Hard Disk Market Synopsis

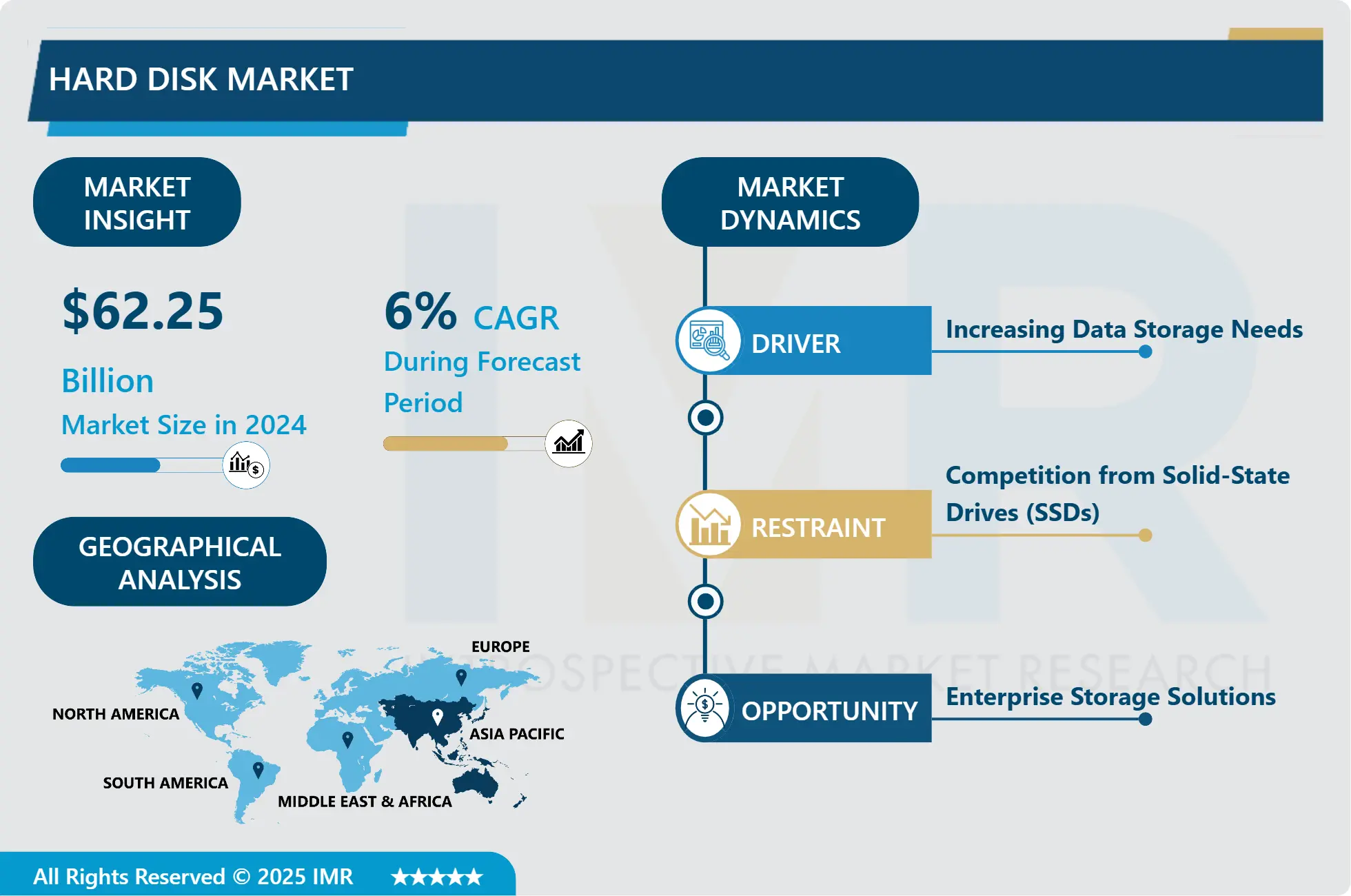

Hard Disk Market Size Was Valued at USD 62.25 Billion in 2024 and is Projected to Reach USD 99.22 Billion by 2032, Growing at a CAGR of 6.00% From 2025-2032.

