Key Market Highlights

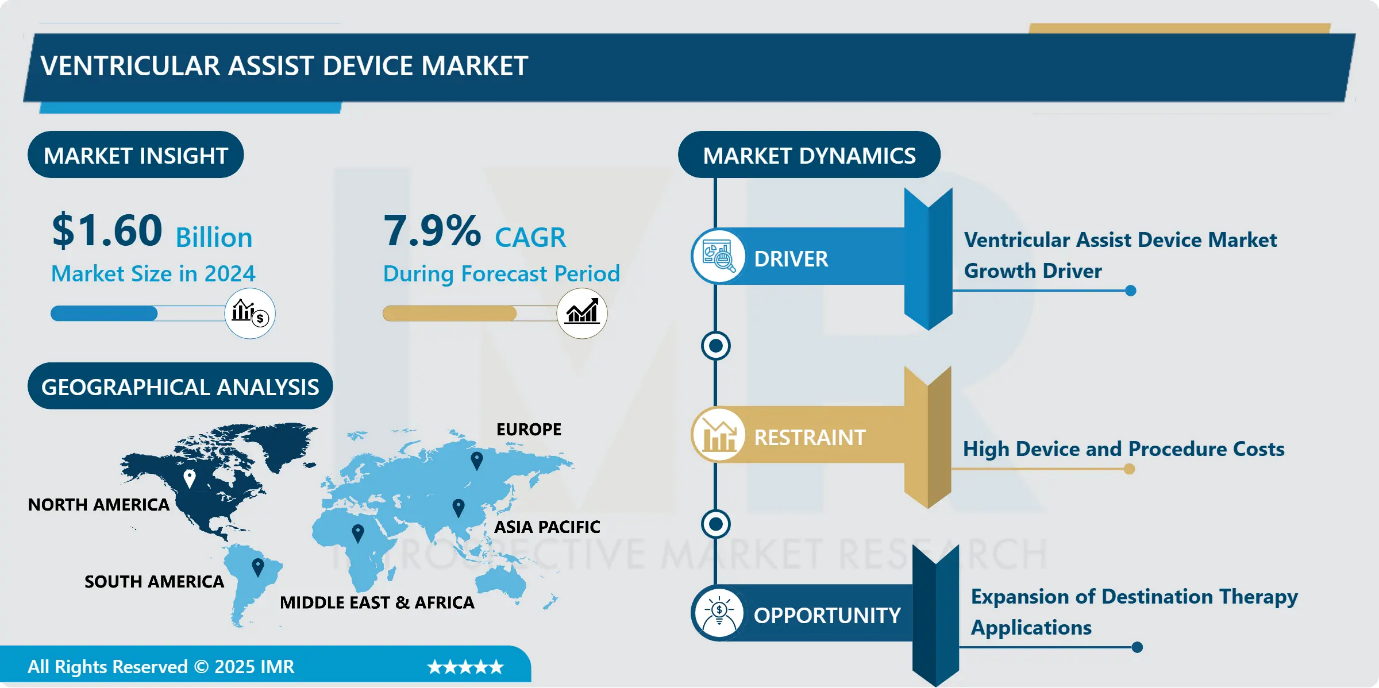

Ventricular Assist Device Market Size Was Valued at USD 1.60 Billion in 2024, and is Projected to Reach USD 3.69 Billion by 2035, Growing at a CAGR of 7.9% from 2025-2035.

- Market Size in 2024: USD 1.60 Billion

- Projected Market Size by 2035: USD 3.69 Billion

- CAGR (2025–2035): 7.9%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By Design: The Implantable Ventricular Assist Device segment is anticipated to lead the market by accounting for 57.8% of the market share throughout the forecast period.

- By Application: The Bridge to Transplant segment is expected to capture 30.8% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 33.6% of the market share during the forecast period.

- Active Players: Abbott (United States), Abiomed (United States), Berlin Heart GmbH (Germany), Cardiac Assist, Inc. (United States), Cirtec Medical (United States), and Other Active Players.

Ventricular Assist Device Market Synopsis:

A ventricular assist device (VAD) is a surgically implanted mechanical pump that supports heart function by assisting weakened ventricles in circulating blood throughout the body. VADs are primarily used in patients with advanced heart failure whose hearts cannot pump sufficient blood to meet the body’s needs. These devices improve cardiac output, alleviate symptoms, and enhance quality of life for months or years. Left ventricular assist devices (LVADs) are the most commonly used, while right and biventricular devices support additional cardiac functions. VADs are applied as bridge-to-transplant, bridge-to-recovery, bridge-to-candidacy, or destination therapy for patients ineligible for transplantation. Rising heart failure prevalence, aging populations, and technological advancements in device design continue to drive the global VAD market.

