Automotive Metal Stamping Market Synopsis:

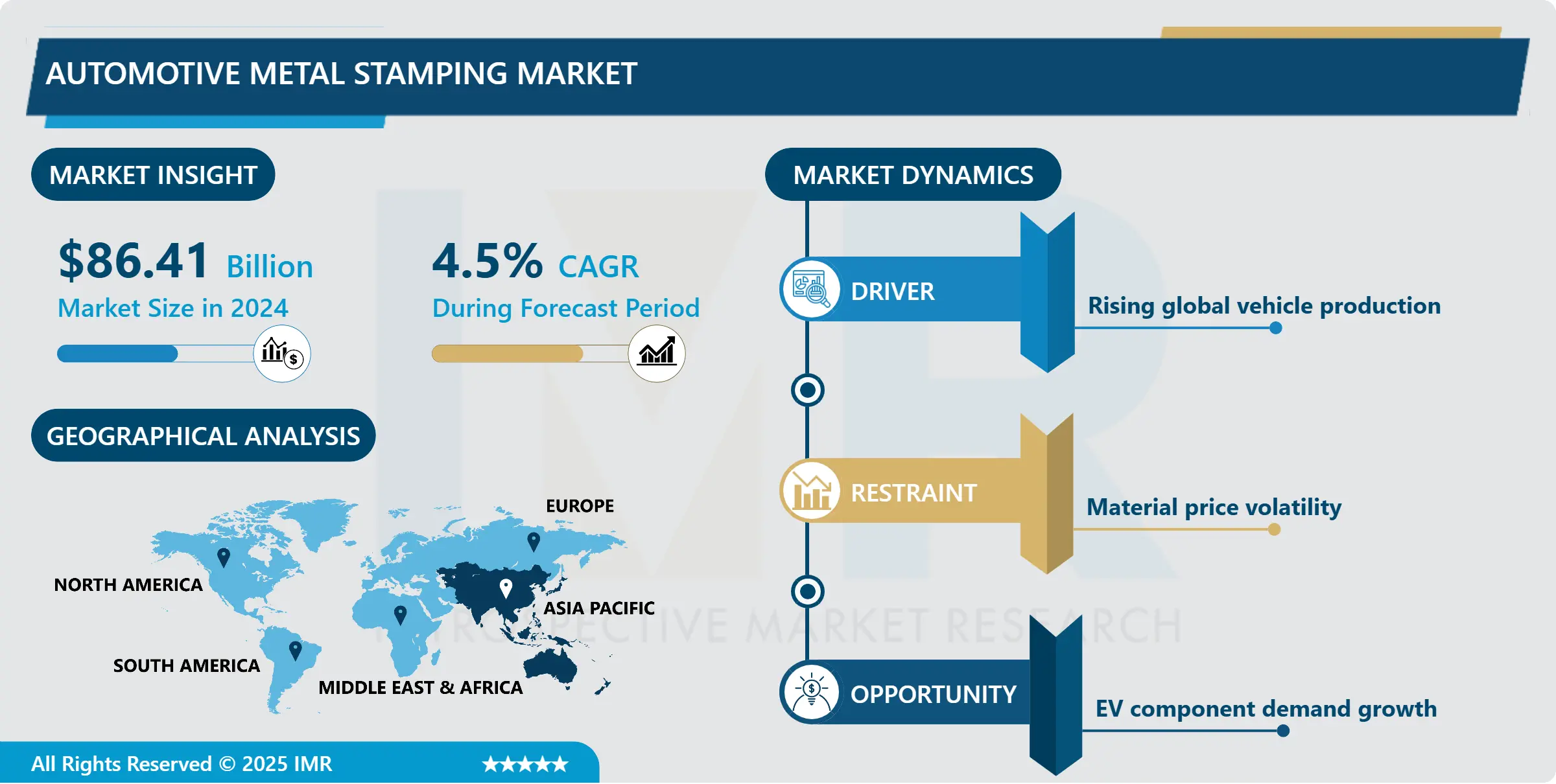

Automotive Metal Stamping Market Size Was Valued at USD 86.41 Billion in 2024, and is Projected to Reach USD 140.23 Billion by 2035, Growing at a CAGR of 4.5% From 2024-2035.

The Automotive Metal Stamping Market is valued at $86.41 billion in 2024 but is projected to decline slightly to $140.23 billion by 2035, reflecting a compound annual growth rate (CAGR) of -4.5%. This stagnation contrasts with optimistic forecasts from industry reports, which predict growth to between $113 billion and $163 billion by similar periods at CAGRs ranging from 3% to 5.1%.

