Metal Packaging Market Synopsis:

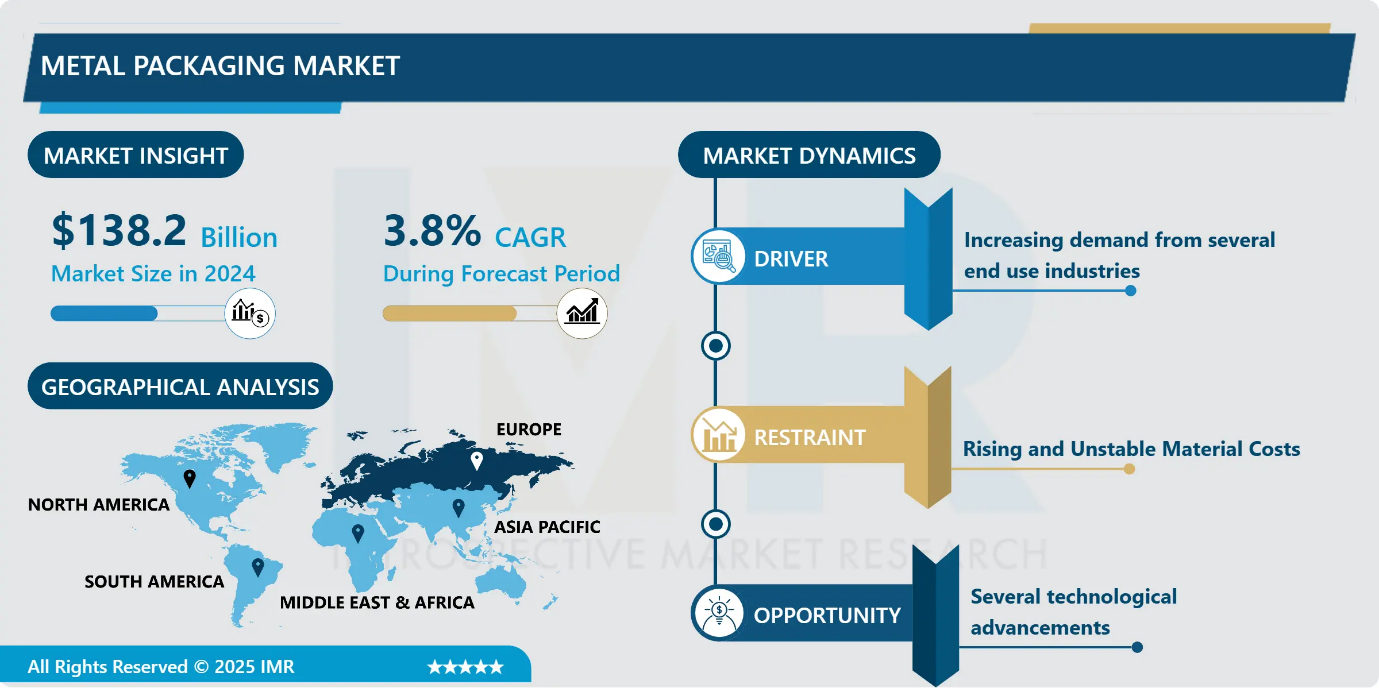

The global metal packaging market size was valued at USD 138.2 billion in 2024 and is projected to reach USD 208.3 billion by 2035, growing at a CAGR of 3.8% from 2025 to 2035.

Metal packaging refers to the use of metal materials, such as aluminium or steel, for the containment and preservation of various products. It offers a durable, versatile, and protective solution for several types of goods, and inherent strength and resistance to external elements for ensuring product integrity during storage, transportation, and handling. Additionally, it is known for its excellent barrier properties, protecting products against moisture, air, light, and other contaminants, thus extending shelf life. As a result, it is essential in preserving product quality, enhancing brand appeal, and minimizing environmental impact in several industries, including food and beverages, pharmaceuticals, cosmetics, and industrial products.

The market is primarily driven by the growing food and beverage (F&B) industry. In addition, the increasing demand for metal packaging solutions for beverages, especially beer, sparkling wines, sodas, iced teas, carbonated soft drinks, energy drinks, and coffee-based refreshments, is influencing the market growth.

