Atherectomy Devices Market Synopsis

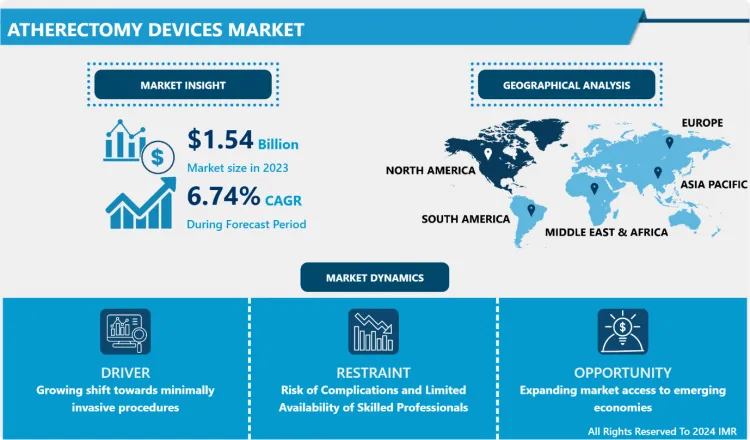

Atherectomy Devices Market Size Was Valued at USD 1.54 Billion in 2023, and is Projected to Reach USD 2.76 Billion by 2032, Growing at a CAGR of 6.74% From 2024-2032.

Atherectomy devices are specialized endovascular instruments used to ablate, debulk, or mechanically remove atherosclerotic diseases or blockages in peripheral, coronary or neurovascular arteries. These devices are used in endovascular intervention to recanalize occluded vessels in patients with peripheral artery disease (PAD), coronary artery disease (CAD), and other. Atherectomy is likewise significant since it contributes to stable management of vascular diseases and alleviation of the given sufferers’ conditions, they experience discomfort, fatigue, and shortness of breath.

- Coronary Artery Disease and Peripheral artery diseases are some the cardinal cardiovascular diseases that have continued to rise, creating a market demand for atherectomy devices. Since, now the demography of the world is shifting with increasing aged people and risk factors encompassing obesity, hypertension and diabetes, hence increasing the need for more sophisticated interventional procedures. Related life-threatening diseases are treated through atherectomy devices that give the market a significant boost because they offer less invasive treatments to patients.

- A third factor relates to technology improvement in atherectomy related equipment and machines. Laser and rotational atherectomy are such innovations that make the process very accurate and less traumatic to the patient in the target site. New device technologies and techniques cost research and development that has informed development of safer and easier to use new devices. These, coupled with raising demand of minimally invasive surgical procedures which are comparatively new in the market is anticipated to boost the market soon.

Atherectomy Devices Market Trend Analysis

Growing shift towards minimally invasive procedures

- Another trend prevailing for the Atherectomy Devices Market is the increasing preference for minimal invasive procedure. Taking their time in the recovery process as well as the risks associated with surgeries are some of the reasons why patients, and healthcare practitioners are employing minimally invasive treatments. The requirements they wanted for atherectomy were accuracy and efficiency with minimal trauma that paved way for quicker hospital readmissions and fast healing from the patient.

- Another trend is the rising usage of complementary techniques when using atherectomy in combination with angioplasty or stenting. This strategy offer a more holistic treatment of difficult vessel obstruction comparing well to other methods therefore improving the overall success rate of an intervention. Therefore, as multi-modal therapies become a mainstream in peripheral interventions the atherectomy devices are being incorporated into more aetiologies of peripheral interventions.

Expanding market access to emerging economies

- In the advent of the Atherectomy Devices Market, one of the most favorable prospects is to extend the market presence in developing countries. The Asia-Pacific, Latin American as well as the Middle East emerging as more and more countries invest in the health care facilities, which in turn requires better technologies in the medical field. The increasing populations’ concerns regarding cardiovascular diseases in these areas help create significant markets for such producers to penetrate the markets with atherectomy.

