Digital Camera Market Synopsis

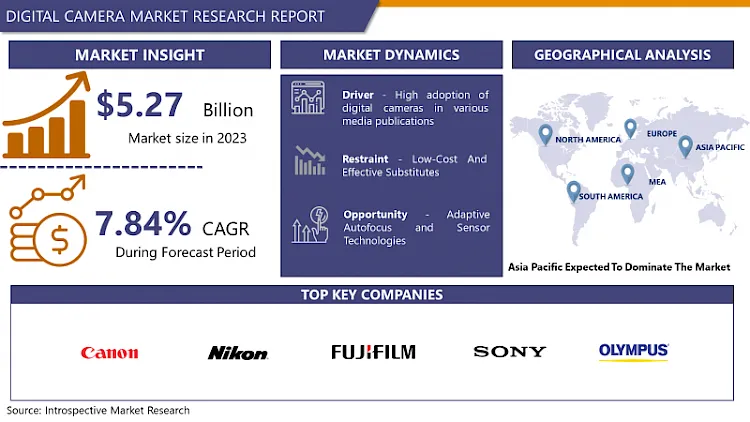

The global market for Digital cameras estimated at USD 5.27 Billion in the year 2023, is anticipated to reach USD 10.4 billion by 2032, growing at a CAGR of 7.84% over the period 2024-2032.

A digital camera is a camera that captures photographs in digital memory. Most cameras produced today are digital, largely replacing those that capture images on photographic film. Digital cameras are now widely incorporated into mobile devices like smartphones with the same or more capabilities and features of dedicated cameras (which are still available).

High-end, high-definition dedicated cameras are still commonly used by professionals and those who desire to take higher-quality photographs. Youngsters widely use digital cameras to capture classic and high-resolution photographs for their personal & professional usage. Mirrorless digital cameras are widely popular among film producers as they can efficiently capture high-resolution videos and images for their film shoots. Consumers largely seek to understand the various parameters such as device compactness, weight, cost, and resolution features of a particular digital camera during its buying process.

The Digital Camera Market Trend Analysis

The Digital Camera Market Trend Analysis

High adoption of digital cameras in various media publications

- The increasing use of digital cameras in sports media is the primary driver of the market. The stadium's high-speed and digital camera structure lets viewers see slow-motion repeats in critical game conditions and improves accuracy while watching. Similarly, high-resolution digital cameras aid in the capture of sharp and crisp images and videos in wildlife, landscape, architecture, and studio photography.

- The emphasis on action photography has increased demand for small digital cameras such as GoPro. Furthermore, social media platforms such as Instagram have significantly expanded the scope of photography, which is expected to drive the digital camera market's growth.

- The global digital camera market is experiencing robust growth driven by various factors, including the growing trend of photography, the use of cameras in entertainment, media, and sports industries, and the increasing number of social media small businesses worldwide. Digital cameras have become essential tools in these industries for both personal and professional photography

- The rising usage of digital cameras in sports media is the key driver of the market. The stadium's high-speed and digital camera system allows viewers to witness slow-motion repeats in critical game conditions and improves accuracy while viewing. Similarly, high-resolution digital cameras aid in the capture of clean and crisp photographs and movies in animal, landscape, architecture, and studio photography. The emphasis on action photography has raised the demand for small digital cameras such as GoPro. Furthermore, social media platforms such as Instagram have significantly enlarged the scope for photography, which is likely to drive the growth of the Digital Camera Market

Adaptive Autofocus and Sensor Technologies

- The photography industry is advancing rapidly, and the introduction of adaptive autofocus and sensor technologies will revolutionize the way to take pictures. Artificial intelligence and machine learning are used to enable autofocus systems to detect and track subjects in motion, making it easier to capture fast-moving objects.

- Additionally, the introduction of revolutionary sensors will allow for larger pixel sizes resulting in higher-resolution images and improved low-light performance. Combined with innovative camera technology, the future will undoubtedly bring ground-breaking advancements in photography.

- Autofocus technologies are one of the most important breakthroughs in the arena of digital photography and as well as digital image processing. Providing versatility and ease of use, autofocus technologies have put photography on digital cameras to a new dimension. However, in the state of the art, there are different focusing systems for digital autofocus in digital cameras.

