Key Market Highlights

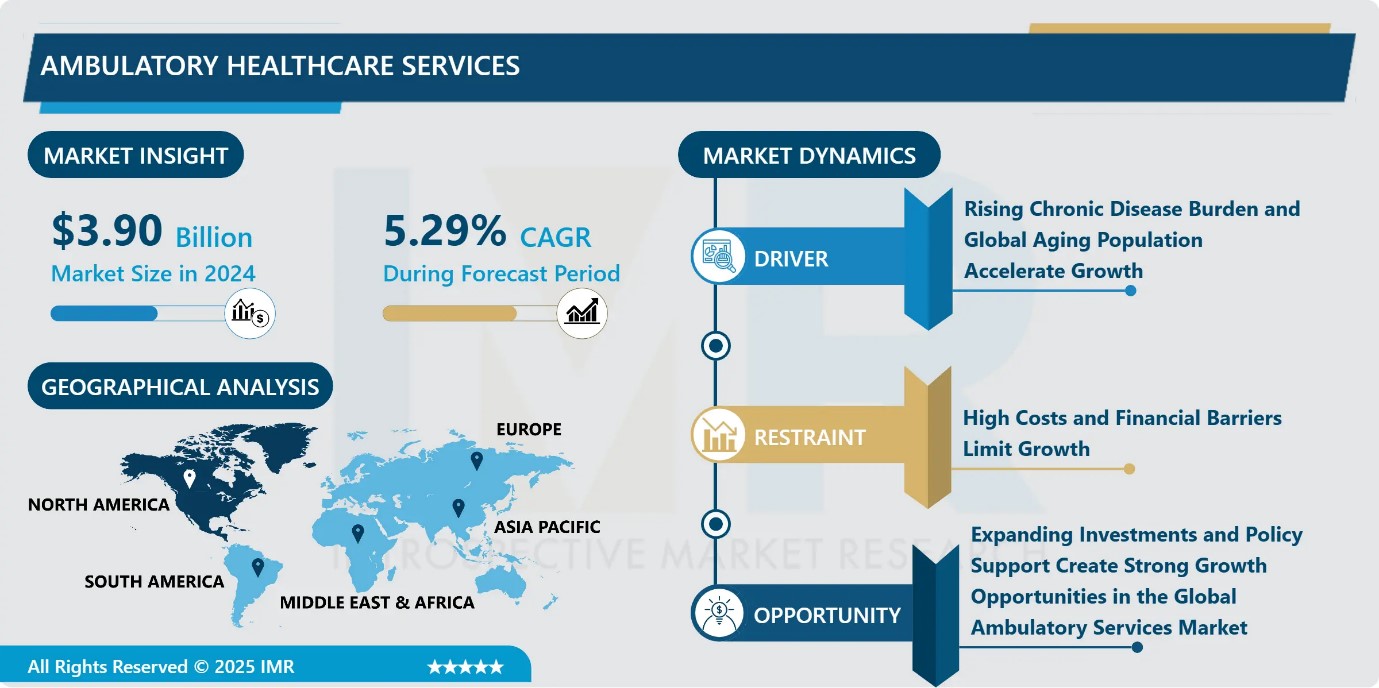

Ambulatory Healthcare Services Market Size Was Valued at USD 3.90 Billion in 2024, and is Projected to Reach USD 6.88 Billion by 2035, Growing at a CAGR of 5.29% from 2025-2035.

- Market Size in 2024: USD 3.90 Billion

- Projected Market Size by 2035: USD 6.88 Billion

- CAGR (2025–2035): 5.26%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By Specialty: The Gastroenterology segment is anticipated to lead the market by accounting for 27.80% of the market share throughout the forecast period.

- By Service Setting: The Primary Care segment is expected to capture 38.02% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 33.06% of the market share during the forecast period.

- Active Players: AmSurg Corp. (U.S.), Apollo Hospitals Enterprise Limited (India), Ascension Health (U.S.), Cleveland Clinic (U.S.), DaVita Inc. (U.S.), and Other Active Players.

Ambulatory Healthcare Services Market Synopsis:

Ambulatory healthcare services, often called outpatient care, cover diagnosis, consultations, treatments and small surgical procedures that do not require hospital admission. These facilities operate in areas such as ophthalmology, gastroenterology, orthopedics, gynecology, pain care and plastic surgery. They were created to improve access, lower costs and offer convenient medical support. Growing chronic illnesses, an aging population, supportive policies and the cost benefits of outpatient treatment are pushing demand higher. Hospitals are steadily shifting suitable procedures out of inpatient departments due to better technology and minimally invasive methods. Wider health insurance coverage, value-based care models, telemedicine and digital services also add to uptake. Although data security and regulatory issues remain, rising geriatric needs and reduced hospital stays continue to support market growth worldwide.

