Next Generation Gynecological Cancer Diagnostic Market Overview

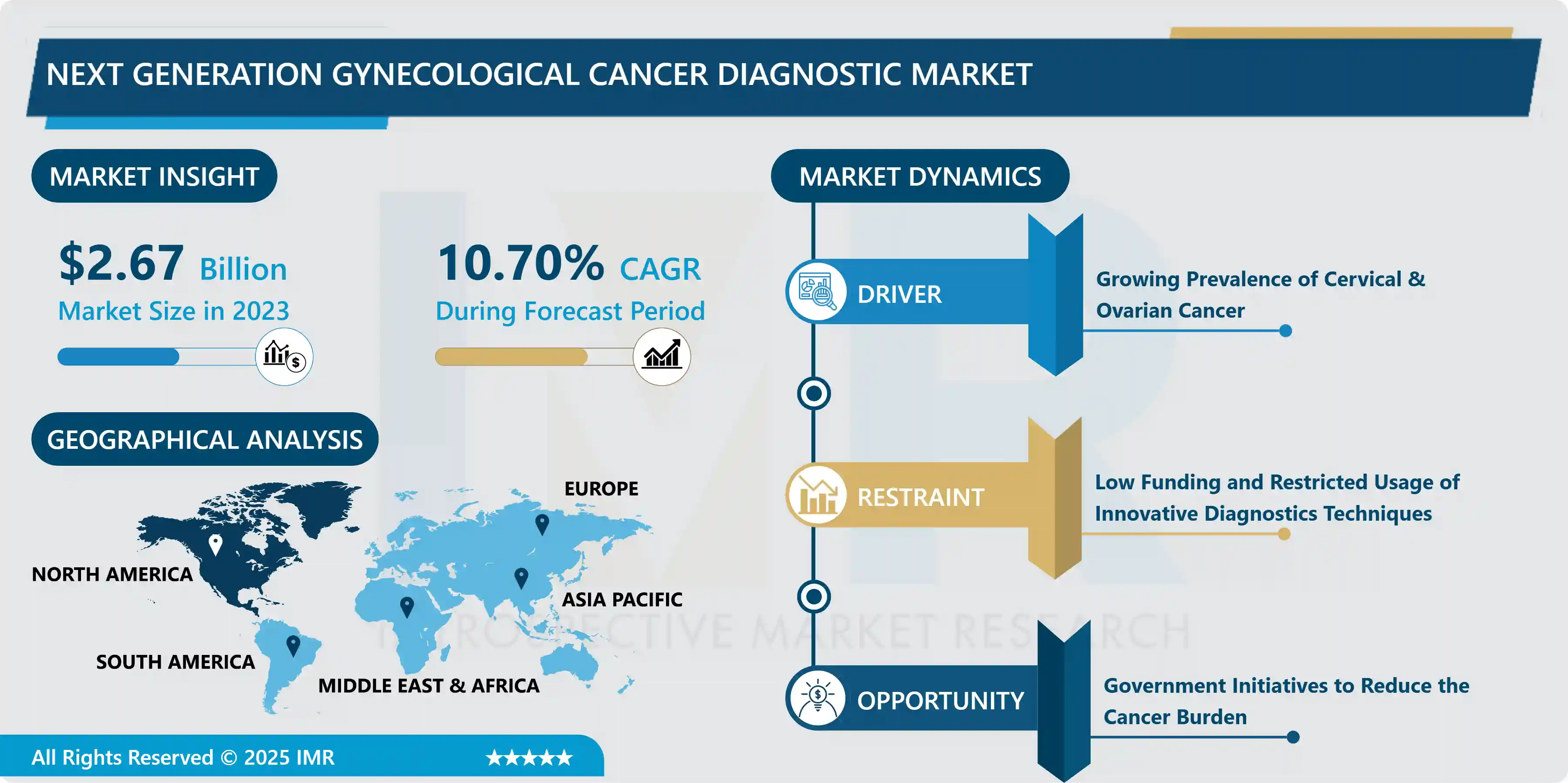

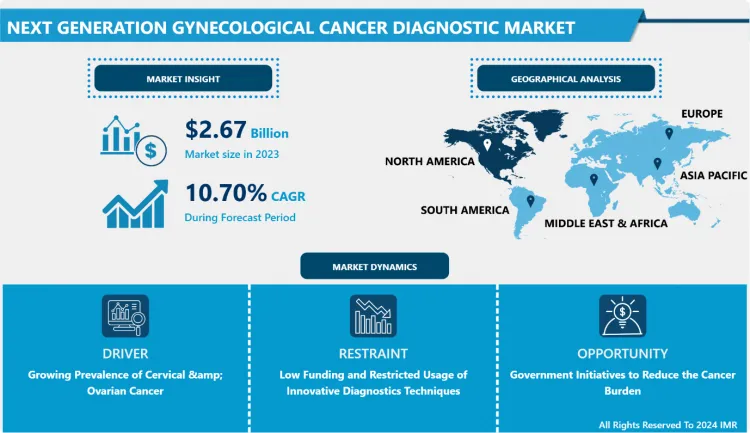

The Global Next Generation Gynecological Cancer Diagnostic Market size is expected to grow from USD 2.67 billion in 2023 to USD 6.67 billion by 2032, at a CAGR of 10.70% during the forecast period (2024-2032).

Cancer that originates in a woman's reproductive organs is referred to as gynecologic cancer. Cancer is always named after the body part where it first appears. Gynecologic cancers can start anywhere in a woman's pelvis, which is the area beneath the stomach and between hip bones. Cervical, ovarian, uterine, vaginal, and vulvar cancers are several types of gynecologic cancer. Ovarian cancer is the most common gynecologic cancer.

Advancement in technology has resulted in the development of innovative techniques for the diagnosis of gynecologic cancer such as quantitative polymerase chain reaction (qPCR) & multiplexing, next-generation sequencing, and lab-on-a-chip (LOAC) & reverse transcription-polymerase chain reaction (RT-PCR), and microarray. Advancements in the technologies of sequencing have supported researchers, and clinics to get knowledge which further helped to discover biomarkers for guidance. According to WHO, cancer is the leading cause of death across the globe, with approximately 10 million deaths in 2020. In the same year, about 342,000 women died due to cervical cancer. The growing prevalence of cervical cancer and the supportive government initiatives to prevent fatalities is expected to support the development of the next generation of gynecological cancer diagnostic over the forecasted timeframe.

Market Dynamics And Factors Next Generation Gynecological Cancer Diagnostic Market

Drivers:

Growing Prevalence of Cervical & Ovarian Cancer

- The increase in the number of gynecological cancer cases is the main factor stimulating the development of next-generation gynecological cancer diagnoses during the analysis period. Breast cancer is the most common cancer diagnosed in women worldwide, whereas, with an estimated 604,000 new cases in 2020, cervical cancer is the fourth most common cancer in women. Around 90% of the estimated 342,000 cervical cancer deaths in 2020 will occur in low- and middle-income countries. HIV-positive women are six times more likely than HIV-negative women to acquire cervical cancer, with HIV accounting for about 5% of all cervical cancer cases. Furthermore, HIV contributes disproportionately to cervical cancer in younger women in all world regions.

