Software Asset Management Market Synopsis

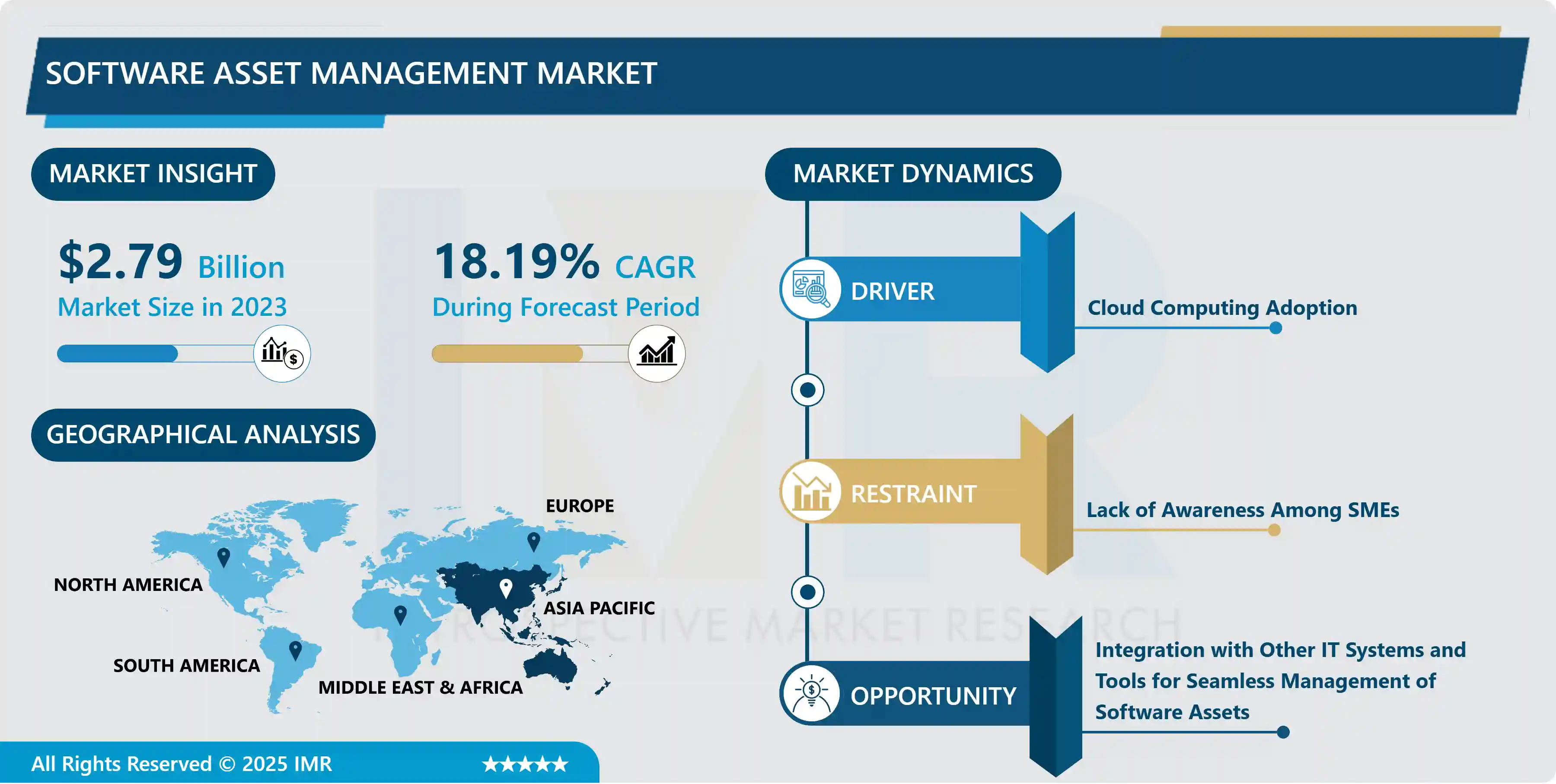

Software Asset Management Market Size Was Valued at USD 2.79 Billion in 2023 and is Projected to Reach USD 12.56 Billion by 2032, Growing at a CAGR of 18.19% From 2024-2032