- With the development of new technologies, photographers will be able to take more creative and stunning photographs and capture moments that have never been seen before. All in all, the future of photography is looking bright, and that can expect to be amazed by the amazing images that innovative camera technology can bring to the table in the future.

Segmentation Analysis of the Digital Camera Market

Digital Camera market segments cover the Product Type, Digital Sensor Type, Component, Distribution Channel, End-User, and Region. By Product Type, the Digital Single-Lens Reflex (DSLR) Cameras segment is anticipated to dominate the Market over the Forecast period.

- DSLR cameras typically deliver high-quality images due to their large image sensors, which capture more light and detail. This results in better low-light performance, lower noise, and a greater dynamic range compared to smaller-sensor cameras.

- DSLR cameras allow to use of a wide variety of lenses, enabling greater flexibility and creativity in photography. Consumers can choose from prime lenses, zoom lenses, and specialty lenses like macro or fisheye to achieve different effects and perspectives.

- Additionally, Digital Single-Lens Reflex (DSLR) offers extensive manual controls, allowing experienced photographers to fine-tune their settings to achieve the desired result. This includes control over the aperture, shutter speed, ISO, white balance, and more.

- DSLR cameras use an optical viewfinder, which shows the image as seen through the lens, providing a clear, real-time view of your subject. This can be advantageous in certain situations, such as bright sunlight, where it may be difficult to see the image on an electronic screen, these factors boost the Digital Single-Lens Reflex (DSLR) Cameras segment, and ultimately these factors boost the digital camera market.

Regional Analysis of the Digital Camera Market

Asia Pacific is expected to Dominate the Market over the Forecast period.

- Most of the world's leading electronics manufacturers, including camera makers, are based in countries within the Asia-Pacific region. Countries like Japan (home to companies like Canon, Nikon, and Sony), South Korea (Samsung), and China (various manufacturers) are known for their strong presence in the electronics industry.

- The Asia-Pacific region has been at the forefront of technological innovation in electronics, including digital cameras. Japanese companies, in particular, have a long history of innovation in the camera industry, consistently introducing new technologies and features that set trends globally.

- The region boasts a skilled workforce in the fields of electronics, engineering, and manufacturing. This pool of skilled labor contributes to the efficient production of high-quality digital cameras.

- The Camera & Imaging Products Association in Japan (CIPA) anticipates the production of 5.29 million mirrorless and DSLR devices in calendar 2022, whereas Nikon forecasts 5.1 million between April 2022 and March 2023.

- Furthermore, the rising number of destination and big wedding events in the Asia-Pacific region has resulted in a boom in demand for wedding photography, significantly impacting the digital camera market.

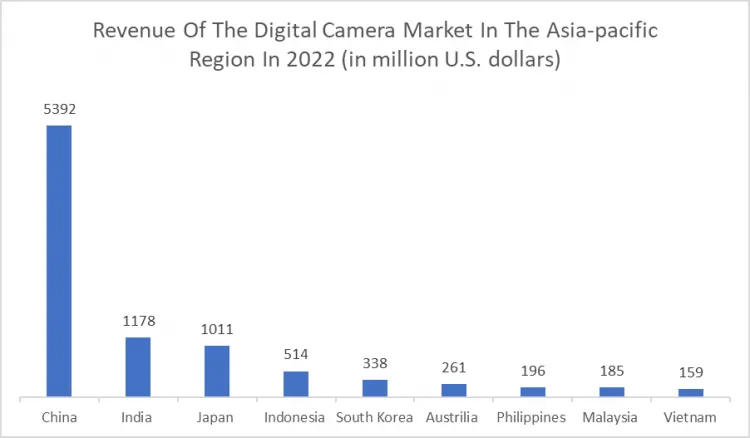

The above graph shows the revenue of the digital camera market in the Asia-Pacific region in 2022. China is the largest country in the digital camera market and they generate revenue of nearly 5,392 USD. India is the second largest country in the Asia Pacific region generating revenue of about 1,178 USD. Also, all other countries belonging to Asia Pacific generate strong revenue from digital cameras, countries like; Japan, Indonesia, South Korea, Australia, Philippines, Malaysia, and Vietnam.

