Key Market Highlights

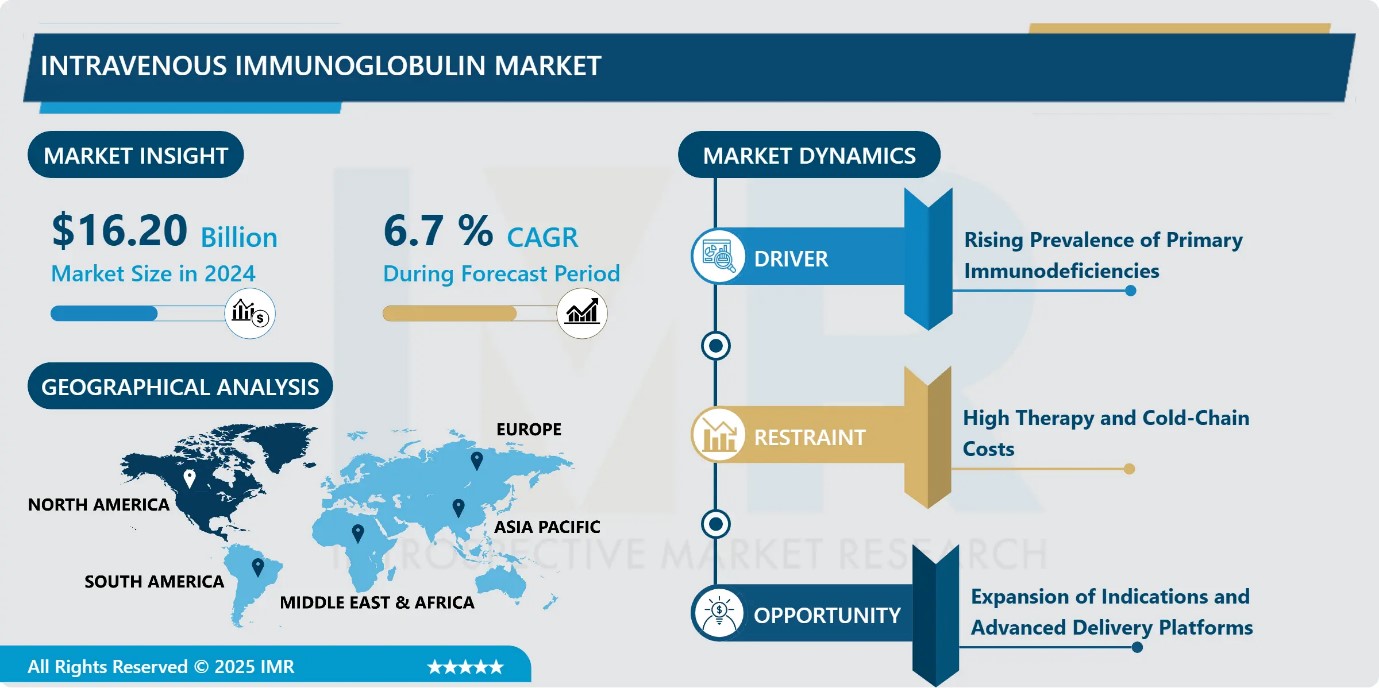

Intravenous Immunoglobulin Market Size Was Valued at USD 16.20 Billion in 2024, and is Projected to Reach USD 33.06 Billion by 2035, Growing at a CAGR of 6.7% from 2025-2035.

- Market Size in 2024: USD 16.20 Billion

- Projected Market Size by 2035: USD 33.06 Billion

- CAGR (2025–2035): 6.7%

- Leading Market in 2024: North America

- Fastest-Growing Market: Asia Pacific

- By Antibody Type: The IgG segment is anticipated to lead the market by accounting for 27.2% of the market share throughout the forecast period.

- By End User: The Hospitals segment is expected to capture 38.5% of the market share, thereby maintaining its dominance over the forecast period.