- Furthermore, huge opportunities could be seen in the growth of future generation atherectomy systems with many characteristics like better direction abilities, superior plaque excision or ability to be compatible with numbers of imaging systems. There will always be a demand for devices that are more efficient as healthcare workers look to treat more complicated vascular disorders effectively. It has been recommended that the companies invest on R&D and immediately begin to launch new products to the market to help them create a competitive edge in the new market.

Atherectomy Devices Market Segment Analysis:

Atherectomy Devices Market is segmented on the basis of Product type, application and end user.

By Product Type, Directional Atherectomy Devices segment is expected to dominate the market during the forecast period

- The Atherectomy Devices Market is examining based on a selection of products that are developed to full different functions in medical treatments. Devices for directional atherectomy are designed to excise the plaque by cutting it and capturing it, and are mainly applied for treating the peripheral vascular disease. Currently available orbital atherectomy devices employ a rotating crown to abrade the plaque as an effective treatment of hard and soft lesion. Consequently, laser atherectomy device operates utilizing laser energy and it is thus very efficient for delicate and strong lesions. Rotational atherectomy devices use a rotating burr to ablate the plaque in the diseased artery, and is typically done in accord with percutaneous coronary interventions to unblock blood vessels and reduce the risk of further occlusions. All these product types are vital in offering least invasive treatment of vascular diseases to the patients.

By Application, Peripheral Vascular segment expected to held the largest share

- The Atherectomy Devices Market categorized by application includes peripheral vascular, cardiovascular and neurovascular. Peripheral vascular applications include ailments that have an impact on the blood vessels outside the heart; however, common peripheral vascular treatment deals with PAD which affects the legs and arms. Cardiovascular application aims at eradicating obstruction and plaque formation in coronary arteries that causes CAD and heart attack. Neurovascular interventions include elimination of atheromatous plaque from arteries that feed the brain in order to reduce the rates of stroke and other cerebrovascular diseases. One application addresses different vascular areas, the other one treating different types of diseases concerning arterie.

Atherectomy Devices Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

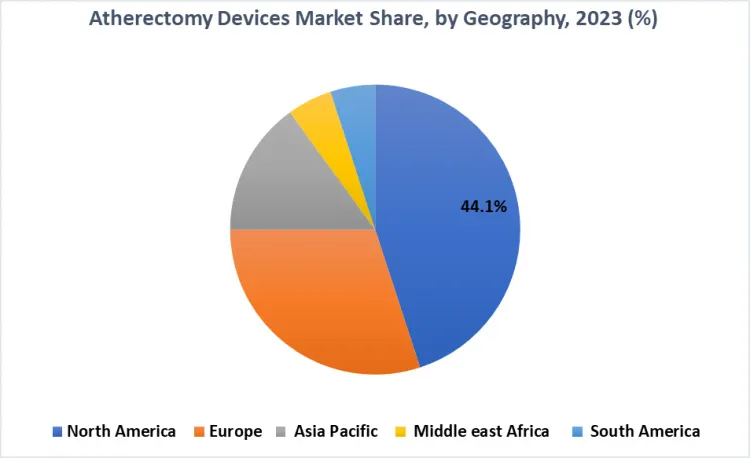

- This market has developed in the North American region, which alone has a share of about 40-45% of the total global market. This is due to the relatively high prevalence of cardiovascular diseases and an increasingly developing health care system that promotes the use of the latest technological solutions in medicine. Also, the growth of this market is supported by established leading medical device manufacturers and sound reimbursement policies. North America also has a developed base of hospitals and surgical centres that proactively invest in the advance atherectomy devices in order to deliver the best to their patients.

- The region’s strengthening continues to be compounded by Current Clinical Research and Trials that seek to enhance the effectiveness and impacts of atherectomy procedures. North America has emerged as the leading market for atherectomy devices due to the availability of skilled healthcare professionals and the enhancing awareness among the population of vascular diseases, and their treatments.

