Neurovascular Guidewires Market Synopsis:

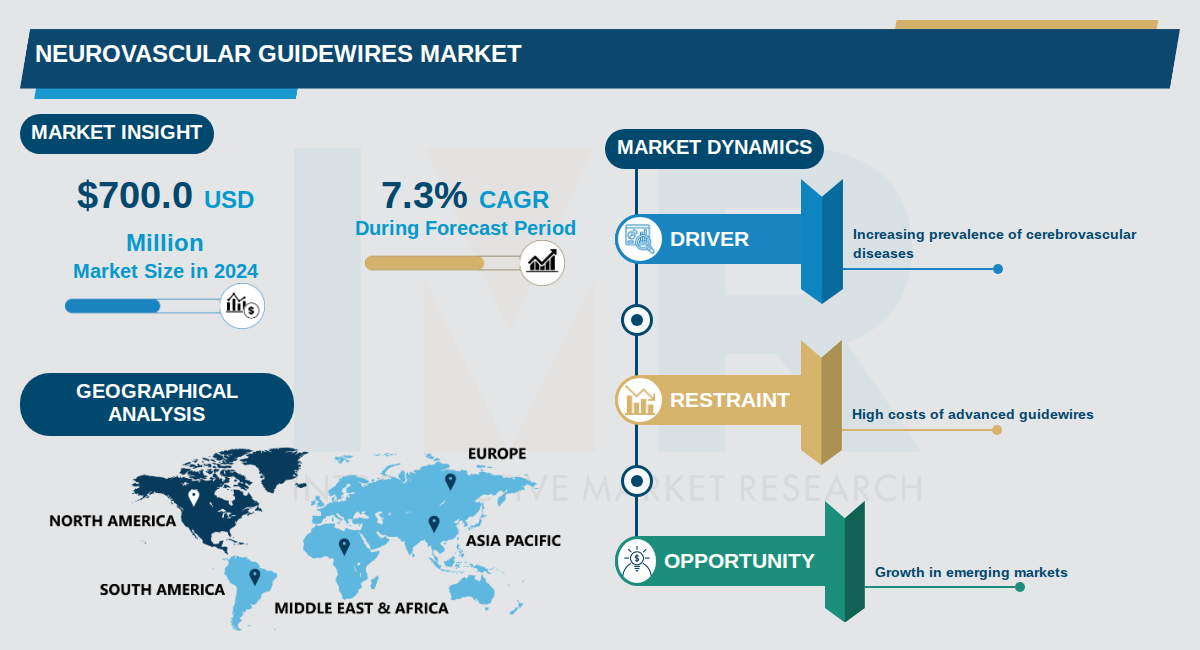

Neurovascular Guidewires Market Size Was Valued at USD 700.0 Million in 2024, and is Projected to Reach USD 1.5 Billion by 2035, Growing at a CAGR of 7.3% From 2024-2035.

The Neurovascular Guidewires Market, valued at approximately $700.0 million in 2024, is projected to reach $1.5 billion by 2035, growing at a compound annual growth rate (CAGR) of 7.3%. This market encompasses specialized medical devices used in minimally invasive neurointerventional procedures to navigate complex cerebral vasculature for treating conditions like strokes, aneurysms, and arteriovenous malformations (AVMs).

Key trends include the dominance of hydrophilic guidewires, expected to capture over 65% market share by 2035 due to their reduced friction and superior navigability in tortuous vessels. North America leads with around 45% share, driven by advanced healthcare infrastructure and high adoption of minimally invasive techniques, while Asia-Pacific emerges as the fastest-growing region owing to rising awareness and healthcare access.

Disparities exist across forecasts, with estimates ranging from $524 million to $2.4 billion by 2035 and CAGRs of 4.1% to 4.9%, reflecting varying assumptions on disorder prevalence and technological adoption. Endovascular surgery remains the largest application segment, bolstered by imaging advancements enabling earlier interventions.

Neurovascular Guidewires Market Trend Analysis:

Shift to Hydrophilic and Advanced Coatings

- Coated guidewires, particularly those with hydrophilic layers, accounted for 63.15% of the vascular guidewires market in 2024 due to improved lubricity in tortuous neurovascular anatomy. Manufacturers like Boston Scientific and Medtronic are investing heavily in PFAS-free coatings to address regulatory scrutiny, filing patents for fluorine-free alternatives that enhance safety and sustainability. This shift reduces friction during insertion, minimizing patient discomfort and procedural complications in endovascular treatments for aneurysms and strokes.

- Non-coated guidewires are growing at a 7.85% CAGR through 2030 as clinicians prioritize tactile feedback in complex cases like chronic total occlusions. Companies such as Terumo are developing hybrid coated models that balance lubrication with direct vessel feel, enabling precise navigation in delicate brain vasculature. These innovations are driving a 4.90% CAGR in the neurovascular guidewires segment overall.

- Advanced coatings improve torque ability and flexibility, with nitinol-based wires leading at 54.85% market share, allowing better performance in minimally invasive neurointerventions.

