Aerospace Materials Market Overview

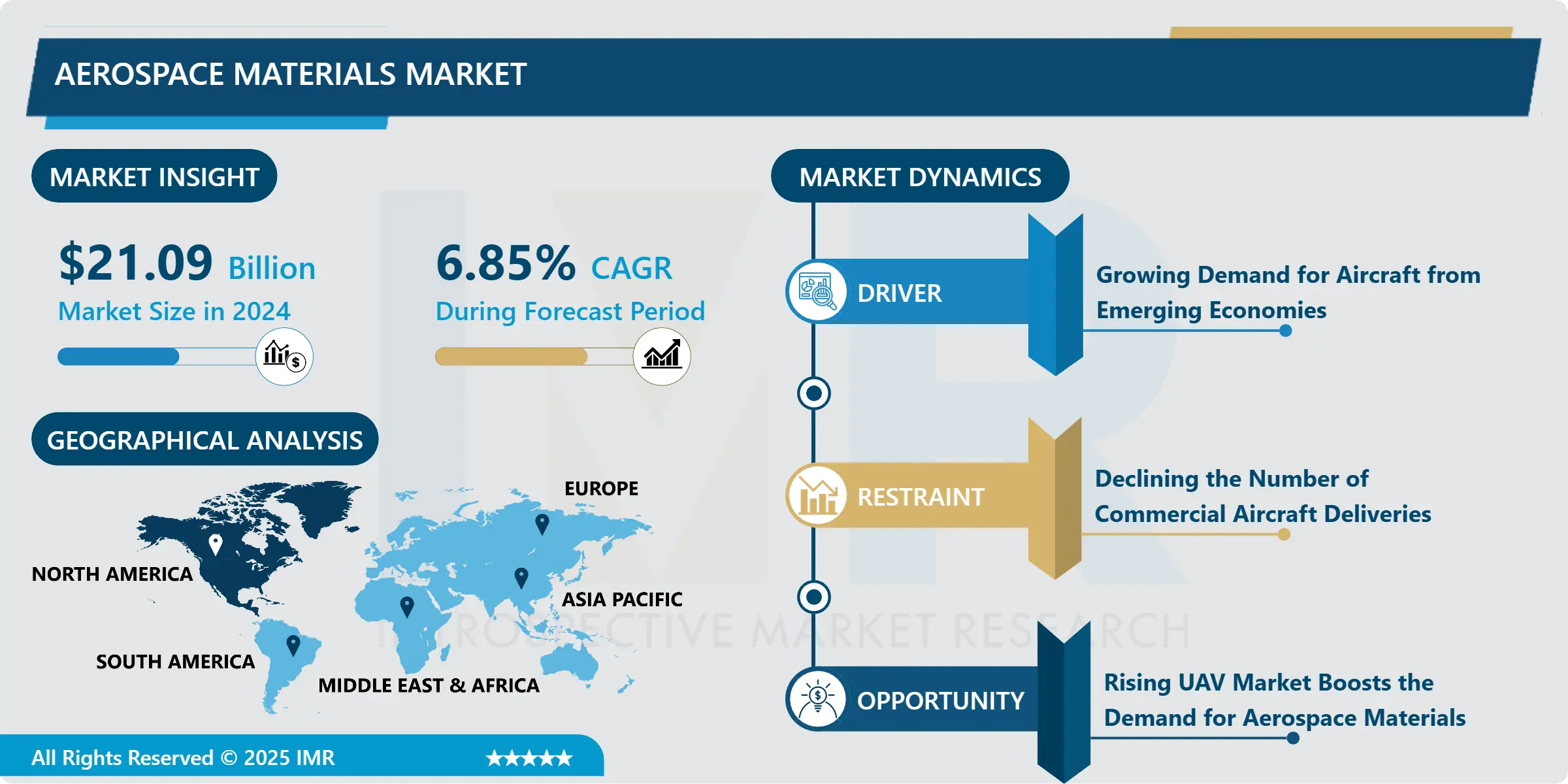

The Global Aerospace Materials market was valued at USD 21.09 billion in 2024 and is expected to reach USD 35.84 billion by the year 2032, at a CAGR of 6.85%

Aerospace materials are referred to as the materials which are utilized by the aircraft OEMs & component producers for creating various aircraft parts. The materials applied in airplane design have been constantly developing. Prior flights were primarily built of spruce and ash wood with muslin covering the wings, while today's airliners are produced mostly of aluminum with some structure made from steel. Aluminum is thin, technically developed in terms of forming and alloying, and it is relatively cheap cost, especially when compared to other composites hence providing effective aerodynamic features to the airplane. Furthermore, materials such as titanium alloys, steel alloys, superalloys, aluminum alloys, and composite materials are utilized to manufacture aircraft. Composite materials in aerospace are applied primarily owing to they have higher strength to weight ratio than metals. Hence, they help inefficient application of fuel enable in declining harmful fuel emissions into the atmosphere. The different types of aerospace composites such as glass fiber reinforced plastics, carbon fiber reinforced plastics, metal matrix composites (MMC), aramid fiber composites, and ceramic matrix composites (CMC). Amidst the COVID-19 pandemic, the global market for Aerospace Materials is estimated to gain US$25.1 Billion by 2027, over the analysis period.