- By Region: North America region is projected to hold 32.6% of the market share during the forecast period.

- Active Players: ADMA Biologics, Inc. (United States), Baxter International Inc. (United States), BDI Pharma Inc. (United States), Bio Products Laboratory (BPL) (United Kingdom), and Other Active Players.

Intravenous Immunoglobulin Market Synopsis:

The Intravenous Immunoglobulin (IVIG) market is defined by the growing need for effective treatment of primary and acquired immunodeficiency disorders, where IVIG serves as the standard and often only therapeutic option. Rising incidence of immune-related conditions, driven by genetic factors and lifestyle-associated health disorders, is increasing dependence on IVIG therapies. Millions of individuals worldwide are affected by primary immunodeficiencies, many of whom remain undiagnosed, highlighting significant unmet medical need. Improved disease awareness, better diagnostic rates, and advancements in plasma collection and manufacturing are strengthening market demand. However, the market is challenged by high treatment costs, as IVIG requires frequent, long-term infusions, placing a substantial financial burden on patients and healthcare systems despite its clinical necessity.

Intravenous Immunoglobulin Market Dynamics and Trend Analysis:

Intravenous Immunoglobulin Market Growth Driver-Rising Prevalence of Primary Immunodeficiencies

- The increasing prevalence of primary immunodeficiency disorders (PIDs) globally is a major driver of the intravenous immunoglobulin (IVIG) market, as these lifelong genetic conditions require continuous immunoglobulin replacement to prevent recurrent and severe infections. Improved diagnostic capabilities, including expanded newborn screening programs, have enabled earlier detection, significantly enlarging the treated patient population. Clinical guidelines widely recognize IVIG as a first-line therapy, reinforcing its routine use in standard care. In response, manufacturers are expanding production capacity and developing high-purity formulations to meet long-term demand, ensuring sustained market growth and stability.

Intravenous Immunoglobulin Market Limiting Factor-High Therapy and Cold-Chain Costs

- The high cost associated with intravenous immunoglobulin (IVIG) therapy remains a significant restraint on market growth. A single treatment course can cost between USD 5,000 and 10,000, with patients often requiring ongoing infusions every three to four weeks, resulting in substantial annual expenditures. Additional financial burden arises from stringent cold-chain storage and transportation requirements, further increasing overall treatment costs. In resource-limited regions, these factors restrict accessibility and adoption. Moreover, complex reimbursement processes and prior authorization requirements delay therapy initiation, limiting market penetration and constraining short-term volume growth despite strong clinical demand.

Intravenous Immunoglobulin Market Expansion Opportunity-Expansion of Indications and Advanced Delivery Platforms

- The intravenous immunoglobulin (IVIG) market presents strong growth opportunities driven by expanding therapeutic indications and advancements in delivery technologies. Regulatory approvals for higher-dose subcutaneous immunoglobulin therapies enable flexible, home-based administration, improving patient adherence and reducing hospital burden. Innovations in plasma fractionation, purification, and recombinant technologies enhance product yield, safety, and efficacy, supporting the development of next-generation immunoglobulin therapies.

- Ongoing research is broadening IVIG use into additional neurological and autoimmune disorders, expanding the addressable patient population. Harmonized regulatory pathways, improved reimbursement integration, and patient-centric delivery models collectively create favorable conditions for sustained market expansion and portfolio diversification.

Intravenous Immunoglobulin Market Challenge and Risk-Risk of Pathogen Transmission

- As a plasma-derived blood product, intravenous immunoglobulin (IVIG) carries an inherent risk of transmitting viral infectious agents, which remains a key market challenge despite significant safety advancements. Although only rare cases of transmission, such as hepatitis C in earlier decades, have been reported, ongoing concerns persist among regulators, providers, and patients. These risks necessitate stringent donor screening, complex viral inactivation processes, and rigorous quality controls, increasing production complexity and costs. While IVIG plays a critical role in providing passive immunity for immune-compromised patients, heightened safety scrutiny can slow regulatory approvals and influence prescribing decisions, particularly in sensitive or high-risk populations.