Software Asset Management (SAM) refers to the process of managing and optimizing an organization's software assets throughout their lifecycle. This includes the procurement, deployment, utilization, and retirement of software to maximize value, minimize risks, and ensure compliance with licensing agreements. SAM involves tracking software licenses, usage, and entitlements to enhance cost efficiency, security, and governance. Key objectives of SAM include reducing software spending by identifying unused or underutilized licenses, ensuring compliance with vendor agreements and regulatory requirements, and mitigating security risks associated with unauthorized or outdated software installations. Effective SAM practices enable organizations to make informed decisions regarding software investments, streamline operations, and maintain a comprehensive view of their software landscape for improved governance and strategic planning. The SAM market encompasses a range of solutions and services aimed at supporting organizations in these efforts, providing tools for inventory management, license optimization, compliance reporting, and software lifecycle management.

The Software Asset Management (SAM) market is experiencing robust growth driven by increasing demand for optimizing software usage and reducing compliance risks. SAM solutions enable organizations to effectively manage software licenses, track usage, and ensure compliance with licensing agreements. As businesses increasingly rely on a diverse range of software applications, SAM tools provide critical insights into license utilization, helping companies optimize costs and streamline operations.

Key drivers fueling the expansion of the SAM market include stringent regulatory requirements, such as GDPR and HIPAA, which emphasize the need for accurate software inventory and compliance. Additionally, the rise of cloud computing and virtualization has further complicated license management, making SAM solutions essential for maintaining governance and controlling software expenditures.

Large enterprises are the primary adopters of SAM solutions due to their complex IT environments and extensive software portfolios. However, small and medium-sized enterprises (SMEs) are increasingly recognizing the benefits of SAM in controlling costs and ensuring legal compliance. As a result, vendors are developing tailored solutions to cater to the unique needs of SMEs, driving further market growth.

The SAM market is characterized by intense competition, with major players investing in innovative technologies such as artificial intelligence (AI) and machine learning (ML) to enhance SAM capabilities. These advancements enable real-time monitoring, predictive analytics, and automated compliance reporting, empowering organizations to proactively manage software assets.

Geographically, North America and Europe lead the SAM market, owing to stringent compliance regulations and high IT spending. However, rapid digitization in emerging economies like Asia-Pacific is fueling SAM adoption, presenting lucrative growth opportunities for market players.

In summary, the SAM market is poised for continued expansion as organizations prioritize cost optimization, compliance, and operational efficiency in an increasingly complex software landscape. Vendors are expected to focus on enhancing product capabilities and expanding their global footprint to capitalize on growing demand for robust software asset management solutions.

Software Asset Management Market Trend Analysis

Evolving Challenges and Opportunities in Cloud-Based Software Asset Management

- Cloud computing and subscription models have significantly transformed the landscape of Software Asset Management (SAM) by introducing new challenges and opportunities for organizations. As cloud technologies continue to dominate IT infrastructure, businesses are increasingly adopting multi-cloud environments, utilizing various cloud platforms for different applications and services. This diversity presents SAM with the complex task of managing software assets across these disparate cloud environments efficiently. SAM strategies now need to accommodate different licensing models and billing structures from different cloud providers, ensuring compliance and cost optimization across the board.

- Moreover, the proliferation of Software as a Service (SaaS) applications has led to a phenomenon known as SaaS sprawl, where organizations accumulate numerous subscriptions across departments. This widespread adoption of SaaS solutions introduces challenges related to subscription management, cost control, and compliance monitoring. SAM tools are evolving to address these challenges by providing robust capabilities for software discovery, optimization, and metering in SaaS environments. Organizations are prioritizing the optimization of subscriptions, identifying redundant or underutilized licenses, and ensuring license portability between on-premises and cloud infrastructures. SAM is becoming a critical component in managing the lifecycle of software assets in a cloud-centric IT ecosystem, enabling organizations to maximize value from their software investments while maintaining compliance and efficiency.

- In summary, cloud computing and subscription models are reshaping SAM practices by necessitating a comprehensive approach to managing software assets across diverse cloud platforms. This shift requires organizations to invest in SAM solutions that can seamlessly handle the complexities of SaaS sprawl, optimize subscription usage, and ensure license portability between on-premises and cloud environments. By leveraging advanced SAM strategies and tools, businesses can navigate the challenges of modern cloud-based IT environments effectively, enabling cost savings, compliance assurance, and enhanced operational efficiency across their software assets.

