Aortic Stenosis Market Synopsis

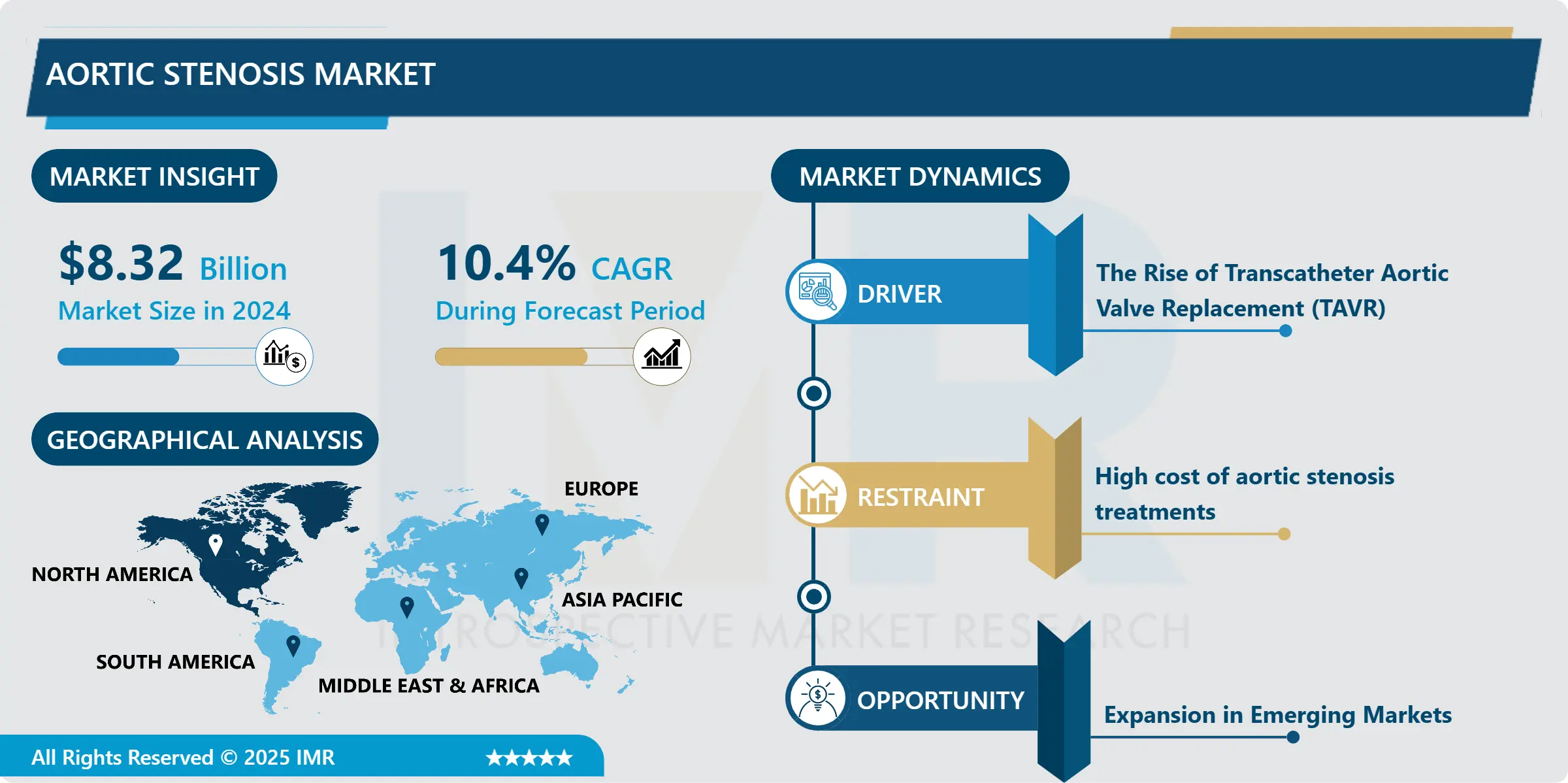

Aortic Stenosis Market Size was valued at USD 8.32 Billion in 2024, and is Projected to Reach USD 16.76 Billion by 2035, Growing at a CAGR of 10.4% From 2025-2035.

