Key Market Highlights

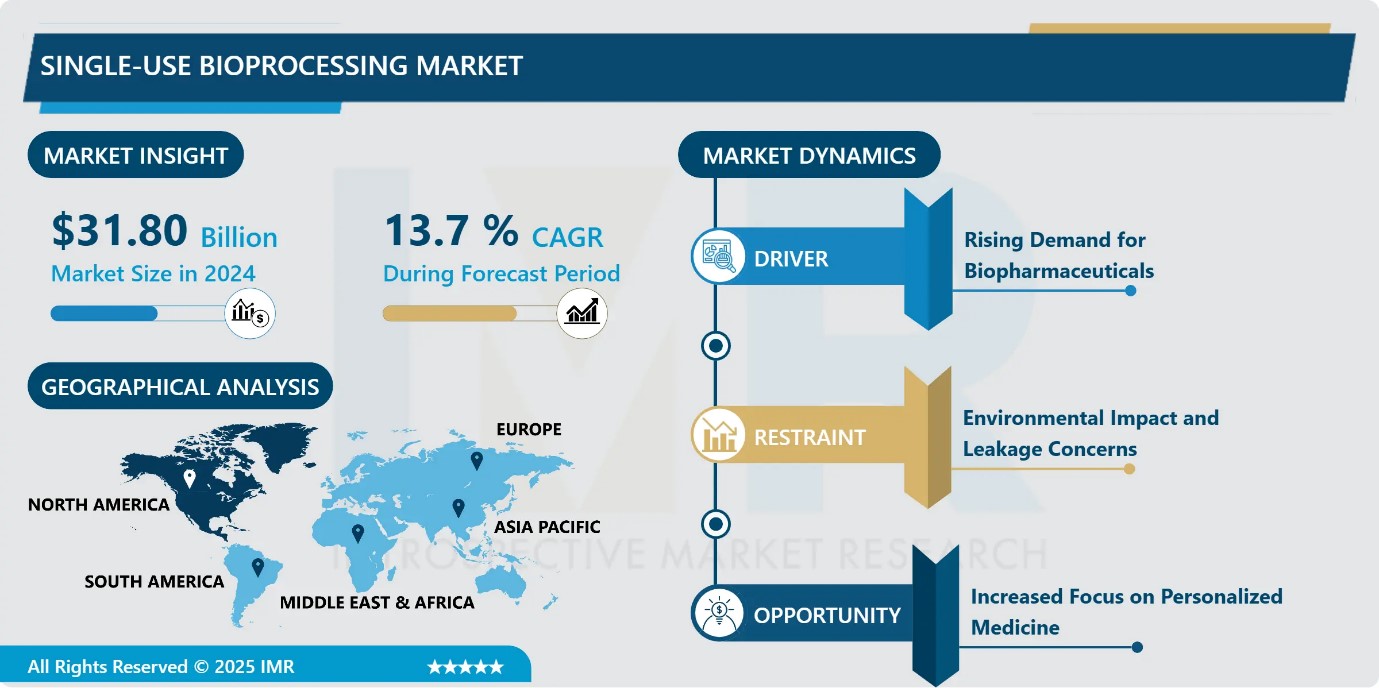

Single-use Bioprocessing Market Size Was Valued at USD 31.80 Billion in 2024, and is Projected to Reach USD 130.55 Billion by 2035, Growing at a CAGR of 13.7% from 2025-2035.

- Market Size in 2024: USD 31.80 Billion

- Projected Market Size by 2035: USD 130.55 Billion

- CAGR (2025–2035): 13.7%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia-Pacific

- By Workflow: The Upstream Processing segment is anticipated to lead the market by accounting for 36.6% of the market share throughout the forecast period.

- By End User: The Biopharmaceutical Companies segment is expected to capture 62.3% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 33.6% of the market share during the forecast period.

- Active Players: AmplifyBio (United States), Avantor, Inc. (United States), Corning Incorporated (United States), Danaher Corporation (United States), Eppendorf AG (Germany), and Other Active Players.