Cybersecurity Integration

- In the realm of Software Asset Management (SAM), the integration with cybersecurity strategies has become essential to mitigate risks associated with outdated or unauthorized software. SAM plays a critical role in identifying potential security vulnerabilities within software assets by conducting continuous monitoring and discovery across an organization's IT infrastructure. By maintaining an up-to-date inventory of software applications and versions, SAM tools can swiftly detect outdated or unpatched software components that may pose security risks. This proactive approach allows organizations to prioritize patching and updates based on criticality, reducing the window of exposure to potential threats and enhancing overall cybersecurity posture.

- Moreover, SAM is instrumental in automating patching and vulnerability scanning processes, further strengthening cybersecurity defenses. Automated patch management capabilities enable SAM tools to deploy security patches promptly across the organization's software assets, reducing the risk of exploitation by cyber attackers. Additionally, vulnerability scanning functionalities integrated into SAM solutions enable organizations to proactively identify and address software vulnerabilities before they can be exploited. By leveraging SAM for automated patching and vulnerability management, organizations can streamline security operations, improve incident response readiness, and mitigate the impact of cybersecurity threats on their IT environments.

- In summary, the integration of SAM with cybersecurity strategies represents a proactive approach to software asset management, focusing on identifying and mitigating security risks associated with software assets. By automating patching and vulnerability scanning processes, SAM empowers organizations to enhance their cybersecurity posture, reduce security vulnerabilities, and strengthen overall resilience against cyber threats. This integration underscores the importance of SAM as a strategic component of comprehensive cybersecurity frameworks, enabling organizations to maintain software compliance, minimize security risks, and safeguard critical IT assets effectively.

Software Asset Management Market Segment Analysis:

Market Name Market Segmented based on By Component, By deployment model, By organization size and By Vertical.

By Component, Solutions segment is expected to dominate the market during the forecast period

- Endpoint security and SIEM (Security Information and Event Management) solutions stand out as critical components within the cybersecurity landscape. Endpoint security focuses on protecting individual devices such as desktops, laptops, smartphones, and other endpoints from various cyber threats. With the proliferation of remote work and the growing number of devices connected to corporate networks, the demand for robust endpoint security solutions has soared. These solutions typically include antivirus software, firewalls, intrusion detection systems, and endpoint detection and response (EDR) tools, all aimed at safeguarding endpoints against malware, ransomware, and unauthorized access.

- On the other hand, SIEM solutions play a pivotal role in monitoring and analyzing security events and incidents across an organization's IT infrastructure. They aggregate and correlate data from various sources like network logs, system logs, and application logs to detect suspicious activities and potential security breaches. SIEM platforms provide real-time visibility into security events, enabling rapid incident response and threat mitigation. They are especially crucial for large enterprises with complex IT environments, where managing and interpreting security logs and alerts manually would be challenging. Due to their effectiveness in threat detection and compliance management, SIEM solutions hold a significant share of the cybersecurity market, driven by the continuous need to strengthen security postures and comply with regulatory requirements.

- In addition to solutions, managed security services (MSS) have become increasingly popular among organizations seeking to enhance their cybersecurity capabilities. Managed security services encompass a range of outsourced security offerings, including continuous monitoring, threat intelligence, incident response, and vulnerability management. MSS providers leverage specialized expertise and advanced tools to detect, analyze, and respond to cyber threats on behalf of their clients. This approach enables organizations to offload the complexities of cybersecurity operations to dedicated security professionals, allowing internal teams to focus on core business activities. The MSS market is expanding rapidly as businesses recognize the benefits of partnering with experienced security providers to mitigate risks and stay ahead of cyber adversaries in today's dynamic threat landscape.

By Vertical, IT and ITeS segment held the largest share in 2023

- The Information Technology and IT-enabled Services (ITeS) sector stands as a cornerstone of modern industry, wielding substantial influence and market impact globally. This sector's significance lies in its ability to catalyze digital transformation across various domains, from finance and healthcare to manufacturing and retail. IT and ITeS encompass a vast array of services, including software development, cybersecurity, cloud computing, and IT consulting. Businesses rely on these services to optimize processes, leverage data analytics for informed decision-making, and enhance customer experiences through digital platforms. As technology continues to evolve, the demand for IT solutions grows unabated, fueling innovation and driving efficiency across the business landscape.