- Ovaries are a part of the female reproductive system, and ovarian cancer occurs when abnormal cells in the ovary begin to proliferate and divide uncontrollably. The most frequent kind of ovarian cancer is epithelial ovarian cancer. Primary peritoneal cancer and fallopian tube cancer are both treated the same way as epithelial ovarian cancer. Germ cell tumors (teratomas and dysgerminomas), stromal tumors (granulosa tumors), and sarcomas are all rare kinds of ovarian cancer. According to a WHO report, 314,000 females were diagnosed with ovarian cancer in 2020, and this number is expected to reach 429,000 by 2040. The fatalities were 207,000 in 2020 which is anticipated to reach 306,000 by 2040. Thus, the growing cases of ovarian and cervical cancer are expected to boost the expansion of the next-generation gynecological cancer diagnostic market over the analysis period.

Restraints:

Low Funding and Restricted Usage of Innovative Diagnostics Techniques

- Techniques involved in next-generation cancer diagnostics are new to the world, and there is a need for more research to validate their effectiveness in diagnostic procedures. Next-Generation Sequencing techniques are Laboratory Developed Tests (LDTs). There are very few laboratories that offer NGS for diagnostics as a skilled labor force is required. Regulatory policies regarding the development and usage of NGS are very strict. In order to get an FDA approval for NGS based in vitro diagnostics technique, the expenditure can cost between USD 20 to 30 million thus, the high developmental cost has restricted the commercialization of NGS diagnostic tests. Furthermore, in developing regions individuals are unaware of the advantages of next-generation diagnostics. In addition, developing regions lack the required funds for the procurement of hardware required for the setup of laboratories thus, hampering the development of the market.