COVID-19 Impact Analysis on the Digital Camera Market

The COVID-19 pandemic had a significant impact on various industries, including the digital camera market. Many digital camera manufacturers are based in countries that were heavily affected by the pandemic, such as Japan and China. Lockdowns, restrictions, and disruptions in these countries' supply chains led to delays in production, shortage of components, and reduced manufacturing capacity. Economic uncertainties and job losses caused by the pandemic led to reduced consumer spending on non-essential items, including digital cameras. Consumers prioritized essentials, which affected the demand for cameras.

During the pandemic, the digital camera industry is facing challenges caused by the COVID-19 pandemic. There are global supply chain issues, which have led to an increase in raw materials and higher production costs. These increases are reflected in the key markets of the digital camera industry. Many retail stores, especially electronics and photography stores, faced closures due to lockdowns and social distancing measures. This impacted the ability of consumers to physically browse and purchase digital cameras.

Top Key Players Covered in the Digital Camera Market

- Canon (Japan)

- Nikon (Japan)

- Fujifilm (Japan)

- Sony (Japan)

- Olympus (Japan)

- Panasonic Lumix (Japan)

- Leica: (Germany)

- Pentax: (Japan)

- Ricoh: (Japan)

- Polaroid: (US)

- GoPro: (US)

- Hasselblad: (Sweden)

- Kodak: (US)

- Sigma: (Japan)

- Samsung Electronics (South Korea)

- Red.com LLC: (US)

- Casio: (Japan)

- SJ Cam: (China)

- Tamron Co. Ltd: (Japan)

- Victor Company of Japan Ltd. (JVC): (Japan)

- Kyocera Corporation (Japan), and Other Major Players.

Key Industry Developments in the 3D Printing Materials and Services Market

- In March 2024, Nikon Corporation (Nikon) announced its entry into an agreement to acquire 100% of the outstanding membership interests of RED.com, LLC (RED) whereby RED will become a wholly-owned subsidiary of Nikon, under a Membership Interest Purchase Agreement with Mr. James Jannard, its founder, and Mr. Jarred Land, its current President, subject to the satisfaction of certain closing conditions thereunder.

- In July 2023, FUJIFILM India announced the launch of its mirrorless digital camera “FUJIFILM X-S20”, in India. It was a new addition to the X Series of mirrorless digital cameras known for their compact and lightweight body and superior image quality based on the company’s proprietary color reproduction technology. In its compact and lightweight body, which was the popular property of the previous model, the X-S20 features AI-based subject-detection AF and the capability to record 6.2K/30P video.

- In October 2022, Fujifilm announced a partnership with Adobe to produce a new mirrorless digital camera firmware, "FUJIFILM X-H2S" (X-H2S), in spring 2023, which would deliver the world's first native Camera to Cloud (C2C) connectivity for mirrorless digital cameras, driven by Frame.io. At the same time, the firmware for the "FT-XH" file transmitters will also be launched.

- In September 2022, Canon U.S.A., Inc., a significant provider of digital imaging solutions, announced the addition of a suite of products to its cinema and broadcast offerings in response to user demand. Canon's latest 8K CINE-SERVO lens for a wide range of productions is the CINE-SERVO 15-120mm T2.95-3.95 EF/PL (CN8x15 IAS S); the EU-V3, a modular expansion unit for the EOS C500 Mark II and EOS C300 Mark III cameras; a Cinema EOS firmware update; and the DP-V2730i, a 27-inch 4K professional reference display that may seamlessly fit into workflows of broadcasters and filmmakers.

|

Global Digital Camera Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 5.27 Bn. |

|

Forecast Period 2024-32 CAGR: |

7.84% |

Market Size in 2032: |

USD 10.4 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Digital Sensor Type |

|

||

|

By Component |

|

||

|

By Distribution channel |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Digital Camera Market by Product Type (2018-2032)

4.1 Digital Camera Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Bridge Compact Digital Cameras

4.5 Mirrorless Interchangeable Lens Cameras

Chapter 5: Digital Camera Market by Digital Sensor Type (2018-2032)

