Automotive Powertrain Market Synopsis:

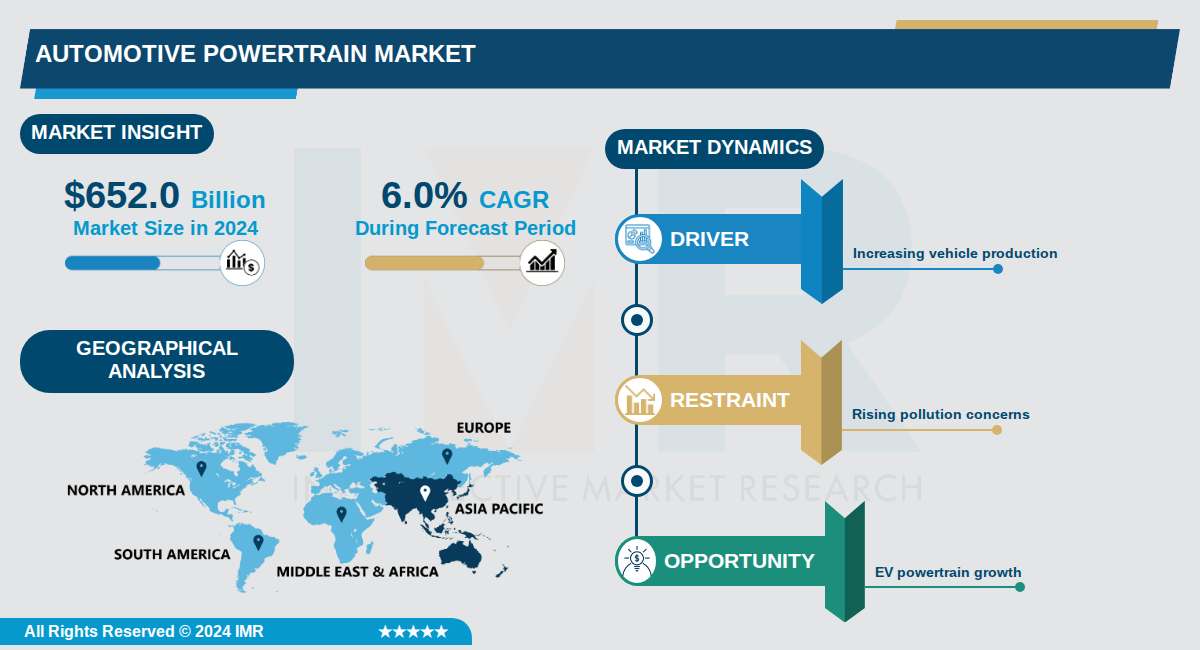

Automotive Powertrain Market Size Was Valued at USD 652.0 Billion in 2024, and is Projected to Reach USD 1.26 Trillion by 2035, Growing at a CAGR of 6.0% From 2024-2035.

