Point Of Care Diagnostics Market Overview

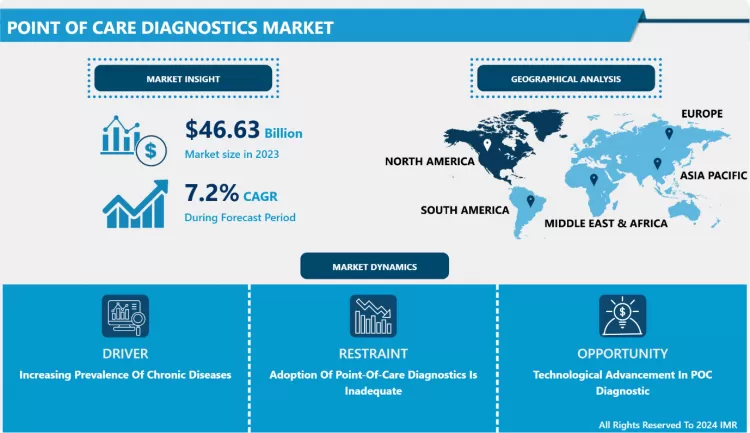

Global Point of Care Diagnostics Market was valued at USD 46.63 billion in 2023 and is expected to reach USD 87.18 billion by the year 2032, at a CAGR of 7.2%.

Point-of-care testing (POCT) is critical for detecting analytes close to the patient, allowing for better disease diagnosis, monitoring, and management. It allows for quick medical decisions because diseases can be diagnosed at an early stage, resulting in better health outcomes for patients by allowing for the early start of treatment. POC testing was first used in 1962 with the development of a method for rapid analysis of blood glucose, and soon after, in 1977, rapid pregnancy tests were developed, ushering in a trend for personalized diagnostics. POC diagnostic devices for monitoring glucose, ECG, blood pressure, and other parameters have greatly aided clinical and personalized healthcare.

Several prospective POCDs have been developed in recent years, providing a platform for next-generation POCT. The biosensor is the most important component of POCD and is directly responsible for an assay's bioanalytical performance. Several label-free biosensors, including electrochemical, surface plasmon resonance (SPR), white light reflectance spectroscopy (WLRS), and others, have been developed and are being used to improve POCD. The growing importance of point-of-care diagnostics in environmental monitoring and public health necessitates the incorporation of technologies that enable simple networking, making it easier for healthcare professionals to interpret test results accurately. Thus, in the coming years, remote access integration of POC tests and their networking is expected to open up new avenues for the industry.

Market Dynamics And Factors For Point of Care Diagnostics Market

Drivers:

Increasing Prevalence Of Chronic Diseases

The POCD market is poised for significant growth as the prevalence of chronic diseases such as diabetes, and kidney disease, and as the prevalence of cardiovascular disease rises, necessitating long-term care and frequent monitoring, so will the demand for cost-effective and innovative point-of-care diagnostic products. Chronic diseases are becoming more common all over the world. Changes in societal behaviour, as well as an aging population, are all contributing to a steady rise in these common and costly long-term health issues. As the middle class grows and urbanization accelerates, people are becoming more sedentary. As a result, obesity rates and cases of diseases such as diabetes are increasing. Chronic disease prevalence is expected to rise by 57% by 2020, according to the World Health Organization. As population growth is expected to be greatest in developing countries, emerging markets will be the hardest hit. As a result, the point care diagnostic market is expected to grow during the forecast period.

Restraints:

Adoption Of Point-Of-Care Diagnostics Is Inadequate

The majority of point-of-care diagnostics tests are performed by clinical professionals with less laboratory experience, such as nurses. Because hospitals have a large number of patients, these individuals concentrate on patient care and are constantly under pressure to provide prompt treatment. The sample collection and all other processes that clinical personnel perform while performing point-of-care diagnostics tests are generally unfamiliar. Furthermore, it has been observed that in most cases, the opinion of lab experts or healthcare workers is ignored. As a result, the decrease in the adoption of point-of-care diagnostics is impeding market growth.

