3D Glass Market Synopsis

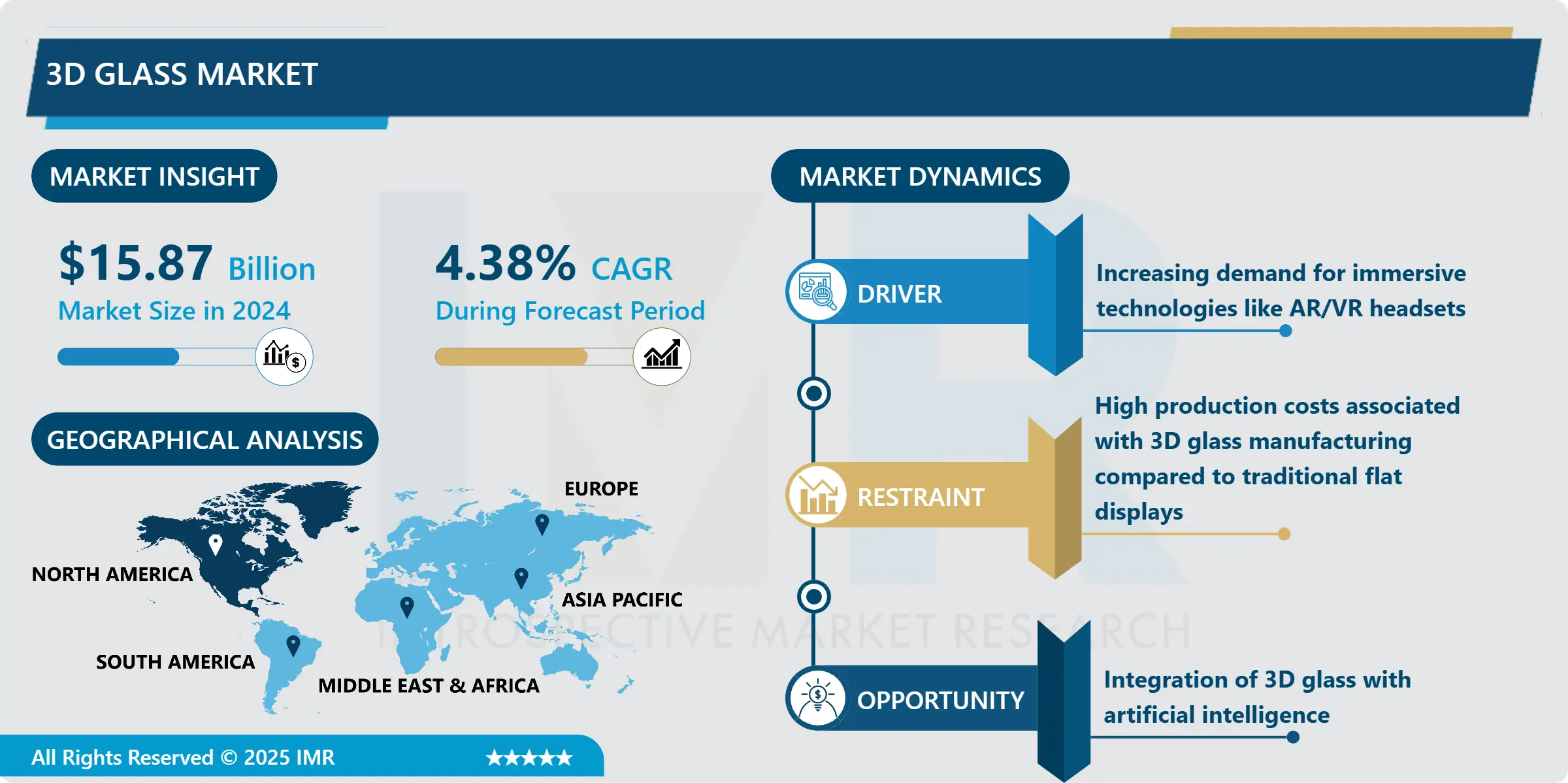

3D Glass Market Size Was Valued at USD 15.87 Billion in 2024, and is Projected to Reach USD 25.43 Billion by 2035, Growing at a CAGR of 4.38% From 2025-2035.