COVID-19 Impact on Aerospace Materials Market

The market was poorly influenced by COVID-19 in 2020. Due to the crisis and the lockdowns foisted to restraints the spread of the virus, passenger air-travel activities were temporarily shut down. Even after the lockdown ended, people were hesitant to travel frequently. As per the International Civil Aviation Organization (ICAO), the overall number of passengers globally bring down by 92% in April 2020, compared to the same month in 2019. In addition, international traffic was demolished by 98%. These factors declined the development of the aerospace industry, which, in turn, poorly impacted the demand for the Aerospace Materials market. Furthermore, the interruption in the supply chain resulting in delays or non-arrival of raw materials disrupted financial flows, and rising defection among production line workers have forced aerospace component manufacturers to operate at partial capacities.

Market Dynamics And Factors For The Aerospace Materials Market

Aerospace Materials Market Drivers- Increasing Demand for Commercial Air Travel

Growth in the aerospace materials market is set to be accelerated mainly by the strongly rising commercial air travel demand. The demand for stronger, lighter, quieter operating, safer, fuel-efficient and lower emission aircraft is turning demand for next-generation materials in manufacturing. Some of the major factors turning growth in the market include the growth in the number of orders and deliveries for new and wide-bodied commercial aircraft, rising number of low-cost carriers, growing demand for lightweight and more fuel-efficient aircraft, and technological developments in composite materials. Low-cost carriers (LCCs) have proved to be strong competitors in the market, especially in the emerging countries of APAC and South America. More travelers are expected to fly more often in the MEA and APAC. Aircraft carriers such as Emirates (UAE), Qatar Airways (Qatar), and Etihad Airways (UAE) are among the biggest players in commercial aviation in the Middle East and carry the majority of passengers who travel between APAC and Europe. The number of people applying air transport is rising, driving the demand for larger airplanes. This demand will bring business opportunities to companies providing aerospace materials and other required components in the aircraft manufacturing industry.

Aerospace Materials Market Restraints- The decline in the number of aircraft deliveries

The decline in the number of aircraft deliveries would directly affect the aerospace materials market. Since more than 80% of the utilization of composite material is in commercial aircraft, the decline in demand for composite owing to the reduced number of aircraft orders would poorly impact the aerospace materials market. For example, the grounding of Boeing 737MAX resulting from accidents suffered by the Malaysian and Ethiopian Airlines, recently, resulted in the cancellation of its orders. In the first quarter of 2020, Airbus and Boeing delivered 122 and 50 commercial aircraft worldwide, which is 22% and 66% less as compared with the first quarter of 2019.

Aerospace Materials Market Opportunities- Rising UAV Market boosting the demand for aerospace materials

UAV (drone) applications in the military have matured, becoming a key asset in military organizations globally and creating business opportunities. Nevertheless, the civil and commercial market for UAVs is in its incipient phases with significant unrealized potential in a wide number of utilizations. Military expenditure for UAV technology is expected to increase as a total percentage of military budgets, providing growth opportunities to specialized drone producers and software developers.

Market Segmentation

Segmentation Analysis of Aerospace Materials Market:

Based on the Aircraft Type, the Commercial Aircraft segment is expected to record the maximum Aerospace Materials market share during the forecast period. General and commercial aircraft are utilized for various purposes, including civil aviation (both private and commercial) and passenger and freight transportation. The demand for aircraft is rising as air passengers are continuously growing in developing economies. As per the International Air Transport Association (IATA), the global air transport industry was valued at USD 838 billion in 2019. It gained over USD 419 billion in 2020, registering a decreasing rate of 50%. Honeywell projected that approximately 7,700 new aircraft deliveries may occur by 2028. Single-aisle aircraft are mainly utilized for commercial purposes. As per Boeing, 32,270 units of single-aisle aircraft (narrow-body aircraft) will be provided globally in the next 20 years, which may grow the demand for aerospace materials in the coming years. This rise will produce additional demand for newer aircraft resulting in aerospace materials demand.

