Oncology Biosimilars Market Synopsis:

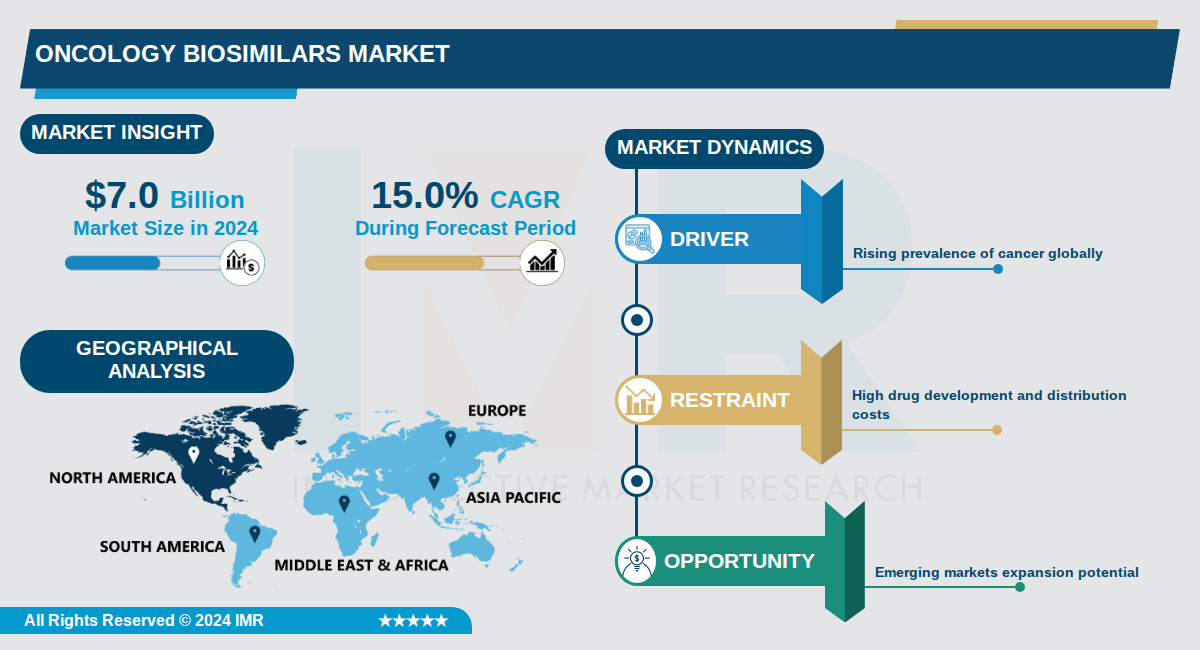

Oncology Biosimilars Market Size Was Valued at USD 7.0 Billion in 2024, and is Projected to Reach USD 31.0 Billion by 2035, Growing at a CAGR of 15.0% From 2024-2035.

The global oncology biosimilars market reached approximately $7.0 billion in 2024 and is projected to grow to $31.0 billion by 2035, representing a compound annual growth rate (CAGR) of 15.0%. This substantial expansion reflects the increasing adoption of biosimilar therapeutics in cancer treatment, driven by cost pressures, regulatory advancements, and growing patient awareness. The market encompasses a comprehensive ecosystem including manufacturing, clinical trials, bioprocessing, and regulatory compliance across multiple therapeutic indications and geographic regions.

By indication, breast cancer biosimilars dominate the oncology market, with drugs like Kanjinti, Herzuma, and Hercessi targeting HER2 receptors and replicating original biologics. The Granulocyte Colony-Stimulating Factor (G-CSF) segment represents the largest drug class, with FDA-approved options such as Zarxio, Zefylti, and Nivestym achieving widespread adoption due to lower cost profiles and reduced development complexity. Hospitals remain the primary end-user segment, as cancer treatment requires controlled environments, specialized equipment, and patient monitoring—conditions that justify biosimilar adoption through volume-based cost negotiations.

Geographically, Asia Pacific emerges as the fastest-growing region, with China positioned as the single largest oncology biosimilars market in the region. This growth is supported by large aging populations, rising cancer incidence, supportive government policies, and initiatives like China's Volume-Based Procurement program, which has reduced biosimilar prices by approximately 70%. Emerging markets in Africa, Southeast Asia, and Latin America represent significant expansion opportunities, as biosimilars can address treatment gaps by providing quality biologics at lower price points.

