Prepared Food Market Synopsis:

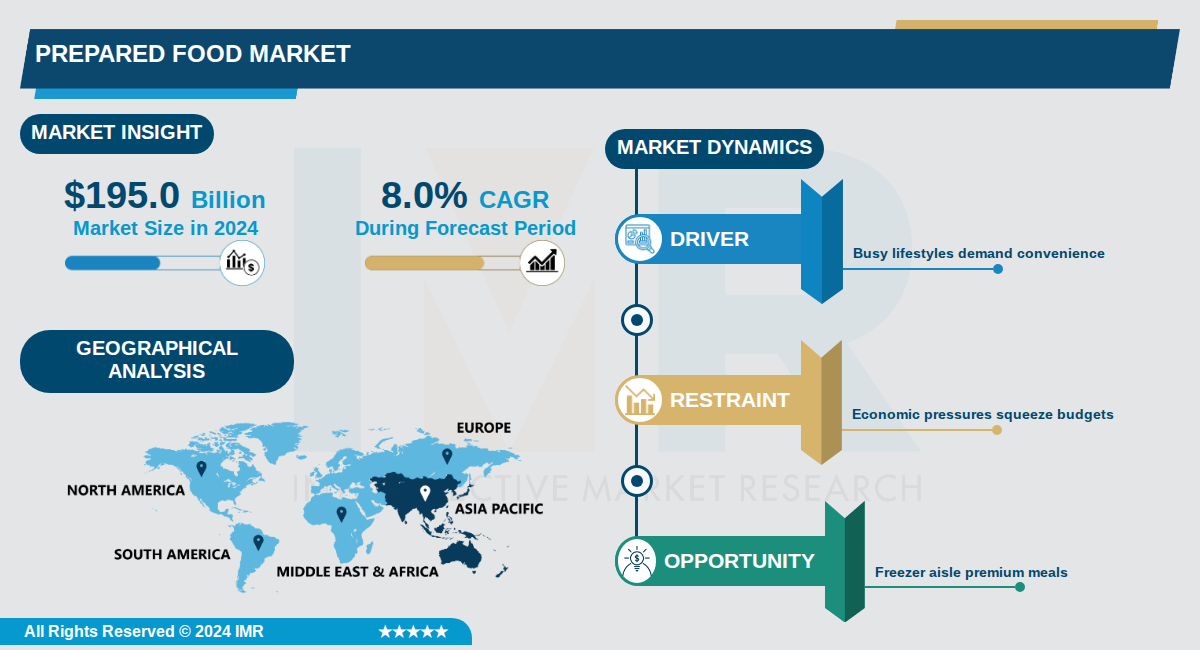

Prepared Food Market Size Was Valued at USD 195.0 Billion in 2024, and is Projected to Reach USD 424.0 Billion by 2035, Growing at a CAGR of 8.0% From 2024-2035.

The global Prepared Food Market, valued at $195.0 billion in 2024, is projected to reach $424.0 billion by 2035, growing at a compound annual growth rate (CAGR) of 8.0%. This robust expansion reflects evolving consumer lifestyles, with increasing demand for convenience foods such as ready-to-eat, ready-to-heat, and ready-to-cook options amid busy schedules and urbanization.