Opportunities:

Government Initiatives to Reduce the Cancer Burden

- By avoiding risk factors and adapting evidence-based prevention strategies, 30 to 50 % of cancers can be avoided. Early detection, as well as adequate treatment and care for cancer patients, can help in decreasing the cancer burden. Many cancers have a good possibility of being cured if detected early and treated appropriately. Several governments have taken steps to combat the spread of noncommunicable diseases. Noncommunicable diseases, such as cardiovascular disease, cancer, chronic respiratory disease, diabetes, and others, are thought to account for over 60% of all deaths in India.

- The National Programme for the Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases, and Stroke (NPCDCS) was started in 2010 with an emphasis on infrastructure, human resource development, health promotion, early diagnosis, management, and referral to prevent and control major NCDs. The Government of India has launched the Tertiary Care Cancer Centers (TCCC) initiative, which aims to establish/strengthen 20 State Cancer Institutes (SCI) and 50 TCCCs across the country to provide comprehensive cancer care. A 'one-time grant' of USD 15 million for each SCI and USD 6 million per TCCC is provided under the scheme, to be used for building construction and equipment procurement. Similar initiatives by other governments are expected to create opportunities for market players.

Segmentation Analysis Of Next Generation Gynecological Cancer Diagnostic Market

- By technology, the Next Generation Sequencing segment is anticipated to develop at the highest CAGR over the forecasted timeframe. Next-Generation Sequencing has proven to be a valuable tool for obtaining a deeper and more precise look into the molecular underpinnings of individual tumors. When compared to traditional approaches, NGS has the potential to have a significant impact on the field of oncology due to its accuracy, sensitivity, and speed. Since NGS can test numerous genes in a single assay, it eliminates the need for multiple tests to find the causative mutation thus, supporting the development of the segment.

- By function, the companion diagnostics segment is anticipated to dominate the next-generation gynecological cancer diagnostic market over the forecasted timeframe. Companion diagnostics assist healthcare professionals in determining a patient's response to a specific agent to improve cancer patient outcomes and improve personalized medicine. This also aids in the reduction of rising healthcare expenses by limiting drug use to only those who will significantly benefit from it thus, strengthening the expansion of the segment in the projected period.

- By application, the biomarker development segment is expected to lead the development of the next-generation gynecological cancer diagnostic market. Patients with the same cancer type used to get the same treatment, but research has shown that tumors, even within the same cancer type, have distinct characteristics. Physicians are increasingly relying on cancer biomarkers to learn more about a patient's tumor and predict which treatment will be most effective against their specific cancer. Biomarkers can be utilized to personalize therapy for individual patients, reducing treatment costs.

Regional Analysis Of Next Generation Gynecological Cancer Diagnostic Market

- The North American region is anticipated to dominate the next-generation cancer diagnostics market over the forecasted period attributed to the growing prevalence of ovarian cancer. According to the American Cancer Society, about 19,880 women in the United States will receive a new diagnosis of ovarian cancer in 2022. The Society also estimated that 12,810 women will die from ovarian cancer. Ovarian cancer is the sixth leading cause of cancer death in women, accounting for more fatalities than any other cancer of the female reproductive system. A woman's lifetime risk of developing ovarian cancer is roughly 1 in 78. Her lifetime chance of dying from ovarian cancer is approximately 1 in 108. This cancer primarily affects older women. About half of the women diagnosed with ovarian cancer are 63 or older. The increasing geriatric population coupled with the rise in the number of gynecologic cancer cases are the main factors supporting the development of the market in this region.

- The European region is expected to have the second-highest share of the next-generation cancer diagnostics market in the analysis period. Cervical cancer is predicted to account for 2.5 % of cancer cases (excluding non-melanoma skin cancers) identified in women in 2020, and 2.4 % of all cancer deaths in women. Cervical cancer is the 11th most common cancer in women and the 12th most common cause of cancer death in them. In 2020, estimated cervical cancer incidence rates differed fivefold and fatality rates eightfold throughout the EU-27. This wide range can be attributed to differences in HPV prevalence, vaccination, and cervical cancer screening strategies between EU countries. The presence of prominent key players and rise in the R&D activities to develop innovative gynecological cancer diagnostic procedures are expected to support the growth of the market in this region.

- The next-generation cancer diagnostics market in the Asia-Pacific region is anticipated to develop at the highest CAGR over the analysis period. According to ICO/IARC Information Centre on HPV and Cancer, every year 123,907 women in India are diagnosed with cervical cancer, and 77,348 die from the disease. Cervical cancer is the second most common disease among women in India, and the second most common cancer among women aged 15 to 44. Moreover, the growing prevalence of ovarian, uterine, vaginal, and vulvar cancer cases in Japan, China, Indonesia, Singapore, and South Korea is expected to propel the growth of the next-generation cancer diagnostics market in this region.

