Solenoid Actuator Market Synopsis:

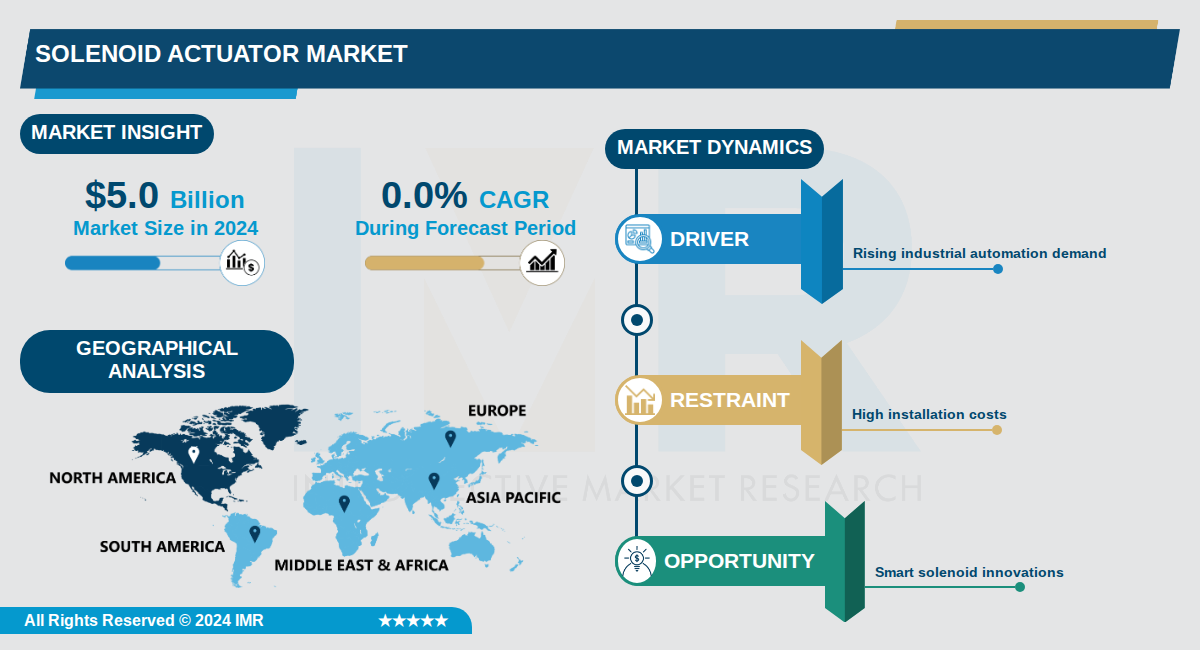

Solenoid Actuator Market Size Was Valued at USD 5.0 Billion in 2024, and is Projected to Reach USD 5.0 Billion by 2035, Growing at a CAGR of 0.0% From 2024-2035.

The global Solenoid Actuator Market reached $5.0 billion in 2024 and is projected to remain stable at $5.0 billion by 2035, reflecting a compound annual growth rate (CAGR) of -0.0% over the forecast period. This stagnation highlights a mature market characterized by balanced supply-demand dynamics across key industries such as automotive, HVAC, machinery, and automation. Despite broader trends of growth in related segments like solenoid valves and automotive solenoids, the overall solenoid actuator sector faces equilibrium due to offsetting factors.

Solenoid actuators, essential components for precise electromechanical control in applications ranging from industrial automation to fluid management, continue to serve diverse end-use industries including construction, energy, and manufacturing. Market segmentation by type, application, and region reveals steady performance, with pneumatic solenoid valves holding a notable share in 2023 and projections indicating sustained demand in smart machinery and electric-powered equipment. Regional analysis underscores leadership in Asia Pacific, driven by automotive production in China, alongside contributions from North America and emerging markets.

Competitive dynamics feature major players focusing on innovations such as IoT integration, energy efficiency, and compatibility with Industry 4.0 infrastructures. While sub-markets like automotive solenoids exhibit CAGRs up to 7.1% and solenoid valves around 4.7%, the broader solenoid actuator market's flat trajectory is informed by comprehensive trend analysis, including historical data from 2021-2024 and forecasts through 2035, emphasizing stability amid technological evolution.

Solenoid Actuator Market Trend Analysis:

Integration of IoT and AI in Solenoid Actuators

- Manufacturers like LINTEC CO. LTD. are embedding IoT sensors and AI algorithms into solenoid actuators to enable predictive maintenance and real-time performance monitoring, reducing downtime by up to 30% in industrial applications such as CNC machinery and robotics. This integration allows actuators to self-diagnose faults and adjust operations dynamically based on data from connected systems. For instance, in assembly lines, AI-driven solenoids optimize energy use by predicting load variations, aligning with Industry 4.0 standards.