Ventricular Assist Device Market Dynamics and Trend Analysis:

Ventricular Assist Device Market Growth Driver - Growing Geriatric Population

- The increasing geriatric population is a significant driver for the Ventricular Assist Devices Market. As individuals age, the risk of developing heart-related conditions, including heart failure, escalates. This demographic shift is expected to lead to a higher demand for ventricular assist devices as older adults often require advanced medical interventions to manage their health. According to demographic studies, the proportion of individuals aged 65 and older is projected to rise substantially in the coming years. This trend suggests that healthcare systems will need to adapt to accommodate the needs of an aging population, thereby creating opportunities for growth within the Ventricular Assist Devices Market.

Ventricular Assist Device Market Limiting Factor - High Device and Procedure Costs

- The high cost associated with ventricular assist device implantation remains a major restraint to market growth, particularly in price-sensitive regions. The procedure involves substantial expenses related to the device, surgery, hospitalization, and post-operative care, with additional financial burden from readmissions. Limited reimbursement coverage from insurers and the requirement for significant capital investment restrict adoption, especially among smaller healthcare facilities. Although improvements in battery life and reduced complication rates are gradually enhancing cost-effectiveness, the upfront financial barriers continue to limit broader penetration of VADs. These economic challenges may slow market expansion despite the growing clinical demand for advanced heart failure therapies.

Ventricular Assist Device Market Expansion Opportunity - Expansion of Destination Therapy Applications

- The growing shortage of donor organs presents a significant market opportunity for ventricular assist devices, particularly in destination therapy applications. Advances in pump durability and long-term performance have enabled VADs to be used as permanent circulatory support, reducing reliance on heart transplantation. Clinical evidence indicates that left ventricular assist device (LVAD) survival rates are approaching those of heart transplants in selected patient populations, especially individuals under 50 years of age. Leading cardiac centers have reported multi-year survival outcomes exceeding registry benchmarks, reinforcing confidence in long-term VAD use. These favorable outcomes are encouraging updates to clinical guidelines and expanding the adoption of destination therapy globally.

Ventricular Assist Device Market Challenge and Risk - Device-Related Complications and Safety Recalls

- Device-related complications and safety recalls continue to pose a significant challenge to the ventricular assist device market. High-profile recall events have highlighted the clinical, financial, and reputational risks associated with device malfunctions, negatively impacting confidence among patients and healthcare providers. Complications such as bleeding, infection, and mechanical failure can lead to additional interventions, prolonged recovery, and increased healthcare costs. Although recent protocol improvements, including revised anticoagulation strategies, have reduced certain adverse events, safety concerns remain a barrier to wider adoption. Strengthening post-market surveillance, enhancing device reliability, and ensuring long-term safety performance are critical to overcoming these challenges and supporting sustained market growth.

Ventricular Assist Device Market Trend - Technological Innovations in Ventricular Assist Devices

- Rapid technological advancements are emerging as a key trend shaping the ventricular assist devices market. Ongoing innovations in device miniaturization, durability, and biocompatibility are improving clinical outcomes while enhancing patient comfort and safety. The adoption of magnetic levitation pump technology, such as next-generation LVADs, has significantly reduced thrombosis risk and improved long-term survival rates compared to conventional systems. In addition, miniaturized percutaneous pumps with smaller delivery profiles enable less invasive procedures and higher procedural success rates. The development of wireless power transfer and remote monitoring technologies further supports the shift toward fully implantable, cable-free devices, broadening clinical applications and driving market growth.

Ventricular Assist Device Market Segment Analysis:

Ventricular Assist Device Market is segmented based on Product Type, Type of Flow/Technology, Design, Application, End User, and Region.

By Design, Implantable ventricular assist segment is expected to dominate the market with around 57.8% share during the forecast period.

- Implantable ventricular assist devices currently dominate the market, accounting for over 80% of total revenue, due to their proven long-term durability and ability to provide sustained circulatory support for advanced heart failure patients. These systems remain the preferred option for destination therapy and extended bridge-to-transplant applications, supporting their continued dominance through 2031. However, percutaneous micro-axial devices are gaining momentum, driven by their minimally invasive nature and compatibility with catheterization-lab workflows. Innovations have extended percutaneous support duration, enabling temporary therapies once limited to implantable systems. Despite this growth, implantable devices remain dominant because of superior longevity, established clinical evidence, and broader therapeutic indications.

