H2S Adsorbent Market Synopsis:

H2S Adsorbent Market Size Was Valued at USD 1.4 Billion in 2024, and is Projected to Reach USD 2.1 Billion by 2035, Growing at a CAGR of 3.8% From 2024-2035.

The H2S Adsorbent Market, valued at $1.4 billion in 2024, is projected to reach $2.1 billion by 2035, growing at a CAGR of 3.8%. This market focuses on materials used to remove hydrogen sulfide (H2S), a toxic gas prevalent in oil and gas operations, through adsorption processes. Key segments include regenerative and non-regenerative types, with applications spanning upstream production, midstream processing, and downstream refining.

The oil and gas sector dominates, accounting for the majority of demand, particularly in upstream activities where H2S removal is critical for safety, environmental compliance, and meeting pipeline specifications. North America and the Middle East lead current market share due to extensive hydrocarbon production, while Asia-Pacific emerges as the fastest-growing region driven by industrialization and energy infrastructure investments.

Major players such as Schlumberger, Halliburton, BASF, and Dow drive innovation in adsorbent technologies, enhancing efficiency and lifespan. The market benefits from steady demand amid global energy needs, though varying regional growth rates reflect differences in regulatory environments and industrial expansion.

H2S Adsorbent Market Trend Analysis:

Shift to Sustainable Adsorbent Materials

- Manufacturers like BASF and Clariant are increasingly adopting renewable, biodegradable, and non-toxic adsorbents such as bio-based activated carbons and natural zeolites derived from agricultural waste to minimize environmental impact. These materials reduce dependence on fossil fuels while offering superior H2S adsorption capacity and selectivity compared to traditional options. This shift aligns with global sustainability goals, with the H2S Adsorbent Market projected to grow from USD 1,398.98 million in 2023 to USD 2,082.39 million by 2031 at a CAGR of 5.14%.

- In the Asia Pacific region, which held 37.64% market share in 2023 valued at USD 526.54 million, companies are prioritizing these green materials amid rapid industrialization and environmental regulations in China and India. For instance, natural zeolites are gaining traction for their cost-effectiveness and eco-friendly profile in natural gas processing. This trend is expected to drive the highest regional CAGR of 6.03% through 2031.

- The renewable energy sector, including biogas production projected to reach 42.37 billion cubic meters by 2027, is accelerating demand for these sustainable adsorbents to remove H2S from biomethane, enabling cleaner fuel alternatives.

Rise of Regenerative H2S Adsorbents

- Regenerative adsorbents are dominating over non-regenerative types due to economic incentives and sustainability, with companies like SLB and Halliburton investing in reusable materials that last several years, slashing operational costs in large-scale operations. These adsorbents can be regenerated multiple times, reducing waste and environmental footprint while handling high H2S volumes in oil refining and gas processing. The oil industry segment, which leads market share, benefits most from this trend amid crude oil production challenges.

- In North America, particularly the US and Canada, regenerative technologies are critical for shale gas operations with high H2S concentrations, supported by stringent safety regulations. Leading firms like BASF and Dow are advancing these for extended lifespan and lower lifecycle costs, positioning the region as a top consumer through 2033.

Development of Advanced Nanomaterials

- Research by companies such as Johnson Matthey and Axens focuses on novel nanomaterials that enhance H2S adsorption capacity, selectivity, and durability, addressing demands in oil and gas where the sector accounts for the majority of market demand. These innovations improve efficiency in complex environments like wastewater treatment and gas processing, with the global H2S Adsorption Technology market projected at USD 2.5 billion in 2025 growing to USD 4.5 billion by 2033 at 7% CAGR.

- Nanomaterials enable integrated solutions combining H2S removal with multi-pollutant treatment, particularly in industries like pulp and paper and chemicals, where firms like ExxonMobil are deploying them for cost-effective operations. This trend supports broader applications beyond energy, mitigating odor and corrosion issues.

