Key Market Highlights

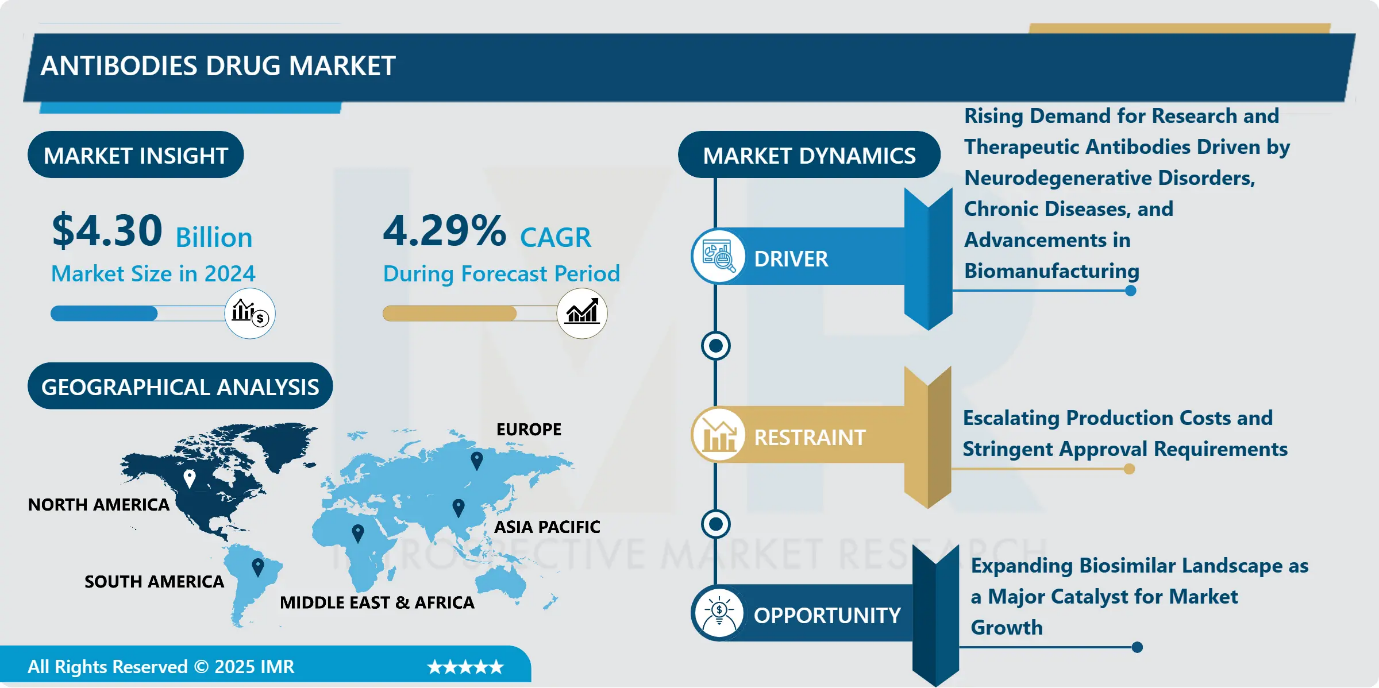

Antibodies Drug Market Size Was Valued at USD 4.30 Billion in 2024, and is Projected to Reach USD 6.83 Billion by 2035, Growing at a CAGR of 4.29% from 2025-2035.

- Market Size in 2024: USD 4.30 Billion

- Projected Market Size by 2035: USD 6.83 Billion

- CAGR (2025–2035): 4.29%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By Drug Type: The Monoclonal Antibodies segment is anticipated to lead the market by accounting for 28% of the market share throughout the forecast period.

- By Application: The Oncology segment is expected to capture 30.88% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 32.07% of the market share during the forecast period.

- Active Players: AbbVie Inc. (U.S.), AstraZeneca (U.K.), Bristol-Myers Squibb Company (U.S.), Charles River Laboratories (U.S.), Eli Lilly and Company (U.S.), and Other Active Players.

