

|

|

|

By Application |

|

||

|

By Price Category |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||