- The adoption is accelerating in automotive sectors where companies like Bosch are deploying AI-enhanced solenoid actuators in new energy vehicles for precise powertrain control, improving efficiency by 15% over traditional models. These smart actuators communicate via IoT networks to synchronize with vehicle telematics, enhancing safety features like automatic braking systems. Market projections indicate this segment will grow at a 12% CAGR through 2035 due to rising demand for connected machinery.

- In HVAC systems, Lesman is leading with IoT-integrated solenoids that use AI for remote monitoring, cutting energy consumption by 25% in commercial buildings through adaptive flow control. This trend supports digitalization efforts, with over 40% of new installations in smart facilities incorporating these features by 2026.

Miniaturization for Robotics and Medical Devices

- Solenoid actuators are shrinking to micro sizes under 10mm, enabling precise control in medical robotics and diagnostic equipment, with companies like Parker Hannifin achieving 50% size reduction while maintaining 200N force output. This allows integration into minimally invasive surgical tools, where compact solenoids handle fluid dosing with micron-level accuracy. Demand in life sciences has surged 18% annually, driven by aging populations and advanced patient care devices.

- In industrial robotics, miniaturized solenoids from Takaha Kiko support high-speed assembly tasks in electronics manufacturing, reducing actuator weight by 40% and boosting robot agility for tasks like pick-and-place operations. These innovations lower overall system costs by 20% and fit into space-constrained OEM designs. By 2031, this trend is expected to capture 25% of the robotics market share.

- Automotive applications see miniaturized solenoids in electric vehicles for transmission control, with Denso reporting 35% improved response times in body electronics, aiding lightweighting efforts to extend EV range.

Shift to Energy-Efficient Electromechanical Designs

- Designs incorporating advanced magnetic materials like rare-earth alloys reduce power draw by 40%, as seen in Emerson's latest solenoid actuators for HVAC and water treatment, complying with EU energy regulations and cutting operational costs by 25% annually. These actuators achieve 95% efficiency ratings, far surpassing pneumatic alternatives. The trend aligns with global sustainability goals, with 60% of new industrial installations prioritizing low-energy models by 2025.

- In renewable energy utilities, solenoids from Moog are optimized for oil & gas flow control and wind turbine safety systems, using regenerative braking to recover 15% of energy during operation. This supports the electrification wave, with market growth projected at 8% CAGR to 2035. Utilities report 30% lower lifecycle costs with these efficient designs.

- Pneumatic solenoid valves, holding 35% market share in 2023 per Cognitive Market Research, are evolving to hybrid electro-pneumatic versions that slash air consumption by 50%, as implemented by SMC Corporation in material handling systems.

Solenoid Actuator Market Segment Analysis:

Solenoid Actuator Market is Segmented on the basis of By Product Type / Configuration, By Application / End-Use Industry, By Geographic Region

By Product Type / Configuration, Linear Solenoid Actuators segment is expected to dominate the market during the forecast period

- Linear solenoid actuators dominate with over 62% market share due to their widespread use in assembly, packaging, and CNC machinery applications where straightforward linear motion conversion is essential.

- The linear segment's dominance is reinforced by established manufacturing ecosystems, lower production costs, and proven reliability across decades of industrial automation deployment.

By Application / End-Use Industry, Industrial Automation segment is expected to dominate the market during the forecast period

- Industrial automation leads the market at 28% driven by accelerating adoption of Industry 4.0 principles and the integration of solenoids as networked data points within larger smart manufacturing systems.

- The automotive sector follows closely at 26.5% with substantial demand from powertrain systems, transmission control, and new energy vehicle battery-loop valves, particularly in Asia-Pacific where production of NEVs and traditional ICE vehicles creates diverse solenoid requirements.

By Geographic Region, Asia-Pacific segment is expected to dominate the market during the forecast period

- Asia-Pacific commands 45% market share driven by rapid industrialization, infrastructure development, and the concentration of automotive manufacturing in China, India, Thailand, and Vietnam where solenoid demand is colossal.

- China alone produces 31.28 million light vehicles annually plus 12.87 million NEV registrations, creating unprecedented demand for battery-loop valves, proportional expanders, and air-damping actuators that propels regional growth at 8.35% CAGR through 2030.

By Market Maturity / Customer Base, Established Industrial Heartlands (North America, Western Europe, Northeast Asia) segment is expected to dominate the market during the forecast period

- Established industrial regions maintain 55% market share due to their developed manufacturing bases, presence of OEM clusters, and regulatory frameworks that mandate advanced automation and safety-critical solenoid applications in oil & gas, power generation, and chemical processing.