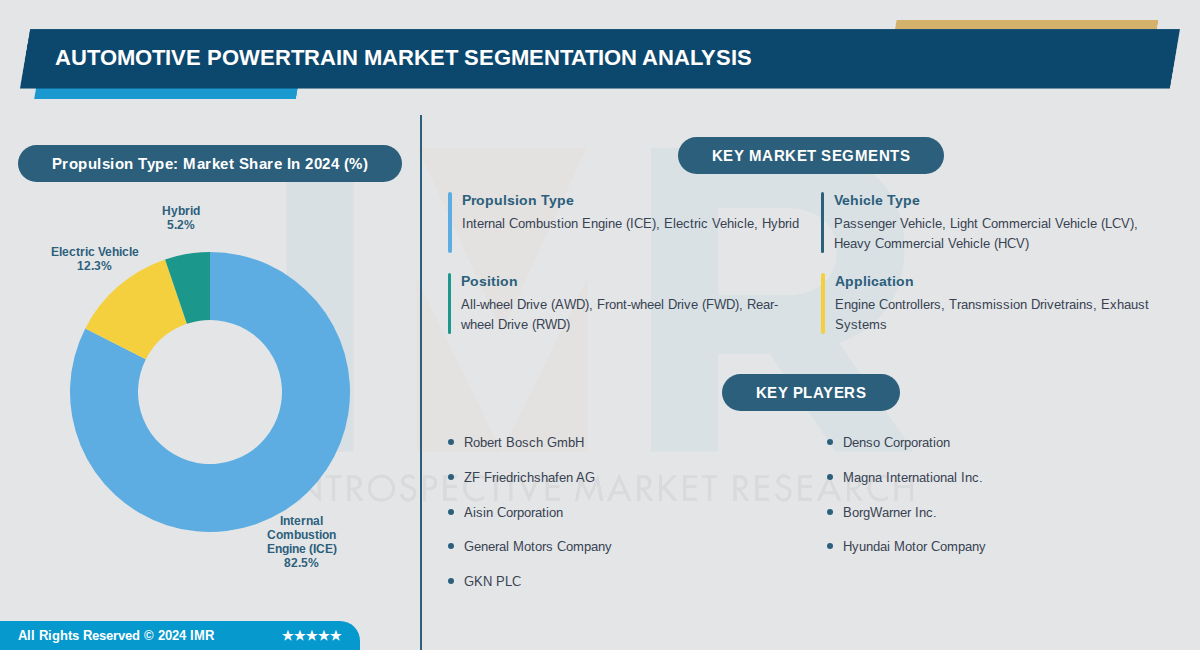

The global automotive powertrain market was valued at $652.0 billion in 2024 and is projected to reach $1.26 trillion by 2035, growing at a compound annual growth rate (CAGR) of 6.0%. This expansion reflects the ongoing evolution of vehicle propulsion systems amid shifting consumer preferences and regulatory pressures. Powertrains, which transmit power from the engine to the wheels, encompass internal combustion engines (ICE), electric vehicles (EV), and hybrids, with ICE still dominating at around 70% market share in 2024 while EV segments rapidly gain traction.

Passenger vehicles lead the market with approximately 75% share in 2024, driven by high global demand, though commercial vehicles are the fastest-growing segment due to fleet modernization and logistics needs. Regionally, Asia-Pacific commands the largest portion at 45%, fueled by manufacturing hubs in China, Japan, India, and South Korea, alongside rising middle-class incomes and urbanization. North America follows with 25% share, bolstered by innovation and EV adoption.

Market projections vary across sources, with some estimating higher growth to $4,605 billion by 2034 at a 15.8% CAGR, highlighting robust demand for advanced powertrains including lightweight materials, multi-speed transmissions, and AI integration. Discrepancies underscore the influence of electrification trends, where EV powertrains are expected to surge from 30% share in 2024. Overall, the sector balances legacy ICE dominance with a pivot toward sustainable technologies.

Automotive Powertrain Market Trend Analysis:

Rapid Electrification of Powertrains

- The electric vehicle segment in the automotive powertrain market is projected to grow at a CAGR of 28.13% through 2035, driven by surging global EV sales and innovations like silicon-carbide inverters and integrated e-axles. In Europe, 3.2 million electric cars were registered in 2023, marking a 20% increase from 2022, fueled by policies such as the European Green Deal. Skoda launched its Enyaq and Enyaq Coupe SUVs in January 2025 with enhanced Enyaq 60 powertrains featuring larger batteries and more power for better range and performance.

- BEV powertrains are focusing on cost reduction through high-silicon anodes, LFP chemistries, and oil-cooled e-motors, enabling major range gains via thermal integration of batteries, motors, and inverters. Ramkrishna Forgings Ltd. secured approval in April 2024 to supply powertrain components to the U.S.'s largest electric passenger vehicle producer, highlighting supply chain shifts toward EV demands. In Asia-Pacific, which held 62% market share in 2025, local production of batteries and motors supports rapid BEV adoption in compact segments.