5.1 Digital Camera Market Snapshot and Growth Engine

5.2 Market Overview

5.3 CCD Sensor

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 CMOS Sensor

5.5 FOVEON X3 Sensor

5.6 Live MOS Sensor

Chapter 6: Digital Camera Market by Component (2018-2032)

6.1 Digital Camera Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Lenses

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Sensors

6.5 LCD Screen

6.6 Memory Card

6.7 Others

Chapter 7: Digital Camera Market by Distribution channel (2018-2032)

7.1 Digital Camera Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Online

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Offline

Chapter 8: Digital Camera Market by End User (2018-2032)

8.1 Digital Camera Market Snapshot and Growth Engine

8.2 Market Overview

8.3 Personal

8.3.1 Introduction and Market Overview

8.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

8.3.3 Key Market Trends, Growth Factors, and Opportunities

8.3.4 Geographic Segmentation Analysis

8.4 Professional

Chapter 9: Company Profiles and Competitive Analysis

9.1 Competitive Landscape

9.1.1 Competitive Benchmarking

9.1.2 Digital Camera Market Share by Manufacturer (2024)

9.1.3 Industry BCG Matrix

9.1.4 Heat Map Analysis

9.1.5 Mergers and Acquisitions

9.2 DOMTAR (US)

9.2.1 Company Overview

9.2.2 Key Executives

9.2.3 Company Snapshot

9.2.4 Role of the Company in the Market

9.2.5 Sustainability and Social Responsibility

9.2.6 Operating Business Segments

9.2.7 Product Portfolio

9.2.8 Business Performance

9.2.9 Key Strategic Moves and Recent Developments

9.2.10 SWOT Analysis

9.3 SAPPI LIMITED (SOUTH AFRICA)

9.4 NIPPON PAPER (JAPAN)

9.5 NINE DRAGON PAPER HOLDINGS (CHINA)

9.6 SVENSKA CELLULOSA AKTIEBOLAGET (SWEDEN)

9.7 PACKAGING CORPORATION OF AMERICA (US)

9.8 JK PAPER LTD. (INDIA)

9.9 SESHASAYEE PAPER & BOARDS LTD. (INDIA)

9.10 DS SMITH (UK)

9.11 MONDI (UK)

9.12 SMURFIT KAPPA GROUP (IRELAND)

9.13 OJI HOLDINGS (JAPAN)

9.14 TAMILNADU NEWSPRINT & PAPERS LTD. (INDIA)

9.15 STORA ENSO (FINLAND)

9.16 INTERNATIONAL PAPER COMPANY (US)

9.17 GEORGIA-PACIFIC LLC (US)

9.18 STORA ENSO OYJ (FINLAND)

9.19 BALLARPUR INDUSTRIES LTD. (AVANTHA) (INDIA)

9.20 UPM (FINLAND)

9.21 WESTROCK (US)

9.22 KIMBERLY-CLARK (US)

9.23 ANDHRA PAPER LTD. (INDIA)

9.24 EMAMI PAPER MILLS LTD. (INDIA)

9.25 KUANTUM PAPERS LTD. (INDIA)

9.26 SATIA INDUSTRIES LTD. (INDIA)

9.27

Chapter 10: Global Digital Camera Market By Region

10.1 Overview

10.2. North America Digital Camera Market

10.2.1 Key Market Trends, Growth Factors and Opportunities

10.2.2 Top Key Companies

10.2.3 Historic and Forecasted Market Size by Segments

10.2.4 Historic and Forecasted Market Size by Product Type

10.2.4.1 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

10.2.4.2 Bridge Compact Digital Cameras

10.2.4.3 Mirrorless Interchangeable Lens Cameras

10.2.5 Historic and Forecasted Market Size by Digital Sensor Type

10.2.5.1 CCD Sensor

10.2.5.2 CMOS Sensor

10.2.5.3 FOVEON X3 Sensor

10.2.5.4 Live MOS Sensor

10.2.6 Historic and Forecasted Market Size by Component

10.2.6.1 Lenses

10.2.6.2 Sensors

10.2.6.3 LCD Screen

10.2.6.4 Memory Card

10.2.6.5 Others

10.2.7 Historic and Forecasted Market Size by Distribution channel