Antibodies Drug Market Synopsis:

The antibody market covers the discovery, development, manufacturing, and use of antibody-based therapies and diagnostic tools. Antibodies are highly specific immune proteins that can be engineered as monoclonal, polyclonal, bispecific, or conjugated forms to precisely target disease-related molecules. Demand for these therapies continues to rise as cases of cancer, autoimmune disorders, and infectious diseases grow worldwide. At the same time, advances in biotechnology such as recombinant DNA methods, improved engineering platforms, and next-generation antibody–drug conjugates are driving faster innovation and better treatment outcomes. Supportive regulatory policies, higher healthcare spending, and expanding pipelines from biotech and pharmaceutical companies further strengthen the market. Overall, the antibody market is experiencing steady, long-term growth fueled by scientific progress and wider therapeutic use.

Antibodies Drug Market Dynamics and Trend Analysis:

Antibodies Drug Market Growth Driver - Rising Demand for Research and Therapeutic Antibodies Driven by Neurodegenerative Disorders, Chronic Diseases, and Advancements in Biomanufacturing

-

The increasing prevalence of neurodegenerative and chronic diseases is significantly boosting the global research antibodies and monoclonal antibody markets. Disorders such as Parkinson’s disease, Huntington’s disease, and Multiple Sclerosis are driving the need for research antibodies to study protein functions and develop personalized therapies and new treatments. Chronic conditions like cancer also affect a large portion of the population about six in ten adults in the U.S. creating strong demand for effective therapies and increasing healthcare spending. Monoclonal antibodies, which made up roughly 91.2% of the market in 2024, rely on scalable and efficient production processes. Improvements in upstream and downstream manufacturing, along with contract manufacturing services, are helping meet growing global demand and support ongoing clinical research and therapeutic innovation.

Antibodies Drug Market Limiting Factor - Escalating Production Costs and Stringent Approval Requirements

-

The antibody and ADC markets continue to face significant restraints that slow overall progress. High manufacturing costs remain a major challenge, as production requires advanced technologies, high-grade raw materials, and experienced scientific talentmaking it difficult for smaller companies to scale their pipelines. Regulatory approval adds another layer of complexity, with strict requirements for safety, purity, and consistency often extending development timelines. Technical limitations in ADCs, including unstable linkers, limited tumor penetration, and potential toxicity, can further impact clinical outcomes and reduce treatment reliability. These combined factors raise development risks, limit accessibility, and restrict broader market expansion.

Antibodies Drug Market Expansion Opportunity - Expanding Biosimilar Landscape as a Major Catalyst for Market Growth

-

One of the most significant opportunities in the antibody therapeutics market comes from the rapid expansion of biosimilars. As many blockbuster monoclonal antibodies lose patent protection, global demand for cost-effective alternatives is rising sharply. Biosimilars offer comparable safety and efficacy at a lower price, making them especially attractive for healthcare systems facing increasing treatment costs. Regulatory agencies worldwide are also providing clearer guidelines and faster review pathways for biosimilars, encouraging developers to scale production. With global biosimilar sales projected to surge and major biologics entering the off-patent phase, companies investing in biosimilar development stand to gain a strong competitive advantage. This trend is expected to reshape market accessibility, affordability, and overall growth.

Antibodies Drug Market Challenge and Risk - High Immunogenicity Risk and Associated Safety Complications

-

A major challenge in the therapeutic antibody market is the persistent risk of immunogenicity and adverse immune reactions. Even with advances in humanization and engineering, antibodies can still trigger unwanted immune responses due to glycosylation variations, structural differences, or aggregation during storage. These reactions may reduce treatment efficacy or lead to severe events such as cytokine release syndrome, particularly with T-cell–engaging therapies, requiring intensive monitoring and hospital-based administration.

- This safety uncertainty complicates clinical adoption and limits use in long-term or outpatient settings. Alongside these concerns, the high development and manufacturing costs driven by complex cell-line engineering, specialized purification processes, and strict cold-chain logistics further restrict scalability and access, especially for smaller biotech and emerging markets.

Antibodies Drug Market Trend - Rapid Growth of Next-Generation Antibody Engineering and Personalized Treatment

-

The most dominant trend shaping the antibodies market is the rapid shift toward highly engineered and personalized antibody therapeutics. Advances in recombinant antibody engineering and bispecific platforms are leading this transformation, allowing researchers to design therapies that target disease pathways with far greater precision than traditional biologics.

- Technologies such as phage and yeast display now enable rapid screening of massive antibody libraries, reducing early discovery timelines and accelerating clinical progress. This push for more targeted, patient-specific treatments is reinforced by rising demand in oncology and immunology, where biomarker-driven therapies are becoming standard practice. As companies invest heavily in next-generation engineering tools and partner with specialized biotech firms, engineered and personalized antibodies are emerging as the central focus of market innovation.