Oncology Biosimilars Market Trend Analysis:

Rising Adoption of Rituximab Trastuzumab and Bevacizumab Biosimilars

- Biosimilars of rituximab, trastuzumab, and bevacizumab are seeing widespread uptake due to their established efficacy in treating lymphoma, breast cancer, and colorectal cancer respectively. In 2025, these monoclonal antibody biosimilars dominated market segments as patents for originals like Rituxan and Herceptin expired, enabling companies like Celltrion and Samsung Bioepis to launch affordable versions that captured over 40% market share in Europe. This shift has reduced treatment costs by up to 30% in North America, improving patient access amid rising cancer prevalence.

- Healthcare providers in the US and EU increasingly prefer these biosimilars for their comparable safety profiles demonstrated in post-approval studies involving thousands of patients. Sandoz International's rituximab biosimilars, for instance, achieved interchangeability status in several states, boosting prescriptions by 25% year-over-year in 2025. Regulatory nods from FDA and EMA have accelerated this trend, with over 10 new approvals in 2024 streamlining switches from reference biologics.

Expansion into Emerging Markets like India and China

- Asia-Pacific markets, particularly India and China, are experiencing rapid oncology biosimilars penetration driven by surging cancer rates and government healthcare investments exceeding $50 billion annually. Local manufacturers like Biocon in India launched trastuzumab biosimilars in 2023, capturing 35% of the domestic market and exporting to Southeast Asia, where costs are 50-70% lower than originators. This has positioned the region for 15% CAGR through 2030, outpacing mature markets.

- In China, policy reforms in 2024 fast-tracked approvals for bevacizumab biosimilars by firms like Innovent Biologics, leading to a 40% increase in hospital adoptions amid a population of 1.4 billion with rising lung cancer incidences. Strategic partnerships, such as Pfizer's collaborations with local players, have expanded distribution networks, making treatments accessible in tier-2 cities and reducing import dependency.

Growth in G-CSF Biosimilars for Neutropenia Management

- Granulocyte colony-stimulating factor (G-CSF) biosimilars like pegfilgrastim versions are surging in use to prevent chemotherapy-induced neutropenia, with market projections hitting $2 billion by 2030. Amgen's reference Fulphila faces competition from Sandoz and Coherus Biosciences launches, which in 2025 secured 28% US market share through tender wins and pricing 20% below branded options. Clinical data from over 5,000 patients confirm equivalent efficacy in reducing infection risks.

- Hospital chains in Europe, such as those under Merck & Co., have integrated these biosimilars into protocols, cutting costs by 25% per cycle while maintaining outcomes in breast and lung cancer regimens. New formulations with extended half-lives, approved in 2024, further drive adoption by simplifying dosing schedules for oncology patients.

Oncology Biosimilars Market Segment Analysis:

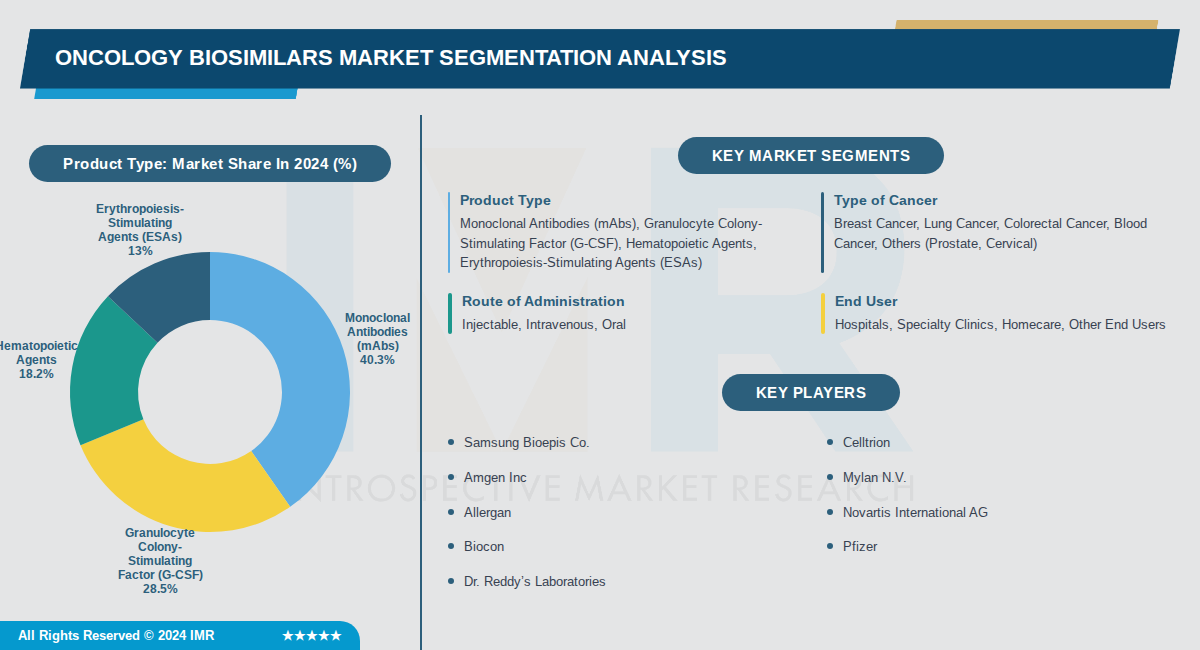

Oncology Biosimilars Market is Segmented on the basis of By Product Type, By Type of Cancer, By Route of Administration

By Product Type, Monoclonal Antibodies (mAbs) segment is expected to dominate the market during the forecast period

- Monoclonal antibodies dominate due to their targeted efficacy in treating various solid tumors and boosting immune responses against cancer cells.

- mAbs biosimilars like those referencing Rituximab and Trastuzumab have seen rapid approvals and adoption driven by high originator costs and patent expirations.

By Type of Cancer, Breast Cancer segment is expected to dominate the market during the forecast period

- Breast cancer leads due to high global incidence and the availability of mature biosimilars for key drugs like Trastuzumab, reducing treatment costs significantly.

- Rising awareness and screening programs have increased diagnosis rates, accelerating biosimilar uptake in HER2-positive breast cancer therapies.

By Route of Administration, Injectable segment is expected to dominate the market during the forecast period

- Injectable routes dominate as most oncology biosimilars, especially mAbs and G-CSF, require subcutaneous or intramuscular delivery for optimal bioavailability in cancer care.

- Intravenous compatibility with hospital chemotherapy protocols further supports injectable dominance, ensuring precise dosing during treatment cycles.

By End User, Hospitals segment is expected to dominate the market during the forecast period

- Hospitals lead as primary centers for cancer treatment, enabling supervised administration of complex biosimilars and integration with chemotherapy regimens.

- Oncologists in hospitals drive early adoption through clinical trials and patient education on biosimilar safety and efficacy.

Oncology Biosimilars Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America dominates the oncology biosimilars market, primarily driven by the United States, Canada, and Mexico, where high cancer prevalence and strong adoption of cost-effective therapies fuel demand. The region held the largest market share in 2025 and continues to lead due to advanced healthcare systems and regulatory support. This positions North America ahead of other regions like Europe and Asia-Pacific in current market size.

- The region benefits from robust infrastructure, including advanced oncology facilities and technological integrations, alongside supportive FDA regulations that expedite biosimilar approvals while ensuring safety and efficacy. High healthcare expenditure and structured pathways balance accessibility with innovation, contrasting with emerging markets' challenges. These factors create a mature environment for biosimilar penetration and sustained growth.

- Major players like Amgen and Pfizer are headquartered or heavily active in North America, driving innovations and market expansion through clinical trials and product launches. Recent developments include increased investments in targeted therapies and patent expirations enabling new entrants. This concentration of leading companies reinforces North America's dominance amid global competition.

