Zimbabwe Pharmaceutical Market Overview

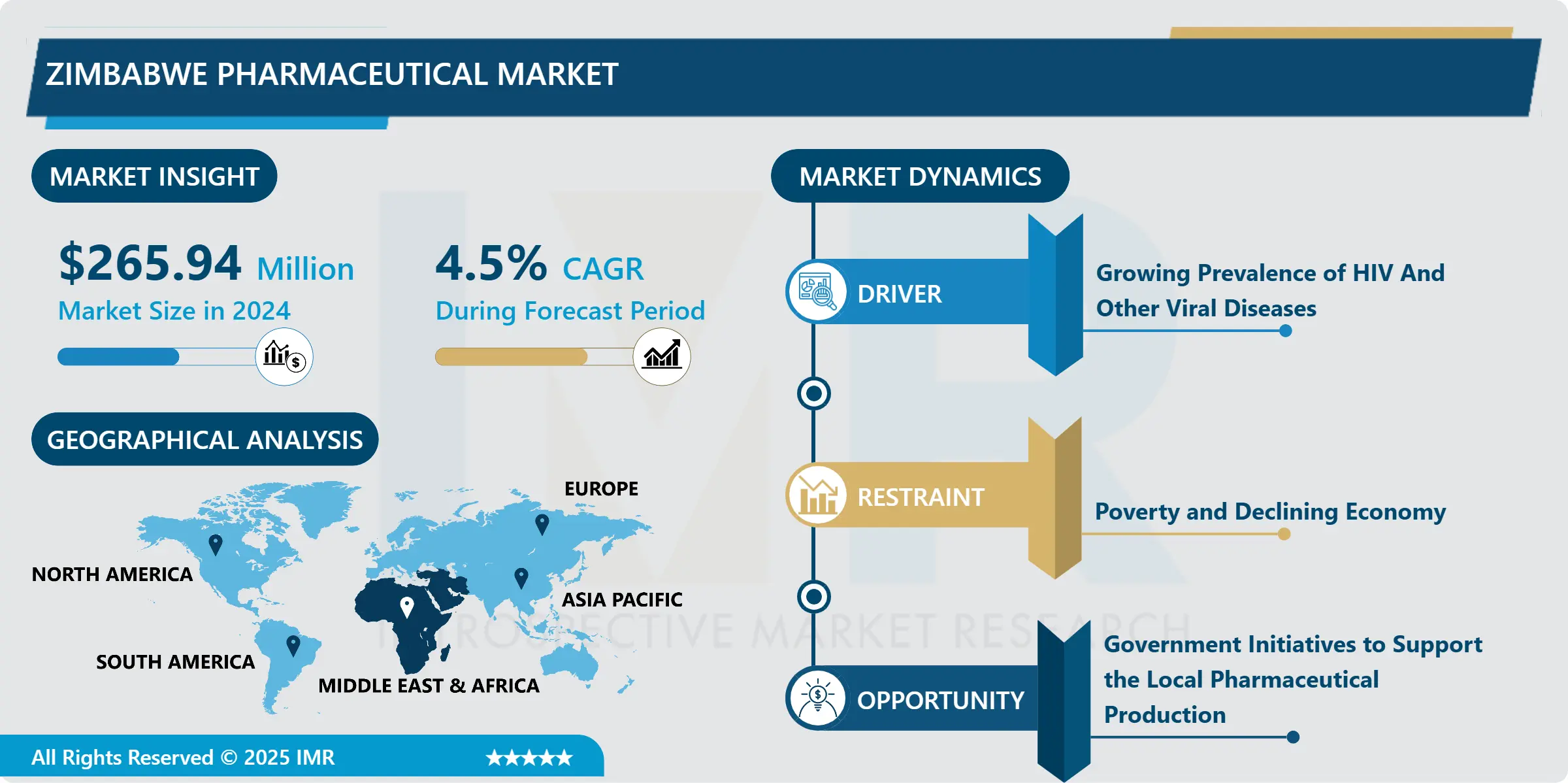

The Zimbabwe Pharmaceutical Market Size Was Valued at USD 265.94 Million In 2024 And Is Projected to Reach USD 431.58 Million By 2035, Registering A CAGR of 4.5% From 2025 to 2035.

