Global Cloud Kitchen Market Overview

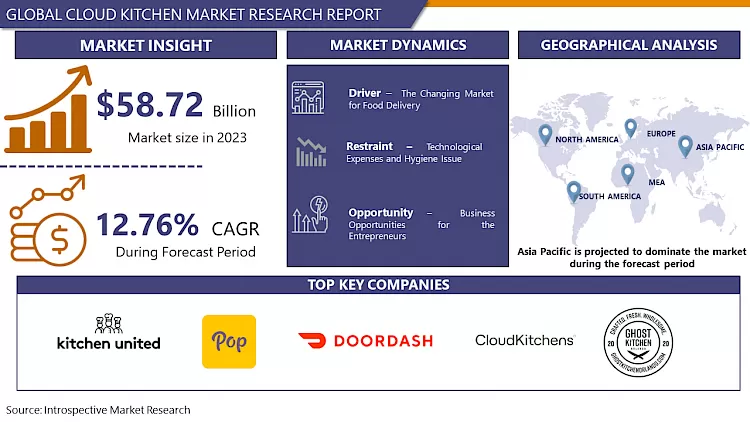

Global Cloud Kitchen Market Size Was Valued at USD 58.72 Billion In 2023 And Is Projected to Reach USD 173.05 Billion By 2032, Growing at A CAGR of 12.76% From 2024 To 2032.

A cloud kitchen is a commercial cooking space that gives restaurants the equipment and assistance they need to make food for takeout and delivery. Unlike traditional brick-and-mortar establishments, cloud kitchens enable the production and delivery of food products with low overhead. Whatever term you give it cloud kitchen, virtual kitchen, shadow kitchen, commissary kitchen, dark kitchen, or ghost kitchen it is fundamentally a place where customers order food mostly online. They can work independently or in the kitchen of a well-known company, although they are usually available online. They go by many names, but they all serve the same purpose: to provide clients with delivery-only meals.

Several terms in the "ghost kitchen" section need to be clarified. For instance, kitchen-as-a-service, often known as dark kitchens, are completely constructed rooms that are hired to concepts for their ghost kitchen responsibilities. Because they offer a full-service kitchen and a delivery concept, it is simple to start a delivery restaurant with little risk and little money. Although there may be a drive-through or takeout area in some ghost kitchens, there isn't a typical storefront or inside seating. No matter what we want to label these digital-only brands, they are significantly addressing a market demand. Additionally, according to recent data, meal delivery orders climbed by more than 150% between 2019 and 2020, and according to UBS, the food delivery market will grow more than 10 times over the next ten years, from $35 billion annually to $365 billion. As the need for food delivery rises, more and more restaurant owners and food entrepreneurs are turning to cloud kitchens as an excellent business solution. The market for cloud kitchens will expand over the forecast period as a result of the rising demand for ordering and meal delivery services.

Market Dynamics And Factors For Cloud Kitchen Market

Drivers:

The Changing Market for Food Delivery

Platforms for online meal delivery are increasing convenience and choice by enabling users to place orders from a variety of eateries with just one swipe on their smartphone. The restaurant meal delivery industry is changing quickly as new internet platforms compete for customers and markets in the Americas, Asia, Europe, and the Middle East. According to McKinsey & Company, although these new Internet platforms are now drawing large investments and having high valuations—five of them are worth more than $1 billion—few actual insights into market dynamics, growth potential, or consumer behavior exist. The market for food delivery is currently valued at USD 83.63 Billion globally, or 1% of the entire food market and 4% of food sold by restaurants and fast-food chains. With an expected five-year growth rate of just 3.5 percent, it has already reached maturity in the majority of countries.

Additionally, the demand for internet meal delivery has increased due to the increase in young people around the world and changing customer tastes. Additionally, a busy lifestyle and an increase in consumer disposable income are key drivers of the cloud kitchen market's expansion. Additionally, it is now simpler to order takeout because of the rise in smartphone usage, increased literacy rates, and easy access to the internet. To enhance their sales and provide meal delivery, businesses are now partnering with online food delivery services like Zomato. Online meal delivery services often provide a variety of promotions, which draw customers and broaden their customer base. As a result, the market for cloud kitchens is growing thanks to effective deals and top-notch customer support.

