Automotive Camera Market Synopsis

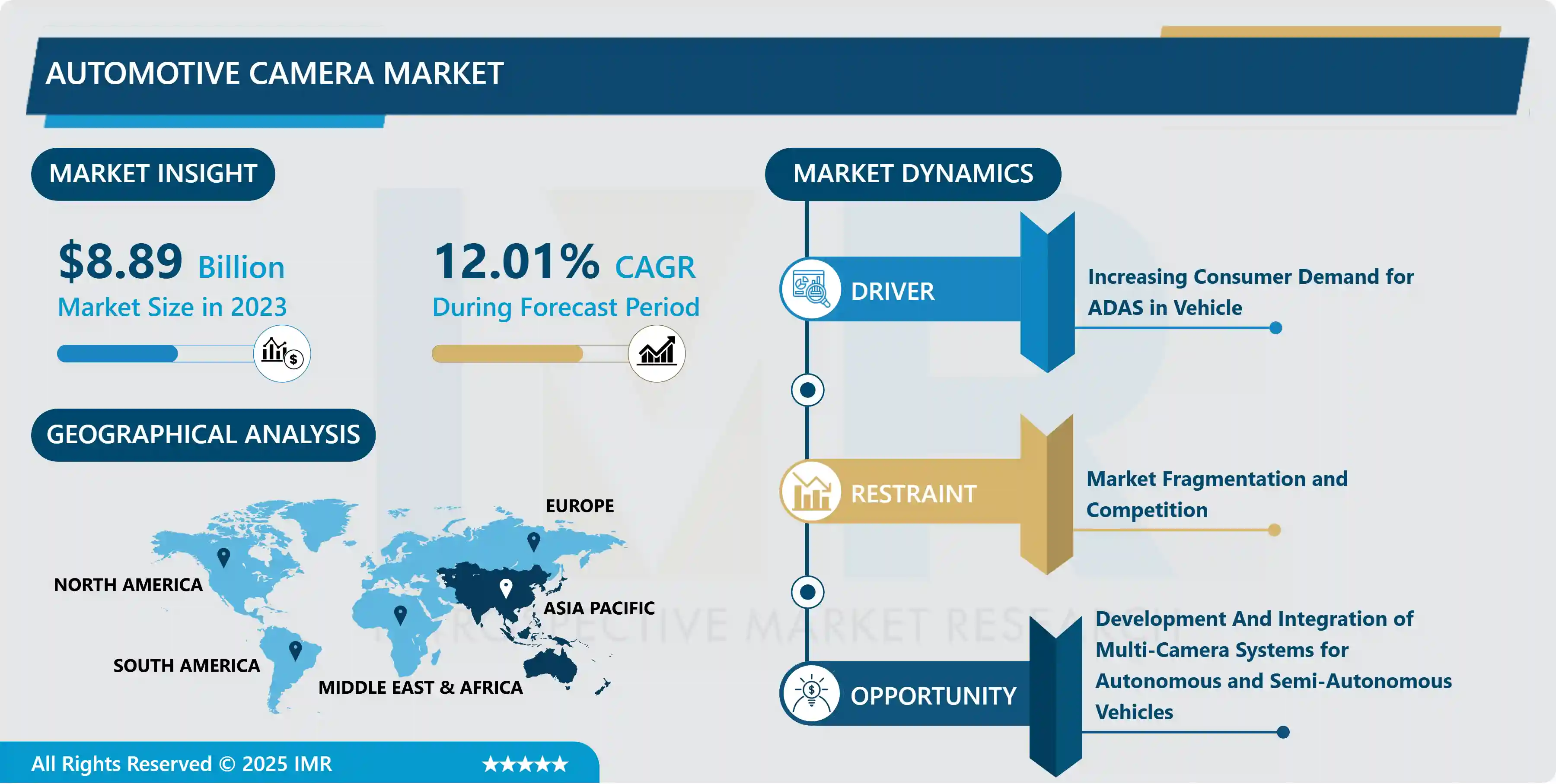

Automotive Camera Market Size Was Valued at USD 8.89 Billion in 2023 and is Projected to Reach USD 24.67 Billion by 2032, Growing at a CAGR of 12.01% From 2024-2032.

Automotive cameras are advanced visual systems integrated into cars to enhance safety, navigation, and driver support. These consist of different types like rearview cameras, front-facing cameras, and surround-view systems, all of which capture live video feeds from different angles around the vehicle. These cameras assist in preventing collisions, warning of lane departures, and aiding in parking by offering drivers thorough visual information. Moreover, they play a crucial role in advanced driver assistance systems (ADAS) and autonomous driving technologies by supplying vital information for understanding the vehicle's environment.