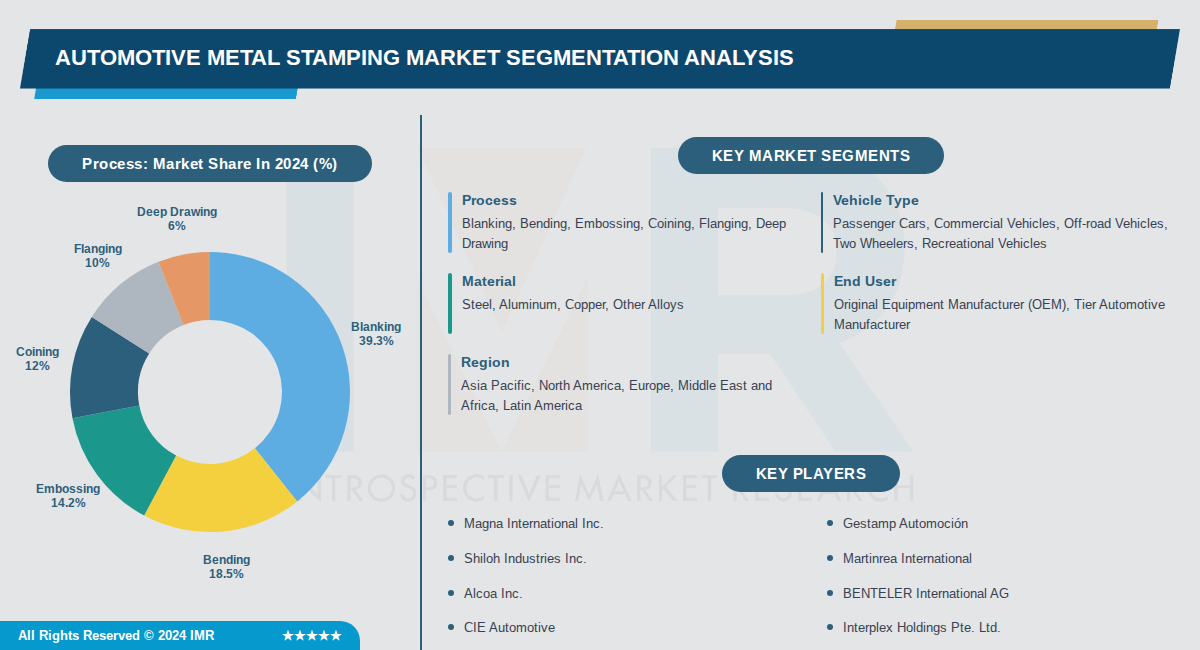

Key market segments include processes like blanking, which held a 40.5% share in 2024, alongside embossing, bending, coining, deep drawing, and flanging. Materials are dominated by steel for its strength and cost-effectiveness, with aluminum gaining traction for lightweighting in electric vehicles (EVs). Passenger cars represent the largest vehicle type segment at 62.3% market share.

Regionally, Asia Pacific leads with a 41.2% share ($35.7 billion in 2024), driven by automotive hubs in China, Japan, South Korea, and India. North America and Europe follow, supported by manufacturing strength and EV transitions, while other regions show slower but emerging growth.

Automotive Metal Stamping Market Trend Analysis:

Rise of Lightweight Material Stamping

- OEMs like Ford and Tesla are increasingly stamping high-strength low-alloy (HSLA) steels and 6xxx series aluminum alloys to reduce vehicle weights by 10-15%, directly improving EV range and fuel efficiency in models such as the Ford F-150 Lightning. This shift has driven aluminum stamping revenue at a 5.18% CAGR, with battery enclosures and chassis components leading demand. Manufacturers report up to 40% scrap reduction through optimized processes for these materials.

- In 2024, launches of high-strength aluminum stamping for EV battery enclosures by suppliers like Magna International addressed corrosion resistance and structural integrity needs. Multi-material designs combining aluminum panels with steel reinforcements are standard in hybrids from Toyota, enhancing crashworthiness while cutting CO2 emissions. Hot-stamping furnaces with multi-zone quench control prevent hydrogen embrittlement in AHSS sheets used by BMW.

- Expansion in Asia-Pacific sees Chinese firms like BAIC investing in lightweight steel stamping for commercial vehicles, supporting a market growth from USD 121 billion in 2024 to USD 130 billion by 2026 at 6.05% CAGR.

Integration of Industry 4.0 Automation

- Robotic multi-stage stamping lines adopted by North American firms like General Motors reduce cycle times by 30% and labor costs by 20%, with 70% adoption projected in high-volume plants by 2026. AI-driven quality control and IoT-enabled presses enable real-time monitoring, cutting downtime by 15% through predictive maintenance. Digital twins and inline optical systems predict defects, boosting on-time delivery for OEMs like Stellantis.

