Commercial Kitchen Appliances Market Synopsis:

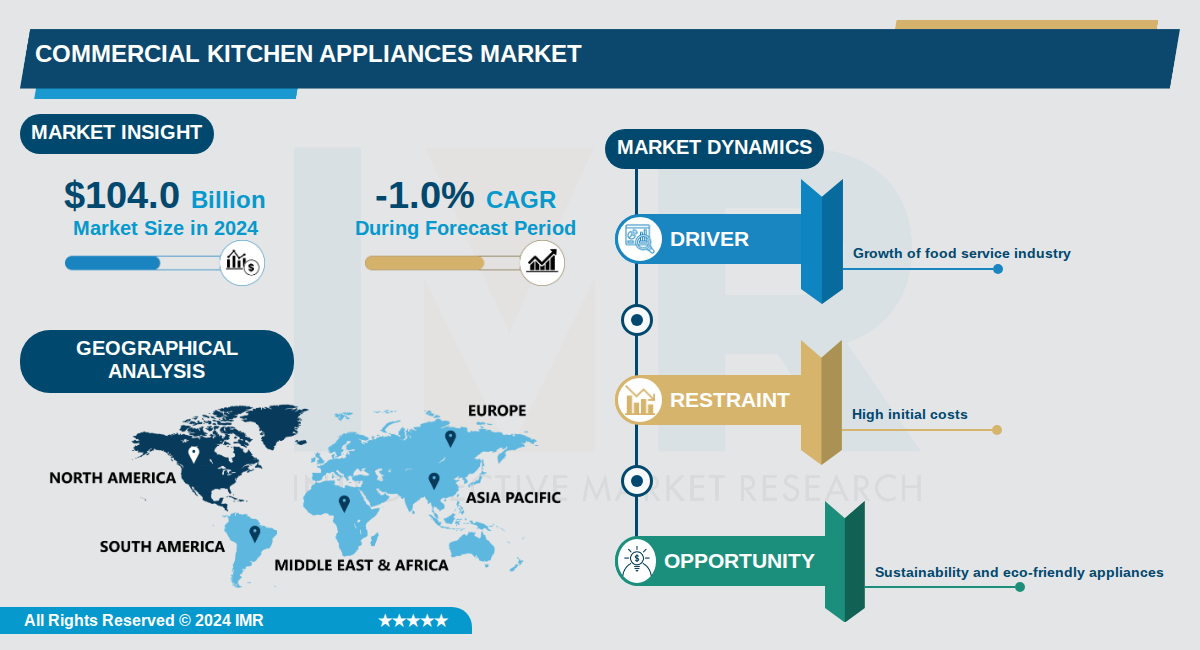

Commercial Kitchen Appliances Market Size Was Valued at USD 104.0 Billion in 2024, and is Projected to Reach USD 94.0 Billion by 2035, Growing at a CAGR of -1.0% From 2024-2035.

Commercial Kitchen Appliances Market Trend Analysis:

Rise of Smart Connected Kitchens

- Smart commercial kitchen equipment is transforming operations with IoT-enabled ovens and fryers from brands like Rational and Electrolux that operators control via mobile apps for remote monitoring and adjustments. Sensors and connected dashboards pull data into unified views for predictive maintenance, reducing downtime by up to 30% as reported in industry case studies from vendors like Hobart. This mainstream adoption addresses labor shortages by automating temperature logs and quality assurance alerts, even after hours.

- AI-powered inventory and waste tracking systems integrated into equipment from companies such as Middleby Corporation optimize stock levels and cut food waste by 20-25% in high-volume restaurants. Programmable induction cooktops with energy tracking, like those from Vulcan, allow precise heat control and real-time usage reports, slashing energy costs by 15% for chains like Chipotle. These features streamline workflows, enabling smaller teams to handle multi-daypart menus efficiently.

- Tech-enhanced kitchens demand compatible support equipment, with New Age Industrial providing custom aluminum fab units that interface seamlessly with robotic prep stations and IoT appliances. Federal regulations like the AIM Act push connected refrigeration using low-GWP R-290 refrigerant in units from True Manufacturing, ensuring compliance while maintaining data logs for FDA Food Code 2022 standards.

Boom in Combi and Speed Ovens

- Combi ovens from Convotherm and Turbochef are surging with a 9% CAGR through 2030, driven by menu agility and higher protein yields that reduce prep time by 40% for restaurants like Panera Bread running multiple dayparts. Self-cleaning combi ovens and steamers automate post-shift maintenance, saving 10-15 labor hours weekly in busy operations. These compact units fit smaller footprints, ideal for ghost kitchens expanding to 25% of the market by 2026.

- High-speed ovens boost throughput with energy-efficient performance, enabling chains like Starbucks to serve diverse menus from breakfast to dinner without expanding kitchen space. Integration with smart controls allows programmable settings for consistent results across locations, cutting energy use by 25% compared to traditional convection models. Market trackers highlight steady expansion as operators prioritize labor relief and speed in fast-casual segments.