Intravenous Immunoglobulin Market Trend-Advancements in IVIG Production Technologies

- Advancements in IVIG production technologies are playing a crucial role in driving market growth by improving manufacturing efficiency and product quality. Innovations in plasma fractionation, purification, and viral inactivation processes have resulted in higher yields and enhanced safety profiles. These improvements help reduce production costs while ensuring consistent availability of IVIG products. Reliable supply and superior quality increase clinician confidence and encourage broader adoption across multiple therapeutic applications. Additionally, modern manufacturing technologies enable scalability to meet rising global demand, supporting long-term market expansion and strengthening the overall competitiveness of the intravenous immunoglobulin market.

Intravenous Immunoglobulin Market Segment Analysis:

Intravenous Immunoglobulin Market is segmented based on into Antibody Type, Product Type, Source, Application, End Users, and Region.

By Antibody Type, IgG segment is expected to dominate the market with around 27.2% share during the forecast period.

- Immunoglobulin G (IgG) dominates the intravenous immunoglobulin market, accounting for the largest share in 2024 and demonstrating strong growth through 2035. Its dominance is driven by its essential role in both immune replacement therapy and immunomodulation across a wide range of autoimmune and inflammatory conditions. IgG’s long half-life, well-established clinical efficacy, and broad therapeutic applicability make it the preferred immunoglobulin class. Manufacturers continue to innovate through advanced purification processes that achieve high IgG purity and by developing high-concentration formulations that shorten infusion times, improve patient comfort, and reduce hospital burden. These factors collectively reinforce IgG’s sustained leadership in the IVIG market.

By End User, Hospitals is expected to dominate with close to 38.5% market share during the forecast period.

- Hospitals led the global intravenous immunoglobulin (IVIG) market in 2024, accounting for nearly half of total revenue, driven by advanced infrastructure, strong capital investment, and favorable reimbursement frameworks. Their ability to manage complex infusion protocols and treat high-acuity immunological and neurological conditions positions hospitals as the primary care setting for IVIG administration.

- Multidisciplinary medical teams enable close monitoring, rapid dose adjustments, and effective management of adverse reactions. Additionally, hospital participation in clinical trials supports early access to innovative therapies. Hospitals dominate the market because they are uniquely equipped to handle severe cases requiring structured administration and comprehensive clinical oversight.

Intravenous Immunoglobulin Market Regional Insights:

North America region is estimated to lead the market with around 38.5% share during the forecast period.

- North America held the dominant share of the global Intravenous Immunoglobulin (IVIG) market in 2024, driven by strong demand for immunomodulatory therapies to manage autoimmune disorders and primary immunodeficiencies within an aging population. The region benefits from a well-established healthcare infrastructure, advanced plasma collection networks, and favorable reimbursement and regulatory policies that support widespread IVIG adoption.

- Ongoing capacity expansions by leading manufacturers, increased government and private investments, and a high volume of clinical trials further strengthen supply stability and innovation. High disease awareness, early diagnosis, precision dosing advancements, and integrated infusion delivery systems collectively explain North America’s continued dominance in the IVIG market.

Intravenous Immunoglobulin Market Active Players:

- ADMA Biologics, Inc. (United States)

- Baxter International Inc. (United States)

- BDI Pharma Inc. (United States)

- Bio Products Laboratory (BPL) (United Kingdom)

- Biotest AG (Germany)

- China Biologics Products Inc. (China)

- CSL Behring (Australia)

- Grifols S.A. (Spain)

- Intas Pharmaceuticals Ltd. (India)

- Kedrion Biopharma (Italy)

- LFB Biotechnologies (France)

- Octapharma AG (Switzerland)

- Pfizer Inc. (United States)

- Sanquin Plasma Products (Netherlands)

- Takeda Pharmaceutical Company Limited (Japan)

- Other Active Players

Key Industry Developments in the Intravenous Immunoglobulin Market:

- In March 2025, Grifols reported positive outcomes from its Phase 2/3 clinical trial. The study evaluated the safety and efficacy of its IVIG therapy in post-polio syndrome (PPS) patients.Results showed IVIG infusions significantly improved physical performance in PPS patients.