Rapid Expansion in Asia-Pacific Markets

- Asia-Pacific is the fastest-growing region for neurovascular guidewires, fueled by medical tourism in India and infrastructure expansions in China, contrasting North America's dominant 40.6% share. Procedure volumes are surging due to rising neurovascular disorder incidence, with local players like MicroPort scaling production to meet demand projected at 8.28% CAGR for neurovascular segments.

- Healthcare access improvements and awareness campaigns are boosting endovascular surgeries, with countries like Japan and South Korea adopting high-end guidewires from Stryker and Penumbra. Investments in catheterization labs have increased guidewire utilization by 15-20% annually in urban centers.

- Emerging markets contribute to global growth from USD 3.59 billion in 2024 to USD 6.04 billion by 2035, as reimbursement policies align with minimally invasive preferences.

Rise of Nitinol-Based and Hybrid Material Designs

- Nitinol guidewires hold 54.85% market share in 2024 for their kink resistance and superior tip flexibility, essential for neurovascular tortuosity in stroke and aneurysm treatments. Companies like Abbott and Cook Medical are pioneering nitinol-stainless steel hybrids, enhancing pushability and lesion crossing in calcified vessels.

- These materials enable core-to-tip engineering with high tip load, standardizing use in neurointerventions where vessel navigation is critical. Mordor Intelligence forecasts stainless steel variants growing at 7.62% CAGR, supporting composite cores that reduce multiple wire exchanges.

- Material innovations improve torque response and safety, with supply-chain localization of medical-grade nitinol de-risking production amid global demands.

Neurovascular Guidewires Market Segment Analysis:

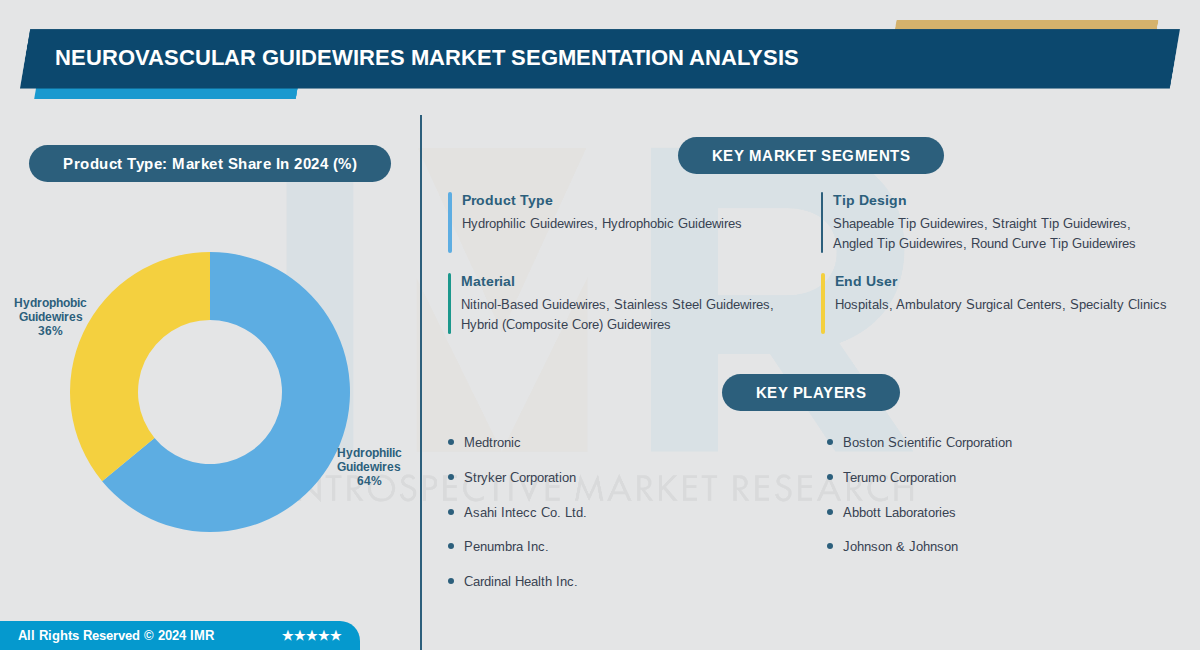

Neurovascular Guidewires Market is Segmented on the basis of By Product Type, By Tip Design, By Material

By Product Type, Hydrophilic Guidewires segment is expected to dominate the market during the forecast period

- Hydrophilic guidewires dominate due to their superior lubricity and ease of navigation through highly tortuous cerebral vasculature.

- They enable enhanced steerability and reduced friction in complex intracranial procedures like thrombectomy and aneurysm coiling.

By Tip Design, Shapeable Tip Guidewires segment is expected to dominate the market during the forecast period

- Shapeable tip guidewires lead due to their versatility in adapting to varied vessel anatomies during neurointerventions.

- They provide precise control and customization, preferred in over 35% of procedures for optimal access to intracranial sites.