Rise of Hybrid Powertrain Architectures

- Hybrids are scaling as bridge technologies with high-efficiency Atkinson engines, dedicated hybrid transmissions, and compact e-axles, delivering urban efficiency without range anxiety where charging infrastructure lags. They serve as a profit and compliance backbone, especially in North America where pickup and SUV mixes favor efficient turbo ICE hybrids for towing. Globally, hybrids hold steady in consumer preferences amid muted EV interest in the U.S., with multi-energy platforms sharing EDU packages and high-voltage components to reduce costs.

- In Europe, tight emissions norms push hybrids alongside BEVs, emphasizing modular e-axles and compact DHTs for new platforms. Asia-Pacific sees broad hybrid penetration due to scale advantages and value-engineered components, supporting export programs adaptable to diverse markets. Ford and GM are positioning hybrids to capitalize on potential changes in fuel economy standards, bridging toward broader EV adoption.

Adoption of Multi-Energy Modular Platforms

- Automakers are re-platforming around modular architectures that support ICE, hybrid, and BEV configurations, sharing bodies-in-white, EDU packages, and high-voltage components to cut tooling costs and speed launches. These flexible platforms win scale by meeting diverse regulations and price points, with right-sizing for segments like small cars using LFP front e-axles or trucks with high-power e-PTOs. In Asia-Pacific, strong local supply bases for inverters and motors accelerate this trend in kei and mini EVs.

- Efficiency gains come from system-level optimizations like low-loss driveline bearings, e-oil pumps, and software-defined energy management for OTA upgrades. Circularity is gaining traction with remanufactured e-axles and second-life batteries influencing fleet tenders. Europe's urban policies and North America's fleet adoptions of BEV vans further drive standardization of software stacks for diagnostics and cybersecurity.

Automotive Powertrain Market Segment Analysis:

Automotive Powertrain Market is Segmented on the basis of By Propulsion Type, By Vehicle Type, By Position

By Propulsion Type, Internal Combustion Engine (ICE) segment is expected to dominate the market during the forecast period

- ICE dominates due to its established global infrastructure, lower upfront costs, and widespread consumer familiarity with conventional vehicles.

- ICE holds over 80% market share as it powers the majority of existing vehicle fleets and continues strong sales in emerging markets like Asia Pacific.

By Vehicle Type, Passenger Vehicle segment is expected to dominate the market during the forecast period

- Passenger vehicles lead due to high global production volumes, rising personal ownership rates, and rapid adoption of new powertrain technologies.

- They account for over 75% of the market driven by urban population growth and consumer demand in regions like Asia Pacific and Europe.

By Position, All-wheel Drive (AWD) segment is expected to dominate the market during the forecast period

- AWD dominates due to superior traction, stability, and performance benefits, especially in SUVs and performance vehicles gaining popularity.

- Increasing demand for premium and off-road capable vehicles worldwide has propelled AWD to the largest revenue share with highest growth rate.

By Application, Engine Controllers segment is expected to dominate the market during the forecast period

- Engine controllers lead as they are critical for power management, efficiency optimization, and integration with advanced electronics in modern vehicles.

- Dominance stems from their essential role in both ICE and electrified powertrains, with high demand from regulatory emissions compliance.

Automotive Powertrain Market Regional Insights:

Asia Pacific Dominates the Automotive Powertrain Market with the Largest Share

- Asia Pacific holds the dominant position in the automotive powertrain market, commanding over 62% market share in 2025 and projected to grow significantly through 2035. Key countries like China, India, Japan, and South Korea drive this leadership due to massive vehicle production volumes, with China alone seeing a 5.7% rise in car production to 2.84 million units in 2022. This region's scale ensures it remains the largest revenue contributor over the forecast period.

