Mobile Health Market Synopsis:

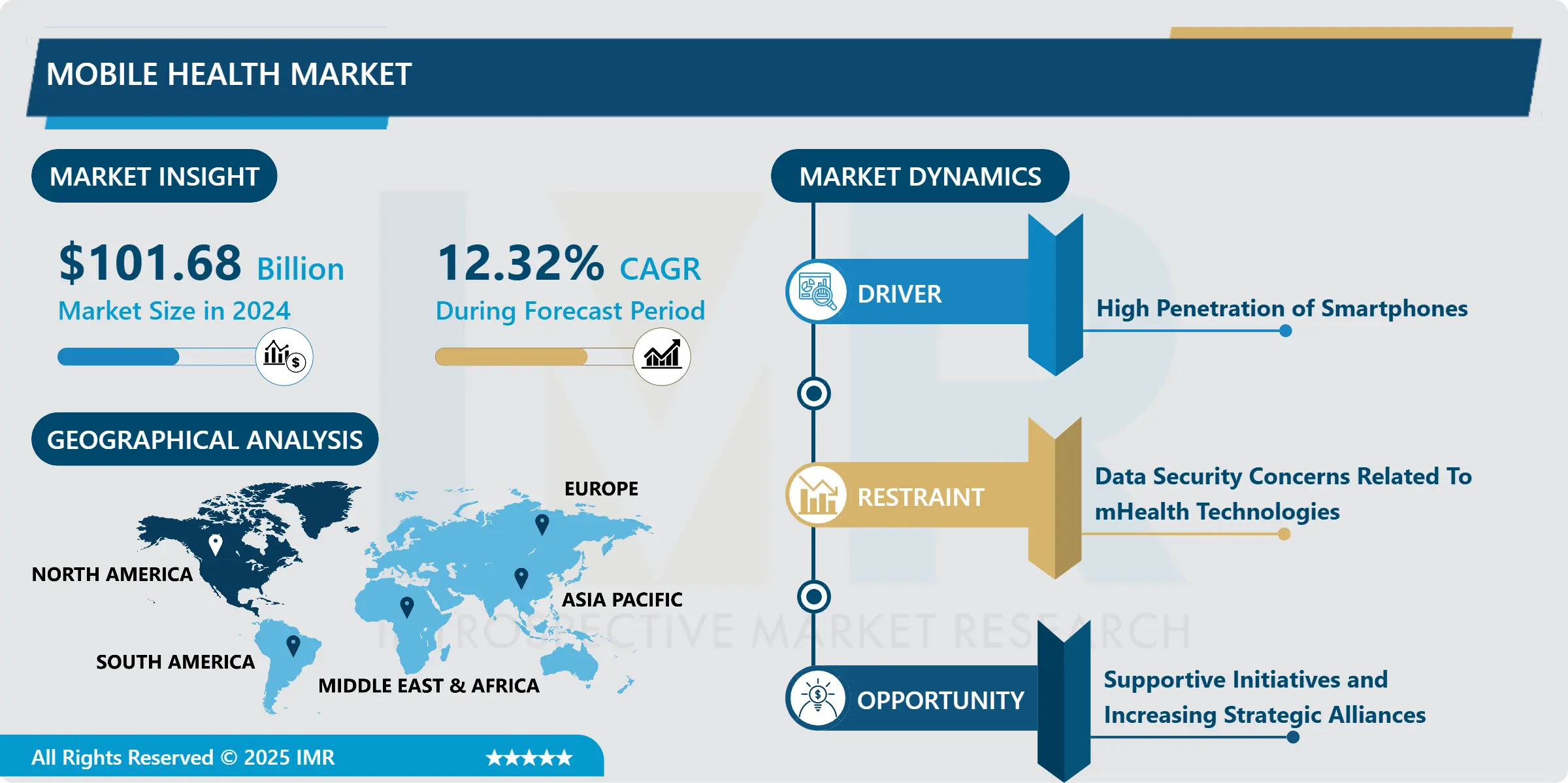

Mobile Health Market Size Was Valued at USD 101.68 Billion in 2024 and is Projected to Reach USD 364.98 Billion by 2035, Growing at a CAGR of 12.32% From 2025-2035.