Aortic stenosis market here covers all forms of remedies ranging from diagnostic apparatus, therapies and any other equipment used to treat patients with this condition. These treatments include drugs and performing procedures like surgical valve replacement or repair to valve replacement in particular using Transcatheter Aortic Valve Replacement (TAVR) therapies developed to enhance blood flow and halt or slow the progression of the disease.

Global aortic stenosis market has been steadily growing as more people develop cardiovascular diseases and cardiologists find solutions for the condition affecting adults. One of the major diseases which are becoming more frequent in the current population include aortic stenosis, and the most affected are the aged people across the world. Different research has pointed out that the condition mainly affects the over 65 years of age persons but the signs are masked until the disease advances. The key principle in the management of AS is prevention and early diagnosis that has been made possible by the development of new diagnostic techniques like echocardiography as well as computed tomography. Moreover, the latest trends in TAVR, smaller catheters, improving surgical outcomes after anterior approaches, and the introduction of subcutaneous implantable cardioverter-defibrillators have expanded the treatment options and created an increasing demand for new surgical technologies.

Since there are more treatment choices available for patients with valvular heart diseases, there are also more medical devices used for aortic valve replacement such as bioprosthetic and mechanical valves that may be complemented by surgical or minimal invasive procedures. Market competitors are actively striving for the development of newer technologies in the aortic stenosis market with increased concern toward the safety and efficiency of the treatment. TAVR procedures are predicted to gain a great demand over the forecast period as experience levels of the TAVR procedures increases, the rate of procedural complications decreases, and quicken the recovery time compared to open-heart surgery. However, the drawback that emanates from these interventions is the high cost, which poses a problem especially for growing markets with limited healthcare revenues.

Aortic Stenosis Market Trend Analysis:

The Rise of Transcatheter Aortic Valve Replacement (TAVR)

- Transcatheter Aortic Valve Replacement (TAVR) is one of the major trends in the USC development due to the growing tendency to use it in patients who are at high risk for standard surgical interventions, including aortic valve replacement. TAVR in an endovascular technique where the new valve is introduced through the blood vessels; usually, femoral artery and do not require cardiopulmonary bypass. This procedure has been adopted frequently by surgeons and physicians for its efficiency in Medicare and high-risk as well as elderly patients with low mortality rate and short post-surgical recovery time than the conventional surgery. Public acceptance embraces TAVR also by steady enhancement of the valve design and the catheter technology contributing to the further success and safety of the process. With additional and further trials revealing positive affects and results of TAVR across various patients, TAVR is likely to be recommended even further given that more and more it is endorsed as a standard approach to managing symptomatic aortic stenosis.

Expansion in Emerging Markets

- Expanded Access to Advanced Diagnostic and Therapeutic solutions in Opportunity The opportunity in the market for aortic stenosis resides mainly in the ability to reach emerging markets and provide those consumers with the treatments for the disease. Currently healthcare systems of countries like China, India and Brazil are witnessing a vertical rise and because of this, people in these countries are seeking for better treatment for heart ailments such as aortic stenosis. Some of these regions consist of a relatively young, but numerously growing elderly population, who are most vulnerable to cardiovascular diseases. In addition, the increased application of less invasive techniques, including TAVR, in these regions could further increase since the alternative heart surgery is dangerous and expensive.

- It is the multi-faceted relation between the local health care centres and the international medical devices manufacturers that could offer a chance to deepen the penetration of more and highly performed treatments in these areas. Secondly, the governments of growing nations are focusing on the improvement of healthcare services, enhancement of insurance services and adoption of advance technologies in treating diseases which can be a profitable growth opportunity for aortic stenosis firms.