By Application, Bridge-to-Transplant is expected to dominate with close to 30.8% market share during the forecast period.

- Bridge-to-Transplant (BTT) currently represents the largest share of the ventricular assist devices market, accounting for nearly half of total adoption. Its dominance is driven by long-established surgical expertise, strong clinical guidelines, and well-defined reimbursement pathways developed over decades. However, Destination Therapy (DT) is emerging as the fastest-growing application, registering a robust CAGR. Improved device durability and clinical outcomes have demonstrated survival rates in selected patient groups comparable to heart transplantation. As evidence supporting long-term VAD use strengthens and donor organ shortages persist, DT adoption is accelerating. Despite rapid growth in DT, BTT remains dominant due to entrenched infrastructure, clinician familiarity, and transplant-centered treatment pathways.

Ventricular Assist Device Market Regional Insights:

North America region is estimated to lead the market with around 33.6% share during the forecast period.

- North America dominates the ventricular assist devices market due to the high burden of cardiovascular diseases and advanced heart failure across the region. Strong reimbursement frameworks, particularly through public healthcare programs, support patient access and encourage widespread clinical adoption. The presence of well-established centers of excellence, comprehensive clinical registries, and transparent outcome reporting further strengthens physician confidence in these devices.

- In addition, frequent collaborations, strategic partnerships, and an active innovation ecosystem position the region as the primary launch market for advanced ventricular assist technologies. Europe remains a key secondary market, driven by increasing investments, supportive research initiatives, and the introduction of innovative ventricular assist systems.

Ventricular Assist Device Market Active Players:

- Abbott (United States)

- Abiomed (United States)

- Berlin Heart GmbH (Germany)

- Cardiac Assist, Inc. (United States)

- Cirtec Medical (United States)

- CorWave SA (France)

- Evaheart, Inc. (Japan)

- FineHeart (France)

- Getinge AB (Sweden)

- Jarvik Heart, Inc. (United States)

- Medtronic plc (Ireland)

- ReliantHeart, Inc. (United States)

- Sun Medical Technology Research Corp. (Japan)

- SynCardia Systems, LLC (United States)

- Terumo Corporation (Japan)

- Other Active Players

Key Industry Developments in the Ventricular Assist Device Market:

- In March 2025, Cadrenal Therapeutics, in collaboration with Abbott, initiated the TECH-LVAD clinical trial. The study evaluates the use of tecarfarin as an anticoagulant in patients implanted with the HeartMate 3 device. This trial aims to optimize anticoagulation management and improve clinical outcomes for LVAD recipients.

- In February 2025, Abbott obtained CE Mark approval for its AVEIR DR dual-chamber leadless pacemaker. This regulatory milestone strengthened the company’s cardiovascular portfolio. The approval supports broader adoption of advanced heart-failure management technologies across European markets.

Design, Operating Mechanism, and Technological Evolution of Ventricular Assist Devices

- Ventricular assist devices (VADs) are advanced mechanical circulatory support systems designed to aid compromised cardiac ventricles in maintaining adequate blood flow. Technically, VADs consist of a blood pump, inflow and outflow cannulas, a driveline or wireless power interface, an external controller, and a power source. Modern devices predominantly utilize continuous-flow technology with axial or centrifugal pumps, offering improved durability, reduced size, and lower thrombosis risk compared to earlier pulsatile systems. Innovations such as magnetic levitation rotors enhance hemocompatibility by minimizing mechanical wear and blood trauma.

- Implantable VADs support long-term applications, including destination therapy and bridge-to-transplant, while percutaneous systems enable short-term hemodynamic support through minimally invasive placement. Integration of real-time monitoring, advanced control algorithms, and improved battery management systems enhances device reliability and patient safety. Ongoing R&D focuses on fully implantable, cable-free designs, biocompatible materials, and optimized anticoagulation protocols to improve long-term outcomes.

|

Ventricular Assist Device Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 1.60 Bn. |

|

Forecast Period 2025-32 CAGR: |

7.9 % |

Market Size in 2035: |

USD 3.69 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Type of Flow/Technology |

|

||

|

By Design |

|

||

|

By Application

|

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Ventricular Assist Device Market by Product Type (2018-2035)