3D glass also known as three-dimensional glass is a kind of glass material which is manufactured normally for 3D viewing. This is done by designing a surface for which interaction with light can make an object look three-dimensional and create an overall depth and volume. 3D glass can be applied in multiple ways such as: in electronics industries, building structures, automobile industries, and virtual reality gadgets.

In consumer electronics, the most popular application of 3D glass is portable electronic devices such as smart phone, tablet, wearable devices and the like. The curves on the edges and the thin form of the 3D glass give the gadgets the aesthetic and comfortable feeling. The material is usually toughened with the extra characteristic of having enhanced scratch resistance; it goes through processes like ion exchange that enhances its strength. Also, 3D glass can incorporate enhanced display solutions, and it enables image sharpness and richer colors, which is useful in high definition applications.

In construction, 3D glass is applied in the construction of attractive, contemporary architecture with uniqueness in design. At the same time, the fact that this material can be given a wide variety of forms may open up new opportunities for architects when choosing the design of the building’s external and internal walls. Today, in automotive industries, 3D glass is applied in the manufacturing of car’s dashboards, infotainment systems, and heads up display systems. It blends seamlessly with applications in these areas as it gives users a better graphical interface while at the same time giving a touch of futurism to interior of the vehicle.

The use of 3D glass in VR and AR devices is worthy of special attention. VR mainly depends on 3D glass lenses because without them there will be no clearly focused visible digital artificial environment. The reason for these is to reduce eye strain and to provide the required depth in order to enable a virtual reality experience. Among the components of AR devices, 3D glass enables placing digital information directly onto the observed physical environment, thus increasing the technology’s usability and interactivity.

There are definitely brighter prospects for 3D glass technology, especially considering that the innovations in the manufacturing sector and material science are being made on-going constantly. Specifically, scientists are carrying out studies with a view of achieving the following improvements on 3D glass; increased strength in addition to reduced weight which are factors that have the potential of extending its usefulness.

Others in the pipeline are flexible 3D glass and smart glass, Glass which has properties that may be altered by an external influence such as light or heat. It could open up new applications in areas such as healthcare where the smart 3D glass could be applied on medical instruments or in renewable energy where the smart material could enhance the functionality of solar panels.

3D Glass Market Trend Analysis

Growing adoption of 3D glass in automotive applications

- The use of 3D glass in cars is expanding rapidly and this is largely defining the 3D glass market. This trend is as a result of the market pull where the society seemed to demand better designed vehicle interior and exterior. Currently, car makers have employed the 3D glass in the production of touch screens, the dashboard as well as the body of automobiles, incorporating it as part of the vehicle’s design to provide a sleek look and to satisfy the consumer’s needs. Modern automobile designs are inclined towards structures incorporated with curved designs, and since 3D glass can be manufactured in a variety of styles, it is considered an ideal option for the automobile industry.

- Other than the said aesthetic uses, 3D glass also has several functional uses in cars for instance. Because it is rugged and hard wearing, it is useful where there will be heavy usage such as screens and buttons including touch screens and control panels. Additionally, 3D glass is versatile to support Heads-Up-Display (HUD), the Augmented Reality (AR) interface, and Advanced Driver Assistance System (ADAS), enhancing safety and utility of automobiles. In addition to this, 3D glass possess even higher temperature resistance and it boasts of even higher light transmission than regular glass making it perfect for use in automobiles.

- The 3D glass used in automotive production is likely to gain strong growth as automobile companies continuing to advance and attempt to incorporate as many technologies as they can into their automobiles. This trend is possible due to the developments in the areas of glass manufacturing technologies, which make 3D glass more affordable by expanding application to luxury and even mid and economy car segments. This trend is well demonstrated in the automobile industry where customers are willing to purchase vehicles that are stained with ICT features, classy, and safe against accidents…Hence, the integral and more practical application of 3D glass, the automotive industry is set to fuel the enhancements of 3D glass market in the near future.