The hard disk market comprises the worldwide industry that is engaged in the production, marketing, and distribution of solid-state drives (SSDs) and hard disk drives (HDDs). HDDs are appropriate for high-capacity storage requirements in a variety of devices, including PCs, servers, and data centers, since they employ magnetic storage to store and retrieve digital data. In contrast to conventional HDDs, SSDs use flash memory for data storage, which provides quicker read/write rates and increased reliability. Growing data creation in industries like as consumer electronics, IT, and telecommunications, together with an increasing need for quicker and more effective storage solutions, are driving the market. Significant factors influencing the growth and evolution of the market include technological breakthroughs, declining costs in SSD manufacturing, and the growing popularity of cloud computing.

The development of data storage technologies and rising demand from a variety of industries have led to further changes in the worldwide hard disk market. The increasing amount of data produced by individuals and enterprises is one of the main factors driving the need for storage solutions with more capacity. The market is expanding due to advancements in solid-state drives (SSDs), which provide enhanced dependability and quicker data access rates than conventional hard disk drives (HDDs).

Driven by fast industrialization, widespread acceptance of new technologies, and growing data center infrastructure, Asia Pacific continues to hold a leading position in the hard disk market geographically. With a high demand from businesses improving their storage capacity to address big data analytics and cloud computing requirements, North America and Europe also make major contributions.

Constraints come in the form of issues like shifting raw material prices and growing competition from cloud storage providers. Technological developments like as NAND flash-based SSDs and helium-filled HDDs are anticipated to maintain market growth despite these obstacles.

The growing need for dependable and high-capacity storage solutions across a variety of industries, including IT, healthcare, telecommunications, and media, is expected to propel the hard disk market's overall steady growth. Product developments, growing distribution networks, and strategic partnerships will probably be essential for businesses looking to take advantage of new possibilities in an ever-changing industry.

Hard Disk Market Trend Analysis

Transition from HDDs to SSD

- The transition from traditional hard disk drives (HDDs) to solid-state drives (SSDs) marks a significant evolution in storage technology, driven by the demand for enhanced performance and efficiency across various sectors. SSDs leverage flash memory technology to store data electronically, eliminating the mechanical components found in HDDs that can cause latency and reduce reliability. This shift translates into faster data access speeds, significantly improving the responsiveness and overall performance of computing devices and storage systems.

- In addition to speed, SSDs offer lower power consumption compared to HDDs, making them more energy-efficient and suitable for battery-powered devices such as laptops and mobile devices. This efficiency not only prolongs battery life but also reduces operational costs in data centers where power consumption is a significant concern. Furthermore, SSDs are inherently more durable and resistant to physical shock and vibration, making them ideal for environments where reliability and data integrity are paramount, such as in industrial applications and mission-critical operations.

- The adoption of SSDs continues to grow across consumer electronics, enterprise storage solutions, and cloud computing platforms due to their superior performance characteristics and evolving cost-effectiveness. As technology advancements drive down the price-per-gigabyte of SSDs, their widespread adoption is expected to accelerate, further solidifying SSDs as the preferred choice for high-performance storage solutions in both consumer and enterprise markets.

Meeting Demands for Higher Storage Capacities

- The explosive growth of data-intensive applications in a variety of industries, including cloud computing, big data analytics, and the spread of high-definition multimedia content, is driving an increase in the need for larger storage capabilities. Strong storage systems that can safely and effectively manage enormous volumes of data are required due to this expansion. In response, producers are giving greater emphasis to creating denser storage options that preserve small form factors while supporting bigger data amounts.

- Advancements in storage technology, such as 3D stacking methods and sophisticated NAND flash memory, are essential for enabling larger storage densities without appreciably expanding the physical footprint. In addition to meeting scalability requirements, these developments also help lower power consumption and improve overall efficiency—factors that are crucial for consumer devices as well as storage settings at the business level.

- Furthermore, research and development into next-generation architectures like storage-class memory (SCM) and non-volatile memory express (NVMe) is being fueled by the desire for denser storage solutions. By delivering significantly faster data access rates and lower latency, these technologies are expected to fulfill the demanding performance needs of contemporary data-centric applications. Finding denser and more effective storage solutions is still crucial to enabling the continuous digital transformation of all sectors as data volumes continue to rise dramatically.

Hard Disk Market Segment Analysis:

Hard Disk Market Segmented based on By Form Factor and By Application.