Advanced Driver Assistance Systems (ADAS) are becoming more popular due to a focus on safety, government regulations, and insurance benefits. Consumers and governments around the world prioritize safety, which has resulted in the implementation of standardized ADAS features in new cars. Governments mandate safety features such as rear-view cameras, leading to an increase in the demand for automotive cameras. Insurance companies provide reduced premiums for vehicles equipped with ADAS, thus prompting consumers to opt for cars containing such technology. This general tendency is fueling the expansion of the car camera sector. The advancement of self-driving cars is fuelled by the development of autonomous driving technology, which necessitates the use of advanced sensors like cameras for ensuring safety during operation. Significant corporations are making large investments in the research and development of self-driving technology, causing an increase in the need for top-notch cameras. Incorporating LiDAR and RADAR sensors improves the precision and dependability of autonomous systems. Corporations such as Tesla and Waymo are leading the way in this field, creating more demand for automotive cameras that provide precise and immediate data.

Automotive Camera Market Trend Analysis

Increasing Consumer Demand for ADAS in Vehicle

- Automotive cameras are essential in ADAS systems, improving safety and convenience for drivers with lane departure warning and automatic emergency braking features. These systems depend on camera data to make instant decisions that enhance driver awareness and avoid accidents. Cameras play a crucial role in facilitating self-driving features and ensuring safe navigation in the increasing automated industry.

- The increasing need for automotive cameras is fuelled by manufacturers incorporating sophisticated ADAS capabilities in new cars and customers wanting to enhance their current vehicles. This trend is especially noticeable in developing markets as ADAS technology becomes cheaper. Different kinds of cameras are employed in Advanced Driver Assistance Systems (ADAS). 360-degree view cameras for parking and maneuvering are provided by Surround-View Cameras due to the need for parking assistance requested by consumers.

- Front and Rear-View Cameras play a crucial role in providing collision alerts and enhancing visibility. Night Vision Cameras identify obstructions in dim lighting, improving nighttime driving safety and meeting consumer's safety needs in any driving situation. Consumers are looking for high-resolution cameras to enhance accuracy in ADAS systems. Improved resolution leads to enhanced object detection, classification, and distance estimation, which are essential for safety features. Combining AI and ML algorithms boosts ADAS functionality through enabling immediate image processing and decision-making, resulting in faster and more trustworthy systems.

Opportunity

Development And Integration of Multi-Camera Systems for Autonomous and Semi-Autonomous Vehicles

- Multi-camera systems are essential for giving autonomous and semi-autonomous vehicles complete environmental awareness in a 360-degree range. They assist in identifying barriers, additional cars, people walking, and traffic signs instantly. By cross-verifying and checking information, these systems ensure reliability and redundancy in autonomous driving, enabling safe operation in case of camera failure or inaccurate data.

- Progress in multi-camera technologies for self-driving cars involves improved high-resolution imaging for more accurate object detection, combining with LiDAR and radar sensors for better perception, and utilizing AI and ML algorithms for instantaneous object recognition and decision-making. These technologies play a vital role in ensuring safe navigation and enhancing the vehicle's capacity to make knowledgeable choices in challenging surroundings.

- The partnership between OEMs and technology suppliers is creating fresh market chances for companies in camera technology, sensor fusion, and AI-powered software. Multi-camera systems can be tailored and adjusted for varying degrees of vehicle autonomy, presenting possibilities across a range of vehicle categories. The increase in autonomous driving technology creates an opportunity for aftermarket solutions to add multi-camera systems to current vehicles, generating extra income for companies in the automotive camera industry.

Automotive Camera Market Segment Analysis:

The Automotive Camera market is segmented based on Type, Technology, Vehicle Type, and Application.

By Technology, Digital Camera Segment Is Expected to Dominate the Market During the Forecast Period

- Integration of digital cameras with Artificial Intelligence (AI) and Machine Learning (ML) algorithms enhances functionality through object recognition and driver monitoring. Sensor fusion combines digital cameras with LiDAR, radar, and ultrasonic sensors for improved accuracy. Enhanced connectivity features like vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication facilitate the development of smart transportation systems and fully autonomous vehicles, making use of the digital format for seamless integration.

- Digital cameras provide benefits compared to analog cameras like improved picture quality, instant processing, and versatility in managing data. Digital cameras are important for technologies such as ADAS and autonomous driving due to their high image resolution. Capturing and analyzing images quickly is crucial for ensuring safety features such as lane departure warnings and collision prevention can function effectively. Moreover, digital cameras can gather individual data points, enabling advanced image analysis and integration with other vehicle systems.