- Servo-electric presses from Schuler Group, consuming 50% less power than hydraulic models, dominate EV structural part production, with servo-driven retrofits expanding forming limits on AHSS sheets. The 2026 Metal Stamping Technology Conference in Nashville highlights AI simulation for virtual die design, reducing prototypes by 50% in R&D at companies like Boeing for aerospace crossovers.

- In Europe, Volkswagen's implementation of robotic vacuum transfer systems limits scale build-up, while modular tooling allows seamless shifts for complex geometries in Audi EVs.

Demand Surge for EV-Specific Stamping

- Stamped battery trays and lightweight frames comprise 40% of market share, with the automotive metal stamping sector growing from USD 96.7 billion in 2026 to USD 142.37 billion by 2034 at 4.95% CAGR, led by Tesla's Gigafactory needs. Precision coining for enclosures ensures micron-level accuracy, meeting safety standards for high-voltage components in Rivian R1T trucks.

- Tier-1 suppliers like Lear Corporation secure platform bundles from OEMs rationalizing counts by offering hot-stamping for AHSS battery housings, reducing parts and improving NVH damping. Embossing innovations create stiffening beads without thinning metal, vital for crashworthiness in Lucid Air sedans.

- Asia-Pacific expansions, including new facilities by Hyundai in India, target passenger car EV production, fueled by government incentives for electrification.

Automotive Metal Stamping Market Segment Analysis:

Automotive Metal Stamping Market is Segmented on the basis of By Process, By Vehicle Type, By Material

By Process, Blanking segment is expected to dominate the market during the forecast period

- Blanking dominates with 39.3% market share as it is the foundational process for cutting and shaping metal sheets into flat components, making it essential for producing body panels and structural elements across all vehicle types.

- Blanking's dominance is driven by its cost-effectiveness and high-speed production capability, enabling manufacturers to process large volumes of components efficiently while maintaining precision for both simple and complex automotive parts.

By Vehicle Type, Passenger Cars segment is expected to dominate the market during the forecast period

- Passenger cars command 62.3% of the market due to their significantly higher production volumes globally, sustained consumer demand for personal transportation, and increased spending power driving urbanization and vehicle ownership.

- The passenger car segment benefits from continuous innovation in lightweight stamped components for fuel efficiency and electric vehicle adoption, where stamped parts are critical for battery housings, structural frames, and body panels in EV designs.

By Material, Steel segment is expected to dominate the market during the forecast period

- Steel dominates with 68% market share due to its superior strength-to-weight ratio, high durability for load-bearing components, cost-effectiveness, and widespread availability, making it the preferred material for structural frames, chassis components, and safety-critical automotive parts.

- Steel's dominance is reinforced by its proven track record in both conventional and heavy-duty commercial vehicles, where high-strength steel variants provide the necessary structural integrity for trucks, buses, and commercial fleets operating under demanding conditions.

By End User, Original Equipment Manufacturer (OEM) segment is expected to dominate the market during the forecast period

- OEMs account for 72% of the market as they control major vehicle production and directly integrate stamped components into manufacturing processes, leveraging large-scale production capabilities and established supply chain relationships.

- OEM dominance is strengthened by their investment in multi-stage stamping systems, flexible tooling, and automation technologies that enable efficient production of different vehicle models while maintaining strict quality and precision standards required for final assembly.

By Region, Asia Pacific segment is expected to dominate the market during the forecast period

- Asia Pacific dominates with 41.2% market share due to the presence of major automotive manufacturers in China, Japan, South Korea, and India, combined with rapid industrialization, urbanization, and the highest vehicle production volumes globally.

- Asia Pacific's leadership is reinforced by government support policies, availability of affordable labor, heavy investment in automotive infrastructure and R&D by key companies, and the region's role as a primary exporter of automotive components to Europe, North America, and Africa.

Automotive Metal Stamping Market Regional Insights:

Asia-Pacific Dominates the Automotive Metal Stamping Market

- Asia-Pacific leads the global Automotive Metal Stamping Market with the highest market share of 35-37.89%, primarily driven by key countries like China, India, Japan, and South Korea. China alone accounts for a significant 12% of the Asia-Pacific market, fueled by rapid automotive production and EV adoption. This region's dominance stems from its position as the manufacturing hub for vehicles worldwide.

- Rapid industrialization, urbanization, and expansion of automotive manufacturing infrastructure boost demand for metal stamping processes like blanking, bending, and coining. Government policies supporting localization, new-energy vehicles, and affordable labor further enhance growth. Investments in industrial parks and OEM facilities around clusters like Shanghai, Guangzhou, Pune, and Chennai solidify its lead.