Top Key Players Covered In Next Generation Gynecological Cancer Diagnostic Market

- Agilent Technologies (California, United States)

- ARUP Laboratories (California, United States)

- BGI Genomics (Shenzhen, China)

- CENTOGENE N.V. (Rostock, Germany)

- F. Hoffmann-La Roche Ltd (Basel, Switzerland)

- Fulgent Genetics (California, United States)

- Illumina Inc. (California, United States)

- Invitae Corporation (California, United States)

- Konica Minolta Inc. (Tokyo, Japan)

- Laboratory Corporation of America Holdings (California, United States)

- Myriad Genetics (Utah, United States)

- OPKO Health Inc. (Florida, United States)

- QIAGEN N.V. (Germany)

- Quest Diagnostics Incorporated (US)

- Thermo Fisher Scientific Inc. (US) and Other Major Players.

Key Industry Developments In The Next Generation Gynecological Cancer Diagnostic Market

- In February 2024, Hologic has received FDA clearance for its AI-enabled Genius Digital Diagnostics System, revolutionizing cervical cancer screening. The system digitizes Pap test slides and employs AI to identify cells for review, allowing cytologists and pathologists to detect potential cancers more efficiently. Hologic claims a study showed a 28% reduction in false negatives for severe lesions compared to traditional methods. Already available in Europe, the system is set to launch in the U.S. this year, giving Hologic a competitive edge over BD, which is still developing its AI-enabled screening technology.

- In September 2024, Ahmedabad-based DNA Wellness Private Limited is investing ?200 crore to set up 100 cervical cancer screening labs across India, introducing the advanced DNA Ploidy Test with exclusive rights from Canada's British Columbia Cancer Research Agency. This non-invasive test, offering 100% specificity and 98% sensitivity, can detect cancerous cells two years earlier than traditional methods. The first lab has launched in Ahmedabad, with more planned in Vadodara, Rajkot, and Surat by October 2024. With cervical cancer causing 1.3 lakh cases and 80,000 deaths annually in India, experts highlight the test's potential to revolutionize early detection and save lives.

|

Next Generation Gynecological Cancer Diagnostic Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.67 Bn. |

|

Forecast Period 2024-32 CAGR: |

10.70 % |

Market Size in 2032: |

USD 6.67 Bn. |

|

Segments Covered: |

By Technology |

|

|

|

By Function |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Next Generation Gynecological Cancer Diagnostic Market by Technology (2018-2032)

4.1 Next Generation Gynecological Cancer Diagnostic Market Snapshot and Growth Engine

4.2 Market Overview

4.3 qPCR & Multiplexing

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Next-Generation Sequencing

4.5 LOAC & RT-PCR

4.6 Other

Chapter 5: Next Generation Gynecological Cancer Diagnostic Market by Function (2018-2032)

5.1 Next Generation Gynecological Cancer Diagnostic Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Companion Diagnostics

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Therapeutic & Monitoring

5.5 Prognostic

5.6 Cancer Screening

5.7 Risk Analysis

Chapter 6: Next Generation Gynecological Cancer Diagnostic Market by Application (2018-2032)

6.1 Next Generation Gynecological Cancer Diagnostic Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Biomarker Development

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 CTC Analysis

6.5 Proteomic Analysis

6.6 Epigenetic Analysis

6.7 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Next Generation Gynecological Cancer Diagnostic Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 BRAINLAB AG

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 DORICON MEDICAL SYSTEMS DIVISION

7.4 EIZO CORPORATION

7.5 INTEGRITECH

7.6 KARL STORZ GMBH & CO. KG

7.7 MERIVAARA CORPORATION

7.8 OLYMPUS CORPORATION

7.9 SKYTRON LLC

7.10 STERIS

7.11 STRYKER CORPORATION

7.12 TRUMPF MEDICAL SYSTEMS INC. ANDOTHER MAJOR PLAYERS.

Chapter 8: Global Next Generation Gynecological Cancer Diagnostic Market By Region

8.1 Overview

8.2. North America Next Generation Gynecological Cancer Diagnostic Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Technology