- The rise of digital cameras in the market is influenced by factors like greater emphasis on car safety, progress in digital imaging technology, and regulatory backing. The increasing need for car safety features and government regulations are causing digital cameras to be incorporated into vehicles for advanced safety measures. Ongoing advancements in digital imaging technology, such as higher-resolution sensors and enhanced low-light capabilities, are also bolstering the dominance of digital cameras in the market.

By Application, Park Assist Systems Segment Held the Largest Share In 2023

- Park assist systems make parking easier and safer by providing real-time visual guidance and automated assistance, reducing the chances of accidents with obstacles and pedestrians while enhancing driver convenience. In today's market, the increasing desire for high-tech vehicles is pushing the popularity of park assist systems, which include automated parking and 360-degree cameras, as essential features, particularly in crowded city areas with minimal parking options.

- Park assist systems use state-of-the-art technology to maneuver, accelerate, and stop cars automatically while parking. These systems utilize cameras and sensors to assist vehicles in parking with limited driver involvement, enhancing convenience and safety. Connecting with other ADAS functions such as cross-traffic alert and pedestrian detection boosts overall functionality and safety. Advanced imaging and night vision features enhance safety in parking areas by providing clearer images and improved visibility in low-light conditions.

- Market trends like urbanization and parking difficulties, consumer desire for safety and ease, and regulations requiring rear-view cameras in new vehicles are the main factors behind the park assist systems' prevalence in the automotive camera market. The growth of urban areas has heightened the demand for parking solutions in congested areas, as consumers place a premium on safety features. Regulatory requirements have also had a significant impact on the widespread acceptance of park assist systems.

Automotive Camera Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast Period

- The United States, especially in North America, is a major center for automotive technology advancements and creativity. Prominent firms and research organizations in the area prioritize automotive camera technology for advanced driver assistance systems, autonomous driving, and connected vehicles. Partnerships between car manufacturers and technology firms, with the help of Silicon Valley, push forward developments in camera technology through artificial intelligence, machine learning, and sensor fusion.

- The strong manufacturing abilities in the area guarantee that top-notch automotive cameras can be created and manufactured in large quantities. There is a clear indication of high consumer desire for safety and convenience in vehicles in North America. Sophisticated camera systems are the basis for the rising popularity of features such as lane departure warning, adaptive cruise control, blind-spot detection, and parking assistance. The increasing enthusiasm for self-driving vehicles is also fueling the demand for advanced multi-camera systems.

- North America has a strong automotive sector with a significant market and high levels of vehicle ownership. The established automotive sector in the region, spearheaded by the U.S., experiences high sales of cars each year, increasing the need for automotive cameras. There is a significant demand for advanced safety features in current vehicles due to a high rate of vehicle ownership per person. Luxurious and top-of-the-line vehicles, which come with cutting-edge technology, play a significant role in the increasing need for multi-camera systems for ADAS and autonomous driving.

Automotive Camera Market Active Players

- Robert Bosch GmbH (Germany)

- Continental AG (Germany)

- DENSO Corporation (Japan)

- Magna International Inc. (Canada)

- Aptiv PLC (Ireland)

- Valeo S.A. (France)

- ZF Friedrichshafen AG (Germany)

- Nidec Corporation (Japan)

- Panasonic Corporation (Japan)

- OmniVision Technologies, Inc. (USA)

- Sony Semiconductor Solutions Corporation (Japan)

- Autoliv Inc. (Sweden)

- Hitachi Automotive Systems, Ltd. (Japan)

- Hyundai Mobis Co., Ltd. (South Korea)

- Harman International Industries, Inc. (USA)

- Gentex Corporation (USA)

- Ficosa International S.A. (Spain)

- Teledyne FLIR LLC (USA)

- STMicroelectronics N.V. (Switzerland)

- ON Semiconductor Corporation (USA)

- Texas Instruments Incorporated (USA)

- LG Innotek Co., Ltd. (South Korea)

- Ambarella, Inc. (USA)

- Mobileye N.V. (Israel)

- Toshiba Corporation (Japan)

Key Industry Developments in the Automotive Camera Market:

- In May 2024, Continental implemented a cross-domain High-Performance Computer (HPC) in a car, which for the first-time hosts cockpit functions along with additional vehicle functions like driving safety. The technology car serves as a showcase for what the development of Software-defined Vehicles (SDVs) can look like for automotive engineers and utilizes the cloud-based Continental Automotive Edge framework. The implementation was leveraged by Qualcomm Technologies, Inc.’s Snapdragon Ride™ Flex System-on-Chip (SoC) with a pre-integrated Snapdragon Ride Vision perception stack.