10.2.7.1 Online

10.2.7.2 Offline

10.2.8 Historic and Forecasted Market Size by End User

10.2.8.1 Personal

10.2.8.2 Professional

10.2.9 Historic and Forecast Market Size by Country

10.2.9.1 US

10.2.9.2 Canada

10.2.9.3 Mexico

10.3. Eastern Europe Digital Camera Market

10.3.1 Key Market Trends, Growth Factors and Opportunities

10.3.2 Top Key Companies

10.3.3 Historic and Forecasted Market Size by Segments

10.3.4 Historic and Forecasted Market Size by Product Type

10.3.4.1 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

10.3.4.2 Bridge Compact Digital Cameras

10.3.4.3 Mirrorless Interchangeable Lens Cameras

10.3.5 Historic and Forecasted Market Size by Digital Sensor Type

10.3.5.1 CCD Sensor

10.3.5.2 CMOS Sensor

10.3.5.3 FOVEON X3 Sensor

10.3.5.4 Live MOS Sensor

10.3.6 Historic and Forecasted Market Size by Component

10.3.6.1 Lenses

10.3.6.2 Sensors

10.3.6.3 LCD Screen

10.3.6.4 Memory Card

10.3.6.5 Others

10.3.7 Historic and Forecasted Market Size by Distribution channel

10.3.7.1 Online

10.3.7.2 Offline

10.3.8 Historic and Forecasted Market Size by End User

10.3.8.1 Personal

10.3.8.2 Professional

10.3.9 Historic and Forecast Market Size by Country

10.3.9.1 Russia

10.3.9.2 Bulgaria

10.3.9.3 The Czech Republic

10.3.9.4 Hungary

10.3.9.5 Poland

10.3.9.6 Romania

10.3.9.7 Rest of Eastern Europe

10.4. Western Europe Digital Camera Market

10.4.1 Key Market Trends, Growth Factors and Opportunities

10.4.2 Top Key Companies

10.4.3 Historic and Forecasted Market Size by Segments

10.4.4 Historic and Forecasted Market Size by Product Type

10.4.4.1 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

10.4.4.2 Bridge Compact Digital Cameras

10.4.4.3 Mirrorless Interchangeable Lens Cameras

10.4.5 Historic and Forecasted Market Size by Digital Sensor Type

10.4.5.1 CCD Sensor

10.4.5.2 CMOS Sensor

10.4.5.3 FOVEON X3 Sensor

10.4.5.4 Live MOS Sensor

10.4.6 Historic and Forecasted Market Size by Component

10.4.6.1 Lenses

10.4.6.2 Sensors

10.4.6.3 LCD Screen

10.4.6.4 Memory Card

10.4.6.5 Others

10.4.7 Historic and Forecasted Market Size by Distribution channel

10.4.7.1 Online

10.4.7.2 Offline

10.4.8 Historic and Forecasted Market Size by End User

10.4.8.1 Personal

10.4.8.2 Professional

10.4.9 Historic and Forecast Market Size by Country

10.4.9.1 Germany

10.4.9.2 UK

10.4.9.3 France

10.4.9.4 The Netherlands

10.4.9.5 Italy

10.4.9.6 Spain

10.4.9.7 Rest of Western Europe

10.5. Asia Pacific Digital Camera Market

10.5.1 Key Market Trends, Growth Factors and Opportunities

10.5.2 Top Key Companies

10.5.3 Historic and Forecasted Market Size by Segments

10.5.4 Historic and Forecasted Market Size by Product Type

10.5.4.1 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

10.5.4.2 Bridge Compact Digital Cameras

10.5.4.3 Mirrorless Interchangeable Lens Cameras

10.5.5 Historic and Forecasted Market Size by Digital Sensor Type

10.5.5.1 CCD Sensor

10.5.5.2 CMOS Sensor

10.5.5.3 FOVEON X3 Sensor

10.5.5.4 Live MOS Sensor

10.5.6 Historic and Forecasted Market Size by Component

10.5.6.1 Lenses

10.5.6.2 Sensors

10.5.6.3 LCD Screen

10.5.6.4 Memory Card

10.5.6.5 Others