Single-use Bioprocessing Market Synopsis:

The single-use bioprocessing market refers to the use of disposable bioprocessing equipment and systems in biopharmaceutical manufacturing. The market has gained strong momentum due to the COVID-19 pandemic, which accelerated the adoption of flexible and scalable manufacturing solutions. The growing commercial success of biopharmaceuticals has encouraged manufacturers to expand production capacities globally, supported by investments in single-use technologies. Increasing focus on advanced therapies such as cell and gene therapies, along with higher clinical trial success rates and regulatory approvals, is further driving demand. Additionally, rising outsourcing of biopharmaceutical manufacturing has led CMOs to widely adopt single-use systems to manage diverse and rapidly changing product portfolios. However, large-scale manufacturers still rely on stainless steel systems, posing a challenge to market growth.

Single-use Bioprocessing Market Dynamics and Trend Analysis:

Single-use Bioprocessing Market Growth Driver-Rising Demand for Biopharmaceuticals

- The rising demand for biopharmaceutical products is a major driver of the single-use bioprocessing market. Continued growth in biologics, including monoclonal antibodies, vaccines, and advanced therapies, is increasing the need for efficient and adaptable manufacturing solutions. Single-use bioprocessing systems support rapid production scale-up and flexible batch processing, enabling manufacturers to respond quickly to evolving market and clinical demands. Their ability to reduce cross-contamination risks, lower cleaning and validation requirements, and shorten production timelines further strengthens adoption. As the global biopharmaceutical sector continues to expand, dependence on single-use technologies is expected to grow, driving sustained market momentum.

Single-use Bioprocessing Market Limiting Factor-Environmental Impact and Leakage Concerns

- Environmental and safety concerns remain key restraints in the single-use bioprocessing market. The extensive reliance on disposable plastic components contributes to increased plastic waste and a higher carbon footprint, creating sustainability challenges due to limited recycling options. These environmental issues have drawn regulatory and industry scrutiny, potentially slowing adoption.

- In addition, concerns related to extractables and leachables from plastic materials pose risks to product quality and patient safety, particularly in sensitive biopharmaceutical applications. Addressing these challenges requires advanced material development and improved waste management solutions. Until such issues are effectively mitigated, environmental impact and leakage concerns may restrain broader market growth.

Single-use Bioprocessing Market Expansion Opportunity-Increased Focus on Personalized Medicine

- The growing emphasis on personalized medicine presents a significant growth opportunity for the single-use bioprocessing market. As healthcare shifts toward patient-specific therapies, manufacturers increasingly require flexible, modular, and small-batch production capabilities. Single-use bioprocessing systems are well suited to meet these needs, offering rapid changeovers, scalability, and customization for individualized biologics and advanced therapies. The rising number of clinical trials targeting personalized treatments, including cell and gene therapies, further accelerates demand for adaptable manufacturing platforms. By enabling efficient, contamination-free production of customized therapies, single-use technologies are becoming integral to personalized medicine development, supporting broader market expansion.

Single-use Bioprocessing Market Challenge and Risk-Regulatory Compliance and Sustainability Pressures

- Regulatory and environmental pressures present significant challenges for the single-use bioprocessing market. Enhanced regulatory scrutiny on extractables and leachables, driven by updated USP standards replacing legacy testing requirements, has increased the complexity and cost of system qualification. Suppliers must invest heavily in advanced material characterization and analytical validation, extending development timelines and favoring established players with strong technical capabilities.

- Simultaneously, rising ESG requirements and circular-economy regulations are intensifying concerns around plastic waste management. Single-use systems generate substantially higher solid waste volumes, while limited recycling infrastructure and rising disposal costs continue to constrain widespread adoption.

Single-use Bioprocessing Market Trend-Advancements in Single-Use Technologies

- Advancements in single-use bioprocessing technologies are emerging as a key market trend, significantly driving industry growth. Continuous improvements in material science and system design have resulted in more durable, reliable, and high-performance disposable components. The integration of advanced filtration solutions, real-time sensors, and monitoring tools has enhanced process control, operational efficiency, and product consistency.

- These innovations support improved sterility assurance while reducing contamination risks and downtime. Furthermore, enhanced automation and data integration capabilities are enabling greater scalability and flexibility across biomanufacturing workflows. Ongoing investments in R&D by major industry players are expected to further strengthen the adoption of single-use systems, supporting sustained market expansion.

Single-use Bioprocessing Market Segment Analysis:

Single-use Bioprocessing Market is segmented based on Product, Application, Workflow, End User and Region.