Opportunity:

Technological Advancement In POC Diagnostic

Technological advancements have resulted in the development of several novel point-of-care diagnostic devices for a variety of applications. Recent advances in biosensing technology, microfluidics, and paper-based diagnostics will improve diagnostic quality and efficiency. Scientists and entrepreneurs have had a significant impact on the development of next-generation POC diagnostic devices based on cutting-edge technologies such as Artificial Intelligence (AI), the Internet of Things (IoT), and so on. POC technologies combined with smart information and communications technology (ICT) hold great promise for managing resources sustainably and improving healthcare delivery in rural areas. Thus, the future holds a lucrative opportunity for the point care diagnostic market.

Market Dynamics And Factors For Point Care Diagnostics Market

By Application, the glucose monitoring segment is forecasted to dominate the point care diagnostic market in the upcoming future. Glucose monitoring is the most common application for point-of-care diagnostic tests. Diabetes patients are monitored using point-of-care testing (POCT) for glucose at the bedside, at home, or in the hospital. The use of point-of-care (POC) glucose meters in self-monitoring of blood glucose is a valuable tool for managing glycemic control in diabetic patients. In adaptive clinical trials involving dose adjustment and blinded studies, glucose testing at the point of care has been used frequently. The most common tests are glucose and HBA1C. Small blood volumes of whole or venous samples are used in CLIA-Waived and moderately complex platforms. Results will be available in minutes. To eliminate potential preanalytical, analytical, and post-analytical errors, the POCT program for glucose should be evaluated. Thus, consolidating the growth of this segment in the projected timeframe.

By platform, the immunoassays segment is expected to have the highest share of the point of care diagnostic market in the projected timeframe. Immunoassays are valuable tools and the traditional gold standard in infectious disease diagnostics, detecting microbial antigens of pathogen-specific antibodies in crude samples such as blood, saliva, or nasal swabs, saving significant time when compared to culturing approaches, which is a critical bottleneck for in treating patients with severe disease. Enzyme-linked immunosorbent assays (ELISAs), lateral flow immunoassays (LFIAs), and chemiluminescent immunoassays are the most commonly used immunoassays for infectious disease serological testing (CLIAs). LIFAs are an especially appealing option because they require less operator skill and have the potential to be used in point-of-care settings. Thus, driving the growth of the immunoassays segment.

By end-users, the diagnostic laboratories segment is expected to dominate the point care diagnostic market in the forecasted timeframe. The prevalence of various ailments is increasing the point care diagnostic market in diagnostic laboratories. Because of the increasing number of COVID-19 cases worldwide and the governments of various countries' repeated requests for people to be tested, many stand-alone diagnostic centers, hospital-based diagnostic labs, and diagnostic chains have been approved and accredited to perform COVID-19 tests. Thus, strengthening the development of this segment.

Regional Analysis Of Point of Care Diagnostics Market

The North American region is anticipated to have the highest share of the point of care diagnostic market in the forecast period due to the growing awareness about the diagnosis of diseases. The global POCT market is expected to grow at a compound annual growth rate (CAGR) of 9.8 percent from 2016 to 2021, from US$ 23.16 billion in 2016. North America accounts for the majority of the global POCT market due to high healthcare affordability, premium healthcare infrastructure, and a high level of patient awareness.

The Asia Pacific region is expected to have the second-highest share of the point of care diagnostic market in the projected timeframe. In India, where healthcare resources and infrastructure are distributed unevenly, point-of-care tests are becoming an important tool for increasing diagnostic coverage of the population. India is a developing economy and a popular location for market investments. The development of healthcare infrastructure, combined with an increase in the prevalence of chronic and targeted diseases such as diabetes and cancer, as well as infectious diseases such as HIV, syphilis, COVID-19, RSV, and others, is expected to drive the regional market. Aside from the growing geriatric population, rising stress levels, and increased use of novel immunoassay techniques, strengthening the development of the point-of-care diagnostic market during the forecast period.