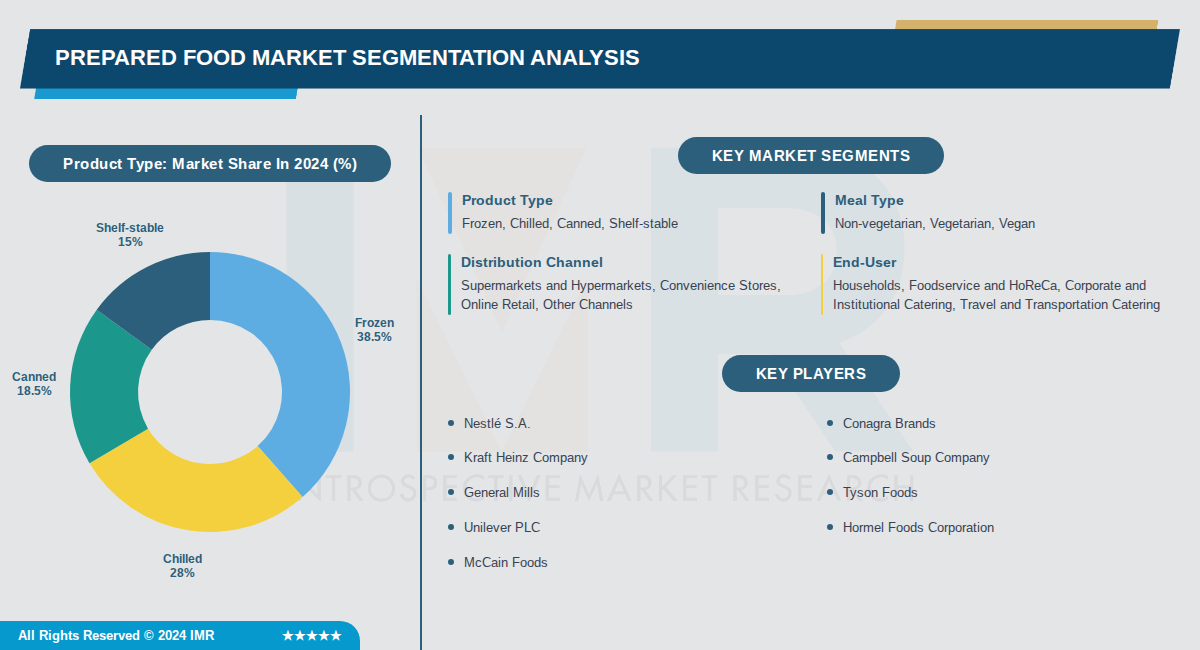

Key market segments include frozen meals, which dominate due to extended shelf life and nutritional retention, followed by chilled and canned varieties. Distribution channels like hypermarkets/supermarkets hold the largest share at around 50%, while online sales are the fastest-growing at a CAGR of up to 9.8%, driven by e-commerce convenience and accessibility.

Regionally, Asia Pacific is the fastest-growing market, fueled by population growth, economic development, and adoption of convenience foods, while Europe leads in share with premium and nutritionally balanced options, and North America emphasizes health trends and organic products.

Prepared Food Market Trend Analysis:

Rise of Freezer Fine Dining

- Frozen meals are surging in popularity with high-quality, globally inspired options hitting grocery shelves, allowing consumers to create restaurant-worthy experiences at home without the cost of dining out. Whole Foods Market highlights products like Flour + Water Cacio e Pepe Pizza, Force of Nature Grass Fed Ancestral Blend Classic Meatballs, and Masienda Beef Birria Quesadillas as prime examples that pair premium ingredients with time-saving preparation. These frozen appetizers and entrees appeal to meal planners seeking convenience while maintaining flavor sophistication.

- Brands are responding to busy lifestyles by offering frozen sides and meals that require minimal effort, such as Mimi Cheng’s Dumplings and Saiga Foods Pho, part of Whole Foods' 2025 LEAP Early Growth Cohort. This trend supports budget-conscious foodies who want elevated eats without cooking from scratch, with sales driven by the desire for high-end taste in the freezer aisle. Good Housekeeping notes similar family-sized options from Kevin’s Natural Foods like premade gluten-free pesto chicken pasta.

- The shift emphasizes quality over basic microwave fare, with innovative textures and flavors like Laoban Crab Rangoon and Whole Foods Market Creamy Harissa & Cheese Phyllo Bites transforming the frozen category into a destination for fine dining hacks.