By Form Factor, 2.5 inch segment is expected to dominate the market during the forecast period

- Because of its small size and effective performance features, 2.5 inch drives have become industry standard in the mobile and consumer electronics industries. Within the domain of portable electronics like laptops, ultrabooks, and tablets, these drives provide an essential equilibrium between storage quantity and physical dimensions. Because of its compact form size, manufacturers are able to create devices that are lightweight and aesthetically pleasing without sacrificing storage capacity. Because 2.5 inch drives often use less power than bigger options, this makes them perfect for customers who value mobility and battery life.

- Furthermore, because of their dependability and adaptability, 2.5 inch drives are preferred in the consumer electronics sector. They are frequently found in external portable devices that are used for media consumption, file storage, and backups. The reason for their broad popularity is that they are attractive to customers who want to increase the storage capacity of their laptops or desktop computers without having to change their internal components since they offer a lot of storage space in a small container. Furthermore, they are a well-liked option for daily computing requirements, ranging from multimedia libraries to personal papers, due to their interoperability with a wide range of operating systems and devices.

- Overall, 2.5-inch drives' dominance in the consumer and mobile markets highlights how well-suited they are to the needs of contemporary computing, where dependability, energy economy, and space efficiency are critical. These drives are anticipated to develop further as technology progresses, possibly including larger storage capacity and quicker data transfer rates while keeping their small size, thereby continuing to satisfy the changing demands of consumers electronics and mobile device users throughout the globe.

By Application, Mobile segment held the largest share in 2024

- The mobile segment of storage devices, led by 2.5 inch and M.2 SSDs, is crucial in the realm of smartphones, tablets, and ultra-portable laptops, where compactness and efficiency are paramount. 2.5 inch drives, known for their balance of storage capacity and physical size, are commonly integrated into laptops and portable external drives. Their adoption in ultra-portable devices is driven by their ability to provide sufficient storage for operating systems, applications, and user data while maintaining a slim profile. This form factor is particularly favored in laptops and ultrabooks where space constraints necessitate smaller components without sacrificing storage capabilities. Additionally, their compatibility with various operating systems and devices makes them a versatile choice for consumers seeking expandable storage options for their mobile computing needs.

- On the other hand, M.2 SSDs represent a newer generation of storage technology increasingly dominant in the mobile segment. These drives offer significantly faster data transfer speeds and lower power consumption compared to traditional 2.5 inch HDDs or even SATA SSDs. Their compact size and direct integration into motherboard slots make them ideal for smartphones, tablets, and ultra-thin laptops that prioritize speed and energy efficiency. M.2 SSDs enhance the overall performance of mobile devices by reducing load times for applications and improving overall system responsiveness, thereby enhancing the user experience. Their deployment in mobile devices underscores a shift towards more efficient storage solutions that can meet the demands of modern computing tasks such as multimedia editing, gaming, and cloud-based applications, all while maintaining longer battery life crucial for mobile use cases.

Hard Disk Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast period

- Asia Pacific stands out as the fastest-growing market for hard disks, propelled by several key factors driving digital transformation across the region. Rapid industrialization and urbanization in countries such as China and India have spurred unprecedented growth in data generation across diverse sectors. For instance, China's booming e-commerce sector, coupled with increasing digitalization in manufacturing and logistics, has led to a soaring demand for robust storage solutions capable of handling vast amounts of transactional and operational data.

- Moreover, the proliferation of mobile devices and IoT applications has further intensified the need for scalable and reliable storage infrastructure. In Japan and South Korea, advanced technological ecosystems are driving demand for high-performance hard disks in areas like AI development, autonomous vehicles, and smart city initiatives. These countries are at the forefront of adopting cutting-edge technologies that require efficient data storage and processing capabilities to support their innovative projects and sustain economic growth.

- In addition to consumer-grade applications, the adoption of enterprise-grade storage solutions is gaining momentum across Asia Pacific. Governments across the region are increasingly investing in digital healthcare systems, smart governance solutions, and cloud-based services, necessitating robust data centers and storage solutions to ensure data security, accessibility, and compliance with regulatory requirements. This burgeoning demand presents significant opportunities for global hard disk manufacturers and providers of storage solutions to expand their presence and cater to the evolving needs of a digitally transforming Asia Pacific market.