The point-of-care diagnostic market in the European region is expected to develop at a significant growth in the projected timeframe. COVID-19 has had a significant impact on Europe, particularly France. As a result of the region's exponential increase in COVID-19 cases, the European economy is suffering. With a high number of fatalities, Spain, Italy, Germany, France, and the United Kingdom are among the most affected European countries. According to the International Health Regulation, the current coronavirus (COVID-19) outbreak has been declared a Public Health Emergency of International Concern by WHO. The rising number of coronavirus infections and demand for advanced diagnostic solutions present a favorable opportunity for the region's adoption of point-of-care diagnostic kits. Rising investments and business activities by industry players are also expected to drive the point-of-care diagnostic market during the forecast period.

Covid-19 Impact Analysis On Point of Care Diagnostics Market

The COVID-19 pandemic has shifted the POC testing landscape in the world. It has fuelled research into the development of testing strategies that are both quick and inexpensive and can be used as point-of-care testing in the community. The pandemic has hastened the trend of experimenting with decentralization. Reaching out to patients outside of laboratories, hospitals, and homes enables a faster response to clinical needs. Point-of-care (POC) detection technologies that enable decentralized, rapid, sensitive, low-cost COVID-19 infection diagnostics are desperately needed around the world. The field of COVID-19 POC diagnostics is rapidly evolving, with many technologies approved for commercialization in the last ten months. In this Perspective, the current state of POC technologies for COVID-19 infection diagnosis and monitoring, as well as future challenges in COVID-19 diagnostics. As the COVID-19 pandemic becomes endemic, the advances made this year will most likely be used to predict future outbreaks and pandemics.

Top Key Players Covered In Point Care Diagnostics Market

- F. Hoffmann-La Roche Ltd (Basel, Switzerland)

- Thermo Fisher Scientific Inc. (Massachusetts, U.S.)

- Abbott Laboratories (Illinois, U.S.)

- Quest Diagnostics Incorporated (New Jersey, U.S.)

- BD (Franklin Lakes, U.S.)

- BioMerieux SA (Marcy l'Etoile, France)

- Cardinal Health, Inc. (Ohio, U.S.)

- Mesa Biotech (California, U.S.)

- Cepheid (California, U.S.)

- Trinity Biotech (Bray, Ireland)

- Quidel Corporation (San Diego, U.S.)

- Bio-Rad Laboratories Inc. (California, U.S.) and Other Major Players.

Key Industry Development In The Point Of Care Diagnostics Market

In January 2022, Roche launched its Cobas Pulse System in countries that accept the CE Mark. This is the latest generation of connected point-of-care solutions from Roche Diagnostics for professional blood glucose management.

In February 2021, Mesa Biotech, Inc. a privately held point-of-care molecular diagnostic company, has been acquired by Thermo Fisher Scientific Inc. Mesa Biotech created the Accula System, a point-of-care PCR-based infectious disease testing platform.

|

Global Point of Care Diagnostics Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 46.63 Bn. |

|

Forecast Period 2023-30 CAGR: |

7.2% |

Market Size in 2032: |

USD 87.18 Bn. |

|

Segments Covered: |

By Application |

|

|

|

By Platform |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Point of Care Diagnostics Market by Application (2018-2032)

4.1 Point of Care Diagnostics Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Infectious Disease Testing Products

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Glucose Monitoring Products

4.5 Pregnancy

4.6 Fertility Testing Products

4.7 Cardiometabolic Monitoring Products

4.8 Others

Chapter 5: Point of Care Diagnostics Market by Platform (2018-2032)