Pharmaceutical products, also known as medicines or drugs, are specialized preparations used in both modern and traditional treatment. They are critical for illness prevention and treatment, as well as public health protection. The use of ineffective, low-quality, or toxic pharmaceuticals can result in therapeutic failure, disease exacerbation, drug resistance, and, in some cases, death. It also reduces trust in healthcare systems, healthcare practitioners, pharmaceutical makers, and distributors. Thus, to prevent the circulation of counterfeit products in the market, stringent regulations are required. According to the United Nations World Population Ageing Report 2019, Zimbabwe's population of individuals aged 65 and above was estimated to be 437,000 in 2019 and is expected to reach 1,297,000 by 2050. The geriatric population is prone to infectious and other age-related diseases. They are susceptible to chronic diseases such as cardiovascular disease, cancer, and gastrointestinal problems. Additionally, HIV, tuberculosis (TB), and malaria are the top three health threats faced by individuals. The increasing prevalence of these diseases has propelled the demand for new therapies. Furthermore, to capitalize on the growing pharma market, several global market players have entered Zimbabwe. The entry of global players coupled with the increasing cases of infectious diseases is anticipated to strengthen the growth of the Zimbabwe Pharmaceutical market over the forecasted period.

Market Dynamics and Factors for Zimbabwe Pharmaceutical Market:

Drivers:

Growing Prevalence of HIV And Other Viral Diseases

Zimbabwe has a widespread HIV epidemic, with 1.27 million people living with HIV (PLHIV), including 1.19 million adults and 69,972 children. In 2020, an estimated 1.27 million people were living with HIV, with 5.53 % of them being children aged 0-14. 60.6% of HIV-positive adults aged 15 and above were female. Annual all-cause deaths among PLHIV have decreased over the last decade, with approximately 28,201 all-cause deaths expected in 2020, down from 127,871 in 2003. Total new HIV infections in Zimbabwe have decreased from 98,668 in 2003 to 24,524 in 2020. ART coverage among all HIV-positive adults was 92% for adult men and 93% for adult women by the end of 2020. Children's coverage was slightly lower, at 66%.

According to the Zimbabwe Population-Based HIV Impact Assessment (ZIMPHIA) 2020, overall HIV prevalence for adults aged 15-49 was 11.8% in 2020, down from 18.1% in the ZDHS in 2005. HIV prevalence varied geographically in the 2020 ZIMPHIA, with higher prevalence in Matabeleland North (14.9%), Bulawayo (14.0%), and Matabeleland South (17.6%) than in the other seven provinces, which were all below 14%. The highest estimated HIV prevalence was nearly 30% for both males (30.9%) and females (33.3%) but occurred at a slightly older age (50-54 years) in males than females (45-49 years). The gender disparity in HIV prevalence was most pronounced among young individuals, with females (6.4%) having three times the prevalence of males (2.8%) aged 20 to 24 years. Though there has been a steep decline in new cases, the demand for ART to treat infected individuals has increased. With support from the President’s Emergency Plan for AIDS Relief (PEPFAR) in the USA, ART coverage has increased nationally. This growth in ART coverage is anticipated to support the growth of the Zimbabwe pharmaceutical market over the analysis period.

Restraints:

Poverty and Declining Economy

Zimbabwe's weak economy will continue to constrain pharmaceutical and healthcare market growth as household incomes and government tax revenues remain low. In addition, Zimbabwe's annual consumer price inflation increased to 285% in August 2022, up from 256.9% the previous month. It was the highest reading since February 2021, amid general increases in all categories of goods and services, particularly food, due to failed harvests caused by droughts. Over the last seven months, the country has faced severe inflationary pressures, which have been attributed to exchange rate volatility and external factors such as the Russia - Ukraine war. This rise in consumer price inflation restricts most civilians from purchasing essential medicines. Despite the support from foreign investments, Zimbabwe's weak economic environment will continue to disincentivize investors from entering the market thereby, hampering the development of the Zimbabwe pharmaceutical market growth over the forecasted period.

Opportunities:

Government Initiatives to Support the Local Pharmaceutical Production

In terms of meeting drug and export requirements, the Zimbabwe Pharmaceutical Industry has proven to be strategic. The sector has thus been prioritized for resuscitation in the National Development Strategy 1 (2021-2025), Zimbabwe National Industrial Policy (2019 - 2023), and the Local Content Strategy to strengthen the local production of essential medicines. Zimbabwe's pharmaceutical industry is made up of nine pharmaceutical companies: CAPS Pharmaceuticals, Varichem Pharmaceuticals, Pharmanova, Datlabs, Plus Five Pharmaceuticals, ZimPharm Graniteside, and Gulf Drug, manufactures human medicines, while Ecomed manufactures veterinary products. These companies account only for 12% of the total medicines consumed as they mostly manufacture generic medicines.