Active Key Players in the Hard Disk Market

- Seagate Technology Holdings PLC

- Western Digital Corporation

- Toshiba Corporation

- Hewlett Packard Enterprise Development LP

- Sony Corporation

- Transcend Information Inc.

- Schneider Electric

- Lenovo Group Limited

- ADATA Technology Co. Ltd

- Buffalo Americas Inc.

- Other Key Players

Hard Disk Market Scope:

|

Global Hard Disk Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 62.25 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.00% |

Market Size in 2032: |

USD 99.22 Bn. |

|

Segments Covered: |

By Form Factor |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Hard Disk Market by Form Factor (2018-2032)

4.1 Hard Disk Market Snapshot and Growth Engine

4.2 Market Overview

4.3 2.5 inch

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 3.5 inch

4.5 Others

Chapter 5: Hard Disk Market by Application (2018-2032)

5.1 Hard Disk Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Mobile

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Consumer

5.5 Desktop

5.6 Enterprise

5.7 Nearline

5.8 Other Applications

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Hard Disk Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 SEAGATE TECHNOLOGY HOLDINGS PLC

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 WESTERN DIGITAL CORPORATION

6.4 TOSHIBA CORPORATION

6.5 HEWLETT PACKARD ENTERPRISE DEVELOPMENT LP

6.6 SONY CORPORATION

6.7 TRANSCEND INFORMATION INCSCHNEIDER ELECTRIC

6.8 LENOVO GROUP LIMITED

6.9 ADATA TECHNOLOGY CO. LTD

6.10 BUFFALO AMERICAS INC.

6.11 OTHER KEY PLAYERS

Chapter 7: Global Hard Disk Market By Region

7.1 Overview

7.2. North America Hard Disk Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Form Factor

7.2.4.1 2.5 inch

7.2.4.2 3.5 inch

7.2.4.3 Others

7.2.5 Historic and Forecasted Market Size by Application

7.2.5.1 Mobile

7.2.5.2 Consumer

7.2.5.3 Desktop

7.2.5.4 Enterprise

7.2.5.5 Nearline

7.2.5.6 Other Applications

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Hard Disk Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Form Factor

7.3.4.1 2.5 inch

7.3.4.2 3.5 inch

7.3.4.3 Others

7.3.5 Historic and Forecasted Market Size by Application

7.3.5.1 Mobile

7.3.5.2 Consumer

7.3.5.3 Desktop

7.3.5.4 Enterprise

7.3.5.5 Nearline

7.3.5.6 Other Applications

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Hard Disk Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Form Factor

7.4.4.1 2.5 inch

7.4.4.2 3.5 inch

7.4.4.3 Others

7.4.5 Historic and Forecasted Market Size by Application

7.4.5.1 Mobile

7.4.5.2 Consumer

7.4.5.3 Desktop

7.4.5.4 Enterprise

7.4.5.5 Nearline

7.4.5.6 Other Applications

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Hard Disk Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Form Factor

7.5.4.1 2.5 inch

7.5.4.2 3.5 inch

7.5.4.3 Others

7.5.5 Historic and Forecasted Market Size by Application

7.5.5.1 Mobile

7.5.5.2 Consumer

7.5.5.3 Desktop

7.5.5.4 Enterprise

7.5.5.5 Nearline

7.5.5.6 Other Applications

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Hard Disk Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Form Factor

7.6.4.1 2.5 inch

7.6.4.2 3.5 inch

7.6.4.3 Others

7.6.5 Historic and Forecasted Market Size by Application

7.6.5.1 Mobile

7.6.5.2 Consumer

7.6.5.3 Desktop

7.6.5.4 Enterprise

7.6.5.5 Nearline

7.6.5.6 Other Applications

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Hard Disk Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Form Factor

7.7.4.1 2.5 inch

7.7.4.2 3.5 inch

7.7.4.3 Others

7.7.5 Historic and Forecasted Market Size by Application

7.7.5.1 Mobile

7.7.5.2 Consumer

7.7.5.3 Desktop

7.7.5.4 Enterprise

7.7.5.5 Nearline

7.7.5.6 Other Applications

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

Hard Disk Market Scope:

|

Global Hard Disk Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 62.25 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.00% |

Market Size in 2032: |

USD 99.22 Bn. |

|

Segments Covered: |

By Form Factor |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||