Ambulatory Healthcare Services Market Dynamics and Trend Analysis:

Ambulatory Healthcare Services Market Growth Driver

Rising Chronic Disease Burden and Global Aging Population Accelerate Growth

- The ambulatory services market is expanding rapidly due to the growing burden of chronic diseases and the steady rise in the elderly population. Chronic conditions now account for 71% of all global deaths, underscoring the increasing need for regular monitoring and cost-effective outpatient treatment. In the United States, 6 in 10 adults live with at least one chronic illness, while 4 in 10 manage two or more, driving strong demand for routine diagnostics, follow-up care, and disease management outside hospital settings. Demographic changes further intensify this trend. By 2030, one in every six people worldwide will be aged 60 or older, with the global elderly population increasing from 1 billion in 2020 to 1.4 billion. These patterns reinforce the growing importance of ambulatory centers as essential hubs for preventive care and long-term chronic condition management.?

Ambulatory Healthcare Services Market Limiting Factor

High Costs and Financial Barriers Limit Growth

- The high cost of ambulatory healthcare services is a major restraint on market growth. Rising expenditures for outpatient hospital and emergency care create affordability challenges, especially in emerging and underdeveloped regions where limited financial resources and underdeveloped healthcare infrastructure restrict adoption. The growth of specialty services, including orthopedics, cardiology, and oncology, further increases financial pressures. Setting up ambulatory surgical centers or specialized clinics requires significant investment in advanced medical equipment, modern operating rooms, diagnostic tools, and trained personnel. These high setup and operational costs make it difficult for smaller providers to compete, leaving the market dominated by large healthcare systems or well-funded private entities, which limits accessibility and constrains overall growth of ambulatory healthcare services globally.

Ambulatory Healthcare Services Market Expansion Opportunity

Expanding Investments and Policy Support Create Strong Growth Opportunities in the Global Ambulatory Services Market

- Growing investments in healthcare systems and supportive government measures are opening substantial opportunities for the global ambulatory services market. Many countries are strengthening primary healthcare networks to expand access and reduce the strain on hospital emergency units. For example, NHS initiatives to reinforce general practice services demonstrate how targeted public funding can enhance the delivery of outpatient care. The market is further supported by the wider use of telemedicine, which improves convenience for patients and reduces the load on physical facilities. Preventive care is also gaining prominence as healthcare providers work to limit the rise of chronic diseases. Moreover, the worldwide shift toward value-based care reflected by 67% of U.S.

Ambulatory Healthcare Services Market Challenge and Risk

Delayed Diagnoses and Workforce Shortages Impacting Service Quality and Accessibility

- Despite the advantages of ambulatory healthcare services, delayed or incorrect diagnoses remain a major challenge. Outpatient centers sometimes fail to detect serious conditions, such as cancer, due to human errors, system inefficiencies, and operational complexities, potentially causing severe patient harm or fatalities.

- In addition, workforce shortages and increasing clinician burnout further constrain the market. Limited staffing, especially in rural areas, combined with high patient loads and administrative responsibilities, reduces clinic capacity and limits access to care. These challenges increase operational pressures, strain existing resources, and affect the quality and efficiency of services. Together, delayed diagnoses and workforce constraints hinder the overall growth and effectiveness of ambulatory healthcare services globally.

Ambulatory Healthcare Services Market Trend

Advancements in Digital Health, Remote Monitoring, and Minimally Invasive Procedures Transform the Global Ambulatory Services Market

- Technological progress is reshaping the global ambulatory services market by broadening clinical capabilities and improving the efficiency of care delivery. Worldwide adoption of digital health systems continues to rise; for example, over 90% of high-income countries have implemented national electronic health record frameworks, enabling faster data exchange and better care coordination. Remote patient monitoring is expanding across regions, allowing continuous tracking of vital signs, symptoms, and treatment adherence, which helps reduce hospital readmissions and strengthens long-term disease management.

- Mobile health applications are also gaining global traction, offering patients tools for appointment scheduling, medication reminders, and self-care support. In parallel, advances in minimally invasive surgical techniques and modern diagnostic technologies now allow numerous procedures to shift from hospitals to outpatient centers, reducing recovery times and increasing accessibility, thereby driving worldwide demand for ambulatory services.

Ambulatory Healthcare Services Market Segment Analysis:

Ambulatory Healthcare Services Market is segmented based on Type Speciality, Service Setting, Technology, End-User and Region.