- In Jan 2024, ALISO VIEJO, Calif. & BARCELONA, indie Semiconductor, Inc., an Autotech solutions innovator, and Ficosa, a leading global company dedicated to the research, development, production, and marketing of advanced vision, safety and efficiency solutions for the automotive industry, have executed a collaboration agreement to develop and commercialize automotive camera solut

|

Automotive Camera Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2024: |

USD 8.89 Bn. |

|

Forecast Period 2024-32 CAGR: |

12.01 % |

Market Size in 2032: |

USD 24.67 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Technology |

|

||

|

By Vehicle Type |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Automotive Camera Market by Type (2018-2032)

4.1 Automotive Camera Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Front View

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Rear View

4.5 Side View

4.6 Interior View

Chapter 5: Automotive Camera Market by Technology (2018-2032)

5.1 Automotive Camera Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Digital Camera

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Infrared Camera

5.5 Thermal Camera

5.6 LiDAR and RADAR Integrated Cameras

Chapter 6: Automotive Camera Market by Vehicle Type (2018-2032)

6.1 Automotive Camera Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Passenger Cars

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Commercial Vehicles

6.5 Electric Vehicles (EVs)

Chapter 7: Automotive Camera Market by Application (2018-2032)

7.1 Automotive Camera Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Park Assist Systems

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Lane Departure Warning

7.5 Adaptive Cruise Control

7.6 Blind Spot Detection

7.7 Driver Monitoring Systems

7.8 Night Vision Systems

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Automotive Camera Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 ROBERT BOSCH GMBH (GERMANY)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 CONTINENTAL AG (GERMANY)

8.4 DENSO CORPORATION (JAPAN)

8.5 MAGNA INTERNATIONAL INC. (CANADA)

8.6 APTIV PLC (IRELAND)

8.7 VALEO S.A. (FRANCE)

8.8 ZF FRIEDRICHSHAFEN AG (GERMANY)

8.9 NIDEC CORPORATION (JAPAN)

8.10 PANASONIC CORPORATION (JAPAN)

8.11 OMNIVISION TECHNOLOGIES INC. (USA)

8.12 SONY SEMICONDUCTOR SOLUTIONS CORPORATION (JAPAN)

8.13 AUTOLIV INC. (SWEDEN)

8.14 HITACHI AUTOMOTIVE SYSTEMS LTD. (JAPAN)

8.15 HYUNDAI MOBIS COLTD. (SOUTH KOREA)

8.16 HARMAN INTERNATIONAL INDUSTRIES INC. (USA)

8.17 GENTEX CORPORATION (USA)

8.18 FICOSA INTERNATIONAL S.A. (SPAIN)

8.19 TELEDYNE FLIR LLC (USA)

8.20 STMICROELECTRONICS N.V. (SWITZERLAND)

8.21 ON SEMICONDUCTOR CORPORATION (USA)

8.22 TEXAS INSTRUMENTS INCORPORATED (USA)

8.23 LG INNOTEK COLTD. (SOUTH KOREA)

8.24 AMBARELLA INC. (USA)

8.25 MOBILEYE N.V. (ISRAEL)

8.26 TOSHIBA CORPORATION (JAPAN)

Chapter 9: Global Automotive Camera Market By Region

9.1 Overview

9.2. North America Automotive Camera Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Type

9.2.4.1 Front View

9.2.4.2 Rear View

9.2.4.3 Side View

9.2.4.4 Interior View

9.2.5 Historic and Forecasted Market Size by Technology

9.2.5.1 Digital Camera

9.2.5.2 Infrared Camera

9.2.5.3 Thermal Camera

9.2.5.4 LiDAR and RADAR Integrated Cameras

9.2.6 Historic and Forecasted Market Size by Vehicle Type

9.2.6.1 Passenger Cars

9.2.6.2 Commercial Vehicles

9.2.6.3 Electric Vehicles (EVs)

9.2.7 Historic and Forecasted Market Size by Application

9.2.7.1 Park Assist Systems

9.2.7.2 Lane Departure Warning

9.2.7.3 Adaptive Cruise Control

9.2.7.4 Blind Spot Detection

9.2.7.5 Driver Monitoring Systems

9.2.7.6 Night Vision Systems

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Automotive Camera Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Type