- Strategic M&A activity, including consolidations by SLB and GE, is accelerating nanomaterial adoption to expand technology portfolios, with market value potentially reaching hundreds of millions annually by the forecast period.

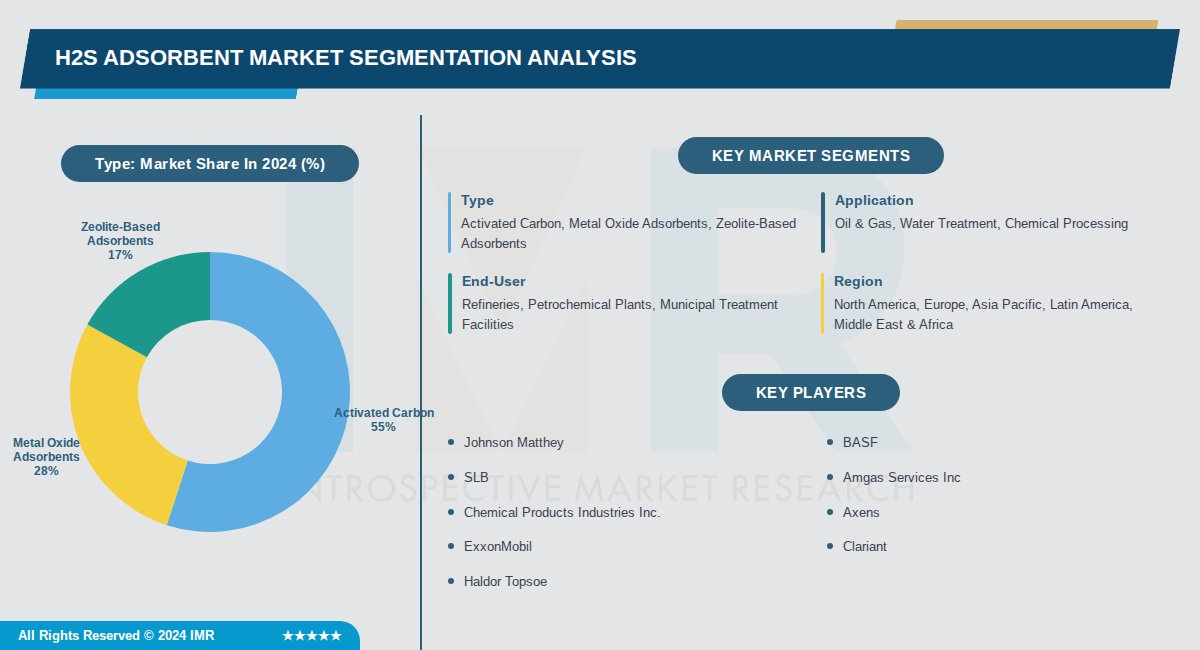

H2S Adsorbent Market Segment Analysis:

H2S Adsorbent Market is Segmented on the basis of By Type, By Application, By End-User

By Type, Activated Carbon segment is expected to dominate the market during the forecast period

- Activated carbon dominates due to its versatile adsorption capabilities, cost-effectiveness, and wide availability for various industrial applications including gas sweetening and odor control.

- It accounts for the largest market share as the most established technology, with coal-based and impregnated variants widely used in oil & gas and water treatment sectors.

By Application, Oil & Gas segment is expected to dominate the market during the forecast period

- Oil & gas leads due to extensive hydrocarbon processing needs, particularly gas sweetening and refinery operations handling high sulfur crude and natural gas.

- It represents over 50% of market revenue driven by global production increases in shale gas and oil sands requiring H2S removal for safety and compliance.

By End-User, Refineries segment is expected to dominate the market during the forecast period

- Refineries dominate as primary end-users for crude oil processing, product finishing, and off-gas treatment to meet stringent emission standards.

- Sustained demand stems from regulatory requirements and high H2S concentrations in global crude oil supplies processed at these facilities.

By Region, North America segment is expected to dominate the market during the forecast period

- North America leads due to extensive shale gas and oil sands development, coupled with strict EPA and OSHA regulations on H2S emissions.