Restraints:

Technological Expenses and Hygiene Issue

The biggest issue with the cloud kitchen model is that it has substituted technical expenditures and hygiene issues for real estate costs. Technically, cloud kitchens are quite expensive. This is because several different meal delivery applications must interface with these kitchens. The kitchen that is closest to the customer's location must receive the orders and relay them to it. Cloud-based solutions are readily available, enabling restaurants to upgrade their technology without incurring significant upfront costs. The monthly subscriber cost, however, also severely strains the finances of many fledgling cooks. As a result, the prices are relatively comparable to those of conventional restaurants. However, because these stores don't offer a dine-in option, the number of customers is significantly constrained. Scaling the cloud kitchen model is challenging. The issue is that businesses frequently construct their kitchens in unclean settings. To keep costs as low as possible, this is done. Customers don't desire their needs to be met in premium real estate. To ensure that the food is edible, the kitchen must be hygienic. Social media has been used extensively to highlight numerous instances of unclean food being given to diners.

In conclusion, there has been a significant development in the restaurant business. Kitchens in the clouds are a relatively recent invention. However, they assist in filling a very significant market gap that was previously ignored by conventional eateries. They are not eliminating present restaurant owners' market share as a result. Instead, they are growing current markets, which helps the entire sector.

Opportunity:

Business Opportunities for the Entrepreneurs

All industries, including those in education, infrastructure, hospitality, and travel, have been touched by technology. The restaurant industry is similar. Therefore, it's essential to approach every company with a fresh perspective as well as renewed interest. primarily to endure, persist, and compete. The Cloud Kitchen approach has gained popularity among novice restaurateurs since it lowers the expense of launching a culinary brand. Even if the idea was becoming more and more popular even before the pandemic, Cloud Kitchens are now more profitable for two main reasons. First of all, they enable restaurants to send food directly to consumers' homes. Additionally, they use resources more effectively thanks to streamlined kitchen processes because they function in a fraction of the space of a conventional restaurant. For a Cloud Kitchen business to be successful, it is essential to comprehend the unit economics of the collaboration with the delivery apps and the cost of acquiring menu items.

Many business owners now have the chance to operate virtual restaurants using shared commercial kitchen areas on a revenue-sharing basis thanks to the Cloud Kitchen arrangement. Cloud kitchen is experiencing nationwide growth, which has increased competition. In addition to attracting repeat customers by serving high-quality food, technology is the most crucial factor in the restaurant's success.

Segmentation Analysis Of Cloud Kitchen Market

By Type, the independent cloud kitchen segment held the largest revenue share in the forecast period of the overall market. Due to the increase in independent companies that serve customers from a single location, the trend is anticipated to last during the forecast period. Independent cloud kitchens mainly cater to customers who like a certain cuisine style and rely heavily on third-party delivery channels. The growing consumer appetite for fast food, international cuisine, and online ordering is anticipated to fuel the growth of the segment.

By Nature, Throughout the forecast period, the franchised segment produced the highest revenue share and led the worldwide cloud kitchen market. The rapid expansion of online meal delivery services has created enormous development potential for cloud kitchen brands, which has fueled the expansion of the franchised market. This sector has grown as a result of the popular franchises becoming more prevalent, particularly in emerging areas. Additionally, the franchisor extends to the franchisee it's assistance, training, and marketing initiatives, favoring the development of the franchise at several sites and thereby assisting the segment's global expansion. During the forecast period, the standalone is anticipated to grow the fastest. Global demand for standalone cloud kitchens has grown dramatically because of their low cost of entry, increased profitability, and simplicity of use. Additionally, the assistance from the companies that supply food has aided in this market growth.

By Deployment Mode, the Mobile segment is anticipated to capture the maximum market share during the forecast period. Mobile apps are excellent tools for interacting with customers. According to research, offering clients a positive cashless experience increases their likelihood of making a purchase. The transaction becomes more convenient the less cash you exchange. You can simply do that with mobile apps. The ability to take payments from a variety of gateways is a feature of a good restaurant ordering app. The buyer can select the most practical alternative in this way.

Regional Analysis Of Cloud Kitchen Market

The Asia Pacific region has emerged as the dominant force in the global cloud kitchen market, driven by a combination of factors including rapid urbanization, changing consumer lifestyles, and widespread adoption of food delivery apps. Countries like India, China, and Southeast Asian nations have seen a surge in demand for convenient, diverse, and affordable food options, creating a fertile ground for cloud kitchen businesses to thrive.

The COVID-19 pandemic acted as a catalyst, accelerating the growth of cloud kitchens in the region. Lockdowns and social distancing measures led to a significant increase in food delivery orders, prompting both established restaurant chains and new entrepreneurs to invest in cloud kitchen operations. This shift allowed businesses to reduce overhead costs associated with traditional dine-in establishments while expanding their reach to a broader customer base.