- A defining characteristic of the IT and ITeS sector is its dynamic nature, characterized by rapid innovation and adaptation to emerging technologies. Artificial intelligence (AI), blockchain, Internet of Things (IoT), and machine learning are reshaping industry paradigms, with IT companies at the forefront of these advancements. Moreover, major global players in the IT sector serve as catalysts for technological progress, fostering collaborations with other industries and driving economic growth. The sector's resilience is evident in its ability to navigate disruptions such as the COVID-19 pandemic, where remote work and digital solutions became indispensable overnight. Moving forward, IT and ITeS will continue to play a pivotal role in shaping the future of work, commerce, and society as a whole, driving innovation and enabling businesses to thrive in an increasingly digital world.

Software Asset Management Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast period

- The Asia Pacific region is experiencing a significant surge in IT investments, particularly in countries like China, India, Japan, and South Korea. This increased investment is playing a crucial role in propelling the Software Asset Management (SAM) market forward. As organizations allocate more resources to enhance their digital infrastructure and IT capabilities, the need to efficiently manage software assets becomes paramount.

- One of the primary drivers behind the growing adoption of SAM solutions in the region is the increasing awareness of compliance and cost management among enterprises. Companies are becoming more cognizant of the risks associated with non-compliance, such as legal penalties and reputational damage. Therefore, there's a heightened emphasis on ensuring that software licenses are used in accordance with vendor agreements and regulatory requirements.

- Moreover, cost management is a key consideration for businesses in the Asia Pacific region. SAM solutions enable organizations to optimize their software usage, identify redundant licenses, and streamline procurement processes. By implementing SAM practices, enterprises can achieve substantial cost savings by eliminating unnecessary expenditures on software licenses and reducing the risk of overspending on IT resources.

- Furthermore, the complexities associated with managing software assets in large enterprises are driving the demand for SAM solutions. As businesses scale up their operations and adopt a diverse range of software applications, the need for centralized control and visibility over software assets becomes imperative. SAM tools provide organizations with the capability to efficiently track and manage their software inventory, ensuring that resources are utilized effectively and compliance obligations are met.

- In summary, the Asia Pacific region is witnessing a robust growth in IT investments, which in turn is fueling the demand for SAM solutions. The convergence of factors such as compliance awareness, cost management, and the need for efficient software asset management is driving enterprises to adopt comprehensive SAM strategies to optimize their IT operations and mitigate risks. This trend is expected to continue as businesses in the region prioritize digital transformation and seek to leverage technology to enhance operational efficiency and competitiveness.

Active Key Players in the Software Asset Management Market

- 1E

- Belarc

- BMC Software

- Broadcom

- Certero

- Eracent

- Flexera

- IBM

- InvGate

- Ivanti

- ManageEngine

- Matrix42

- Micro Focus

- Microsoft

- Open iT

- Scalable Software

- ServiceNow

- Snow Software

- Symphony SummitAI

- USU Software AG

- Xensam

- Other Key Players

Key Industry Developments in the Software Asset Management Market:

- In July 2021, Snow Software introduced Snow Atlas, the first integrated platform built to help organizations discover, monitor, and optimize their technology investments both on-premises and in the cloud. The first solutions available on the new cloud-native platform are SAM, SaaS management, and ITSM integrations which were earlier delivered as a service, are now in early access.

- In March 2021- Ivanti acquired Cherwell Software, a provider of service management solutions to enterprises. With the help of this acquisition, Ivanti aims to enlarge the range of its Neurons platform, that provides asset management and end-to-end service to IT businesses.