Based on Type, the composite materials segment is expected to register the largest share of the Aerospace Materials market over the forecast period. Composites are increasingly being opted over traditional material for the production of a range of products for the simple reason that they combine properties of different constituent materials to offer more benefits and features to the end-users. Composite materials are thus turning the trend of one-piece designs, or fewer components in aircraft assembly. Man-made composite materials utilized in the aerospace industry mainly comprise carbon-fiber-reinforced plastic (CFRP) and glass-fiber-reinforced plastic (GFRP). CFRPs are the most applied composite materials in both functional and cabin components currently. Aircraft OEMs have started including considerable amounts of carbon composites even in single-aisle, long in-service passenger jets.

Based on the Application, the structural frames segment is expected to register the largest share for the Aerospace Materials market over the forecast period. Materials such as aluminum are compared very suitable for aircraft's frame owing to the lightweight and strength. In addition, aerospace materials utilized in structural frames are lighter than steel and hence enable higher aircraft payload and improved fuel efficiency. Also, materials such as aluminum are majorly resistant to corrosion thereby enhancing aircraft safety.

Regional Analysis of Aerospace Materials Market:

The North American region is expected to dominate the aerospace materials market over the forecast period. The US represents the maximum market for aerospace materials, primarily owing to significant research and development investments by the government in the aerospace sector, the presence of various major aircraft manufacturers such as Carpenter Technology Corporation (US), Allegheny Technologies Incorporated (US), ATI Metals (US), and others, also the adoption of different growth strategies, such as developments and mergers and accession by leading market participants.

Players Covered in Aerospace Materials Market are :

- Carpenter Technology Corporation (US)

- Constellium SE (France)

- Rio Tinto Group (UK)

- Toray Industries Inc. (Japan)

- Alcoa Corporation (US)

- Teijin Limited (Japan)

- Hexcel Corporation (US)

- AMG N.V. (Netherlands)

- NOVELIS (US)

- Hexcel (US)

- Aleris Corporation (US)

- Arconic Inc. (the US)

- Allegheny Technologies Incorporated (US)

- ATI Metals (US)

- Kaiser Aluminum (US)

- VSMPO-AVISMA Corporation (Russia)

- Kobe Steel Ltd. (Japan)

- TIMET (Berkshire Hathaway Inc.) (US)

- DuPont de Nemours Inc. (the US)

- and others active Players.

Key Industry Developments In The Aerospace Materials Market

- December 2023: Teijin Limited announced the production and sale of Tenax Carbon Fiber, made using sustainable acrylonitrile (AN) waste and leftover biomass materials. This innovative carbon fiber supported industries like aerospace by offering an eco-friendly solution without compromising performance. The development highlighted Teijin's commitment to sustainability and advancing green technologies for diverse industrial applications.

- June 2023: Toray Industries showcased its cutting-edge composite material solutions at the 2023 Paris Air Show, highlighting TORAYCA carbon fiber, thermoset materials, and thermoplastic composites. The company facilitated large-scale composite adoption in commercial and general aviation and advanced next-generation programs through innovative product launches, reaffirming its leadership in aerospace materials innovation.

|

Aerospace Materials Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 21.09 Bn. |

|

Forecast Period 2022-28 CAGR: |

6.85% |

Market Size in 2032: |

USD 35.84 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Aircraft Type |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Aerospace Materials Market by Type (2018-2032)

4.1 Aerospace Materials Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Steel Alloys

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Titanium Alloys

4.5 Aluminum Alloys

4.6 Super Alloys

4.7 Plastics

4.8 Others

Chapter 5: Aerospace Materials Market by Aircraft Type (2018-2032)

5.1 Aerospace Materials Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Commercial Aircraft

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Business & General Aviation

5.5 Military Aircraft

5.6 Helicopters

5.7 Rotorcrafts

5.8 Others

Chapter 6: Aerospace Materials Market by Application (2018-2032)

6.1 Aerospace Materials Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Structural Frames

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Cabin Interiors

6.5 Propulsion System

6.6 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Aerospace Materials Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 CARRIER