By Material, Nitinol-Based Guidewires segment is expected to dominate the market during the forecast period

- Nitinol-based guidewires dominate with their superelastic properties, kink resistance, and shape memory essential for brain vessels.

- They exhibit the fastest growth at over 7.5% CAGR, driven by superior performance in navigating sensitive neurovasculature.

By End User, Hospitals segment is expected to dominate the market during the forecast period

- Hospitals lead due to high procedural volumes in neurointerventional suites and availability of advanced imaging equipment.

- They remain the primary revenue generators for complex emergency cases like strokes and aneurysms.

Neurovascular Guidewires Market Regional Insights:

Neurovascular Guidewires Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the Neurovascular Guidewires Market with over 45% revenue share, primarily led by the United States, followed by Canada and Mexico. This leadership stems from the high prevalence of neurovascular diseases like strokes and aneurysms, coupled with a strong preference for minimally invasive procedures that require precise guidewire navigation. The region's advanced medical ecosystem ensures high adoption rates of these devices.

- The region benefits from superior healthcare infrastructure, including state-of-the-art hospitals and specialized neurointerventional centers, alongside favorable reimbursement policies that encourage procedure volumes. Robust regulatory frameworks by the FDA support rapid innovation and market entry of new guidewire technologies. Significant R&D investments further solidify its position as the market leader.

- Major players such as Medtronic, Stryker, and Terumo maintain strong headquarters and manufacturing presence in the U.S., driving competition and innovation. Recent developments include advancements in hydrophilic coatings and nitinol-based guidewires, with clinical trials and FDA approvals accelerating adoption. Strategic partnerships with hospitals have expanded market penetration in this region.

Active Key Players in the Neurovascular Guidewires Market:

- Medtronic (Ireland)

- Boston Scientific Corporation (USA)

- Stryker Corporation (USA)

- Terumo Corporation (Japan)

- Asahi Intecc Co. Ltd. (Japan)

- Abbott Laboratories (USA)

- Penumbra Inc. (USA)

- Johnson & Johnson (USA)

- Cardinal Health Inc. (USA)

- Cook Medical Inc. (USA)

- B. Braun Melsungen AG (Germany)

- MicroVention (USA)

- MicroPort Scientific Corporation (China)

- Teleflex Incorporated (USA)

- Merit Medical Systems (USA)

- Integer Holdings Corporation (USA)

- AngioDynamics (USA)

- Lepu Medical Technology (China)

- Nipro Corporation (Japan)

- Other Active Players

|

Neurovascular Guidewires Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 700.0 Million |

|

Forecast Period 2024-2035 CAGR: |

7.3 % |

Market Size in 2035: |

USD 1.5 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Tip Design |

|

||

|

By Material |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Neurovascular Guidewires Market by Product Type (2017-2035)

4.1 Neurovascular Guidewires Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Hydrophilic Guidewires

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Hydrophobic Guidewires

Chapter 5: Neurovascular Guidewires Market by Tip Design (2017-2035)

5.1 Neurovascular Guidewires Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Shapeable Tip Guidewires

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Straight Tip Guidewires

5.5 Angled Tip Guidewires

5.6 Round Curve Tip Guidewires

Chapter 6: Neurovascular Guidewires Market by Material (2017-2035)

6.1 Neurovascular Guidewires Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Nitinol-Based Guidewires

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Stainless Steel Guidewires

6.5 Hybrid (Composite Core) Guidewires

Chapter 7: Neurovascular Guidewires Market by End User (2017-2035)

7.1 Neurovascular Guidewires Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Ambulatory Surgical Centers

7.5 Specialty Clinics

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Neurovascular Guidewires Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 MEDTRONIC

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 BOSTON SCIENTIFIC CORPORATION

8.4 STRYKER CORPORATION

8.5 TERUMO CORPORATION

8.6 ASAHI INTECC CO. LTD.

8.7 ABBOTT LABORATORIES

8.8 PENUMBRA INC.

8.9 JOHNSON & JOHNSON

8.10 CARDINAL HEALTH INC.

8.11 COOK MEDICAL INC.

8.12 B. BRAUN MELSUNGEN AG

8.13 MICROVENTION

8.14 MICROPORT SCIENTIFIC CORPORATION

8.15 TELEFLEX INCORPORATED

8.16 MERIT MEDICAL SYSTEMS

8.17 INTEGER HOLDINGS CORPORATION

8.18 ANGIODYNAMICS

8.19 LEPU MEDICAL TECHNOLOGY

8.20 NIPRO CORPORATION

Chapter 9: Global Neurovascular Guidewires Market By Region

9.1 Overview

9.2. North America Neurovascular Guidewires Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Neurovascular Guidewires Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Neurovascular Guidewires Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Neurovascular Guidewires Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Neurovascular Guidewires Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Neurovascular Guidewires Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Neurovascular Guidewires Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 700.0 Million |

|

Forecast Period 2024-2035 CAGR: |

7.3 % |

Market Size in 2035: |

USD 1.5 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Tip Design |

|

||

|

By Material |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||