Shift to Energy-Efficient Appliances

- Induction cooktops and electric ovens from brands like Wolf and Miele dominate due to 50% lower energy consumption than gas models, aligning with global pushes for eco-friendly tech amid rising carbon emission concerns. The commercial segment holds 69% market share in large cooking appliances, valued at USD 37.92 billion in 2025, fueled by hospitality growth in hotels and resorts requiring scalable efficient units. Government incentives in Europe promote these, with adoption up 18% year-over-year.

- Low-GWP refrigerants like R-290 in commercial units from Traulsen comply with the federal AIM Act's phase-down to 15% of baseline by 2036, reducing environmental impact while maintaining performance in high-traffic kitchens. Programmable appliances with energy tracking help operators like Darden Restaurants cut utility bills by 20%, supporting sustainability goals. Advancements in self-cleaning steamers further minimize water and power use, appealing to chains focused on green certifications.

Commercial Kitchen Appliances Market Segment Analysis:

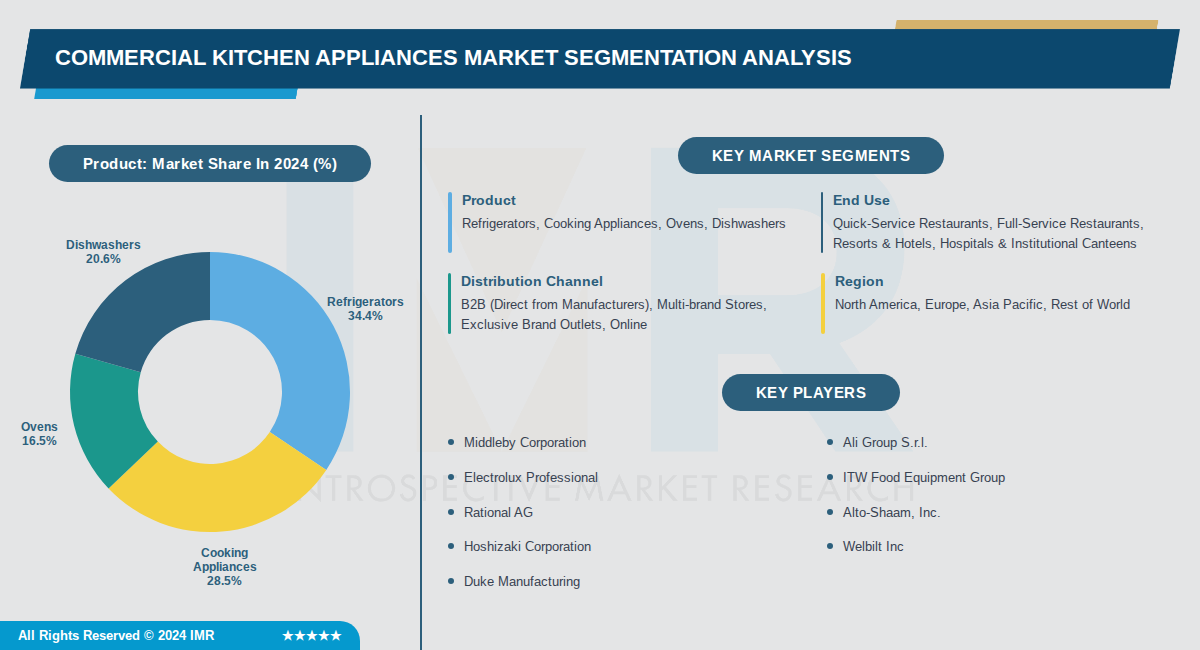

Commercial Kitchen Appliances Market is Segmented on the basis of By Product, By End Use, By Distribution Channel

By Product, Refrigerators segment is expected to dominate the market during the forecast period

- Refrigerators lead due to sustained replacement needs for walk-ins, reach-ins, and undercounter units in longstanding foodservice operations.

- Regulations like US AIM Act HFC limits and EU F-gas updates accelerate transitions to natural-refrigerant systems, driving cold-side replacements.

By End Use, Quick-Service Restaurants segment is expected to dominate the market during the forecast period

- Quick-service restaurants dominate due to increasing home delivery services and adoption of drive-through formats that reduce overhead costs.

- Technological adoption like online ordering and payments boosts throughput-focused equipment demand in QSRs.

By Distribution Channel, B2B (Direct from Manufacturers) segment is expected to dominate the market during the forecast period

- B2B direct sales lead as major foodservice chains and institutions prefer bulk procurement from manufacturers for customized solutions.

- Diversified conglomerates like Middleby and Electrolux maintain strong OEM relationships with global chains through direct channels.

By Region, North America segment is expected to dominate the market during the forecast period

- North America dominates due to high concentration of restaurants, hotels, cafes, and food chains plus rising dining out trends.