Aortic Stenosis Market Segment Analysis:

Aortic Stenosis Market is segmented on the basis of Type, Aortic Valve Types, Severity, End user and Region

By Type, Congenital Aortic Stenosis segment is expected to dominate the market during the forecast period

- Congenital aortic stenosis – a heart defect which develops before birth should remain the market leader during the forecast period due to the constant growth of knowledge about the existence of this disease and its early diagnosis. This segment comprises rheumatic heart diseases that develop when the aortic valve in the heart gets closed, thereby blocking blood flow in the body. Since it is a congenital disease, patients may need appropriate therapy soon after birth to avoid further problems like heart failure or arrhythmias. Improvements in standard services such as dianostics and screening techniques have made congenital aortic stenosis increasingly apparent in infants and children, and more patients are seeking ways to manage and treat it, whether by surgical means, catheterisation or medication.

- The increasing incidence rate of congenital aortic stenosis along with technological advancements of the treatment procedures will propel the growth of this market over the aforementioned years. Children especially need highly individualized care and follow up, and this applies to both surgical treatment and postoperative care. In addition, technologies are advancing and the market is developing because it is conceivable to treat aortic stenosis through superior techniques that involve valve replacements and minimally invasive treatments that create better results for patients due to shorter recovery periods. Because the disease remains relatively unknown among most healthcare practitioners and patients, the congenital aortic stenosis segment is expected to remain on robust growth in the global healthcare industry.

By Aortic Valve Types, Mechanical Aortic Valves, segment expected to held the largest share

- The mechanical aortic valve segment is expected to hold the largest market share by 2032, because of its reliability and stability, use to efficiency of its performance as compared to other type of valves used for aortic valve replacement. These valves are constructed of such materials as titanium, carbon, or ceramics and, in contrast to tissue values, have a lifespan expected to last from several decades; for this reason, surgeons prefer implanting mechanical valves to young patients or those with long life expectancies. These valves are designed to opened and closed in response to the pressures and stress prevailing in the circulatory System; this is one of the reasons that makes it preferred. Furthermore, the discrepancy indicate that mechanical valves are preferred globally with regard to valve-related aftermaths hence contributing to its dominance in the market.

- In situations where patients require anticoagulant therapy for the rest of their lives due to the propensity of developing clots, mechanical valves remain popular due to high durability and internal trust. With the increase in aged clients, coupled with the increasing prevalence of ailment such as aortic valve disease, tend to rise there is an increasing need for a Mechanical valve which is durable and reliable. Moreover, the technology has enhanced the design of mechanical valves making it easier to implant with low complications. These factors are expected to further augment the segment in the market for aortic valve replacement to ensure is maintains the position of the best product in the market as preferred by most healthcare facility around the world and the patients who require effective and long-lasting solutions in their respective hospitals.

Aortic Stenosis Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North American held the 45% market share in 2023 on the premises of aortic stenosis market all across the globe. The United States has the biggest contribution to this share because of its sophisticated health care system, availability of enriched technological facilities for medical treatments, and high per capita health care expenses. Another reason is the demographic one, as North America has, and continues to, experience an increasing number of elderly people, which is the group mostly affected by aortic stenosis.

- The rising minimally invasive operations – including the transcatheter aortic valve replacement (TAVR) has expanded the demand for the market in this region. Further, North America has a robust reimbursement model across aortic valve replacement surgeries and other cardiovascular procedures giving high patient access to care. The region is also blessed with firstly, leading market players that continue to develop medical device and therapeutic solutions for aortic stenosis.

Active Key Players in the Aortic Stenosis Market:

- Abbott Laboratories (USA)

- Aortic Innovations (USA)

- Biotronik (Germany)

- Boston Scientific Corporation (USA)

- CoreValve Inc. (USA)

- Edwards Lifesciences Corporation (USA)

- Johnson & Johnson (USA)

- LivaNova PLC (UK)

- Medtronic (Ireland)

- Medtronic plc (Ireland)

- Philips Healthcare (Netherlands)

- Sorin Group (Italy)

- St. Jude Medical (USA)

- Terumo Corporation (Japan)

- Vascutek Ltd. (UK)

- Other Active Players

Key Industry Development in the Aortic Stenosis Market:

- In November 2024, Abbott announced the first patient procedures with its investigational transcatheter aortic valve implantation (TAVI) balloon-expandable system for treating symptomatic severe aortic stenosis. This investigational Abbott TAVI system is the first step toward Abbott's software-guided balloon-expandable TAVI system and is designed to build a foundation for artificial intelligence (AI) guided procedures. Once the investigational balloon-expandable system completes clinical development and is approved by regulatory authorities, Abbott's structural heart portfolio will offer physicians another TAVI management option to meet the patient's needs along with the company's Navitor TAVI system, which is already commercially available.