- In March 2024, Argenx SE announced that Japan’s Ministry of Health, Labour, and Welfare (MHLW) approved VYVGART (efgartigimod alfa). The approval covers intravenous (IV) administration. It is indicated for adult patients with primary immune thrombocytopenia (ITP).

Technological Innovations, Manufacturing Processes, and Advanced Formulations Shaping the Global Intravenous Immunoglobulin (IVIG) Market

- The intravenous immunoglobulin (IVIG) market is primarily driven by plasma-derived immunoglobulin G (IgG), which undergoes advanced fractionation and purification processes to ensure high purity, viral safety, and consistent efficacy. Manufacturing employs technologies such as cold ethanol fractionation, ion-exchange chromatography, and nanofiltration, complemented by viral inactivation steps like solvent-detergent treatment and pasteurization. Recent innovations include recombinant IgG production and high-concentration formulations that reduce infusion times and improve patient compliance. IVIG products are available in intravenous and subcutaneous formats, with liquid and lyophilized presentations tailored for diverse clinical requirements.

- Therapeutic applications span primary immunodeficiencies, autoimmune and inflammatory disorders, neurological conditions, and infectious disease management. Critical process parameters, including plasma donor selection, antibody titer consistency, and stability during cold-chain logistics, directly impact product quality. Regulatory frameworks enforce stringent batch testing, traceability, and pharmacovigilance, ensuring safety. Technological advancements in formulation and delivery systems are expanding indications, enabling decentralized administration, and optimizing the therapeutic index of IVIG therapies globally.

|

Intravenous Immunoglobulin Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 16.20 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.7% |

Market Size in 2035: |

USD 33.06 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Source

|

|

||

|

By Application

|

|

||

|

By End Users |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Intravenous Immunoglobulin Market by Antibody Type (2018-2035)

4.1 Intravenous Immunoglobulin Market Snapshot and Growth Engine

4.2 Market Overview

4.3 IgG

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 IgM

4.5 IgA

4.6 IgE

4.7 IgD

4.8 and Others

Chapter 5: Intravenous Immunoglobulin Market by Product Type (2018-2035)

5.1 Intravenous Immunoglobulin Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Intravenous Immunoglobulin

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Subcutaneous Immunoglobulin

5.5 Combination Therapies

5.6 Liquid

5.7 Lyophilized

5.8 and Others

Chapter 6: Intravenous Immunoglobulin Market by Source (2018-2035)

6.1 Intravenous Immunoglobulin Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Human Plasma

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Recombinant Techniques

6.5 and Others

Chapter 7: Intravenous Immunoglobulin Market by Application (2018-2035)

7.1 Intravenous Immunoglobulin Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Primary Immunodeficiency

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Hypogammaglobulinemia

7.5 Chronic Inflammatory Demyelinating Polyneuropathy (CIDP)

7.6 Myasthenia Gravis

7.7 Multifocal Motor Neuropathy (MMN)

7.8 Immune Thrombocytopenic Purpura (ITP)

7.9 Guillain-Barré Syndrome (GBS)

7.10 Autoimmune Disorders

7.11 Infectious Diseases

7.12 and Others

Chapter 8: Intravenous Immunoglobulin Market by End Users (2018-2035)

8.1 Intravenous Immunoglobulin Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Hospitals

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Specialty Clinics & Neurology Centers

8.5 Homecare

8.6 Pharmaceutical Companies

8.7 and Others

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Intravenous Immunoglobulin Market Share by Manufacturer/Service Provider(2024)