Moreover, the introduction of resealable and customizable cans offers enhanced functionality and storage capacities which represents another major growth-inducing factor. Along with this, manufacturers are focusing on creating innovative and visually appealing designs for personal care products to expand their consumer base., thus propelling market growth. Besides this, the growing consumer awareness of the health benefits associated with preserving organic produce in metal-based packaging products is accelerating market growth. Furthermore, the pharmaceutical industry's growing use of aerosol cans, extensive research and development (R&D) activities, and rapid urbanization worldwide are expected to further drive the market's expansion

Metal Packaging Market Growth and Trend Analysis:

Metal Packaging Market Growth Driver - Increasing demand from several end use industries

-

The market is driven by the increasing demand from various end use industries. In addition, the escalating demand in the food and beverage (F&B) industry is augmenting market growth. Also, metal packaging, such as aluminium cans and steel containers, offers excellent protection for food products, preserving their freshness, taste, and nutritional value. Moreover, the widespread adoption of these packaging in the pharmaceutical industry to secure tamper-resistant packaging and maintain the efficacy and safety of drugs represents another major growth-inducing factor.

- Along with this, metal packaging, with its inherent strength and airtight properties, ensures that medications remain protected from external factors that could compromise their quality, thus propelling market growth. Furthermore, it complies with stringent regulatory requirements for pharmaceutical packaging, making it a preferred choice for drug manufacturers, thereby creating a positive market outlook.

Metal Packaging Market Limiting Factor - Rising and Unstable Material Costs

-

Even though metal packaging is great, the cost of materials like aluminium and steel often goes up and down. These price changes make it hard for packaging companies to plan their costs. Sometimes, they have to increase prices, which can drive customers to choose cheaper options like plastic.

- The cost of these metals can rise because of global events, energy costs, or changes in supply. Smaller companies find it especially hard to deal with these price swings, as they don’t have the resources to buy large quantities in advance or handle losses.

- When metal prices go up suddenly, it becomes more expensive to make cans, tins, and containers. This can slow down production and make metal packaging less attractive to cost-focused businesses. Also, companies may be afraid to invest in new metal packaging machines or factories if they don’t know what the material costs will be in the future. So, even though demand is rising, the unpredictable cost of raw materials is a big challenge for the industry

Metal Packaging Market Expansion Opportunity - Several technological advancements

-

Technological advancements have significantly impacted the industry, leading to improved designs, manufacturing processes, and functionalities. These innovations have made packaging more versatile, convenient, and sustainable, further driving its adoption. In addition, engineers have found ways to optimize metal thickness without compromising strength, reducing the weight of metal cans and containers, which lowers production costs, enhances transportation efficiency, and reduces fuel consumption and greenhouse gas (GHG) emissions during distribution, thus influencing the market growth.

- Moreover, the incorporation of smart packaging features such as radio frequency identification (RFID) tags and quick response (QR) codes on packaging allows enhanced supply chain visibility, traceability, and consumer engagement representing another major growth-inducing factor. This technology enables real-time tracking of products, ensuring efficient inventory management and reducing the risk of counterfeiting. Furthermore, advances in surface treatment technologies made metal packaging more resistant to corrosion and abrasion, extending the shelf life of packaged goods and enhancing the visual appeal of the packaging thus propelling the market growth.

Metal Packaging Market Challenge and Risk - Strong Competition from Other Materials

-

Even though metal packaging is useful and eco-friendly, it faces tough competition from other materials like plastic, paper, and glass. These materials are often cheaper or lighter, which makes them more attractive to some companies.

- Plastic is still very popular because it is flexible, lightweight, and often cheaper to produce. Paper and cardboard are also being used more because people think they are natural and biodegradable. New types of packaging, like plant-based plastics, are gaining popularity too.

- In some places, the recycling systems for metal aren’t as good, which makes it harder for people to recycle cans. Also, metal packaging is heavier than some alternatives, which can make shipping more expensive. For companies, cost is a big factor. If metal packaging is more expensive, they may choose a cheaper material to save money even if it’s less eco-friendly. So, while metal packaging has many advantages, it must constantly improve and compete with newer, cheaper, or lighter packaging options.