The region's tech-savvy population and high smartphone penetration rates have played a crucial role in the success of cloud kitchens. Food delivery platforms like Swiggy, Zomato in India, Meituan in China, and Grab in Southeast Asia have become integral to urban life, providing a ready distribution channel for cloud kitchen brands. These platforms have also invested in their own cloud kitchen spaces, further driving market growth.

Government support and favorable regulations in many Asian countries have contributed to the rapid expansion of the cloud kitchen sector. For instance, Singapore's government has actively encouraged the development of cloud kitchens as part of its food industry transformation map. Similarly, in India, the government's focus on promoting entrepreneurship and digitalization has indirectly benefited the cloud kitchen ecosystem.

Top Key Players Covered In Cloud Kitchen Market

- Dahmakan

- Kitchen United

- DoorDash, Inc.

- Zuul Kitchens, Inc.

- Kitopi Catering Services LLC

- City Storage Systems LLC

- CloudKitchens

- Zomato

- Keatz GmbH

- KITCHEN MANTRA

- Franklin Junction

- Nextbite Brands LLC.

- REEF TECHNOLOGY INC.

- Virturant Brands

- Rebel Foods Private Limited

- Ghost Kitchen Orlando

- Pop Meals

- Swiggy

- Starbucks Corporation and other major players.

Key Industry Development In The Cloud Kitchen Market

- In January 2024, ITC announced plans to expand its cloud kitchen business beyond its pilot phase in Bengaluru. The company, which referred to this venture as "food-tech," identified it as a key growth area. ITC was operating three brands in this space: ITC Aashirvaad Soul Creations for North Indian comfort food, ITC Master Chef Creations for North Indian gourmet cuisines, and ITC Sunfeast Baked Creations for bakery products. The expansion aimed to bring these cloud kitchen services to more cities across India.

- In May 2023, Swiggy expanded its premium food delivery service, Swiggy Gourmet, to 31 cities across India, including Pune, Kolkata, and Jaipur. This move was aimed at strengthening the company's position in the premium food category.

- In March 2022, DoorDash entered into an agreement to acquire Bbot, a technology company specializing in hospitality solutions. This acquisition was intended to enhance DoorDash's offerings in the U.S. market, providing merchants with more comprehensive solutions for both in-store and online channels, including digital ordering and payment systems.

- In July 2021, DoorDash launched a new business initiative by opening a temporary kitchen facility in San Jose, California. This kitchen was set up to prepare meals for six different restaurants, allowing DoorDash to expand its service offerings and explore new operational models.

|

Global Cloud Kitchen Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 58.72 Bn. |

|

Forecast Period 2024-32 CAGR: |

12.76% |

Market Size in 2032: |

USD 173.05 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Nature |

|

||

|

By Deployment Mode |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Cloud Kitchen Market by Type (2018-2032)

4.1 Cloud Kitchen Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Independent

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Shared Kitchen

4.5 Kitchen Pods

Chapter 5: Cloud Kitchen Market by Nature (2018-2032)

5.1 Cloud Kitchen Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Standalone

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Franchised

Chapter 6: Cloud Kitchen Market by Deployment Mode (2018-2032)

6.1 Cloud Kitchen Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Web

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Mobile

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Cloud Kitchen Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 TRIDENT SEAFOODS CORPORATION (USA)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 OCEAN BEAUTY SEAFOODS (USA)