- US foodservice establishments contributed USD 1.5 trillion to the economy in 2023, fueling equipment demand.

Commercial Kitchen Appliances Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the commercial kitchen appliances market, primarily led by the United States and Canada, which boast extensive foodservice networks including restaurants, hotels, and institutional kitchens. The region's mature market infrastructure supports high penetration of premium equipment. Mexico contributes through growing hospitality sectors, reinforcing North America's overall leadership.

- Advanced infrastructure, stringent energy-efficiency regulations, and a focus on sustainability drive dominance in North America. The U.S. AIM Act enforces limits on high-GWP refrigerants and mandates leak detection, spurring replacements of refrigeration systems. Robust multi-unit restaurant chains prioritize IoT-enabled and connected appliances for operational efficiency.

- Major players like Middleby Corporation, Electrolux Professional, and Ali Group hold significant shares with innovative offerings tailored to the region. Recent developments include Signature Kitchen Suite's February 2024 launch of AI-powered ovens and dishwashers at KBIS, emphasizing smart technology. These advancements underscore North America's trend toward high-performance, sustainable solutions.

Active Key Players in the Commercial Kitchen Appliances Market:

- Middleby Corporation (USA)

- Ali Group S.r.l. (Italy)

- Electrolux Professional (Sweden)

- ITW Food Equipment Group (USA)

- Rational AG (Germany)

- Alto-Shaam, Inc. (USA)

- Hoshizaki Corporation (Japan)

- Welbilt Inc (USA)

- Duke Manufacturing (USA)

- MKN Maschinenfabrik Kurt Neubauer GmbH & Co. KG (Germany)

- Fagor Professional (Spain)

- Cambro Manufacturing (USA)

- Hatco Corporation (USA)

- True Manufacturing Co., Inc. (USA)

- The Vollrath Company, LLC (USA)

- Henny Penny Corporation (USA)

- Hobart Corporation (USA)

- Garland Group (USA)

- Vulcan (USA)

- Blodgett (USA)

- Other Active Players

|

Commercial Kitchen Appliances Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 104.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

-1.0 % |

Market Size in 2035: |

USD 94.0 Billion |

|

Segments Covered: |

By Product |

|

|

|

By End Use |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Commercial Kitchen Appliances Market by Product (2017-2035)

4.1 Commercial Kitchen Appliances Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Refrigerators

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Cooking Appliances

4.5 Ovens

4.6 Dishwashers

Chapter 5: Commercial Kitchen Appliances Market by End Use (2017-2035)

5.1 Commercial Kitchen Appliances Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Quick-Service Restaurants

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Full-Service Restaurants

5.5 Resorts & Hotels

5.6 Hospitals & Institutional Canteens

Chapter 6: Commercial Kitchen Appliances Market by Distribution Channel (2017-2035)

6.1 Commercial Kitchen Appliances Market Snapshot and Growth Engine

6.2 Market Overview

6.3 B2B (Direct from Manufacturers)

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Multi-brand Stores

6.5 Exclusive Brand Outlets

6.6 Online

Chapter 7: Commercial Kitchen Appliances Market by Region (2017-2035)

7.1 Commercial Kitchen Appliances Market Snapshot and Growth Engine

7.2 Market Overview

7.3 North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Europe

7.5 Asia Pacific

7.6 Rest of World

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Commercial Kitchen Appliances Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 MIDDLEBY CORPORATION

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 ALI GROUP S.R.L.

8.4 ELECTROLUX PROFESSIONAL

8.5 ITW FOOD EQUIPMENT GROUP

8.6 RATIONAL AG

8.7 ALTO-SHAAM

8.8 INC.

8.9 HOSHIZAKI CORPORATION

8.10 WELBILT INC

8.11 DUKE MANUFACTURING

8.12 MKN MASCHINENFABRIK KURT NEUBAUER GMBH & CO. KG

8.13 FAGOR PROFESSIONAL

8.14 CAMBRO MANUFACTURING

8.15 HATCO CORPORATION

8.16 TRUE MANUFACTURING CO.

8.17 INC.

8.18 THE VOLLRATH COMPANY

8.19 LLC

8.20 HENNY PENNY CORPORATION

8.21 HOBART CORPORATION

8.22 GARLAND GROUP

8.23 VULCAN

8.24 BLODGETT

Chapter 9: Global Commercial Kitchen Appliances Market By Region

9.1 Overview

9.2. North America Commercial Kitchen Appliances Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Commercial Kitchen Appliances Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Commercial Kitchen Appliances Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Commercial Kitchen Appliances Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Commercial Kitchen Appliances Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Commercial Kitchen Appliances Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Commercial Kitchen Appliances Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 104.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

-1.0 % |

Market Size in 2035: |

USD 94.0 Billion |

|

Segments Covered: |

By Product |

|

|

|

By End Use |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||