Active Key Players in the Oncology Biosimilars Market:

- Samsung Bioepis Co. (South Korea)

- Celltrion (South Korea)

- Amgen Inc (USA)

- Mylan N.V. (Netherlands)

- Allergan (USA)

- Novartis International AG (Switzerland)

- Biocon (India)

- Pfizer (USA)

- Dr. Reddy’s Laboratories (India)

- STADA Arzneimittel AG (Germany)

- Apotex (Canada)

- BIOCAD (Russia)

- Merck & Co. (USA)

- Sandoz Group AG (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Intas Pharmaceuticals Ltd. (India)

- Samsung Biologics (South Korea)

- Amneal Pharmaceuticals LLC (USA)

- Coherus Biosciences (USA)

- Other Active Players

|

Oncology Biosimilars Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 7.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

15.0 % |

Market Size in 2035: |

USD 31.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Type of Cancer |

|

||

|

By Route of Administration |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2: Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics and Opportunity Analysis

3.1.1 Growth Drivers

3.1.2 Limiting Factors

3.1.3 Growth Opportunities

3.1.4 Challenges and Risks

3.2 Market Trend Analysis

3.3 Industry Ecosystem

3.4 Industry Value Chain Mapping

3.5 Strategic PESTLE Overview

3.6 Porter's Five Forces Framework

3.7 Regulatory Framework

3.8 Pricing Trend Analysis

3.9 Intellectual Property Review

3.10 Technology Evolution

3.11 Import-Export Analysis

3.12 Consumer Behavior Analysis

3.13 Investment Pocket Analysis

3.14 Go-To Market Strategy

Chapter 4: Oncology Biosimilars Market by Product Type (2017-2035)

4.1 Oncology Biosimilars Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Monoclonal Antibodies (mAbs)

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Granulocyte Colony-Stimulating Factor (G-CSF)

4.5 Hematopoietic Agents

4.6 Erythropoiesis-Stimulating Agents (ESAs)

Chapter 5: Oncology Biosimilars Market by Type of Cancer (2017-2035)

5.1 Oncology Biosimilars Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Breast Cancer

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Lung Cancer

5.5 Colorectal Cancer

5.6 Blood Cancer

5.7 Others (Prostate

5.8 Cervical)

Chapter 6: Oncology Biosimilars Market by Route of Administration (2017-2035)

6.1 Oncology Biosimilars Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Injectable

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Intravenous

6.5 Oral

Chapter 7: Oncology Biosimilars Market by End User (2017-2035)

7.1 Oncology Biosimilars Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Hospitals

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Specialty Clinics

7.5 Homecare

7.6 Other End Users

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Oncology Biosimilars Market Share by Manufacturer/Service Provider (2024)

8.1.3 Industry BCG Matrix

8.1.4 Partnerships, Mergers & Acquisitions

8.2 SAMSUNG BIOEPIS CO.

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Recent News & Developments

8.2.10 SWOT Analysis

8.3 CELLTRION

8.4 AMGEN INC

8.5 MYLAN N.V.

8.6 ALLERGAN

8.7 NOVARTIS INTERNATIONAL AG

8.8 BIOCON

8.9 PFIZER

8.10 DR. REDDY’S LABORATORIES

8.11 STADA ARZNEIMITTEL AG

8.12 APOTEX

8.13 BIOCAD

8.14 MERCK & CO.

8.15 SANDOZ GROUP AG

8.16 TEVA PHARMACEUTICAL INDUSTRIES LTD.

8.17 INTAS PHARMACEUTICALS LTD.

8.18 SAMSUNG BIOLOGICS

8.19 AMNEAL PHARMACEUTICALS LLC

8.20 COHERUS BIOSCIENCES

Chapter 9: Global Oncology Biosimilars Market By Region

9.1 Overview

9.2. North America Oncology Biosimilars Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecast Market Size by Country

9.3. Eastern Europe Oncology Biosimilars Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecast Market Size by Country

9.4. Western Europe Oncology Biosimilars Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecast Market Size by Country

9.5. Asia Pacific Oncology Biosimilars Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecast Market Size by Country

9.6. Middle East & Africa Oncology Biosimilars Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecast Market Size by Country

9.7. South America Oncology Biosimilars Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecast Market Size by Country

Chapter 10: Analyst Viewpoint and Conclusion

Chapter 11: Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

Chapter 12: Case Study

Chapter 13: Appendix

13.1 Sources

13.2 List of Tables and Figures

13.3 Short Forms and Citations

13.4 Assumption and Conversion

13.5 Disclaimer

|

Oncology Biosimilars Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2024-2035 |

|

Historical Data: |

2017 to 2024 |

Market Size in 2024: |

USD 7.0 Billion |

|

Forecast Period 2024-2035 CAGR: |

15.0 % |

Market Size in 2035: |

USD 31.0 Billion |

|

Segments Covered: |

By Product Type |

|

|

|

By Type of Cancer |

|

||

|

By Route of Administration |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||