Expanding applications of 3D glass beyond consumer electronics

- The market that depends solely on consumer electronics products like smartphones, tablets, wearables, etc 3D glass is a highly promising market with an incredibly high potential in various other fields. The first promising field that can be mentioned is automotive. Through the adoption of the 3D glass in car’s information management panels, inner panels and the head up displays, what is gotten is high elongation, stunning looks and an impressively improved sensitivity to touch. This can enhance the interaction, and safety of the users which conforms with the trend of integrating sophisticated technologies in vehicles. All the same, 3D glass can also be applied in external auto parts to give the car a classy and modern outlook and at the same time, is very strong and can withstand harsh environmental climates.

- Besides automotive utilization, architecture is another massive prospect for the 3D glass market since it is among the biggest consumers of glass. 3D glass has certain specific characteristics such as strength, non-ponderousness and the capacity to produce complex shapes and that is why it is very useful in creation of extraordinary architectural visions. It can be used for designing beautiful and functional outer and inner shells, divisions, and ornamental patterns. With respect to appearance, buildings that incorporate 3D glass in its structures will be more appealing as more light is controlled to gain entrance into the buildings. Secondly, 3D glass in architecture introduce efficiency by allowing for better natural light control and lastly it introduce an additional flexibility in the building’s structural design.

- Further, 3D glass is gradually becoming considerable in the medical profession as well. In the medical devices sector, the property of 3D glass includes biocompatibility where the material is non-reactive with the human body’s tissues, chemicals resistance, and ability to produce complex shapes needed in the manufacturing of medical devices. It is most desirable in creating higher accuracy diagnostic equipment and sophisticated surgical equipment and wearable health devices. The use of 3D glass in these applications can result in the creation of more robust and effective tools that will positively impact the quality of treatments and patients’ well-being. Thus, the involvement of the 3D glass market with these varying industries can be most helpful in expanding its horizons and enhance various industries’ progression.

3D Glass Market Segment Analysis:

3D Glass Market Segmented based on Type, and Applications.

By Type, Polarized 3D Glasses is expected to dominate the market during the forecast period

- The 3D glass market is segmented into three main types: These are classified into; Anaglyph 3D glasses, Polarized 3D glasses, and Active Shutter 3D glasses. Of these segments, it can be ascertained that the Polarized 3D Glasses segment is at the moment enjoying the most market share. The main reasons that contributed to dominance of the related products are the following factors that defines polarized glasses from other types. Cinema and home theatre industries use polarized 3D glasses mainly because of their cheap price, simplicity, and quality image display. Contrary to the anaglyph glasses that use color filters and produce lower quality and distorted color images polarized glasses make use of polarisation to create relief and are more comfortable for watching 3D movies.

- Thus, the widespread of polarized 3D glasses is contributed by their versatility with the different types of display systems that are both passive and active 3D television. This versatility has made them favorite in the market with both the consumers as well as the manufactures. Finally, there is no need to replace batteries or synchronize the polarizing 3D glasses with the display; such being the case, the polarizing 3D glasses are cheaper and easier to produce and maintain as compared to the active shutter 3D glasses. The absence of electronic components and the frame’s minimal weight also increase user comfort, which in turn promotes the massive use of light frames.

- In addition, continuing improvements in the field of manufactured displays together with the industry’s increasing interest in 3D content for media, gaming, and other virtual realities have further solidified the existence of polarizing 3D glasses. Key players, manufacturers as well as cinema chains continue to support the polarized 3D system and are constantly sourcing for the technology and enhancing its quality. Therefore, the polarized 3D glasses segment will continue to dominate the 3D glass market due to ongoing advancements in 3D technology, customers’ preferences for quality and comfort when watching 3D videos and movies, and growing utilization of 3D technology across different industries.

By Application, Smartphone segment held the largest share

- Smartphones, wearable devices, televisions, virtual reality headsets, and other segments and subsegments have been identified and categorized as the 3D glass market application. From there, the current leading sub-segment is the smartphone segment. This is mainly because the smartphone is a part of modern society that is both widespread and constantly developing. Larger original equipment manufacturers of smartphones are using 3D glass in smartphones for beauty, better quality, and touch experience. The innovation on 3D glass has become more common in the developing of smartphones as it offers the option of a curvy screen and edge-to-edge power touch devices as well as sophisticated touch sensitivity that attracts more consumers.