- In October 2020- ServiceNow partnered with IBM Corporation to help companies reduce operational risk at an affordable cost by applying artificial intelligence (AI) technology to automate IT operations.

|

Software Asset Management Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.79 Bn. |

|

Forecast Period 2024-32 CAGR: |

18.19% |

Market Size in 2032: |

USD 12.56 Bn. |

|

Segments Covered: |

By Component |

|

|

|

By Deployment Model |

|

||

|

By Organization Size |

|

||

|

By Vertical |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

Snow Software (Sweden), Flexera (US), USU Software AG (Germany), Ivanti (US), BMC Software (US), ServiceNow (US), Certero (UK), Matrix42 (Germany), Broadcom (US), Eracent (US), Scalable Software (US), Belarc (US), IBM (US), Micro Focus (UK), Microsoft (US), ManageEngine (US), Xensam (Sweden), InvGate (Argentina), Symphony SummitAI (US), 1E (UK), Open iT (US), Lansweeper (Belgium), and License Dashboard (UK) and Other Major Players. |

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Software Asset Management Market by Component (2018-2032)

4.1 Software Asset Management Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Solutions

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Services

Chapter 5: Software Asset Management Market by Deployment Model (2018-2032)

5.1 Software Asset Management Market Snapshot and Growth Engine

5.2 Market Overview

5.3 On-premises

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Cloud

Chapter 6: Software Asset Management Market by Organization Size (2018-2032)

6.1 Software Asset Management Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Large Enterprises

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 SMEs

Chapter 7: Software Asset Management Market by Vertical (2018-2032)

7.1 Software Asset Management Market Snapshot and Growth Engine

7.2 Market Overview

7.3 BFSI

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 IT and ITeS

7.5 Telecom

7.6 Manufacturing

7.7 Retail and eCommerce

7.8 Government

7.9 Healthcare and Life Sciences

7.10 Education

7.11 Media and Entertainment

7.12 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Software Asset Management Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 ABBOTT (U.S.)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 THE KRAFT HEINZ COMPANY (U.S.)

8.4 CARGILL INC. (U.S.)

8.5 MEAD JOHNSON & COMPANY

8.6 LLC. (U.S.)

8.7 SUN-MAID GROWERS OF CALIFORNIA (U.S.)

8.8 HIPP GMBH & CO. VERTRIEB KG (GERMANY)

8.9 PZ CUSSONS (U.K.)

8.10 RECKITT BENCKISER GROUP PLC (U.K)

8.11 BLEDINA SA (FRANCE)

8.12 DANONE SA (FRANCE)

8.13 NESTLE S.A. (SWITZERLAND)

8.14 HERO GROUP (SWITZERLAND)

8.15 ALTER S.L. (ITALY)

8.16 FRIESLANDCAMPINA (NETHERLANDS)

8.17 PERRIGO COMPANY PLC (IRELAND)

8.18 SEMPER AB (SWEDEN)

8.19 FEIHE INTERNATIONAL INC. (CHINA)

8.20 ASAHI GROUP HOLDINGS LTD. (JAPAN)

8.21 KEWPIE CORPORATION (JAPAN)

8.22 MORINAGA MILK INDUSTRY CO. LTD. (JAPAN)

8.23 BELLAMY’S ORGANIC (AUSTRALIA)

Chapter 9: Global Software Asset Management Market By Region

9.1 Overview

9.2. North America Software Asset Management Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Component

9.2.4.1 Solutions

9.2.4.2 Services

9.2.5 Historic and Forecasted Market Size by Deployment Model

9.2.5.1 On-premises

9.2.5.2 Cloud

9.2.6 Historic and Forecasted Market Size by Organization Size

9.2.6.1 Large Enterprises

9.2.6.2 SMEs

9.2.7 Historic and Forecasted Market Size by Vertical

9.2.7.1 BFSI

9.2.7.2 IT and ITeS

9.2.7.3 Telecom

9.2.7.4 Manufacturing

9.2.7.5 Retail and eCommerce

9.2.7.6 Government

9.2.7.7 Healthcare and Life Sciences

9.2.7.8 Education

9.2.7.9 Media and Entertainment

9.2.7.10 Others

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Software Asset Management Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Component

9.3.4.1 Solutions

9.3.4.2 Services

9.3.5 Historic and Forecasted Market Size by Deployment Model

9.3.5.1 On-premises

9.3.5.2 Cloud

9.3.6 Historic and Forecasted Market Size by Organization Size

9.3.6.1 Large Enterprises

9.3.6.2 SMEs

9.3.7 Historic and Forecasted Market Size by Vertical

9.3.7.1 BFSI

9.3.7.2 IT and ITeS

9.3.7.3 Telecom

9.3.7.4 Manufacturing

9.3.7.5 Retail and eCommerce

9.3.7.6 Government

9.3.7.7 Healthcare and Life Sciences

9.3.7.8 Education

9.3.7.9 Media and Entertainment

9.3.7.10 Others

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Software Asset Management Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Component