7.4 CLEARWATER SEAFOODS INC. (CANADA)

7.5 SMOKED SALMON PROCESSORS ASSOCIATION (CANADA)

7.6 COOKE AQUACULTURE INC. (CANADA)

7.7 OCEAN WISE (CANADA)

7.8 MOWI ASA (NORWAY)

7.9 LEROY SEAFOOD AS (NORWAY)

7.10 AKVAFARMØY AS (NORWAY)

7.11 MARINE HARVEST ASA (NORWAY)

7.12 GRIEG SEAFOOD ASA (NORWAY)

7.13 SALMAR ASA (NORWAY)

7.14 LEROY SEAFOOD GROUP ASA (NORWAY)

7.15 OCEANIC SALMON LIMITED (NEW ZEALAND)

7.16 ICELAND SEAFOOD INTERNATIONAL HF. (ICELAND)

7.17 BAKKAFROST SEAFOOD GROUP P/F (FAROE ISLANDS)

7.18 SALMON SCOTLAND LTD. (SCOTLAND)

7.19 SCOTTISH SALMON COMPANY LTD. (SCOTLAND)

7.20 AUSTRALIS AQUACULTURE LTD. (CHILE)

7.21 SALMONES CAMANCHACA S.A. (CHILE)

7.22 AQUACHILE S.A. (CHILE)

7.23 MITSUBISHI CORPORATION (JAPAN)

7.24 NICHIREI CORPORATION (JAPAN)

7.25 KINKI OCEAN SALMON COLTD. (JAPAN)

Chapter 8: Global Cloud Kitchen Market By Region

8.1 Overview

8.2. North America Cloud Kitchen Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Independent

8.2.4.2 Shared Kitchen

8.2.4.3 Kitchen Pods

8.2.5 Historic and Forecasted Market Size by Nature

8.2.5.1 Standalone

8.2.5.2 Franchised

8.2.6 Historic and Forecasted Market Size by Deployment Mode

8.2.6.1 Web

8.2.6.2 Mobile

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Cloud Kitchen Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Independent

8.3.4.2 Shared Kitchen

8.3.4.3 Kitchen Pods

8.3.5 Historic and Forecasted Market Size by Nature

8.3.5.1 Standalone

8.3.5.2 Franchised

8.3.6 Historic and Forecasted Market Size by Deployment Mode

8.3.6.1 Web

8.3.6.2 Mobile

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Cloud Kitchen Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Independent

8.4.4.2 Shared Kitchen

8.4.4.3 Kitchen Pods

8.4.5 Historic and Forecasted Market Size by Nature

8.4.5.1 Standalone

8.4.5.2 Franchised

8.4.6 Historic and Forecasted Market Size by Deployment Mode

8.4.6.1 Web

8.4.6.2 Mobile

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Cloud Kitchen Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Independent

8.5.4.2 Shared Kitchen

8.5.4.3 Kitchen Pods

8.5.5 Historic and Forecasted Market Size by Nature

8.5.5.1 Standalone

8.5.5.2 Franchised

8.5.6 Historic and Forecasted Market Size by Deployment Mode

8.5.6.1 Web

8.5.6.2 Mobile

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Cloud Kitchen Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Independent

8.6.4.2 Shared Kitchen

8.6.4.3 Kitchen Pods

8.6.5 Historic and Forecasted Market Size by Nature

8.6.5.1 Standalone

8.6.5.2 Franchised

8.6.6 Historic and Forecasted Market Size by Deployment Mode

8.6.6.1 Web

8.6.6.2 Mobile

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Cloud Kitchen Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Independent

8.7.4.2 Shared Kitchen

8.7.4.3 Kitchen Pods

8.7.5 Historic and Forecasted Market Size by Nature

8.7.5.1 Standalone

8.7.5.2 Franchised

8.7.6 Historic and Forecasted Market Size by Deployment Mode

8.7.6.1 Web

8.7.6.2 Mobile

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Cloud Kitchen Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 58.72 Bn. |

|

Forecast Period 2024-32 CAGR: |

12.76% |

Market Size in 2032: |

USD 173.05 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Nature |

|

||

|

By Deployment Mode |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Cloud Kitchen Market research report is 2024-2032.

Dahmakan, Starbucks Coffee Company, Kitchen United, DoorDash, Inc., Zuul Kitchens, Inc., Kitopi Catering Services LLC, City Storage Systems LLC, CloudKitchens, Zomato, Keatz GmbH, KITCHEN MANTRA., Franklin Junction, Nextbite Brands LLC., REEF TECHNOLOGY INC., Virturant Brands, Rebel Foods Private Limited, Ghost Kitchen Orlando, Pop Meals, Swiggy, Starbucks Corporation, and other major players.

The Cloud Kitchen Market is segmented into Type, Nature, Deployment Mode, and region. By Type, the market is categorized into Independent, Shared Kitchen, and Kitchen Pods. By Nature, the market is categorized into Standalone, Franchised. By Deployment Mode, the market is categorized into Web and Mobile. By region, it is analyzed across North America (U.S.; Canada; Mexico), Europe (Germany; U.K.; France; Italy; Russia; Spain, etc.), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

A cloud kitchen is a commercial cooking space that gives restaurants the equipment and assistance they need to make food for takeout and delivery. Unlike traditional brick-and-mortar establishments, cloud kitchens enable the production and delivery of food products with low overhead.

Global Cloud Kitchen Market Size Was Valued at USD 58.72 Billion In 2023 And Is Projected to Reach USD 173.05 Billion By 2032, Growing at A CAGR of 12.76% From 2024 To 2032.