Active Key Players in the Atherectomy Devices Market

- Abbott Laboratories (USA)

- Avinger, Inc. (USA)

- BD (Becton, Dickinson and Company) (USA)

- Boston Scientific Corporation (USA)

- C. R. Bard, Inc. (USA)

- Cardinal Health (USA)

- JOMED (Germany)

- Medtronic (Ireland)

- Phillips Healthcare (Netherlands)

- Terumo Corporation (Japan) and Other key Players

|

Global Atherectomy Devices Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 1.54 Billion |

|

Forecast Period 2024-32 CAGR: |

6.74% |

Market Size in 2032: |

USD 2.76 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Atherectomy Devices Market by Product Type (2018-2032)

4.1 Atherectomy Devices Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Directional Atherectomy Devices

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Orbital Atherectomy Devices

4.5 Laser Atherectomy Devices

4.6 Rotational Atherectomy Devices

Chapter 5: Atherectomy Devices Market by Application (2018-2032)

5.1 Atherectomy Devices Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Peripheral Vascular

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Cardiovascular

5.5 Neurovascular

Chapter 6: Atherectomy Devices Market by End User (2018-2032)

6.1 Atherectomy Devices Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals & Surgical Centers

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Ambulatory Care Centers

6.5 Research Laboratories & Academic Institutes

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Atherectomy Devices Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ABBOTT LABORATORIES (USA)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 AVINGER INC. (USA)

7.4 BD (BECTON

7.5 DICKINSON AND COMPANY) (USA)

7.6 BOSTON SCIENTIFIC CORPORATION (USA)

7.7 C. R. BARD INC. (USA)

7.8 CARDINAL HEALTH (USA)

7.9 JOMED (GERMANY)

7.10 MEDTRONIC (IRELAND)

7.11 PHILLIPS HEALTHCARE (NETHERLANDS)

7.12 TERUMO CORPORATION (JAPAN) OTHER KEY PLAYERS

7.13

Chapter 8: Global Atherectomy Devices Market By Region

8.1 Overview

8.2. North America Atherectomy Devices Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Product Type

8.2.4.1 Directional Atherectomy Devices

8.2.4.2 Orbital Atherectomy Devices

8.2.4.3 Laser Atherectomy Devices

8.2.4.4 Rotational Atherectomy Devices

8.2.5 Historic and Forecasted Market Size by Application

8.2.5.1 Peripheral Vascular

8.2.5.2 Cardiovascular

8.2.5.3 Neurovascular

8.2.6 Historic and Forecasted Market Size by End User

8.2.6.1 Hospitals & Surgical Centers

8.2.6.2 Ambulatory Care Centers

8.2.6.3 Research Laboratories & Academic Institutes

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Atherectomy Devices Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Product Type

8.3.4.1 Directional Atherectomy Devices

8.3.4.2 Orbital Atherectomy Devices

8.3.4.3 Laser Atherectomy Devices

8.3.4.4 Rotational Atherectomy Devices

8.3.5 Historic and Forecasted Market Size by Application

8.3.5.1 Peripheral Vascular

8.3.5.2 Cardiovascular

8.3.5.3 Neurovascular

8.3.6 Historic and Forecasted Market Size by End User

8.3.6.1 Hospitals & Surgical Centers

8.3.6.2 Ambulatory Care Centers

8.3.6.3 Research Laboratories & Academic Institutes

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Atherectomy Devices Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Product Type

8.4.4.1 Directional Atherectomy Devices

8.4.4.2 Orbital Atherectomy Devices

8.4.4.3 Laser Atherectomy Devices

8.4.4.4 Rotational Atherectomy Devices

8.4.5 Historic and Forecasted Market Size by Application

8.4.5.1 Peripheral Vascular

8.4.5.2 Cardiovascular

8.4.5.3 Neurovascular

8.4.6 Historic and Forecasted Market Size by End User

8.4.6.1 Hospitals & Surgical Centers

8.4.6.2 Ambulatory Care Centers

8.4.6.3 Research Laboratories & Academic Institutes

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Atherectomy Devices Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Product Type