A variety of medical and public health procedures facilitated by mobile devices, including smartphones, tablets, and wearable sensors, are included in the mobile health (mHealth) market. This market offers a range of applications that let consumers access healthcare services remotely and are made for wellness management, diagnosis, treatment, and health monitoring. Real-time patient data gathering, remote consultations, and tailored health management are made possible by mHealth technologies, which also help to reduce costs and enhance healthcare results. Advances in mobile technology, rising smartphone adoption, and an increasing focus on chronic illness management and preventative healthcare are driving the market's rise.

A growing emphasis on patient-centric treatment, rapid technological breakthroughs, and rising smartphone usage are driving a transformative phase in the mobile health (mHealth) business. This industry, which includes a variety of mobile-accessible health-related services and apps, has the potential to completely transform the healthcare system by lowering costs, increasing accessibility, and improving overall care quality.

The widespread use of smartphones and mobile apps has increased accessibility to healthcare services beyond previous levels. Since a sizable section of the world's population possesses a smartphone, mHealth solutions can reach a wide range of people, including those who live in remote and underserved locations. This accessibility is especially important in areas with poor healthcare infrastructure, as mobile health apps can offer vital services like information access, health monitoring, and remote consultations. Because of this, mHealth is essential in closing the gap between patients and healthcare professionals and guaranteeing that everyone, wherever, has access to high-quality care.

The mHealth market is expanding due to technological developments in mobile devices, wearable sensors, and communication networks. Mobile health applications are becoming more sophisticated and individualized thanks to the integration of innovations like artificial intelligence, machine learning, and the Internet of Things (IoT). By enabling automated medication and appointment reminders, real-time health monitoring, and predictive analytics, these technologies enhance patient outcomes while lessening the strain on healthcare institutions. Furthermore, the arrival of 5G technology is anticipated to augment the potential of mobile health applications by offering a quicker and more dependable connectivity, which is crucial for the smooth provision of digital health services.

The mHealth industry is expanding due to a number of important factors, one of which is the shift towards patient-centric treatment. The goal of contemporary healthcare systems is to enable people to actively participate in their own health management. Numerous tools for self-care are available through mobile health applications, including diet and nutrition apps, activity trackers, and mental health support systems. These apps give users insightful information about their health, empowering them to take control of their health and lead better lives. Additionally, by enabling patients to share data with healthcare practitioners and monitor their illnesses on a continual basis, mHealth solutions help manage chronic diseases by assuring prompt interventions and lowering readmission rates to hospitals.

The significant financial advantages of mHealth also play a role in its quick global adoption. mHealth applications assist cut healthcare expenditures for consumers and providers by eliminating the need for in-person consultations and hospital visits. For instance, telemedicine services allow for remote consultations, which relieve pressure on healthcare facilities while also saving time and money on trip. Additionally, by reducing administrative procedures and enabling better resource management, mobile health applications can increase operational efficiencies inside healthcare companies. The potential cost savings of mobile health (mHealth) provide a strong argument for its wider adoption since healthcare systems around the world are under increasing financial strain.

To reach its full potential, the mHealth sector needs to overcome a number of obstacles despite its many benefits. Concerns about data security and privacy are critical since health information is sensitive. Gaining patient trust and promoting the use of mHealth solutions depend on ensuring strong data privacy measures and meeting regulatory standards. In addition, the digital gap continues to be a major obstacle because not everyone has access to a smartphone or a dependable internet connection. Making efforts to improve digital literacy and increase connectivity in underserved areas is crucial to guaranteeing that the advantages of mobile health are shared fairly.

In summary, the market for mobile health is expanding at an astounding rate thanks to developments in technology, improved accessibility, and a move toward patient-centered treatment. Despite the need to address issues like data security and the digital divide, mHealth has the unquestionable potential to revolutionize healthcare delivery and enhance patient outcomes. Stakeholders must work together as the market develops to build a safe, inclusive, and technologically advanced mHealth environment that offers everyone access to high-quality, reasonably priced healthcare.