- In October 2024, Edwards Lifesciences announced results from the EARLY TAVR Trial, the first randomized, controlled trial designed to study the best strategy for treating asymptomatic severe aortic stenosis (AS) and the benefits of early intervention with transcatheter aortic valve replacement (TAVR). The trial results demonstrated that asymptomatic severe AS patients randomized to Edwards TAVR experienced superior outcomes compared with guideline-recommended clinical surveillance. Trial investigators presented the data today during a late-breaking clinical trials session at Transcatheter Cardiovascular Therapeutics (TCT), the annual scientific symposium of the Cardiovascular Research Foundation (CRF). They were published simultaneously in The New England Journal of Medicine.

|

Global Aortic Stenosis Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 8.32 Billion |

|

Forecast Period 2025-35 CAGR: |

10.4% |

Market Size in 2035: |

USD 16.76 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Aortic Valve Types |

|

||

|

By Severity |

|

||

|

By End user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Aortic Stenosis Market by Type (2018-2035)

4.1 Aortic Stenosis Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Congenital Aortic Stenosis

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Acquired Aortic Stenosis

Chapter 5: Aortic Stenosis Market by Aortic Valve Types (2018-2035)

5.1 Aortic Stenosis Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Mechanical Aortic Valves

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Bioprosthetic (Tissue) Aortic Valves

Chapter 6: Aortic Stenosis Market by Severity (2018-2035)

6.1 Aortic Stenosis Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Mild Aortic Stenosis

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Moderate Aortic Stenosis

6.5 Severe Aortic Stenosis

Chapter 7: Aortic Stenosis Market by End user (2018-2035)

7.1 Aortic Stenosis Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospital

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Clinics

7.5 Ambulatory Surgical Centers

7.6 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Aortic Stenosis Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 ABBOTT LABORATORIES (USA)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 AORTIC INNOVATIONS (USA)

8.4 BIOTRONIK (GERMANY)

8.5 BOSTON SCIENTIFIC CORPORATION (USA)

8.6 COREVALVE INC. (USA)

8.7 EDWARDS LIFESCIENCES CORPORATION (USA)

8.8 JOHNSON & JOHNSON (USA)

8.9 LIVANOVA PLC (UK)

8.10 MEDTRONIC (IRELAND)

8.11 MEDTRONIC PLC (IRELAND)

8.12 PHILIPS HEALTHCARE (NETHERLANDS)

8.13 SORIN GROUP (ITALY)

8.14 ST. JUDE MEDICAL (USA)

8.15 TERUMO CORPORATION (JAPAN)

8.16 VASCUTEK LTD. (UK)

8.17

Chapter 9: Global Aortic Stenosis Market By Region

9.1 Overview

9.2. North America Aortic Stenosis Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Type

9.2.4.1 Congenital Aortic Stenosis

9.2.4.2 Acquired Aortic Stenosis

9.2.5 Historic and Forecasted Market Size by Aortic Valve Types

9.2.5.1 Mechanical Aortic Valves

9.2.5.2 Bioprosthetic (Tissue) Aortic Valves

9.2.6 Historic and Forecasted Market Size by Severity

9.2.6.1 Mild Aortic Stenosis

9.2.6.2 Moderate Aortic Stenosis

9.2.6.3 Severe Aortic Stenosis

9.2.7 Historic and Forecasted Market Size by End user

9.2.7.1 Hospital

9.2.7.2 Clinics

9.2.7.3 Ambulatory Surgical Centers

9.2.7.4 Others

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Aortic Stenosis Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Type