Antibodies Drug Market Segment Analysis:

Antibodies Drug Market is segmented based on Drug type, Technology, Application, End-User and Region

By Drug Type, Monoclonal antibodies segment is expected to dominate the market with around 28% share during the forecast period.

-

The monoclonal antibodies segment remained the dominant category in 2024, accounting for over 28% of total market revenue. Its dominance is primarily due to the superior specificity, reproducibility, and consistency that monoclonal antibodies provide qualities essential for modern research in oncology, immunology, and infectious diseases. Researchers rely on mAbs because they bind to a single epitope, ensuring precise results across ELISA, Western blotting, and flow cytometry. This reliability makes them the preferred choice for large-scale clinical and academic projects.

- Their growing use in humanized and fully human therapeutic pipelines further strengthens demand. Additionally, advancements in scalable bioprocessing and rising investment in targeted therapies explain why monoclonal antibodies continue to outperform all other antibody types in research and development settings.

By Application, Oncology is expected to dominate with close to 30.88% market share during the forecast period.

-

The Oncology segment, representing 30.88% of the disease indication share in 2024, remains the largest contributor to the antibody market due to the rising global cancer burden and strong clinical adoption of targeted antibody therapies. Antibodies’ ability to bind tumor-specific antigens with high precision has made them central to modern oncology, supporting widespread use in immunotherapy, diagnostics, and personalized treatment planning. Increasing funding for oncology R&D, rapid approval of novel monoclonal, bispecific, and antibody-drug conjugate therapies, and growing use of biomarker-guided treatment selection have strengthened this segment’s dominance. With global cancer cases projected to reach 24.1 million by 2030, demand for advanced antibody-based therapies continues to rise, ensuring sustained growth and reinforcing oncology’s leading position in the antibody market.

Antibodies Drug Market Regional Insights:

North America region is estimated to lead the market with around 32.07% share during the forecast period.

-

North America dominated the global research antibodies market with a 32.07% share in 2024, supported by advanced healthcare infrastructure, extensive R&D investment, and a high concentration of pharmaceutical and biotech companies. The U.S. leads the region because of over 1.9 million annual cancer cases and widespread adoption of antibody-based assays in oncology, immunology, and neurology, which drives strong demand for research antibodies.

- The presence of numerous academic research centers, active biopharma pipelines, and regulatory support for innovative therapies further strengthen the market’s leadership. North America also benefits from advanced antibody discovery technologies, including hybridoma and phage display methods, which accelerate development. These factors collectively make the region the largest and most influential contributor to the global research antibodies market.

Antibodies Drug Market Active Players:

- AbbVie Inc. (U.S.)

- AstraZeneca (U.K.)

- Bristol-Myers Squibb Company (U.S.)

- Charles River Laboratories (U.S.)

- Eli Lilly and Company (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Genmab A/S (Denmark)

- Johnson & Johnson (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Regeneron Pharmaceuticals (U.S.)

- Sanofi S.A. (France)

- Seagen Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Other Active Players

Key Industry Developments in the Antibodies Drug Market:

-

In October 2025, Johnson & Johnson (US) advanced its antibody discovery efforts by launching a digital transformation initiative focused on cloud technologies and data analytics to accelerate R&D efficiency.

- In September 2025, AbbVie (US) strengthened its immuno-oncology portfolio by acquiring a biotech startup specializing in bispecific antibodies, expanding its therapeutic capabilities and competitive position.

Technological Advancements Accelerating Innovation and Manufacturing Efficiency in the Antibody Drugs Market

-

The antibody drugs market is being reshaped by major improvements in how these therapies are designed, tested, and manufactured. Today, researchers use advanced tools such as high-throughput screening, phage display libraries, and AI-powered modelling to identify antibodies with stronger precision and better binding capabilities. New formats like bispecific antibodies and antibody-drug conjugates allow treatments to target cancer cells more accurately or deliver powerful payloads directly to diseased tissue.