4.1 Ventricular Assist Device Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Left Ventricular Assist Device

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Right Ventricular Assist Device

4.5 Biventricular Assist Device

4.6 and Total Artificial Heart

Chapter 5: Ventricular Assist Device Market by Type of Flow/Technology (2018-2035)

5.1 Ventricular Assist Device Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Continuous Flow and Pulsatile Flow

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

Chapter 6: Ventricular Assist Device Market by Design (2018-2035)

6.1 Ventricular Assist Device Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Implantable Ventricular Assist Device and Transcutaneous Ventricular Assist Device

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

Chapter 7: Ventricular Assist Device Market by Application (2018-2035)

7.1 Ventricular Assist Device Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Destination Therapy

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Bridge to Transplant

7.5 Bridge to Candidacy

7.6 and Bridge to Recovery

Chapter 8: Ventricular Assist Device Market by End User (2018-2035)

8.1 Ventricular Assist Device Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospitals & Ambulatory Surgical Centers

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Specialty Clinics

8.5 and Others

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Ventricular Assist Device Market Share by Manufacturer/Service Provider(2024)

9.1.3 Industry BCG Matrix

9.1.4 PArtnerships, Mergers & Acquisitions

9.2 ABBOTT (UNITED STATES)

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 ABIOMED (UNITED STATES)

9.4 BERLIN HEART GMBH (GERMANY)

9.5 CARDIAC ASSIST

9.6 INC. (UNITED STATES)

9.7 CIRTEC MEDICAL (UNITED STATES)

9.8 CORWAVE SA (FRANCE)

9.9 EVAHEART

9.10 INC. (JAPAN)

9.11 FINEHEART (FRANCE)

9.12 GETINGE AB (SWEDEN)

9.13 JARVIK HEART

9.14 INC. (UNITED STATES)

9.15 MEDTRONIC PLC (IRELAND)

9.16 RELIANTHEART

9.17 INC. (UNITED STATES)

9.18 SUN MEDICAL TECHNOLOGY RESEARCH CORP. (JAPAN)

9.19 SYNCARDIA SYSTEMS

9.20 LLC (UNITED STATES)

9.21 TERUMO CORPORATION (JAPAN)

9.22 AND OTHER ACTIVE PLAYERS.

Chapter 10: Global Ventricular Assist Device Market By Region

10.1 Overview

10.2. North America Ventricular Assist Device Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.2.4.1 US

10.2.4.2 Canada

10.2.4.3 Mexico

10.3. Eastern Europe Ventricular Assist Device Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.3.4.1 Russia

10.3.4.2 Bulgaria

10.3.4.3 The Czech Republic

10.3.4.4 Hungary

10.3.4.5 Poland

10.3.4.6 Romania

10.3.4.7 Rest of Eastern Europe

10.4. Western Europe Ventricular Assist Device Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.4.4.1 Germany

10.4.4.2 UK

10.4.4.3 France

10.4.4.4 The Netherlands

10.4.4.5 Italy

10.4.4.6 Spain

10.4.4.7 Rest of Western Europe

10.5. Asia Pacific Ventricular Assist Device Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.5.4.1 China

10.5.4.2 India

10.5.4.3 Japan

10.5.4.4 South Korea

10.5.4.5 Malaysia

10.5.4.6 Thailand

10.5.4.7 Vietnam

10.5.4.8 The Philippines

10.5.4.9 Australia

10.5.4.10 New Zealand

10.5.4.11 Rest of APAC

10.6. Middle East & Africa Ventricular Assist Device Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.6.4.1 Turkiye

10.6.4.2 Bahrain

10.6.4.3 Kuwait

10.6.4.4 Saudi Arabia

10.6.4.5 Qatar

10.6.4.6 UAE

10.6.4.7 Israel

10.6.4.8 South Africa

10.7. South America Ventricular Assist Device Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

10.7.4.1 Brazil

10.7.4.2 Argentina

10.7.4.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

Chapter 12 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 13 Case Study

Chapter 14 Appendix

12.1 Sources

12.2 List of Tables and figures

12.3 Short Forms and Citations

12.4 Assumption and Conversion

12.5 Disclaimer

|

Ventricular Assist Device Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 1.60 Bn. |

|

Forecast Period 2025-32 CAGR: |

7.9 % |

Market Size in 2035: |

USD 3.69 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Type of Flow/Technology |

|

||

|

By Design |

|

||

|

By Application

|

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||