- It holds the largest share from substantial natural gas production with elevated H2S levels necessitating specialized adsorbents.

H2S Adsorbent Market Regional Insights:

Asia Pacific Dominates the H2S Adsorbent Market with the Largest Share

- Asia Pacific holds the largest market share of 37.64% in 2023, valued at USD 526.54 Million, making it the dominant region globally. Key countries like China, India, and Japan drive this leadership through their massive industrial bases and high demand for H2S removal in oil & gas, refining, and chemical sectors. This region outpaces others due to its sheer scale and rapid economic expansion.

- Rapid industrialization, urbanization, and growing environmental concerns fuel demand, supported by government initiatives to curb sulfur emissions. Technological advancements in adsorbent efficiency align with strict regulations in countries like China, enhancing adoption in wastewater treatment and biogas purification. Infrastructure investments in energy projects further solidify the region's market position.

- Major economies such as China play a pivotal role, with heavy investments in industrial and renewable energy infrastructure boosting adsorbent use. Leading players focus on Asia Pacific for expansion due to high growth potential, including developments in high-capacity H2S removal technologies tailored for local refineries and gas processing plants.

Active Key Players in the H2S Adsorbent Market:

- Johnson Matthey (UK)

- BASF (Germany)

- SLB (USA)

- Amgas Services Inc (USA)

- Chemical Products Industries Inc. (USA)

- Axens (France)

- ExxonMobil (USA)

- Clariant (Switzerland)

- Haldor Topsoe (Denmark)

- Sinopec (China)

- SJ Environmental Corporation (USA)

- Dorf Ketal Chemicals (India)

- Halliburton (USA)

- Dow (USA)

- Akzonobel (Netherlands)

- Huntsman (USA)

- Ineos (UK)

- NALCO Water (USA)

- CNPC (China)

- Other Active Players

|

H2S Adsorbent Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.4 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.8 % |

Market Size in 2035: |

USD 2.1 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: H2S Adsorbent Market by Type (2017-2035)

4.1 H2S Adsorbent Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Activated Carbon

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Metal Oxide Adsorbents

4.5 Zeolite-Based Adsorbents

Chapter 5: H2S Adsorbent Market by Application (2017-2035)

5.1 H2S Adsorbent Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Oil & Gas

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Water Treatment

5.5 Chemical Processing

Chapter 6: H2S Adsorbent Market by End-User (2017-2035)

6.1 H2S Adsorbent Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Refineries

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Petrochemical Plants

6.5 Municipal Treatment Facilities

Chapter 7: H2S Adsorbent Market by Region (2017-2035)

7.1 H2S Adsorbent Market Snapshot and Growth Engine

7.2 Market Overview

7.3 North America

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Europe

7.5 Asia Pacific

7.6 Latin America

7.7 Middle East & Africa

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 H2S Adsorbent Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 JOHNSON MATTHEY

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 BASF

8.4 SLB

8.5 AMGAS SERVICES INC

8.6 CHEMICAL PRODUCTS INDUSTRIES INC.

8.7 AXENS

8.8 EXXONMOBIL

8.9 CLARIANT

8.10 HALDOR TOPSOE

8.11 SINOPEC

8.12 SJ ENVIRONMENTAL CORPORATION

8.13 DORF KETAL CHEMICALS

8.14 HALLIBURTON

8.15 DOW

8.16 AKZONOBEL

8.17 HUNTSMAN

8.18 INEOS

8.19 NALCO WATER

8.20 CNPC

Chapter 9: Global H2S Adsorbent Market By Region

9.1 Overview

9.2. North America H2S Adsorbent Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe H2S Adsorbent Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe H2S Adsorbent Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific H2S Adsorbent Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa H2S Adsorbent Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America H2S Adsorbent Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

H2S Adsorbent Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 1.4 Billion |

|

Forecast Period 2024-2035 CAGR: |

3.8 % |

Market Size in 2035: |

USD 2.1 Billion |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||