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 EMERSON ELECTRIC COMPANY

7.4 GEA GROUP

7.5 BEVERAGE-AIR CORPORATION

7.6 DAIKIN INDUSTRIES LTDDANFOSS A/S

7.7 DOVER CORPORATION

7.8 ELECTROLUX AB

7.9 GE APPLIANCES

7.10 HUSSMANN CORPORATION

7.11 ILLINOIS TOOL WORKS INCINGERSOLL-RAND PLC

7.12 METALFRIO SOLUTIONS SA

7.13 UNITED TECHNOLOGIES CORPORATION

7.14 WHIRLPOOL CORPORATION

7.15 STANDEX INTERNATIONAL CORPORATION

7.16 LENNOX INTERNATIONAL INCDAIKIN INDUSTRIESLTDAHT COOLING SYSTEMS GMBH

7.17 MANITOWOC COMPANY INCPANASONIC CORPORATION

7.18 HOSHIZAKI CORPORATION

Chapter 8: Global Aerospace Materials Market By Region

8.1 Overview

8.2. North America Aerospace Materials Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Steel Alloys

8.2.4.2 Titanium Alloys

8.2.4.3 Aluminum Alloys

8.2.4.4 Super Alloys

8.2.4.5 Plastics

8.2.4.6 Others

8.2.5 Historic and Forecasted Market Size by Aircraft Type

8.2.5.1 Commercial Aircraft

8.2.5.2 Business & General Aviation

8.2.5.3 Military Aircraft

8.2.5.4 Helicopters

8.2.5.5 Rotorcrafts

8.2.5.6 Others

8.2.6 Historic and Forecasted Market Size by Application

8.2.6.1 Structural Frames

8.2.6.2 Cabin Interiors

8.2.6.3 Propulsion System

8.2.6.4 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Aerospace Materials Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Steel Alloys

8.3.4.2 Titanium Alloys

8.3.4.3 Aluminum Alloys

8.3.4.4 Super Alloys

8.3.4.5 Plastics

8.3.4.6 Others

8.3.5 Historic and Forecasted Market Size by Aircraft Type

8.3.5.1 Commercial Aircraft

8.3.5.2 Business & General Aviation

8.3.5.3 Military Aircraft

8.3.5.4 Helicopters

8.3.5.5 Rotorcrafts

8.3.5.6 Others

8.3.6 Historic and Forecasted Market Size by Application

8.3.6.1 Structural Frames

8.3.6.2 Cabin Interiors

8.3.6.3 Propulsion System

8.3.6.4 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Aerospace Materials Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Steel Alloys

8.4.4.2 Titanium Alloys

8.4.4.3 Aluminum Alloys

8.4.4.4 Super Alloys

8.4.4.5 Plastics

8.4.4.6 Others

8.4.5 Historic and Forecasted Market Size by Aircraft Type

8.4.5.1 Commercial Aircraft

8.4.5.2 Business & General Aviation

8.4.5.3 Military Aircraft

8.4.5.4 Helicopters

8.4.5.5 Rotorcrafts

8.4.5.6 Others

8.4.6 Historic and Forecasted Market Size by Application

8.4.6.1 Structural Frames

8.4.6.2 Cabin Interiors

8.4.6.3 Propulsion System

8.4.6.4 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Aerospace Materials Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Steel Alloys

8.5.4.2 Titanium Alloys

8.5.4.3 Aluminum Alloys

8.5.4.4 Super Alloys

8.5.4.5 Plastics

8.5.4.6 Others

8.5.5 Historic and Forecasted Market Size by Aircraft Type

8.5.5.1 Commercial Aircraft

8.5.5.2 Business & General Aviation

8.5.5.3 Military Aircraft

8.5.5.4 Helicopters

8.5.5.5 Rotorcrafts

8.5.5.6 Others

8.5.6 Historic and Forecasted Market Size by Application

8.5.6.1 Structural Frames

8.5.6.2 Cabin Interiors

8.5.6.3 Propulsion System

8.5.6.4 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Aerospace Materials Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Steel Alloys

8.6.4.2 Titanium Alloys

8.6.4.3 Aluminum Alloys

8.6.4.4 Super Alloys

8.6.4.5 Plastics

8.6.4.6 Others

8.6.5 Historic and Forecasted Market Size by Aircraft Type

8.6.5.1 Commercial Aircraft

8.6.5.2 Business & General Aviation

8.6.5.3 Military Aircraft

8.6.5.4 Helicopters

8.6.5.5 Rotorcrafts

8.6.5.6 Others

8.6.6 Historic and Forecasted Market Size by Application

8.6.6.1 Structural Frames

8.6.6.2 Cabin Interiors

8.6.6.3 Propulsion System

8.6.6.4 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Aerospace Materials Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Steel Alloys

8.7.4.2 Titanium Alloys

8.7.4.3 Aluminum Alloys

8.7.4.4 Super Alloys

8.7.4.5 Plastics

8.7.4.6 Others

8.7.5 Historic and Forecasted Market Size by Aircraft Type

8.7.5.1 Commercial Aircraft

8.7.5.2 Business & General Aviation

8.7.5.3 Military Aircraft

8.7.5.4 Helicopters

8.7.5.5 Rotorcrafts

8.7.5.6 Others

8.7.6 Historic and Forecasted Market Size by Application

8.7.6.1 Structural Frames

8.7.6.2 Cabin Interiors

8.7.6.3 Propulsion System

8.7.6.4 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Aerospace Materials Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 21.09 Bn. |

|

Forecast Period 2022-28 CAGR: |

6.85% |

Market Size in 2032: |

USD 35.84 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Aircraft Type |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||