9.3.4.1 Front View

9.3.4.2 Rear View

9.3.4.3 Side View

9.3.4.4 Interior View

9.3.5 Historic and Forecasted Market Size by Technology

9.3.5.1 Digital Camera

9.3.5.2 Infrared Camera

9.3.5.3 Thermal Camera

9.3.5.4 LiDAR and RADAR Integrated Cameras

9.3.6 Historic and Forecasted Market Size by Vehicle Type

9.3.6.1 Passenger Cars

9.3.6.2 Commercial Vehicles

9.3.6.3 Electric Vehicles (EVs)

9.3.7 Historic and Forecasted Market Size by Application

9.3.7.1 Park Assist Systems

9.3.7.2 Lane Departure Warning

9.3.7.3 Adaptive Cruise Control

9.3.7.4 Blind Spot Detection

9.3.7.5 Driver Monitoring Systems

9.3.7.6 Night Vision Systems

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Automotive Camera Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Type

9.4.4.1 Front View

9.4.4.2 Rear View

9.4.4.3 Side View

9.4.4.4 Interior View

9.4.5 Historic and Forecasted Market Size by Technology

9.4.5.1 Digital Camera

9.4.5.2 Infrared Camera

9.4.5.3 Thermal Camera

9.4.5.4 LiDAR and RADAR Integrated Cameras

9.4.6 Historic and Forecasted Market Size by Vehicle Type

9.4.6.1 Passenger Cars

9.4.6.2 Commercial Vehicles

9.4.6.3 Electric Vehicles (EVs)

9.4.7 Historic and Forecasted Market Size by Application

9.4.7.1 Park Assist Systems

9.4.7.2 Lane Departure Warning

9.4.7.3 Adaptive Cruise Control

9.4.7.4 Blind Spot Detection

9.4.7.5 Driver Monitoring Systems

9.4.7.6 Night Vision Systems

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Automotive Camera Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Type

9.5.4.1 Front View

9.5.4.2 Rear View

9.5.4.3 Side View

9.5.4.4 Interior View

9.5.5 Historic and Forecasted Market Size by Technology

9.5.5.1 Digital Camera

9.5.5.2 Infrared Camera

9.5.5.3 Thermal Camera

9.5.5.4 LiDAR and RADAR Integrated Cameras

9.5.6 Historic and Forecasted Market Size by Vehicle Type

9.5.6.1 Passenger Cars

9.5.6.2 Commercial Vehicles

9.5.6.3 Electric Vehicles (EVs)

9.5.7 Historic and Forecasted Market Size by Application

9.5.7.1 Park Assist Systems

9.5.7.2 Lane Departure Warning

9.5.7.3 Adaptive Cruise Control

9.5.7.4 Blind Spot Detection

9.5.7.5 Driver Monitoring Systems

9.5.7.6 Night Vision Systems

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Automotive Camera Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Type

9.6.4.1 Front View

9.6.4.2 Rear View

9.6.4.3 Side View

9.6.4.4 Interior View

9.6.5 Historic and Forecasted Market Size by Technology

9.6.5.1 Digital Camera

9.6.5.2 Infrared Camera

9.6.5.3 Thermal Camera

9.6.5.4 LiDAR and RADAR Integrated Cameras

9.6.6 Historic and Forecasted Market Size by Vehicle Type

9.6.6.1 Passenger Cars

9.6.6.2 Commercial Vehicles

9.6.6.3 Electric Vehicles (EVs)

9.6.7 Historic and Forecasted Market Size by Application

9.6.7.1 Park Assist Systems

9.6.7.2 Lane Departure Warning

9.6.7.3 Adaptive Cruise Control

9.6.7.4 Blind Spot Detection

9.6.7.5 Driver Monitoring Systems

9.6.7.6 Night Vision Systems

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Automotive Camera Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Type

9.7.4.1 Front View

9.7.4.2 Rear View

9.7.4.3 Side View

9.7.4.4 Interior View

9.7.5 Historic and Forecasted Market Size by Technology

9.7.5.1 Digital Camera

9.7.5.2 Infrared Camera

9.7.5.3 Thermal Camera

9.7.5.4 LiDAR and RADAR Integrated Cameras

9.7.6 Historic and Forecasted Market Size by Vehicle Type

9.7.6.1 Passenger Cars

9.7.6.2 Commercial Vehicles

9.7.6.3 Electric Vehicles (EVs)

9.7.7 Historic and Forecasted Market Size by Application

9.7.7.1 Park Assist Systems

9.7.7.2 Lane Departure Warning

9.7.7.3 Adaptive Cruise Control

9.7.7.4 Blind Spot Detection

9.7.7.5 Driver Monitoring Systems

9.7.7.6 Night Vision Systems

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Automotive Camera Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2024: |

USD 8.89 Bn. |

|

Forecast Period 2024-32 CAGR: |

12.01 % |

Market Size in 2032: |

USD 24.67 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Technology |

|

||

|

By Vehicle Type |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||