- Major players benefit from heavy R&D and manufacturing expansions by companies like Magna, Gestamp, and local OEMs such as those in China and Japan. Recent developments include servo-press installations for advanced high-strength steel components and EV integration. The region exports stamped parts to Europe, North America, and Africa, reinforcing its global supply chain role.

Active Key Players in the Automotive Metal Stamping Market:

- Magna International Inc. (Canada)

- Gestamp Automoción (Spain)

- Shiloh Industries Inc. (USA)

- Martinrea International (Canada)

- Alcoa Inc. (USA)

- BENTELER International AG (Germany)

- CIE Automotive (Spain)

- Interplex Holdings Pte. Ltd. (Singapore)

- Caparo Group (UK)

- Acro Metal Stamping (USA)

- Kenmode Precision Metal Stamping (USA)

- JBM Group (India)

- Manor Tool and Manufacturing Company (USA)

- Lindy Manufacturing (USA)

- Goshen Stamping Company (USA)

- Aro Metal Stamping (USA)

- American Industrial Company (USA)

- Tempco Manufacturing (USA)

- A.J. Rose Manufacturing Co. (USA)

- Other Active Players

|

Automotive Metal Stamping Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 86.41 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.5 % |

Market Size in 2035: |

USD 140.23 Billion |

|

Segments Covered: |

By Process |

|

|

|

By Vehicle Type |

|

||

|

By Material |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Automotive Metal Stamping Market by Process (2017-2035)

4.1 Automotive Metal Stamping Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Blanking

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Bending

4.5 Embossing

4.6 Coining

4.7 Flanging

4.8 Deep Drawing

Chapter 5: Automotive Metal Stamping Market by Vehicle Type (2017-2035)

5.1 Automotive Metal Stamping Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Passenger Cars

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Commercial Vehicles

5.5 Off-road Vehicles

5.6 Two Wheelers

5.7 Recreational Vehicles

Chapter 6: Automotive Metal Stamping Market by Material (2017-2035)

6.1 Automotive Metal Stamping Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Steel

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Aluminum

6.5 Copper

6.6 Other Alloys

Chapter 7: Automotive Metal Stamping Market by End User (2017-2035)

7.1 Automotive Metal Stamping Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Original Equipment Manufacturer (OEM)

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Tier Automotive Manufacturer

Chapter 8: Automotive Metal Stamping Market by Region (2017-2035)

8.1 Automotive Metal Stamping Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Asia Pacific

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 North America

8.5 Europe

8.6 Middle East and Africa

8.7 Latin America

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Automotive Metal Stamping Market Share by Manufacturer/Service Provider (2024)

9.1.3 Industry BCG Matrix

9.1.4 Partnerships, Mergers & Acquisitions

9.2 MAGNA INTERNATIONAL INC.

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 GESTAMP AUTOMOCIÓN

9.4 SHILOH INDUSTRIES INC.

9.5 MARTINREA INTERNATIONAL

9.6 ALCOA INC.

9.7 BENTELER INTERNATIONAL AG

9.8 CIE AUTOMOTIVE

9.9 INTERPLEX HOLDINGS PTE. LTD.

9.10 CAPARO GROUP

9.11 ACRO METAL STAMPING

9.12 KENMODE PRECISION METAL STAMPING

9.13 JBM GROUP

9.14 MANOR TOOL AND MANUFACTURING COMPANY

9.15 LINDY MANUFACTURING

9.16 GOSHEN STAMPING COMPANY

9.17 ARO METAL STAMPING

9.18 AMERICAN INDUSTRIAL COMPANY

9.19 TEMPCO MANUFACTURING

9.20 A.J. ROSE MANUFACTURING CO.

Chapter 10: Global Automotive Metal Stamping Market By Region

10.1 Overview

10.2. North America Automotive Metal Stamping Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.3. Eastern Europe Automotive Metal Stamping Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.4. Western Europe Automotive Metal Stamping Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.5. Asia Pacific Automotive Metal Stamping Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.6. Middle East & Africa Automotive Metal Stamping Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.7. South America Automotive Metal Stamping Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

Chapter 11: Analyst Viewpoint and Conclusion

Chapter 12: Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 13: Case Study

Chapter 14: Appendix

14.1 Sources

14.2 List of Tables and Figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Automotive Metal Stamping Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 86.41 Billion |

|

Forecast Period 2024-2035 CAGR: |

4.5 % |

Market Size in 2035: |

USD 140.23 Billion |

|

Segments Covered: |

By Process |

|

|

|

By Vehicle Type |

|

||

|

By Material |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||