By Specialty, Gastroenterology segment is expected to dominate the market with around 27.80% share during the forecast period.

- Gastroenterology stands as the dominant application segment in the ambulatory healthcare services market, driven by the high global prevalence of gastrointestinal disorders and the growing shift toward minimally invasive diagnostic and therapeutic procedures. Research indicates that more than 27.80% of the global population experiences functional GI disorders. Ambulatory surgery centers frequently perform colonoscopies, endoscopic evaluations, and related interventions due to their efficiency and same-day discharge benefits.

- The adoption of advanced technologies such as capsule endoscopy and enhanced endoscopic imaging further strengthens the segment’s position. Additionally, expanding colorectal screening guidelines beginning at age 45 continue to increase patient flow, solidifying gastroenterology as the leading application category.

By Service Setting, Primary Care is expected to dominate with close to 38.02% market share during the forecast period.

- The Primary Care segment remains the dominant force in the ambulatory healthcare services market, capturing over 38.02% of total revenue in 2024. This leadership is primarily due to its role as the first access point for preventive care, routine checkups, and long-term management of chronic illnesses, which affect nearly one-third of adults worldwide. Patient dependency on continuous monitoring, prescription management, and early diagnosis keeps service volumes consistently high.

- Additionally, digital health adoption used in over 25% of primary care interactions improves efficiency and accessibility, supporting further expansion. Growing government funding, community-based care models, and rising demand for cost-effective outpatient solutions further reinforce why primary care outperforms other segments. As healthcare systems shift toward value-based care, this segment is expected to retain its dominance.

Ambulatory Healthcare Services Market Regional Insights:

North America region is estimated to lead the market with around 33.06% share during the forecast period.

North America leads the global ambulatory healthcare services market, accounting for 33.06% of total revenues in 2024. The region’s dominance is driven by advanced healthcare infrastructure, high healthcare spending, and well-established insurance coverage. The United States has over 14,000 urgent care centers and approximately 11,815 Ambulatory Surgical Centers (ASCs), supporting the growing preference for outpatient care and minimally invasive procedures. Favorable reimbursement policies, including a 2.9% Medicare payment increase for ASCs, and telehealth adoption in 23% of patient encounters further accelerate market growth. Additionally, government initiatives and the presence of major healthcare providers enhance service quality and accessibility, reinforcing North America’s position as the leading market for ambulatory healthcare services globally.

Ambulatory Healthcare Services Market Active Players:

- AmSurg Corp. (U.S.)

- Apollo Hospitals Enterprise Limited (India)

- Ascension Health (U.S.)

- Cleveland Clinic (U.S.)

- DaVita Inc. (U.S.)

- Envision Healthcare (U.S.)

- Fresenius Medical Care AG & Co. KGaA (Germany)

- HCA Healthcare Inc. (U.S.)

- IntegraMed America Inc. (U.S.)

- LabCorp (U.S.)

- Medical Facilities Corporation (Canada)

- Quest Diagnostics (U.S.)

- Sonic Healthcare Limited (Australia)

- Surgery Partners Inc. (U.S.)

- Terveystalo (Finland)

- Other Active Players

Key Industry Developments in the Ambulatory Healthcare Services Market:

- In September 2025, DaVita Inc. (US) introduced a telehealth initiative to enhance engagement and follow-up care for chronic kidney disease patients, highlighting the growing integration of digital solutions in patient-centered care.

- In June 2025, Ascension Health advanced its acquisition of AmSurg, expanding its ambulatory surgery center network and outpatient service capacity. This move aligns with Ascension’s strategic focus on ambulatory care.

Impact of Advanced Technologies on Efficiency, Accessibility, and Quality in the Global Ambulatory Healthcare Services Market

- The ambulatory healthcare services market is being transformed by advanced technologies that improve patient care, efficiency, and accessibility. Electronic Health Records (EHRs) allow seamless management of patient information, supporting better care coordination across providers. Telemedicine platforms and mobile health apps enable remote consultations, follow-ups, and continuous monitoring, reducing the need for hospital visits. Remote Patient Monitoring (RPM) devices track vital signs and medication adherence in real time, helping providers intervene early. Minimally invasive surgical techniques, robotic-assisted procedures, and advanced diagnostic imaging make complex treatments feasible in outpatient settings, shortening recovery times.