Metal Packaging Market Segment Analysis:

Metal Packaging Market is segmented based on Type, Application, End-Users, and Region

-

By Type, segment is expected to dominate the market during the forecast period

Cans are widely utilized in the food and beverage industry due to their exceptional protective properties, preserving the quality and freshness of perishable goods. The popularity of canned beverages, including soft drinks and alcoholic beverages, contributes significantly to the market's expansion. Moreover, canned food products offer convenience and longer shelf life, appealing to modern consumers' busy lifestyles which represents another major growth-inducing factor. - Besides this, metal containers are prevalent in the pharmaceutical and industrial sectors, ensuring the safe storage and transportation of various products. Also, aerosol cans find extensive application in the personal care and household segments, providing ease of use and precise dispensing thus propelling the market growth. Furthermore, the rising demand for cans due to their versatility, widespread use, and favourable consumer perception is creating a positive market outlook

By Application, Metal Packaging segment held the largest share in 2024

-

The increasing demand for steel in metal packaging is due to its exceptional strength and durability which is influencing the market growth. Also, steel container cans provide robust protection to numerous products, safeguarding them from physical damage and external elements during handling, transportation, and storage augmenting the market growth.

- Besides this, steel’s ability to preserve the quality and integrity of food, beverages, and pharmaceuticals has led to a surge in demand for steel packaging solutions. Furthermore, advancements in steel manufacturing processes have led to the development of lightweight steel packaging without compromising its strength, which is further accelerating the steel's appeal as a cost-effective and efficient packaging solution. Along with this, the recyclability of steel supports sustainability initiatives, reducing the environmental impact and promoting a circular economy, thus influencing market growth.

Metal Packaging Market Regional Insights:

-

Europe is dominating the market growth due to the well-established and mature packaging industry, which is adopting metal packaging solutions for several products. The European market's preference for metal packaging is driven by its inherent sustainability, recyclability, and eco-friendly attributes, aligning with the region's strong emphasis on environmental concerns and circular economy practices. Besides this, stringent regulations and quality standards imposed by European authorities for packaging materials led to the widespread adoption of metal packaging in industries such as food and beverages, pharmaceuticals, and personal care to ensure product integrity, safety, and hygiene compliance, thus propelling market growth.

Metal Packaging Market Active Players:

- Alltub Group (France)

- Alucon Public Company Limited (Thailand)

- Amcor plc (Australia)

- Ardagh Group S.A. (Luxembourg)

- Ball Corporation (USA)

- CANPACK Group (Poland)

- CCL Containers (Canada)

- CL Smith Company (USA)

- Crown Holdings, Inc. (USA)

- Desjardin SAS (France)

- DS Containers (USA)

- Envases Universales Group (Mexico)

- Greif, Inc. (USA)

- Grupo Zapata (Mexico)

- Hindustan Tin Works Ltd. (India)

- Massilly Group (France)

- Mauser Packaging Solutions (USA)

- Metal Packaging Europe (Belgium)

- Montebello Packaging (Canada)

- Nampak Ltd. (South Africa)

- NCI Packaging (Australia)

- Sarten Ambalaj Sanayive Ticaret A.S. (Turkey)

- Silgan Holdings Inc. (USA)

- Sonoco Products Company (USA)

- Tata Tinplate (TCIL) (India)

- Tecnocap Group (Italy)

- Toyo Seikan Group Holdings, Ltd. (Japan)

- Trivium Packaging (Netherlands)

- TUBEX GmbH (Germany)

- Universal Can Corporation (Japan)

- Other active players

|

Metal Packaging Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 138.2 billion |

|

Forecast Period 2025-35 CAGR: |

3.8% |

Market Size in 2035: |

USD 208.3 billion |

|

Segments Covered: |

By Material |

|

|

|

By Type |

|

||

|

By |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Metal Packaging Market by Product (2018-2035)

4.1 Metal Packaging Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Aluminium

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Steel

Chapter 5: Metal Packaging Market by Application (2018-2035)

5.1 Metal Packaging Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cans

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Bulk Containers

5.5 Shipping Barrels and Drums

5.6 Caps and Closures

Chapter 6: Metal Packaging Market by Distribution Channel (2018-2035)

6.1 Metal Packaging Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Not Applicable

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

Chapter 7: Metal Packaging Market by End User (2018-2035)