By Workflow, Upstream processing segment is expected to dominate the market with around 36.6% share during the forecast period.

- Upstream processing accounted for around 36.6% of total single-use bioprocessing revenue in 2024, driven by strong industry confidence in single-use bioreactors for mammalian cell culture applications. Advances such as high-intensity perfusion and improved process control have enhanced productivity, making disposable bioreactors well suited for large-scale monoclonal antibody manufacturing. While upstream remains the largest segment, downstream processing is gaining momentum, growing at a CAGR of approximately 15.05% as innovations in membrane-based separation, resin-free chromatography, and single-pass filtration improve performance.

By End User, Biopharmaceutical companies is expected to dominate with close to 62.3% market share during the forecast period.

- Biopharmaceutical companies accounted for approximately 62.3% of total single-use bioprocessing purchases in 2024, maintaining their position as the dominant end-user segment. However, growth within this group has begun to moderate as major players complete large-scale conversion to single-use platforms and shift focus toward process optimization and efficiency gains. In contrast, academic and clinical research institutes are emerging as the fastest-growing users supported by public funding and research grants. The adoption of disposable systems in educational settings facilitates hands-on training without complex infrastructure, strengthening long-term market demand through workforce familiarity.

Single-use Bioprocessing Market Regional Insights:

North America region is estimated to lead the market with around 33.6% share during the forecast period.

- North America dominates the global single-use bioprocessing market, holding nearly 33.6% revenue share in 2024. This leadership is driven by a well-established biopharmaceutical and biomanufacturing ecosystem across the U.S. and Canada, supported by strong government funding and favorable regulatory frameworks.

- Significant public investments such as U.S. initiatives to expand biological manufacturing and COVID-19 vaccine development have accelerated adoption of single-use technologies. High R&D activity in biologics, cell and gene therapies, along with rapid vaccine production needs, further boosts demand. Additionally, strong collaboration between biotech firms and CDMOs, advanced infrastructure, and industry bodies like BPSA reinforce regional growth.

Single-use Bioprocessing Market Active Players:

- AmplifyBio (United States)

- Avantor, Inc. (United States)

- Corning Incorporated (United States)

- Danaher Corporation (United States)

- Eppendorf AG (Germany)

- Getinge (Applikon Biotechnology) (Sweden)

- Lonza (Switzerland)

- Merck KGaA (Germany)

- PBS Biotech, Inc. (United States)

- Sartorius AG (Germany)

- Sartorius Stedim Biotech (France)

- Sphere Bio (United Kingdom)

- Takara Bio (Japan)

- Thermo Fisher Scientific, Inc. (United States)

- WuXi Biologics (China)

- Other Active Players

Key Industry Developments in the Single-use Bioprocessing Market:

- In June 2025, Sphere Bio broadened its footprint in China through a new distribution agreement. The partnership was formed with Redbert Biotechnology. It focuses on commercializing picodroplet microfluidics for single-cell analysis.

- In May 2025, WuXi Biologics successfully completed its first commercial PPQ campaign. The run utilized three 5,000 L single-use bioreactors at its Hangzhou facility. The company reported a 70% reduction in protein production costs.

Design Architecture and Modular Configuration of Disposable Systems

- Single-use bioprocessing refers to manufacturing systems that utilize disposable components such as bioreactor bags, tubing, connectors, filters, sensors, and mixing systems in place of traditional stainless-steel equipment. These systems are primarily fabricated from multilayer polymer films engineered for chemical resistance, low extractables, and mechanical integrity. Single-use bioreactors support batch, fed-batch, and perfusion modes, with working volumes ranging from small-scale process development to commercial production exceeding 5,000 liters.

- Integration of single-use sensors for pH, dissolved oxygen, and temperature enables real-time monitoring and closed-loop process control. Modular upstream and downstream assemblies facilitate rapid configuration changes, minimize cleaning and sterilization requirements, and reduce contamination risks. Advanced disposable downstream solutions, including membrane adsorbers and single-pass tangential-flow filtration, are increasingly replacing resin-based systems. Overall, single-use technologies provide scalable, flexible, and efficient manufacturing platforms for biologics, vaccines, and advanced therapies.