- Additionally, wearable health devices and data analytics assist in population health management by identifying risks and personalizing care plans. Together, these innovations enhance patient engagement, streamline workflows, and offer cost-effective, high-quality alternatives to traditional inpatient care, positioning ambulatory services as a central part of modern healthcare delivery.

|

Ambulatory Healthcare Services Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 3.90 BN. |

|

Forecast Period 2025-32 CAGR: |

5.29% |

Market Size in 2035: |

USD 6.88 BN. |

|

Segments Covered: |

By Specialty |

|

|

|

By Service Setting

|

|

||

|

By Technology |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Ambulatory Healthcare Service Market by Type (2018-2035)

4.1 Ambulatory Healthcare Service Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Specialty (Ophthalmology

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Orthopedics

4.5 Gastroenterology

4.6 Cardiology

4.7 Pediatrics

4.8 Plastic Surgery)

Chapter 5: Ambulatory Healthcare Service Market by Service Setting (2018-2035)

5.1 Ambulatory Healthcare Service Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Primary Care Clinics

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Surgical Specialty Clinics

5.5 Emergency Departments

Chapter 6: Ambulatory Healthcare Service Market by Technology (2018-2035)

6.1 Ambulatory Healthcare Service Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Telemedicine Platforms

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Mobile Health Applications

6.5 Remote Patient Monitoring

6.6 Electronic Health Records

6.7 Wearable Health Devices

Chapter 7: Ambulatory Healthcare Service Market by End-User (2018-2035)

7.1 Ambulatory Healthcare Service Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Ambulatory Surgery Centers

7.5 Clinics

7.6 Home Care Settings

7.7 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Ambulatory Healthcare Service Market Share by Manufacturer/Service Provider(2024)

8.1.3 Industry BCG Matrix

8.1.4 PArtnerships, Mergers & Acquisitions

8.2 AMSURG CORP. (USA)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 APOLLO HOSPITALS ENTERPRISE LIMITED (INDIA)

8.4 ASCENSION HEALTH (USA)

8.5 CLEVELAND CLINIC (USA)

8.6 DAVITA INC. (USA)

8.7 ENVISION HEALTHCARE (USA)

8.8 FRESENIUS MEDICAL CARE AG & CO. KGAA (GERMANY)

8.9 HCA HEALTHCARE INC. (USA)

8.10 INTEGRAMED AMERICA INC. (USA)

8.11 LABORATORY CORPORATION OF AMERICA HOLDINGS (USA)

8.12 MEDICAL FACILITIES CORPORATION (CANADA)

8.13 QUEST DIAGNOSTICS INCORPORATED (USA)

8.14 SONIC HEALTHCARE LIMITED (AUSTRALIA)

8.15 SURGERY PARTNERS INC. (USA)

8.16 TERVEYSTALO PLC (FINLAND)

8.17 AND OTHER ACTIVE PLAYERS

Chapter 9: Global Ambulatory Healthcare Service Market By Region

9.1 Overview

9.2. North America Ambulatory Healthcare Service Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.2.4.1 US

9.2.4.2 Canada

9.2.4.3 Mexico

9.3. Eastern Europe Ambulatory Healthcare Service Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.3.4.1 Russia

9.3.4.2 Bulgaria

9.3.4.3 The Czech Republic

9.3.4.4 Hungary

9.3.4.5 Poland

9.3.4.6 Romania

9.3.4.7 Rest of Eastern Europe

9.4. Western Europe Ambulatory Healthcare Service Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.4.4.1 Germany

9.4.4.2 UK

9.4.4.3 France

9.4.4.4 The Netherlands

9.4.4.5 Italy

9.4.4.6 Spain

9.4.4.7 Rest of Western Europe

9.5. Asia Pacific Ambulatory Healthcare Service Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.5.4.1 China

9.5.4.2 India

9.5.4.3 Japan

9.5.4.4 South Korea

9.5.4.5 Malaysia

9.5.4.6 Thailand

9.5.4.7 Vietnam

9.5.4.8 The Philippines

9.5.4.9 Australia

9.5.4.10 New Zealand

9.5.4.11 Rest of APAC

9.6. Middle East & Africa Ambulatory Healthcare Service Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.6.4.1 Turkiye

9.6.4.2 Bahrain

9.6.4.3 Kuwait

9.6.4.4 Saudi Arabia

9.6.4.5 Qatar

9.6.4.6 UAE

9.6.4.7 Israel

9.6.4.8 South Africa

9.7. South America Ambulatory Healthcare Service Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

9.7.4.1 Brazil

9.7.4.2 Argentina

9.7.4.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

Chapter 11 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12 Case Study

Chapter 13 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Ambulatory Healthcare Services Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 3.90 BN. |

|

Forecast Period 2025-32 CAGR: |

5.29% |

Market Size in 2035: |

USD 6.88 BN. |

|

Segments Covered: |

By Specialty |

|

|

|

By Service Setting

|

|

||

|

By Technology |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||