- On the manufacturing side, upgraded cell lines, modern bioreactors, and more efficient purification systems help companies produce antibodies at larger scale and lower cost. Meanwhile, sophisticated analytical methods ensure each drug meets strict safety and quality standards. Regulatory support for newer production approaches, including continuous manufacturing, is also speeding up development. Altogether, these technical advancements are enabling more effective therapies and quicker paths from research to market.

|

Antibodies Drug Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 4.30 Bn. |

|

Forecast Period 2025-32 CAGR: |

4.29% |

Market Size in 2035: |

USD 6.83 Bn. |

|

Segments Covered: |

By Drug Type |

|

|

|

By Technology |

|

||

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Antibodies Drug Market by Drug Type (2018-2035)

4.1 Antibodies Drug Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Monoclonal Antibodies

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Polyclonal Antibodies

4.5 Bispecific Antibodies

4.6 Antibody–Drug Conjugates (ADCs)

4.7 Nanobodies

Chapter 5: Antibodies Drug Market by Technology (2018-2035)

5.1 Antibodies Drug Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Recombinant DNA Technology

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Hybridoma Technology

5.5 Phage Display

5.6 Transgenic Technology

5.7 AI-Assisted Antibody Engineering

Chapter 6: Antibodies Drug Market by Application (2018-2035)

6.1 Antibodies Drug Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Oncology

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Autoimmune Disorders

6.5 Infectious Diseases

6.6 Cardiovascular Diseases

Chapter 7: Antibodies Drug Market by End-User (2018-2035)

7.1 Antibodies Drug Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Pharmaceutical & Biotechnology Companies

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Hospitals

7.5 Research Institutes

7.6 Clinical Laboratories

7.7 CROs/CMOs

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Antibodies Drug Market Share by Manufacturer/Service Provider(2024)

8.1.3 Industry BCG Matrix

8.1.4 PArtnerships, Mergers & Acquisitions

8.2 ABBVIE INC. (USA)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 ASTRAZENECA (UNITED KINGDOM)

8.4 BRISTOL-MYERS SQUIBB COMPANY (USA)

8.5 CHARLES RIVER LABORATORIES (USA)

8.6 ELI LILLY AND COMPANY (USA)

8.7 F. HOFFMANN-LA ROCHE LTD. (SWITZERLAND)

8.8 GENMAB A/S (DENMARK)

8.9 JOHNSON & JOHNSON (USA)

8.10 MERCK & CO.

8.11 INC. (USA)

8.12 NOVARTIS AG (SWITZERLAND)

8.13 PFIZER INC. (USA)

8.14 REGENERON PHARMACEUTICALS (USA)

8.15 SANOFI S.A. (FRANCE)

8.16 SEAGEN INC. (USA)

8.17 THERMO FISHER SCIENTIFIC INC. (USA) AND OTHER ACTIVE PLAYERS

Chapter 9: Global Antibodies Drug Market By Region

9.1 Overview

9.2. North America Antibodies Drug Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.2.4.1 US

9.2.4.2 Canada

9.2.4.3 Mexico

9.3. Eastern Europe Antibodies Drug Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.3.4.1 Russia

9.3.4.2 Bulgaria

9.3.4.3 The Czech Republic

9.3.4.4 Hungary

9.3.4.5 Poland

9.3.4.6 Romania

9.3.4.7 Rest of Eastern Europe

9.4. Western Europe Antibodies Drug Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.4.4.1 Germany

9.4.4.2 UK

9.4.4.3 France

9.4.4.4 The Netherlands

9.4.4.5 Italy

9.4.4.6 Spain

9.4.4.7 Rest of Western Europe

9.5. Asia Pacific Antibodies Drug Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.5.4.1 China

9.5.4.2 India

9.5.4.3 Japan

9.5.4.4 South Korea

9.5.4.5 Malaysia

9.5.4.6 Thailand

9.5.4.7 Vietnam

9.5.4.8 The Philippines

9.5.4.9 Australia

9.5.4.10 New Zealand

9.5.4.11 Rest of APAC

9.6. Middle East & Africa Antibodies Drug Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.6.4.1 Turkiye

9.6.4.2 Bahrain

9.6.4.3 Kuwait

9.6.4.4 Saudi Arabia

9.6.4.5 Qatar

9.6.4.6 UAE

9.6.4.7 Israel

9.6.4.8 South Africa

9.7. South America Antibodies Drug Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

9.7.4.1 Brazil

9.7.4.2 Argentina

9.7.4.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

Chapter 11 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12 Case Study

Chapter 13 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Antibodies Drug Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 4.30 Bn. |

|

Forecast Period 2025-32 CAGR: |

4.29% |

Market Size in 2035: |

USD 6.83 Bn. |

|

Segments Covered: |

By Drug Type |

|

|

|

By Technology |

|

||

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||