8.5.4.1 Directional Atherectomy Devices

8.5.4.2 Orbital Atherectomy Devices

8.5.4.3 Laser Atherectomy Devices

8.5.4.4 Rotational Atherectomy Devices

8.5.5 Historic and Forecasted Market Size by Application

8.5.5.1 Peripheral Vascular

8.5.5.2 Cardiovascular

8.5.5.3 Neurovascular

8.5.6 Historic and Forecasted Market Size by End User

8.5.6.1 Hospitals & Surgical Centers

8.5.6.2 Ambulatory Care Centers

8.5.6.3 Research Laboratories & Academic Institutes

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Atherectomy Devices Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Product Type

8.6.4.1 Directional Atherectomy Devices

8.6.4.2 Orbital Atherectomy Devices

8.6.4.3 Laser Atherectomy Devices

8.6.4.4 Rotational Atherectomy Devices

8.6.5 Historic and Forecasted Market Size by Application

8.6.5.1 Peripheral Vascular

8.6.5.2 Cardiovascular

8.6.5.3 Neurovascular

8.6.6 Historic and Forecasted Market Size by End User

8.6.6.1 Hospitals & Surgical Centers

8.6.6.2 Ambulatory Care Centers

8.6.6.3 Research Laboratories & Academic Institutes

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Atherectomy Devices Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Product Type

8.7.4.1 Directional Atherectomy Devices

8.7.4.2 Orbital Atherectomy Devices

8.7.4.3 Laser Atherectomy Devices

8.7.4.4 Rotational Atherectomy Devices

8.7.5 Historic and Forecasted Market Size by Application

8.7.5.1 Peripheral Vascular

8.7.5.2 Cardiovascular

8.7.5.3 Neurovascular

8.7.6 Historic and Forecasted Market Size by End User

8.7.6.1 Hospitals & Surgical Centers

8.7.6.2 Ambulatory Care Centers

8.7.6.3 Research Laboratories & Academic Institutes

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Atherectomy Devices Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 1.54 Billion |

|

Forecast Period 2024-32 CAGR: |

6.74% |

Market Size in 2032: |

USD 2.76 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Application |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Atherectomy Devices Market research report is 2024-2032.

Boston Scientific Corporation (USA), Medtronic (Ireland), Terumo Corporation (Japan), Cardinal Health (USA), Avinger, Inc. (USA), Abbott Laboratories (USA), C. R. Bard, Inc. (USA), BD (Becton, Dickinson and Company) (USA), Phillips Healthcare (Netherlands), JOMED (Germany) and Other Major Players.

The Atherectomy Devices Market is segmented into by Product Type (Directional Atherectomy Devices, Orbital Atherectomy Devices, Laser Atherectomy Devices, Rotational Atherectomy Devices), Application (Peripheral Vascular, Cardiovascular, Neurovascular), End User (Hospitals & Surgical Centers, Ambulatory Care Centers, Research Laboratories & Academic Institutes). By region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; Netherlands; Italy; Russia; Spain; Rest of Western Europe), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

Atherectomy devices are specialized endovascular instruments used to ablate, debulk, or mechanically remove atherosclerotic diseases or blockages in peripheral, coronary or neurovascular arteries. These devices are used in endovascular intervention to recanalize occluded vessels in patients with peripheral artery disease (PAD), coronary artery disease (CAD), and other. Atherectomy is likewise significant since it contributes to stable management of vascular diseases and alleviation of the given sufferers’ conditions, they experience discomfort, fatigue, and shortness of breath.

Atherectomy Devices Market Size Was Valued at USD 1.54 Billion in 2023, and is Projected to Reach USD 2.76 Billion by 2032, Growing at a CAGR of 6.74% From 2024-2032.