- Developing Asia-Pacific economies demonstrate the most vigorous growth potential, with infrastructure projects and new manufacturing facilities creating incremental demand that is expected to exceed growth rates in mature markets through 2035.

Solenoid Actuator Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the solenoid actuator market due to its established industrial heartlands and high-value consumption, particularly in the U.S., Canada, and Mexico. The region leads in advanced manufacturing and imports significant volumes of actuators to support its robust industrial base. This positions North America as the center of gravity for the global market.

- The region's dominance is driven by a highly developed industrial and automation landscape, including strong demand from oil and gas, power generation, water treatment, and chemical processing sectors. Favorable regulations and infrastructure support widespread integration into automated control systems and safety-critical operations. These factors ensure sustained high consumption and market leadership.

- Major export hubs like the United States serve as key destinations for high-value products, with significant production and import activities. Leading players leverage the U.S. energy sector, which accounts for substantial demand, alongside recent developments in smart automation and energy-efficient systems. Germany and Japan also contribute but North America remains the primary consumer hub.

Active Key Players in the Solenoid Actuator Market:

- LINTEC CO., LTD. (Japan)

- NSF (USA)

- Lesman (USA)

- EMWorks (Canada)

- Magnet-Schultz of America (MSA) (USA)

- Indian Solenoids (India)

- Takano (Japan)

- Kendrion (Germany)

- Asahi (Japan)

- Magnetic Sensor Systems (USA)

- TLX Technologies (USA)

- LOVATO Electric (Italy)

- Process Systems (USA)

- Rotork (UK)

- Emerson Electric Co. (USA)

- Belimo (Switzerland)

- Flowserve (USA)

- SMC Corporation (Japan)

- Festo AG & Co. KG (Germany)

- Other Active Players

|

Solenoid Actuator Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 5.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

0.0 % |

Market Size in 2035: |

USD 5.0 Billion |

|

Segments Covered: |

By Product Type / Configuration |

|

|

|

By Application / End-Use Industry |

|

||

|

By Geographic Region |

|

||

|

By Market Maturity / Customer Base |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Solenoid Actuator Market by Product Type / Configuration (2017-2035)

4.1 Solenoid Actuator Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Linear Solenoid Actuators

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Rotary Solenoid Actuators

4.5 Proportional Solenoid Actuators

4.6 Latching Solenoid Actuators

4.7 Tubular and Flat-Faced Solenoid Actuators

Chapter 5: Solenoid Actuator Market by Application / End-Use Industry (2017-2035)

5.1 Solenoid Actuator Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Industrial Automation

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Automotive & Transportation

5.5 HVAC & Appliances

5.6 Water Treatment & Fluid Control

5.7 Medical & Life Sciences

5.8 Energy & Utilities

Chapter 6: Solenoid Actuator Market by Geographic Region (2017-2035)

6.1 Solenoid Actuator Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Asia-Pacific

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 North America

6.5 Europe

6.6 Middle East & Africa

6.7 Latin America

Chapter 7: Solenoid Actuator Market by Market Maturity / Customer Base (2017-2035)

7.1 Solenoid Actuator Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Established Industrial Heartlands (North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Western Europe

7.5 Northeast Asia)

7.6 Developing High-Growth Economies (Southeast Asia

7.7 Indian Subcontinent)

7.8 Emerging Regional Markets

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Solenoid Actuator Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 LINTEC CO.

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 LTD.

8.4 NSF

8.5 LESMAN

8.6 EMWORKS

8.7 MAGNET-SCHULTZ OF AMERICA (MSA)

8.8 INDIAN SOLENOIDS

8.9 TAKANO

8.10 KENDRION

8.11 ASAHI

8.12 MAGNETIC SENSOR SYSTEMS

8.13 TLX TECHNOLOGIES

8.14 LOVATO ELECTRIC

8.15 PROCESS SYSTEMS

8.16 ROTORK

8.17 EMERSON ELECTRIC CO.

8.18 BELIMO

8.19 FLOWSERVE

8.20 SMC CORPORATION

8.21 FESTO AG & CO. KG

Chapter 9: Global Solenoid Actuator Market By Region

9.1 Overview

9.2. North America Solenoid Actuator Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Solenoid Actuator Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Solenoid Actuator Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Solenoid Actuator Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Solenoid Actuator Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Solenoid Actuator Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Solenoid Actuator Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 5.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

0.0 % |

Market Size in 2035: |

USD 5.0 Billion |

|

Segments Covered: |

By Product Type / Configuration |

|

|

|

By Application / End-Use Industry |

|

||

|

By Geographic Region |

|

||

|

By Market Maturity / Customer Base |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||