5.1 Point of Care Diagnostics Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Molecular Diagnostic

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Immunoassays

5.5 Lateral Flow Assays

5.6 Others

Chapter 6: Point of Care Diagnostics Market by End-User (2018-2032)

6.1 Point of Care Diagnostics Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Clinics

6.5 Diagnostic Laboratories

6.6 Home Care

6.7 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Point of Care Diagnostics Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ALFA LAVAL AB

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 THERMAX LIMITED

7.4 IHI CORPORATION

7.5 BABCOCK & WILCOX ENTERPRISES INCFORBES MARSHALL

7.6 BHARAT HEAVY ELECTRICALS LIMITED

7.7 HARBIN ELECTRIC GROUP (CHINA)

7.8 GENERAL ELECTRIC

7.9 HURST BOILER & WELDING CO INCAC BOILERS

7.10 SIEMENS

7.11 MITSUBISHI HEAVY INDUSTRIES LTDTHYSSENKRUPP AG

7.12 VIESSMANN LIMITED

Chapter 8: Global Point of Care Diagnostics Market By Region

8.1 Overview

8.2. North America Point of Care Diagnostics Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Application

8.2.4.1 Infectious Disease Testing Products

8.2.4.2 Glucose Monitoring Products

8.2.4.3 Pregnancy

8.2.4.4 Fertility Testing Products

8.2.4.5 Cardiometabolic Monitoring Products

8.2.4.6 Others

8.2.5 Historic and Forecasted Market Size by Platform

8.2.5.1 Molecular Diagnostic

8.2.5.2 Immunoassays

8.2.5.3 Lateral Flow Assays

8.2.5.4 Others

8.2.6 Historic and Forecasted Market Size by End-User

8.2.6.1 Hospitals

8.2.6.2 Clinics

8.2.6.3 Diagnostic Laboratories

8.2.6.4 Home Care

8.2.6.5 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Point of Care Diagnostics Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Application

8.3.4.1 Infectious Disease Testing Products

8.3.4.2 Glucose Monitoring Products

8.3.4.3 Pregnancy

8.3.4.4 Fertility Testing Products

8.3.4.5 Cardiometabolic Monitoring Products

8.3.4.6 Others

8.3.5 Historic and Forecasted Market Size by Platform

8.3.5.1 Molecular Diagnostic

8.3.5.2 Immunoassays

8.3.5.3 Lateral Flow Assays

8.3.5.4 Others

8.3.6 Historic and Forecasted Market Size by End-User

8.3.6.1 Hospitals

8.3.6.2 Clinics

8.3.6.3 Diagnostic Laboratories

8.3.6.4 Home Care

8.3.6.5 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Point of Care Diagnostics Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Application

8.4.4.1 Infectious Disease Testing Products

8.4.4.2 Glucose Monitoring Products

8.4.4.3 Pregnancy

8.4.4.4 Fertility Testing Products

8.4.4.5 Cardiometabolic Monitoring Products

8.4.4.6 Others

8.4.5 Historic and Forecasted Market Size by Platform

8.4.5.1 Molecular Diagnostic

8.4.5.2 Immunoassays

8.4.5.3 Lateral Flow Assays

8.4.5.4 Others

8.4.6 Historic and Forecasted Market Size by End-User

8.4.6.1 Hospitals

8.4.6.2 Clinics

8.4.6.3 Diagnostic Laboratories

8.4.6.4 Home Care

8.4.6.5 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Point of Care Diagnostics Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Application

8.5.4.1 Infectious Disease Testing Products

8.5.4.2 Glucose Monitoring Products

8.5.4.3 Pregnancy

8.5.4.4 Fertility Testing Products

8.5.4.5 Cardiometabolic Monitoring Products

8.5.4.6 Others

8.5.5 Historic and Forecasted Market Size by Platform

8.5.5.1 Molecular Diagnostic

8.5.5.2 Immunoassays

8.5.5.3 Lateral Flow Assays

8.5.5.4 Others

8.5.6 Historic and Forecasted Market Size by End-User

8.5.6.1 Hospitals

8.5.6.2 Clinics

8.5.6.3 Diagnostic Laboratories

8.5.6.4 Home Care

8.5.6.5 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Point of Care Diagnostics Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Application