9.3.4.1 Congenital Aortic Stenosis

9.3.4.2 Acquired Aortic Stenosis

9.3.5 Historic and Forecasted Market Size by Aortic Valve Types

9.3.5.1 Mechanical Aortic Valves

9.3.5.2 Bioprosthetic (Tissue) Aortic Valves

9.3.6 Historic and Forecasted Market Size by Severity

9.3.6.1 Mild Aortic Stenosis

9.3.6.2 Moderate Aortic Stenosis

9.3.6.3 Severe Aortic Stenosis

9.3.7 Historic and Forecasted Market Size by End user

9.3.7.1 Hospital

9.3.7.2 Clinics

9.3.7.3 Ambulatory Surgical Centers

9.3.7.4 Others

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Aortic Stenosis Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Type

9.4.4.1 Congenital Aortic Stenosis

9.4.4.2 Acquired Aortic Stenosis

9.4.5 Historic and Forecasted Market Size by Aortic Valve Types

9.4.5.1 Mechanical Aortic Valves

9.4.5.2 Bioprosthetic (Tissue) Aortic Valves

9.4.6 Historic and Forecasted Market Size by Severity

9.4.6.1 Mild Aortic Stenosis

9.4.6.2 Moderate Aortic Stenosis

9.4.6.3 Severe Aortic Stenosis

9.4.7 Historic and Forecasted Market Size by End user

9.4.7.1 Hospital

9.4.7.2 Clinics

9.4.7.3 Ambulatory Surgical Centers

9.4.7.4 Others

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Aortic Stenosis Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Type

9.5.4.1 Congenital Aortic Stenosis

9.5.4.2 Acquired Aortic Stenosis

9.5.5 Historic and Forecasted Market Size by Aortic Valve Types

9.5.5.1 Mechanical Aortic Valves

9.5.5.2 Bioprosthetic (Tissue) Aortic Valves

9.5.6 Historic and Forecasted Market Size by Severity

9.5.6.1 Mild Aortic Stenosis

9.5.6.2 Moderate Aortic Stenosis

9.5.6.3 Severe Aortic Stenosis

9.5.7 Historic and Forecasted Market Size by End user

9.5.7.1 Hospital

9.5.7.2 Clinics

9.5.7.3 Ambulatory Surgical Centers

9.5.7.4 Others

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Aortic Stenosis Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Type

9.6.4.1 Congenital Aortic Stenosis

9.6.4.2 Acquired Aortic Stenosis

9.6.5 Historic and Forecasted Market Size by Aortic Valve Types

9.6.5.1 Mechanical Aortic Valves

9.6.5.2 Bioprosthetic (Tissue) Aortic Valves

9.6.6 Historic and Forecasted Market Size by Severity

9.6.6.1 Mild Aortic Stenosis

9.6.6.2 Moderate Aortic Stenosis

9.6.6.3 Severe Aortic Stenosis

9.6.7 Historic and Forecasted Market Size by End user

9.6.7.1 Hospital

9.6.7.2 Clinics

9.6.7.3 Ambulatory Surgical Centers

9.6.7.4 Others

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Aortic Stenosis Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Type

9.7.4.1 Congenital Aortic Stenosis

9.7.4.2 Acquired Aortic Stenosis

9.7.5 Historic and Forecasted Market Size by Aortic Valve Types

9.7.5.1 Mechanical Aortic Valves

9.7.5.2 Bioprosthetic (Tissue) Aortic Valves

9.7.6 Historic and Forecasted Market Size by Severity

9.7.6.1 Mild Aortic Stenosis

9.7.6.2 Moderate Aortic Stenosis

9.7.6.3 Severe Aortic Stenosis

9.7.7 Historic and Forecasted Market Size by End user

9.7.7.1 Hospital

9.7.7.2 Clinics

9.7.7.3 Ambulatory Surgical Centers

9.7.7.4 Others

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Aortic Stenosis Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 8.32 Billion |

|

Forecast Period 2025-35 CAGR: |

10.4% |

Market Size in 2035: |

USD 16.76 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Aortic Valve Types |

|

||

|

By Severity |

|

||

|

By End user |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||