Mobile Health Market Trend Analysis:

Increasing Adoption of Smartphones and Mobile Devices in Healthcare

- The way that smartphones and other mobile devices are being used is drastically changing the healthcare industry. Smartphones are becoming more and more commonplace, and with them come useful tools for getting access to a variety of health-related apps and services. With features like appointment scheduling, medication reminders, and virtual consultations at their fingertips, these gadgets give consumers the ease of managing their health while on the road. Through the use of health-related applications, patients can connect with medical professionals directly, communicating with them, getting diagnostic services, and accessing medical records all without having to make in-person appointments. This accessibility is especially helpful in the management of chronic illnesses, when prompt actions and regular monitoring are essential.

- Furthermore, the increasing prevalence of mobile devices is narrowing the accessibility gap for healthcare, particularly in isolated and underprivileged areas. These areas have historically had difficulty getting access to high-quality healthcare because of infrastructure deficiencies in the medical field as well as geographic constraints. On the other hand, mobile health solutions allow medical professionals to access patients outside of cities. Patients in remote locations can get prescriptions filled, contact specialists, and even take part in health education initiatives by using mobile platforms. Furthermore, real-time data transmission to healthcare practitioners via mobile devices with health monitoring capabilities allows for remote diagnosis and ongoing health tracking. This guarantees prompt medical attention and gives patients the confidence to actively manage their health, which eventually improves health outcomes and lowers healthcare inequities.

Telemedicine's Ascent in the mHealth Sector

- In the mHealth industry, telemedicine has become a prominent trend that is transforming the provision of healthcare services. The COVID-19 pandemic significantly accelerated the uptake of telehealth services by emphasizing the necessity for social distancing and reducing in-person interactions. Patients can now obtain medical advice and treatment without leaving their homes thanks to virtual consultations, which have become a competitive alternative to regular office visits. This change decreased the strain on healthcare institutions, improving patient comfort while also lowering the danger of viral transmission and freeing up resources for essential in-person care. The pandemic proved telemedicine's usefulness and efficacy, which helped it gain traction and be incorporated into regular medical procedures.

- Consequently, there has been an upsurge in the creation of advanced telemedicine applications and platforms. These days, these technologies provide a plethora of features beyond simple video chats. For example, with connected devices and apps, users can obtain electronic prescriptions, get diagnoses remotely, and participate in ongoing health monitoring. Artificial intelligence (AI) and machine learning algorithms are also being integrated into telemedicine platforms in order to improve diagnosis precision and offer individualized treatment recommendations. Furthermore, by allowing for frequent remote check-ins and real-time health data sharing between patients and healthcare providers, these platforms can improve the management of chronic illnesses. Telemedicine has become a vital component of the contemporary mHealth ecosystem because to its all-encompassing approach, which not only improves patient outcomes but also boosts the overall efficiency of healthcare delivery.

Mobile Health Market Segment Analysis:

Mobile Health Market Segmented based on By Product and Service and By End User.

By Product and Service, mHealth Apps segment is expected to dominate the market with around 31.69% share during the forecast period.

- The main reasons why healthcare apps have such a strong market presence in the mHealth space are their accessibility and wide appeal. These applications address many different aspects of health and wellness, ranging from general wellbeing and mental health support to nutrition management and fitness tracking. For example, fitness tracking applications let users track their progress over time, create goals, and keep an eye on their physical activity levels. Nutrition applications include meal planning tools, calorie counters, and dietary guidance to assist users in maintaining good eating habits. Applications for mental health provide tools including stress reduction plans, meditation guidance, and online therapy. Through the integration of aspects from fitness, diet, and mental health into a single platform, general wellness apps offer a holistic approach to health. Healthcare apps' broad range of features and adaptability appeal to a wide range of users, which helps explain their dominant market position.

- The cost-effectiveness and user-friendliness of healthcare apps contribute to their widespread use. A wide range of people can use these applications because many of them are free or inexpensively priced. Because of their straightforward design, people of different ages and technological proficiency may utilize their features and navigate them with ease. Furthermore, healthcare applications provide prompt assistance and feedback, which is essential for sustaining user interest and encouraging healthy behaviors. For instance, a mental health app can provide quick relaxation techniques to help with stress, while a fitness app can give real-time information on steps walked and calories burned. These apps' promptness and ease of use align with the needs of contemporary users who seek dependable and expedient health management solutions. Because of this, millions of people's daily routines now include healthcare apps, which has cemented their dominance in the mHealth market.