Portioned Labor-Saving Ingredients

- Pre-cut produce, pre-portioned proteins, and ready-to-use ingredients are essential for kitchens aiming to save time while preserving quality and consistency, as predicted by Baldor Specialty Foods' Mark Pastore. These products address labor constraints and rising grocery costs by enabling operators and home cooks to create craveable meals efficiently without sacrificing flavor. Consumers increasingly opt for these despite higher upfront prices because they save valuable time over whole produce or scratch prep.

- Baldor emphasizes that this trend reflects adaptation to economic pressures, with ingredients that 'work harder on the plate' like pre-prepped fresh foods becoming staples in grocery carts. For busy households, this middle ground between takeout and full cooking reduces wallet strain and supports healthier choices. Examples include pre-portioned meats and diced vegetables that streamline meal assembly.

- The focus on efficiency aligns with broader shifts, as seen in Good Housekeeping's coverage of family brands like Amy’s offering family-size entrees and Kidfresh's hidden veggie kids meals available at Target.

Bold Globally Rooted Flavors

- Global flavors are justifying premium positioning with strong momentum around Afro-Caribbean influences, bringing ingredients like Scotch bonnet, tamarind, okra, oxtail, yuzu, and sudachi to U.S. stores, according to Baldor's Matthew Rendine. These bold, foreign cuisine staples are gaining recognition and enhancing prepared foods with refined sour and citrus notes. Operators are prioritizing flavor-forward experiences to meet consumer demands for excitement amid cost constraints.

- This trend ties into prepared foods by integrating international profiles into convenient formats, such as frozen global meals and pre-prepped spice blends. Whole Foods examples like MiLà Caramelized Scallion Oil Noodles showcase how these flavors elevate ready-to-eat options. It reflects a broader crave for diverse, premium taste without added kitchen effort.

Prepared Food Market Segment Analysis:

Prepared Food Market is Segmented on the basis of By Product Type, By Meal Type, By Distribution Channel

By Product Type, Frozen segment is expected to dominate the market during the forecast period

- Frozen prepared foods dominate the market due to extended shelf life, convenience, and widespread availability in supermarkets and hypermarkets globally. Frozen products represent the largest category with superior logistical advantages and consumer familiarity.

- The frozen segment benefits from advanced cold chain infrastructure expansion in developing regions and consistent consumer preference for portion-controlled frozen meals that reduce food waste and preparation time.

By Meal Type, Non-vegetarian segment is expected to dominate the market during the forecast period

- Non-vegetarian meals command the largest market share due to traditional consumer preferences and broader global meat consumption patterns across North America, Europe, and Asia-Pacific regions.

- The vegan segment is the fastest-growing category driven by millennial health consciousness and animal welfare concerns, with market participants introducing innovative vegan-ready meals and snacks to capture this expanding demographic.

By Distribution Channel, Supermarkets and Hypermarkets segment is expected to dominate the market during the forecast period

- Supermarkets and hypermarkets dominate as the primary distribution channel due to vast product availability, extensive shelf space, and consumer preference for product selection and tangible shopping experiences in established retail locations.

- The e-commerce segment is experiencing rapid growth driven by hassle-free door-to-door delivery options and increased online platform penetration, particularly in developed markets like the United Kingdom and United States.

By End-User, Households segment is expected to dominate the market during the forecast period

- Household consumers represent the dominant end-user segment, driven by urbanization, growing working populations, and increased reliance on prepared meals due to busy lifestyles and high personal discretionary income in developed regions.

- The household segment benefits from rising time-saving food solution demand and the structural shift toward convenience consumption patterns, particularly in North America which captures 40.9% of global prepared food market share.

Prepared Food Market Regional Insights:

Asia-Pacific Emerges as the Fastest-Growing and Increasingly Dominant Region

- Asia-Pacific is positioned as the fastest-growing region in the prepared food market, driven by rapid urbanization, demographic expansion, and a burgeoning middle class with increasing disposable incomes. China leads this growth with a projected 10.2% CAGR through 2036, while India is forecast to grow at 11.8% CAGR, supported by rapid quick-commerce expansion and a food retail sector valued at USD 719 billion. Japan's aging population drives demand for high-quality frozen meals, while Indonesia's younger demographic accelerates growth in pasta and noodle-based ready-to-eat products.