8.6.4.1 Infectious Disease Testing Products

8.6.4.2 Glucose Monitoring Products

8.6.4.3 Pregnancy

8.6.4.4 Fertility Testing Products

8.6.4.5 Cardiometabolic Monitoring Products

8.6.4.6 Others

8.6.5 Historic and Forecasted Market Size by Platform

8.6.5.1 Molecular Diagnostic

8.6.5.2 Immunoassays

8.6.5.3 Lateral Flow Assays

8.6.5.4 Others

8.6.6 Historic and Forecasted Market Size by End-User

8.6.6.1 Hospitals

8.6.6.2 Clinics

8.6.6.3 Diagnostic Laboratories

8.6.6.4 Home Care

8.6.6.5 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Point of Care Diagnostics Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Application

8.7.4.1 Infectious Disease Testing Products

8.7.4.2 Glucose Monitoring Products

8.7.4.3 Pregnancy

8.7.4.4 Fertility Testing Products

8.7.4.5 Cardiometabolic Monitoring Products

8.7.4.6 Others

8.7.5 Historic and Forecasted Market Size by Platform

8.7.5.1 Molecular Diagnostic

8.7.5.2 Immunoassays

8.7.5.3 Lateral Flow Assays

8.7.5.4 Others

8.7.6 Historic and Forecasted Market Size by End-User

8.7.6.1 Hospitals

8.7.6.2 Clinics

8.7.6.3 Diagnostic Laboratories

8.7.6.4 Home Care

8.7.6.5 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Point of Care Diagnostics Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 46.63 Bn. |

|

Forecast Period 2023-30 CAGR: |

7.2% |

Market Size in 2032: |

USD 87.18 Bn. |

|

Segments Covered: |

By Application |

|

|

|

By Platform |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Frequently Asked Questions :

The forecast period in the Point of Care Diagnostics Market research report is 2024-2032.

F. Hoffmann-La Roche Ltd (Basel, Switzerland), Thermo Fisher Scientific Inc. (Massachusetts, U.S.), Abbott Laboratories (Illinois, U.S.), Quest Diagnostics Incorporated (New Jersey, U.S.), BD (Franklin Lakes, U.S.), BioMerieux SA (Marcy l'Etoile, France), Cardinal Health, Inc. (Ohio, U.S.), Mesa Biotech (California, U.S.), Cepheid (California, U.S.), Trinity Biotech (Bray, Ireland), Quidel Corporation (San Diego, U.S.), Bio-Rad Laboratories Inc. (California, U.S.) and other major players.

The Point of Care Diagnostics Market is segmented into Application, Platform, End-User, and region. By Application, the market is categorized into Infectious Disease Testing Products, Glucose Monitoring Products, Pregnancy, and Fertility Testing Products, Cardiometabolic Monitoring Products, and Others. By Platform, the market is categorized into Molecular Diagnostic, Immunoassays, Lateral Flow Assays, and Others. By End-User, the market is categorized into Hospitals, Clinics, Diagnostic Laboratories, Home Care, Others. By region, it is analyzed across North America (U.S.; Canada; Mexico), Europe (Germany; U.K.; France; Italy; Russia; Spain, etc.), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

Point-of-care testing (POCT) is critical for detecting analytes close to the patient, allowing for better disease diagnosis, monitoring, and management. It allows for quick medical decisions because diseases can be diagnosed at an early stage, resulting in better health outcomes for patients by allowing for the early start of treatment.

Global Point of Care Diagnostics Market was valued at USD 46.63 billion in 2023 and is expected to reach USD 87.18 billion by the year 2032, at a CAGR of 7.2%.