9.1.3 Industry BCG Matrix

9.1.4 PArtnerships, Mergers & Acquisitions

9.2 ADMA BIOLOGICS

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Recent News & Developments

9.2.10 SWOT Analysis

9.3 INC. (UNITED STATES)

9.4 BAXTER INTERNATIONAL INC. (UNITED STATES)

9.5 BDI PHARMA INC. (UNITED STATES)

9.6 BIO PRODUCTS LABORATORY (BPL) (UNITED KINGDOM)

9.7 BIOTEST AG (GERMANY)

9.8 CHINA BIOLOGICS PRODUCTS INC. (CHINA)

9.9 CSL BEHRING (AUSTRALIA)

9.10 GRIFOLS S.A. (SPAIN)

9.11 INTAS PHARMACEUTICALS LTD. (INDIA)

9.12 KEDRION BIOPHARMA (ITALY)

9.13 LFB BIOTECHNOLOGIES (FRANCE)

9.14 OCTAPHARMA AG (SWITZERLAND)

9.15 PFIZER INC. (UNITED STATES)

9.16 SANQUIN PLASMA PRODUCTS (NETHERLANDS)

9.17 TAKEDA PHARMACEUTICAL COMPANY LIMITED (JAPAN)

9.18 AND OTHER ACTIVE PLAYERS.

Chapter 10: Global Intravenous Immunoglobulin Market By Region

10.1 Overview

10.2. North America Intravenous Immunoglobulin Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecast Market Size by Country

10.2.4.1 US

10.2.4.2 Canada

10.2.4.3 Mexico

10.3. Eastern Europe Intravenous Immunoglobulin Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecast Market Size by Country

10.3.4.1 Russia

10.3.4.2 Bulgaria

10.3.4.3 The Czech Republic

10.3.4.4 Hungary

10.3.4.5 Poland

10.3.4.6 Romania

10.3.4.7 Rest of Eastern Europe

10.4. Western Europe Intravenous Immunoglobulin Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecast Market Size by Country

10.4.4.1 Germany

10.4.4.2 UK

10.4.4.3 France

10.4.4.4 The Netherlands

10.4.4.5 Italy

10.4.4.6 Spain

10.4.4.7 Rest of Western Europe

10.5. Asia Pacific Intravenous Immunoglobulin Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecast Market Size by Country

10.5.4.1 China

10.5.4.2 India

10.5.4.3 Japan

10.5.4.4 South Korea

10.5.4.5 Malaysia

10.5.4.6 Thailand

10.5.4.7 Vietnam

10.5.4.8 The Philippines

10.5.4.9 Australia

10.5.4.10 New Zealand

10.5.4.11 Rest of APAC

10.6. Middle East & Africa Intravenous Immunoglobulin Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecast Market Size by Country

10.6.4.1 Turkiye

10.6.4.2 Bahrain

10.6.4.3 Kuwait

10.6.4.4 Saudi Arabia

10.6.4.5 Qatar

10.6.4.6 UAE

10.6.4.7 Israel

10.6.4.8 South Africa

10.7. South America Intravenous Immunoglobulin Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecast Market Size by Country

10.7.4.1 Brazil

10.7.4.2 Argentina

10.7.4.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

Chapter 12 Our Thematic Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

Chapter 13 Case Study

Chapter 14 Appendix

14.1 Sources

14.2 List of Tables and figures

14.3 Short Forms and Citations

14.4 Assumption and Conversion

14.5 Disclaimer

|

Intravenous Immunoglobulin Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 16.20 Bn. |

|

Forecast Period 2025-32 CAGR: |

6.7% |

Market Size in 2035: |

USD 33.06 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Source

|

|

||

|

By Application

|

|

||

|

By End Users |

|

||

|

By Region |

|

||

|

Growth Driver: |

|

||

|

Limiting Factor |

|

||

|

Expansion Opportunity |

|

||

|

Challenge and Risk |

|

||

|

Companies Covered in the Report: |

|

||