- The region benefits from organized retail proliferation, e-commerce expansion, and evolving consumer preferences toward convenience foods and Westernized eating habits. Asia-Pacific's prepared foods market is estimated at approximately USD 70 billion with a CAGR of 6.5%, and online sales channels are experiencing rapid growth at 9.8% CAGR, reflecting strong preference for e-commerce convenience. Distribution challenges in rural areas are being addressed through expanding modern retail formats and quick-commerce networks.

- Leading global players including Nestlé S.A. and Kraft Heinz compete alongside growing local manufacturers who leverage cost-effective offerings and region-specific products such as tropical fruit-based meals and nutritionally-fortified options. The competitive landscape is intensifying as Asia-Pacific captures increasing market share, with particular strength in premium segments in developed markets like Japan and South Korea, while emerging markets drive volume growth through affordable, convenient meal solutions.

Active Key Players in the Prepared Food Market:

- Nestlé S.A. (Switzerland)

- Conagra Brands (USA)

- Kraft Heinz Company (USA)

- Campbell Soup Company (USA)

- General Mills (USA)

- Tyson Foods (USA)

- Unilever PLC (United Kingdom)

- Hormel Foods Corporation (USA)

- McCain Foods (Canada)

- Dr. Oetker (Germany)

- Nissin Foods Holdings (Japan)

- Toyo Suisan Kaisha (Japan)

- Princes Limited (United Kingdom)

- The Hain Celestial Group (USA)

- B&G Foods Inc. (USA)

- Associated British Foods (United Kingdom)

- Kellanov (USA)

- J.M. Smucker Co. (USA)

- Other Active Players

|

Prepared Food Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 195.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

8.0 % |

Market Size in 2035: |

USD 424.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Meal Type |

|

||

|

By Distribution Channel |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Prepared Food Market by Product Type (2017-2035)

4.1 Prepared Food Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Frozen

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Chilled

4.5 Canned

4.6 Shelf-stable

Chapter 5: Prepared Food Market by Meal Type (2017-2035)

5.1 Prepared Food Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Non-vegetarian

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Vegetarian

5.5 Vegan

Chapter 6: Prepared Food Market by Distribution Channel (2017-2035)

6.1 Prepared Food Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Supermarkets and Hypermarkets

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Convenience Stores

6.5 Online Retail

6.6 Other Channels

Chapter 7: Prepared Food Market by End-User (2017-2035)

7.1 Prepared Food Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Households

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Foodservice and HoReCa

7.5 Corporate and Institutional Catering

7.6 Travel and Transportation Catering

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Prepared Food Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 NESTLÉ S.A.

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 CONAGRA BRANDS

8.4 KRAFT HEINZ COMPANY

8.5 CAMPBELL SOUP COMPANY

8.6 GENERAL MILLS

8.7 TYSON FOODS

8.8 UNILEVER PLC

8.9 HORMEL FOODS CORPORATION

8.10 MCCAIN FOODS

8.11 DR. OETKER

8.12 NISSIN FOODS HOLDINGS

8.13 TOYO SUISAN KAISHA

8.14 PRINCES LIMITED

8.15 THE HAIN CELESTIAL GROUP

8.16 B&G FOODS INC.

8.17 ASSOCIATED BRITISH FOODS

8.18 KELLANOV

8.19 J.M. SMUCKER CO.

Chapter 9: Global Prepared Food Market By Region

9.1 Overview

9.2. North America Prepared Food Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Prepared Food Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Prepared Food Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Prepared Food Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Prepared Food Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Prepared Food Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Prepared Food Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 195.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

8.0 % |

Market Size in 2035: |

USD 424.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Meal Type |

|

||

|

By Distribution Channel |

|

||

|

By End-User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||