10.5.7 Historic and Forecasted Market Size by Distribution channel

10.5.7.1 Online

10.5.7.2 Offline

10.5.8 Historic and Forecasted Market Size by End User

10.5.8.1 Personal

10.5.8.2 Professional

10.5.9 Historic and Forecast Market Size by Country

10.5.9.1 China

10.5.9.2 India

10.5.9.3 Japan

10.5.9.4 South Korea

10.5.9.5 Malaysia

10.5.9.6 Thailand

10.5.9.7 Vietnam

10.5.9.8 The Philippines

10.5.9.9 Australia

10.5.9.10 New Zealand

10.5.9.11 Rest of APAC

10.6. Middle East & Africa Digital Camera Market

10.6.1 Key Market Trends, Growth Factors and Opportunities

10.6.2 Top Key Companies

10.6.3 Historic and Forecasted Market Size by Segments

10.6.4 Historic and Forecasted Market Size by Product Type

10.6.4.1 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

10.6.4.2 Bridge Compact Digital Cameras

10.6.4.3 Mirrorless Interchangeable Lens Cameras

10.6.5 Historic and Forecasted Market Size by Digital Sensor Type

10.6.5.1 CCD Sensor

10.6.5.2 CMOS Sensor

10.6.5.3 FOVEON X3 Sensor

10.6.5.4 Live MOS Sensor

10.6.6 Historic and Forecasted Market Size by Component

10.6.6.1 Lenses

10.6.6.2 Sensors

10.6.6.3 LCD Screen

10.6.6.4 Memory Card

10.6.6.5 Others

10.6.7 Historic and Forecasted Market Size by Distribution channel

10.6.7.1 Online

10.6.7.2 Offline

10.6.8 Historic and Forecasted Market Size by End User

10.6.8.1 Personal

10.6.8.2 Professional

10.6.9 Historic and Forecast Market Size by Country

10.6.9.1 Turkiye

10.6.9.2 Bahrain

10.6.9.3 Kuwait

10.6.9.4 Saudi Arabia

10.6.9.5 Qatar

10.6.9.6 UAE

10.6.9.7 Israel

10.6.9.8 South Africa

10.7. South America Digital Camera Market

10.7.1 Key Market Trends, Growth Factors and Opportunities

10.7.2 Top Key Companies

10.7.3 Historic and Forecasted Market Size by Segments

10.7.4 Historic and Forecasted Market Size by Product Type

10.7.4.1 Digital Single-Lens Reflex (DSLR) Cameras Compact Digital Cameras

10.7.4.2 Bridge Compact Digital Cameras

10.7.4.3 Mirrorless Interchangeable Lens Cameras

10.7.5 Historic and Forecasted Market Size by Digital Sensor Type

10.7.5.1 CCD Sensor

10.7.5.2 CMOS Sensor

10.7.5.3 FOVEON X3 Sensor

10.7.5.4 Live MOS Sensor

10.7.6 Historic and Forecasted Market Size by Component

10.7.6.1 Lenses

10.7.6.2 Sensors

10.7.6.3 LCD Screen

10.7.6.4 Memory Card

10.7.6.5 Others

10.7.7 Historic and Forecasted Market Size by Distribution channel

10.7.7.1 Online

10.7.7.2 Offline

10.7.8 Historic and Forecasted Market Size by End User

10.7.8.1 Personal

10.7.8.2 Professional

10.7.9 Historic and Forecast Market Size by Country

10.7.9.1 Brazil

10.7.9.2 Argentina

10.7.9.3 Rest of SA

Chapter 11 Analyst Viewpoint and Conclusion

11.1 Recommendations and Concluding Analysis

11.2 Potential Market Strategies

Chapter 12 Research Methodology

12.1 Research Process

12.2 Primary Research

12.3 Secondary Research

|

Global Digital Camera Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 5.27 Bn. |

|

Forecast Period 2024-32 CAGR: |

7.84% |

Market Size in 2032: |

USD 10.4 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Digital Sensor Type |

|

||

|

By Component |

|

||

|

By Distribution channel |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the Report: |

|

||