9.4.4.1 Solutions

9.4.4.2 Services

9.4.5 Historic and Forecasted Market Size by Deployment Model

9.4.5.1 On-premises

9.4.5.2 Cloud

9.4.6 Historic and Forecasted Market Size by Organization Size

9.4.6.1 Large Enterprises

9.4.6.2 SMEs

9.4.7 Historic and Forecasted Market Size by Vertical

9.4.7.1 BFSI

9.4.7.2 IT and ITeS

9.4.7.3 Telecom

9.4.7.4 Manufacturing

9.4.7.5 Retail and eCommerce

9.4.7.6 Government

9.4.7.7 Healthcare and Life Sciences

9.4.7.8 Education

9.4.7.9 Media and Entertainment

9.4.7.10 Others

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Software Asset Management Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Component

9.5.4.1 Solutions

9.5.4.2 Services

9.5.5 Historic and Forecasted Market Size by Deployment Model

9.5.5.1 On-premises

9.5.5.2 Cloud

9.5.6 Historic and Forecasted Market Size by Organization Size

9.5.6.1 Large Enterprises

9.5.6.2 SMEs

9.5.7 Historic and Forecasted Market Size by Vertical

9.5.7.1 BFSI

9.5.7.2 IT and ITeS

9.5.7.3 Telecom

9.5.7.4 Manufacturing

9.5.7.5 Retail and eCommerce

9.5.7.6 Government

9.5.7.7 Healthcare and Life Sciences

9.5.7.8 Education

9.5.7.9 Media and Entertainment

9.5.7.10 Others

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Software Asset Management Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Component

9.6.4.1 Solutions

9.6.4.2 Services

9.6.5 Historic and Forecasted Market Size by Deployment Model

9.6.5.1 On-premises

9.6.5.2 Cloud

9.6.6 Historic and Forecasted Market Size by Organization Size

9.6.6.1 Large Enterprises

9.6.6.2 SMEs

9.6.7 Historic and Forecasted Market Size by Vertical

9.6.7.1 BFSI

9.6.7.2 IT and ITeS

9.6.7.3 Telecom

9.6.7.4 Manufacturing

9.6.7.5 Retail and eCommerce

9.6.7.6 Government

9.6.7.7 Healthcare and Life Sciences

9.6.7.8 Education

9.6.7.9 Media and Entertainment

9.6.7.10 Others

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Software Asset Management Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Component

9.7.4.1 Solutions

9.7.4.2 Services

9.7.5 Historic and Forecasted Market Size by Deployment Model

9.7.5.1 On-premises

9.7.5.2 Cloud

9.7.6 Historic and Forecasted Market Size by Organization Size

9.7.6.1 Large Enterprises

9.7.6.2 SMEs

9.7.7 Historic and Forecasted Market Size by Vertical

9.7.7.1 BFSI

9.7.7.2 IT and ITeS

9.7.7.3 Telecom

9.7.7.4 Manufacturing

9.7.7.5 Retail and eCommerce

9.7.7.6 Government

9.7.7.7 Healthcare and Life Sciences

9.7.7.8 Education

9.7.7.9 Media and Entertainment

9.7.7.10 Others

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Software Asset Management Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 2.79 Bn. |

|

Forecast Period 2024-32 CAGR: |

18.19% |

Market Size in 2032: |

USD 12.56 Bn. |

|

Segments Covered: |

By Component |

|

|

|

By Deployment Model |

|

||

|

By Organization Size |

|

||

|

By Vertical |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

Snow Software (Sweden), Flexera (US), USU Software AG (Germany), Ivanti (US), BMC Software (US), ServiceNow (US), Certero (UK), Matrix42 (Germany), Broadcom (US), Eracent (US), Scalable Software (US), Belarc (US), IBM (US), Micro Focus (UK), Microsoft (US), ManageEngine (US), Xensam (Sweden), InvGate (Argentina), Symphony SummitAI (US), 1E (UK), Open iT (US), Lansweeper (Belgium), and License Dashboard (UK) and Other Major Players. |

||