- The current trend in the market is the high-end smartphones that require premium design and hence the use of materials such as 3D glass. When consumer matures, trying to get longer, slimmer, and more elegant, device, manufacturers use 3D glass for touch and for seeing. The use of 3D glass not only gives a better feel and looking but also it has more resistance to scratch and impact required by some of the users. BM stays for bezel-less and foldable smartphones, which creates additional demand for 3D glass since it is the material for such designs.

- Also, the growth of new technologies and constant competition in the sphere of creating new smartphones also play a significant role in the monopolistic position of the smartphone segment in the 3D glass market. Corporations are in a steady process of performing research to establish better, stronger, and more visually appealing glasses to counter rival innovations. In addition, the addition of AR and better display technologies is only possible if there is quality 3D glass used in smartphones; thus, the segment’s significance is established. Understood that the smartphone market will remain active and dynamic for a long time, the need for 3D glass also remains stable, which guarantees the lead of the segment.

3D Glass Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- The growth of the 3D glass industry is expected to be greatest in the North American region because of the higher technological development and spending on technological growth as well as innovation. The region comprises many major technology companies and research organizations that remain vendor-neutral and consistently develop new materials and production technologies. Out of all these regions, North America has assumed a highly strategic position with regards to focusing on innovation; by stressing more on 3D Glass that delivers top of the line qualities in terms of durability and clarity, they have thereby addressing most of the essential functions for functional use as seen in the electronics, automobile, and medical fields. Another advantage for companies operating in this region is that they managed to generate and accumulate solid patent protection.

- Another factor, is the more switches of product types demand, especially consumer electronics like smart phones, tablet and wearable devices, which apply 3D glass for better user experience and appearance. North American market, with focus on United States where population has high levels of consumption and demands hi-tech gadgets and high-quality goods. The reason that the market is demanding energy harvesting pathogen detection is due to this demand forcing more manufacturers to pay attention to this area. Besides, it is found that technology giants such as Apple and Google, both companies are from the USA, these play a vital role in mapping the market trends and integrating 3D glass in its prod667uct line.

- North America holds a robust supply chain as well as manufacturing industry for 3D glass, due to which it leads in this market. The region offers state of the art manufacturing plant, quality manpower, and supply chain for the efficient manufacture and distribution of 3D glass products. Moreover, the governmental consumer policies and promotion to provide incentives toward the development of technology and production act as essentials to the market. Such factors as these coupled with the symbiotic relationships among the various key industry players make North America to provide a favorable background for the 3D glass market’s growth and domination.

Active Key Players in the 3D Glass Market

- AGC Inc. (Japan)

- Asahi Glass Co. Ltd. (Japan)

- Avancis GmbH (Germany)

- Corning Inc. (United States)

- Corning Precision Materials Co., Ltd. (South Korea)

- DuraTech Industries (United States)

- First Solar Inc. (United States)

- Guardian Industries (United States)

- HOYA Corporation (Japan)

- LENS Technology (China)

- NEG (Nippon Electric Glass Co., Ltd.) (Japan)

- Nippon Electric Glass Co. Ltd. (Japan)

- NSG Group (Nippon Sheet Glass Co., Ltd.) (Japan)

- Saint-Gobain S.A. (France)

- Samsung Corning Advanced Glass (South Korea)

- Schott AG (Germany)

- Shenzhen O-Film Tech Co., Ltd. (China)

- Taiwan Glass Ind. Corp. (Taiwan)

- Trisolaris Co. Ltd. (Taiwan)

- Xinyi Glass Holdings Limited (China)

- Other Active Players

|

Global 3D Glass Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 15.87 Bn. |

|

Forecast Period 2025-35 CAGR: |

4.38 % |

Market Size in 2035: |

USD 25.43 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: 3D Glass Market by Type (2018-2035)

4.1 3D Glass Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Anaglyph 3D Glasses

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Polarized 3D Glasses

4.5 Active Shutter 3D Glasses

Chapter 5: 3D Glass Market by Application (2018-2035)

5.1 3D Glass Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Smartphone

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Wearable Device

5.5 Televisions

5.6 Virtual Reality Headsets

5.7 Others

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 3D Glass Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 AGC INC. (JAPAN)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 ASAHI GLASS CO. LTD. (JAPAN)