By End User, Healthcare Payers segment is anticipated to account for around 30.11% market share during the upcoming years.

- In the mHealth market, healthcare payers—which include insurance companies, governments, and other organizations in charge of paying for medical services—are essential players. These institutions are responsible for controlling healthcare expenses and enhancing the efficacy and efficiency of service provision. Payers can impact healthcare outcomes and costs significantly by utilizing mHealth solutions. Payers may now deploy comprehensive patient monitoring systems, which are essential for managing chronic illnesses and guaranteeing continuity of care, thanks to mHealth technology. Real-time data on patient health indicators is provided by these systems, enabling prompt actions that can avert problems and hospital readmissions. Furthermore, by providing resources for early identification and health risk assessments, mHealth solutions aid preventative care programs and further lower the frequency of acute medical events and their related expenses.

- The ability to optimize healthcare spending and improve patient outcomes is what motivates healthcare payers to adopt mHealth services. By offering frequent check-ins and reminders, payers can enhance patient adherence to treatment plans through telehealth services and remote patient monitoring. Patients are better able to control their diseases thanks to this ongoing involvement, which lowers the need for ER visits and hospital admissions. Additionally, mHealth technology makes it easier for medical professionals to coordinate patient care, guaranteeing that patients receive thorough and coordinated care. In order to find opportunities for cost reductions and efficiency gains, healthcare trends can be examined using the data gathered through mHealth platforms. Healthcare payers can obtain a high return on investment by incorporating mHealth solutions into their operations, which will increase their share of these technologies' deployment in the mHealth market. In addition to improving patient care, this smart use of mHealth services helps keep healthcare systems financially viable.

Mobile Health Market Regional Insights:

North America market is estimated to maintain leadership with around 29.42% share across the forecast duration.

- The dominant shareholder in the worldwide mHealth market is expected to be North America, which is expected to grow at a CAGR of 15.8% during the course of the forecast year. mHealth services in North America are anticipated to be driven by factors like the quick adoption of smartphones, improvements in coverage networks, an increase in the prevalence of chronic illnesses, and a sharp rise in the senior population. In North America and Europe, one in four people may be 65 or older by the year 2050, according to the UN's World Population Ageing Report 2019. After Europe, it also boasts the second-largest aging population globally. The widespread use of mHealth is one of the main reasons driving this market's growth. According to the CDC, for example, 86.9% of doctors who practice in offices utilize at least one kind of electronic medical record (EMR) system.

- The market has also profited recently from a rise in product launches, mergers, and acquisitions. For example, Allscripts and Microsoft announced in July 2020 that they will be working together to develop cloud-based IT solutions. It is anticipated that this will assist the business in improving patient engagement through its healthcare technologies. Innovating and releasing new services and goods, the majority of major firms also make more investments in the North American market.

Active Key Players in the Mobile Health Market:

- AT&T,

- Samsung Electronics Co.,

- Allscripts Healthcare Solutions,

- Apple, Inc.,

- Airstrip Technologies, Inc.,

- Orange,

- mQure,

- Qualcomm, Inc.,

- Telefonica S.A.,

- SoftServe,

- Vodafone Group,

- Other Key Players

Key Industry Developments in the Mobile Health Market:

- In May 2025, Superpower acquired Base to boost its AI-doctor app capabilities. It had just raised about USD 30 million in Series A and is building a broad “health super-app” combining wearables, lab tests, nutrition, sleep, hormone optimization.

- In May 2025, This is a mobile-health product development story the startup is integrating hardware, testing, AI, and mobile app services to expand its offering.