7.1 Metal Packaging Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Beverage

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Food

7.5 Cosmetics and Personal Care

7.6 Household

7.7 Paints and Varnishes

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Metal Packaging Market Share by Manufacturer/Service Provider(2024)

8.1.3 Industry BCG Matrix

8.1.4 PArtnerships, Mergers & Acquisitions

8.2 ALLTUB GROUP (FRANCE)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 ALUCON PUBLIC COMPANY LIMITED (THAILAND)

8.4 AMCOR PLC (AUSTRALIA)

8.5 ARDAGH GROUP S.A. (LUXEMBOURG)

8.6 BALL CORPORATION (USA)

8.7 CANPACK GROUP (POLAND)

8.8 CCL CONTAINERS (CANADA)

8.9 CL SMITH COMPANY (USA)

8.10 CROWN HOLDINGS

8.11 INC. (USA)

8.12 DESJARDIN SAS (FRANCE)

8.13 DS CONTAINERS (USA)

8.14 ENVASES UNIVERSALES GROUP (MEXICO)

8.15 GREIF

8.16 INC. (USA)

8.17 GRUPO ZAPATA (MEXICO)

8.18 HINDUSTAN TIN WORKS LTD. (INDIA)

8.19 MASSILLY GROUP (FRANCE)

8.20 MAUSER PACKAGING SOLUTIONS (USA)

8.21 METAL PACKAGING EUROPE (BELGIUM)

8.22 MONTEBELLO PACKAGING (CANADA)

8.23 NAMPAK LTD. (SOUTH AFRICA)

8.24 NCI PACKAGING (AUSTRALIA)

8.25 SARTEN AMBALAJ SANAYIVE TICARET A.S. (TURKEY)

8.26 SILGAN HOLDINGS INC. (USA)

8.27 SONOCO PRODUCTS COMPANY (USA)

8.28 TATA TINPLATE (TCIL) (INDIA)

8.29 TECNOCAP GROUP (ITALY)

8.30 TOYO SEIKAN GROUP HOLDINGS

8.31 LTD. (JAPAN)

8.32 TRIVIUM PACKAGING (NETHERLANDS)

8.33 TUBEX GMBH (GERMANY)

8.34 UNIVERSAL CAN CORPORATION (JAPAN)

8.35 AND OTHER ACTIVE PLAYERS.

Chapter 9: Global Metal Packaging Market By Region

9.1 Overview

9.2. North America Metal Packaging Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.2.4.1 US

9.2.4.2 Canada

9.2.4.3 Mexico

9.3. Eastern Europe Metal Packaging Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.3.4.1 Russia

9.3.4.2 Bulgaria

9.3.4.3 The Czech Republic

9.3.4.4 Hungary

9.3.4.5 Poland

9.3.4.6 Romania

9.3.4.7 Rest of Eastern Europe

9.4. Western Europe Metal Packaging Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.4.4.1 Germany

9.4.4.2 UK

9.4.4.3 France

9.4.4.4 The Netherlands

9.4.4.5 Italy

9.4.4.6 Spain

9.4.4.7 Rest of Western Europe

9.5. Asia Pacific Metal Packaging Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.5.4.1 China

9.5.4.2 India

9.5.4.3 Japan

9.5.4.4 South Korea

9.5.4.5 Malaysia

9.5.4.6 Thailand

9.5.4.7 Vietnam

9.5.4.8 The Philippines

9.5.4.9 Australia

9.5.4.10 New Zealand

9.5.4.11 Rest of APAC

9.6. Middle East & Africa Metal Packaging Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.6.4.1 Turkiye

9.6.4.2 Bahrain

9.6.4.3 Kuwait

9.6.4.4 Saudi Arabia

9.6.4.5 Qatar

9.6.4.6 UAE

9.6.4.7 Israel

9.6.4.8 South Africa

9.7. South America Metal Packaging Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

9.7.4.1 Brazil

9.7.4.2 Argentina

9.7.4.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

Chapter 11 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12 Case Study

Chapter 13 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Metal Packaging Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2024 |

Market Size in 2024: |

USD 138.2 billion |

|

Forecast Period 2025-35 CAGR: |

3.8% |

Market Size in 2035: |

USD 208.3 billion |

|

Segments Covered: |

By Material |

|

|

|

By Type |

|

||

|

By |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||