6.4 AVANCIS GMBH (GERMANY)

6.5 CORNING INC. (UNITED STATES)

6.6 CORNING PRECISION MATERIALS CO. LTD. (SOUTH KOREA)

6.7 DURATECH INDUSTRIES (UNITED STATES)

6.8 FIRST SOLAR INC. (UNITED STATES)

6.9 GUARDIAN INDUSTRIES (UNITED STATES)

6.10 HOYA CORPORATION (JAPAN)

6.11 LENS TECHNOLOGY (CHINA)

6.12 NEG (NIPPON ELECTRIC GLASS CO. LTD.) (JAPAN)

6.13 NIPPON ELECTRIC GLASS CO. LTD. (JAPAN)

6.14 NSG GROUP (NIPPON SHEET GLASS CO. LTD.) (JAPAN)

6.15 SAINT-GOBAIN S.A. (FRANCE)

6.16 SAMSUNG CORNING ADVANCED GLASS (SOUTH KOREA)

6.17 SCHOTT AG (GERMANY)

6.18 SHENZHEN O-FILM TECH CO. LTD. (CHINA)

6.19 TAIWAN GLASS IND. CORP. (TAIWAN)

6.20 TRISOLARIS CO. LTD. (TAIWAN)

6.21 XINYI GLASS HOLDINGS LIMITED (CHINA)

6.22 OTHER ACTIVE PLAYERS

Chapter 7: Global 3D Glass Market By Region

7.1 Overview

7.2. North America 3D Glass Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Type

7.2.4.1 Anaglyph 3D Glasses

7.2.4.2 Polarized 3D Glasses

7.2.4.3 Active Shutter 3D Glasses

7.2.5 Historic and Forecasted Market Size by Application

7.2.5.1 Smartphone

7.2.5.2 Wearable Device

7.2.5.3 Televisions

7.2.5.4 Virtual Reality Headsets

7.2.5.5 Others

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe 3D Glass Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Type

7.3.4.1 Anaglyph 3D Glasses

7.3.4.2 Polarized 3D Glasses

7.3.4.3 Active Shutter 3D Glasses

7.3.5 Historic and Forecasted Market Size by Application

7.3.5.1 Smartphone

7.3.5.2 Wearable Device

7.3.5.3 Televisions

7.3.5.4 Virtual Reality Headsets

7.3.5.5 Others

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe 3D Glass Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Type

7.4.4.1 Anaglyph 3D Glasses

7.4.4.2 Polarized 3D Glasses

7.4.4.3 Active Shutter 3D Glasses

7.4.5 Historic and Forecasted Market Size by Application

7.4.5.1 Smartphone

7.4.5.2 Wearable Device

7.4.5.3 Televisions

7.4.5.4 Virtual Reality Headsets

7.4.5.5 Others

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific 3D Glass Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Type

7.5.4.1 Anaglyph 3D Glasses

7.5.4.2 Polarized 3D Glasses

7.5.4.3 Active Shutter 3D Glasses

7.5.5 Historic and Forecasted Market Size by Application

7.5.5.1 Smartphone

7.5.5.2 Wearable Device

7.5.5.3 Televisions

7.5.5.4 Virtual Reality Headsets

7.5.5.5 Others

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa 3D Glass Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Type

7.6.4.1 Anaglyph 3D Glasses

7.6.4.2 Polarized 3D Glasses

7.6.4.3 Active Shutter 3D Glasses

7.6.5 Historic and Forecasted Market Size by Application

7.6.5.1 Smartphone

7.6.5.2 Wearable Device

7.6.5.3 Televisions

7.6.5.4 Virtual Reality Headsets

7.6.5.5 Others

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America 3D Glass Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Type

7.7.4.1 Anaglyph 3D Glasses

7.7.4.2 Polarized 3D Glasses

7.7.4.3 Active Shutter 3D Glasses

7.7.5 Historic and Forecasted Market Size by Application

7.7.5.1 Smartphone

7.7.5.2 Wearable Device

7.7.5.3 Televisions

7.7.5.4 Virtual Reality Headsets

7.7.5.5 Others

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Global 3D Glass Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 15.87 Bn. |

|

Forecast Period 2025-35 CAGR: |

4.38 % |

Market Size in 2035: |

USD 25.43 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||