8.2.4.1 qPCR & Multiplexing

8.2.4.2 Next-Generation Sequencing

8.2.4.3 LOAC & RT-PCR

8.2.4.4 Other

8.2.5 Historic and Forecasted Market Size by Function

8.2.5.1 Companion Diagnostics

8.2.5.2 Therapeutic & Monitoring

8.2.5.3 Prognostic

8.2.5.4 Cancer Screening

8.2.5.5 Risk Analysis

8.2.6 Historic and Forecasted Market Size by Application

8.2.6.1 Biomarker Development

8.2.6.2 CTC Analysis

8.2.6.3 Proteomic Analysis

8.2.6.4 Epigenetic Analysis

8.2.6.5 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Next Generation Gynecological Cancer Diagnostic Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Technology

8.3.4.1 qPCR & Multiplexing

8.3.4.2 Next-Generation Sequencing

8.3.4.3 LOAC & RT-PCR

8.3.4.4 Other

8.3.5 Historic and Forecasted Market Size by Function

8.3.5.1 Companion Diagnostics

8.3.5.2 Therapeutic & Monitoring

8.3.5.3 Prognostic

8.3.5.4 Cancer Screening

8.3.5.5 Risk Analysis

8.3.6 Historic and Forecasted Market Size by Application

8.3.6.1 Biomarker Development

8.3.6.2 CTC Analysis

8.3.6.3 Proteomic Analysis

8.3.6.4 Epigenetic Analysis

8.3.6.5 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Next Generation Gynecological Cancer Diagnostic Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Technology

8.4.4.1 qPCR & Multiplexing

8.4.4.2 Next-Generation Sequencing

8.4.4.3 LOAC & RT-PCR

8.4.4.4 Other

8.4.5 Historic and Forecasted Market Size by Function

8.4.5.1 Companion Diagnostics

8.4.5.2 Therapeutic & Monitoring

8.4.5.3 Prognostic

8.4.5.4 Cancer Screening

8.4.5.5 Risk Analysis

8.4.6 Historic and Forecasted Market Size by Application

8.4.6.1 Biomarker Development

8.4.6.2 CTC Analysis

8.4.6.3 Proteomic Analysis

8.4.6.4 Epigenetic Analysis

8.4.6.5 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Next Generation Gynecological Cancer Diagnostic Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Technology

8.5.4.1 qPCR & Multiplexing

8.5.4.2 Next-Generation Sequencing

8.5.4.3 LOAC & RT-PCR

8.5.4.4 Other

8.5.5 Historic and Forecasted Market Size by Function

8.5.5.1 Companion Diagnostics

8.5.5.2 Therapeutic & Monitoring

8.5.5.3 Prognostic

8.5.5.4 Cancer Screening

8.5.5.5 Risk Analysis

8.5.6 Historic and Forecasted Market Size by Application

8.5.6.1 Biomarker Development

8.5.6.2 CTC Analysis

8.5.6.3 Proteomic Analysis

8.5.6.4 Epigenetic Analysis

8.5.6.5 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Next Generation Gynecological Cancer Diagnostic Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Technology

8.6.4.1 qPCR & Multiplexing

8.6.4.2 Next-Generation Sequencing

8.6.4.3 LOAC & RT-PCR

8.6.4.4 Other

8.6.5 Historic and Forecasted Market Size by Function

8.6.5.1 Companion Diagnostics

8.6.5.2 Therapeutic & Monitoring

8.6.5.3 Prognostic

8.6.5.4 Cancer Screening

8.6.5.5 Risk Analysis

8.6.6 Historic and Forecasted Market Size by Application

8.6.6.1 Biomarker Development

8.6.6.2 CTC Analysis

8.6.6.3 Proteomic Analysis

8.6.6.4 Epigenetic Analysis

8.6.6.5 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Next Generation Gynecological Cancer Diagnostic Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Technology

8.7.4.1 qPCR & Multiplexing

8.7.4.2 Next-Generation Sequencing

8.7.4.3 LOAC & RT-PCR

8.7.4.4 Other

8.7.5 Historic and Forecasted Market Size by Function

8.7.5.1 Companion Diagnostics

8.7.5.2 Therapeutic & Monitoring

8.7.5.3 Prognostic

8.7.5.4 Cancer Screening

8.7.5.5 Risk Analysis

8.7.6 Historic and Forecasted Market Size by Application

8.7.6.1 Biomarker Development

8.7.6.2 CTC Analysis

8.7.6.3 Proteomic Analysis

8.7.6.4 Epigenetic Analysis

8.7.6.5 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Next Generation Gynecological Cancer Diagnostic Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.67 Bn. |

|

Forecast Period 2024-32 CAGR: |

10.70 % |

Market Size in 2032: |

USD 6.67 Bn. |

|

Segments Covered: |

By Technology |

|

|

|

By Function |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||