(Source: https://www.businessinsider.com)

|

Mobile Health Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 101.68 Billion |

|

Forecast Period 2025-2035 CAGR: |

12.32% |

Market Size in 2035: |

USD 364.98 Billion |

|

Segments Covered: |

By Product and Service |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Mobile Health Market by Product and Service (2018-2032)

4.1 Mobile Health Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Introduction

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 mHealth Apps

4.5 Healthcare Apps

4.6 Medical Apps

4.7 Connected Medical devices

4.8 mHealth Services

Chapter 5: Mobile Health Market by End User (2018-2032)

5.1 Mobile Health Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Introduction

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Healthcare Providers

5.5 Healthcare Payers

5.6 Patients/Consumers

5.7 Other end users

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Mobile Health Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 AT&T SAMSUNG ELECTRONICS CO. ALLSCRIPTS HEALTHCARE SOLUTIONS APPLE INC. AIRSTRIP TECHNOLOGIES INC. ORANGE

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 MQURE QUALCOMM INC. TELEFONICA S.A. SOFTSERVE VODAFONE GROUP

6.4 OTHER KEY PLAYERS

Chapter 7: Global Mobile Health Market By Region

7.1 Overview

7.2. North America Mobile Health Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Product and Service

7.2.4.1 Introduction

7.2.4.2 mHealth Apps

7.2.4.3 Healthcare Apps

7.2.4.4 Medical Apps

7.2.4.5 Connected Medical devices

7.2.4.6 mHealth Services

7.2.5 Historic and Forecasted Market Size by End User

7.2.5.1 Introduction

7.2.5.2 Healthcare Providers

7.2.5.3 Healthcare Payers

7.2.5.4 Patients/Consumers

7.2.5.5 Other end users

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Mobile Health Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Product and Service

7.3.4.1 Introduction

7.3.4.2 mHealth Apps

7.3.4.3 Healthcare Apps

7.3.4.4 Medical Apps

7.3.4.5 Connected Medical devices

7.3.4.6 mHealth Services

7.3.5 Historic and Forecasted Market Size by End User

7.3.5.1 Introduction

7.3.5.2 Healthcare Providers

7.3.5.3 Healthcare Payers

7.3.5.4 Patients/Consumers

7.3.5.5 Other end users

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Mobile Health Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Product and Service

7.4.4.1 Introduction

7.4.4.2 mHealth Apps

7.4.4.3 Healthcare Apps

7.4.4.4 Medical Apps

7.4.4.5 Connected Medical devices

7.4.4.6 mHealth Services

7.4.5 Historic and Forecasted Market Size by End User

7.4.5.1 Introduction

7.4.5.2 Healthcare Providers

7.4.5.3 Healthcare Payers

7.4.5.4 Patients/Consumers

7.4.5.5 Other end users

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Mobile Health Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Product and Service

7.5.4.1 Introduction

7.5.4.2 mHealth Apps

7.5.4.3 Healthcare Apps

7.5.4.4 Medical Apps

7.5.4.5 Connected Medical devices

7.5.4.6 mHealth Services

7.5.5 Historic and Forecasted Market Size by End User

7.5.5.1 Introduction

7.5.5.2 Healthcare Providers

7.5.5.3 Healthcare Payers

7.5.5.4 Patients/Consumers

7.5.5.5 Other end users

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Mobile Health Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Product and Service

7.6.4.1 Introduction

7.6.4.2 mHealth Apps

7.6.4.3 Healthcare Apps

7.6.4.4 Medical Apps

7.6.4.5 Connected Medical devices

7.6.4.6 mHealth Services

7.6.5 Historic and Forecasted Market Size by End User

7.6.5.1 Introduction

7.6.5.2 Healthcare Providers

7.6.5.3 Healthcare Payers

7.6.5.4 Patients/Consumers

7.6.5.5 Other end users

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Mobile Health Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Product and Service

7.7.4.1 Introduction

7.7.4.2 mHealth Apps

7.7.4.3 Healthcare Apps

7.7.4.4 Medical Apps

7.7.4.5 Connected Medical devices

7.7.4.6 mHealth Services

7.7.5 Historic and Forecasted Market Size by End User

7.7.5.1 Introduction

7.7.5.2 Healthcare Providers

7.7.5.3 Healthcare Payers

7.7.5.4 Patients/Consumers

7.7.5.5 Other end users

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Mobile Health Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 101.68 Billion |

|

Forecast Period 2025-2035 CAGR: |

12.32% |

Market Size in 2035: |

USD 364.98 Billion |

|

Segments Covered: |

By Product and Service |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||