- The dominance is fueled by robust infrastructure for automotive manufacturing, surging demand for automated transmissions, and supportive government policies. In China and India, rising consumer purchasing power and urbanization boost sales of advanced vehicles requiring upgraded powertrains. Energy-saving programs like China's New Energy Vehicle initiative further accelerate adoption of electrified systems amid rapid economic growth.

- Major players benefit from the region's manufacturing hubs, with significant developments in electric vehicle powertrains. High production in Japan and South Korea supports global supply chains, while India's expanding middle class drives passenger vehicle demand. Recent trends show exponential growth in EV and hybrid segments, positioning Asia Pacific companies at the forefront of innovation.

Active Key Players in the Automotive Powertrain Market:

- Robert Bosch GmbH (Germany)

- Denso Corporation (Japan)

- ZF Friedrichshafen AG (Germany)

- Magna International Inc. (Canada)

- Aisin Corporation (Japan)

- BorgWarner Inc. (USA)

- General Motors Company (USA)

- Hyundai Motor Company (South Korea)

- GKN PLC (UK)

- Toyota Motor Corporation (Japan)

- Volkswagen AG (Germany)

- Ford Motor Company (USA)

- Continental AG (Germany)

- Dana Incorporated (USA)

- JTEKT Corporation (Japan)

- Mitsubishi Electric Corp (Japan)

- AVL List GmbH (Austria)

- Bonfiglioli Riduttori S.P.A (Italy)

- Other Active Players

|

Automotive Powertrain Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 652.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 1.26 Trillion |

|

Segments Covered: |

By Propulsion Type |

|

|

|

By Vehicle Type |

|

||

|

By Position |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Automotive Powertrain Market by Propulsion Type (2017-2035)

4.1 Automotive Powertrain Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Internal Combustion Engine (ICE)

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Electric Vehicle

4.5 Hybrid

Chapter 5: Automotive Powertrain Market by Vehicle Type (2017-2035)

5.1 Automotive Powertrain Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Passenger Vehicle

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Light Commercial Vehicle (LCV)

5.5 Heavy Commercial Vehicle (HCV)

Chapter 6: Automotive Powertrain Market by Position (2017-2035)

6.1 Automotive Powertrain Market Snapshot and Growth Engine

6.2 Market Overview

6.3 All-wheel Drive (AWD)

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Front-wheel Drive (FWD)

6.5 Rear-wheel Drive (RWD)

Chapter 7: Automotive Powertrain Market by Application (2017-2035)

7.1 Automotive Powertrain Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Engine Controllers

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Transmission Drivetrains

7.5 Exhaust Systems

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Automotive Powertrain Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 ROBERT BOSCH GMBH

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 DENSO CORPORATION

8.4 ZF FRIEDRICHSHAFEN AG

8.5 MAGNA INTERNATIONAL INC.

8.6 AISIN CORPORATION

8.7 BORGWARNER INC.

8.8 GENERAL MOTORS COMPANY

8.9 HYUNDAI MOTOR COMPANY

8.10 GKN PLC

8.11 TOYOTA MOTOR CORPORATION

8.12 VOLKSWAGEN AG

8.13 FORD MOTOR COMPANY

8.14 CONTINENTAL AG

8.15 DANA INCORPORATED

8.16 JTEKT CORPORATION

8.17 MITSUBISHI ELECTRIC CORP

8.18 AVL LIST GMBH

8.19 BONFIGLIOLI RIDUTTORI S.P.A

Chapter 9: Global Automotive Powertrain Market By Region

9.1 Overview

9.2. North America Automotive Powertrain Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Automotive Powertrain Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Automotive Powertrain Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Automotive Powertrain Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Automotive Powertrain Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Automotive Powertrain Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Automotive Powertrain Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 652.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

6.0 % |

Market Size in 2035: |

USD 1.26 Trillion |

|

Segments Covered: |

By Propulsion Type |

|

|

|

By Vehicle Type |

|

||

|

By Position |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||