|

Single-use Bioprocessing Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 31.80 Bn. |

|

Forecast Period 2025-32 CAGR: |

13.7 % |

Market Size in 2035: |

USD 130.55 Bn. |

|

Segments Covered: |

By Product |

|

|

|

By Application

|

|

||

|

By Workflow |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Single-use Bioprocessing Market by Product (2018-2035)

4.1 Single-use Bioprocessing Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Filtration Assemblies

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Disposable Bioreactors

4.5 Disposable Mixers

4.6 Media Bags and Containers

4.7 and Others

Chapter 5: Single-use Bioprocessing Market by Application (2018-2035)

5.1 Single-use Bioprocessing Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Filtration

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Purification

5.5 Cell Culture

5.6 and Others

Chapter 6: Single-use Bioprocessing Market by Workflow (2018-2035)

6.1 Single-use Bioprocessing Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Upstream Processing

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Fermentation

6.5 and Downstream Processing

Chapter 7: Single-use Bioprocessing Market by End User (2018-2035)

7.1 Single-use Bioprocessing Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Biopharmaceutical Companies

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Clinical & Academic Research Institutes

7.5 and Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Single-use Bioprocessing Market Share by Manufacturer/Service Provider(2024)

8.1.3 Industry BCG Matrix

8.1.4 PArtnerships, Mergers & Acquisitions

8.2 AMPLIFYBIO (UNITED STATES)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 AVANTOR

8.4 INC. (UNITED STATES)

8.5 CORNING INCORPORATED (UNITED STATES)

8.6 DANAHER CORPORATION (UNITED STATES)

8.7 EPPENDORF AG (GERMANY)

8.8 GETINGE – APPLIKON BIOTECHNOLOGY (SWEDEN)

8.9 LONZA (SWITZERLAND)

8.10 MERCK KGAA (GERMANY)

8.11 PBS BIOTECH

8.12 INC. (UNITED STATES)

8.13 SARTORIUS AG (GERMANY)

8.14 SARTORIUS STEDIM BIOTECH (FRANCE)

8.15 SPHERE BIO (UNITED KINGDOM)

8.16 TAKARA BIO (JAPAN)

8.17 THERMO FISHER SCIENTIFIC

8.18 INC. (UNITED STATES)

8.19 WUXI BIOLOGICS (CHINA)

8.20 AND OTHER ACTIVE PLAYERS.

Chapter 9: Global Single-use Bioprocessing Market By Region

9.1 Overview

9.2. North America Single-use Bioprocessing Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.2.4.1 US

9.2.4.2 Canada

9.2.4.3 Mexico

9.3. Eastern Europe Single-use Bioprocessing Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.3.4.1 Russia

9.3.4.2 Bulgaria

9.3.4.3 The Czech Republic

9.3.4.4 Hungary

9.3.4.5 Poland

9.3.4.6 Romania

9.3.4.7 Rest of Eastern Europe

9.4. Western Europe Single-use Bioprocessing Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.4.4.1 Germany

9.4.4.2 UK

9.4.4.3 France

9.4.4.4 The Netherlands

9.4.4.5 Italy

9.4.4.6 Spain

9.4.4.7 Rest of Western Europe

9.5. Asia Pacific Single-use Bioprocessing Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.5.4.1 China

9.5.4.2 India

9.5.4.3 Japan

9.5.4.4 South Korea

9.5.4.5 Malaysia

9.5.4.6 Thailand

9.5.4.7 Vietnam

9.5.4.8 The Philippines

9.5.4.9 Australia

9.5.4.10 New Zealand

9.5.4.11 Rest of APAC

9.6. Middle East & Africa Single-use Bioprocessing Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.6.4.1 Turkiye

9.6.4.2 Bahrain

9.6.4.3 Kuwait

9.6.4.4 Saudi Arabia

9.6.4.5 Qatar

9.6.4.6 UAE

9.6.4.7 Israel

9.6.4.8 South Africa

9.7. South America Single-use Bioprocessing Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

9.7.4.1 Brazil

9.7.4.2 Argentina

9.7.4.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

Chapter 11 Our Thematic Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12 Case Study

Chapter 13 Appendix

13.1 Sources

13.2 List of Tables and figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Single-use Bioprocessing Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 31.80 Bn. |

|

Forecast Period 2025-32 CAGR: |

13.7 % |

Market Size in 2035: |

USD 130.55 Bn. |

|

Segments Covered: |

By Product |

|

|

|

By Application

|

|

||

|

By Workflow |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||