Additionally, they are not compliant with standards set by the World Health Organization (Good Manufacturing Practices). The financial requirement for the implementation of the strategy is USD 45 million, out of which USD 43 million will be allocated to the costs for GMP upgrading and product development and US$ 2 million for support infrastructure. This support from the government will help the local companies to comply with GMP standards set by the WHO resulting in the production of anti-retroviral drugs that are mostly imported from countries. The introduction of the Pharmaceutical Manufacturing Strategy in Zimbabwe is anticipated to create lucrative opportunities for local market players over the forecasted period.

Segmentation Analysis of Zimbabwe Pharmaceutical Market

By Drug Type, the prescription drug segment is anticipated to dominate throughout the forecasted period. The prevalence of Malaria, HIV, Tuberculosis, and Human Papilloma Virus (HOV) are some of the major diseases that have contributed to the growth of prescription drugs in the country. According to WHO, it was estimated that 29,000 people were diagnosed with TB in 2020, and about 2,100 of these succumbed to the disease. Additionally, the country also reports a large number of malarial cases every year. Malaria is still one of Zimbabwe's top three causes of illness and death. Pregnant women and children under the age of five are among the most vulnerable, and more than half of the population lives in high-risk areas. Malaria cases increased by 58% from 242,951 in 2019 to 384,956 in 2020, according to the Ministry of Health and Child Care. This growth in cases represents a rise in the demand for prescription drugs. Drugs that are administered for the treatment of HIV and Malaria are prescribed and are not sold OTC thus, supporting the expansion of the segment in the projected period.

By Therapeutic Category, the antiviral segment is estimated to lead the growth of the Zimbabwe pharmaceutical market during the analysis period. Antivirals are medications that help fight off certain viruses that can cause disease. Antivirals are preventive as well as treatment drugs. The growing prevalence of HIV, malaria, and respiratory infections has raised the demand for antiviral drugs. The recent outbreak of COVID-19 further increased the demand for an antiviral drugs. According to WHO, 257,156 confirmed cases of COVID-19 were reported till September 2022. Though the number of confirmed cases has declined in recent months, however, the pandemic is not over yet. In addition, the prevalence of other viral diseases is anticipated to strengthen the growth of the segment throughout the projected period.

By Distribution Channel, the hospital pharmacy segment is expected to have the highest share of the market. The growth of this segment is mainly attributed to the increasing visit to primary healthcare settings such as hospitals. Hospital pharmacies have most of the medications in stock and provide them at reasonable rates. As these are government-funded pharmacies, the cost of overall treatment decreases as most of the medications are generic. With the declining economy in Zimbabwe, individuals are preferring hospital pharmacies over other options thereby, helping the development of the segment.

Top Key Players Covered In Zimbabwe Pharmaceutical Market

- Bayer AG

- CAPS Pharmaceuticals

- Pfizer Inc

- Plus Five Pharmaceuticals

- ZimPharm Graniteside

- Pharmanova

- Gulf Drug

- Datlabs

- GlaxoSmithKline PLC

- Icon Pharmaceuticals

- Varichem

- Seasons Pharmaceuticals

- Graniteside Chemicals (Pvt) Ltd, and Other Major Players

Key Industry Developments In Zimbabwe Pharmaceutical Market

- In August 2024, Zimbabwe's Health and Child Care Minister, Dr. Douglas Mombeshora, announced at the 19th CII India-Africa Business Conclave that the country imports 90% of its pharmaceutical products from India but seeks partnerships to establish local production to reduce costs and expand access. Highlighting Zimbabwe’s central location as a potential hub for neighboring markets, Dr. Mombeshora emphasized the mutual benefits for both nations. Additionally, he called for collaborations in telemedicine to enhance Zimbabwe’s e-health platform and reduce the need for patients to travel to India for specialist care. The delegation, led by Vice President C.G.D.N. Chiwenga, also explored avenues for agricultural equipment and e-commerce development.

- In November 2024, Zimbabwe’s pharmaceutical industry, currently operating at 50% capacity, is poised for growth under the Zimbabwe Industrial Reconstruction and Growth Plan (ZIRGP), which includes a revolving fund partially financed by a sugar tax and streamlined registration processes to boost local production. The government aims to reduce reliance on imports, save up to $75 million annually through public procurement of locally produced medicines, and recapitalize the sector with $45 million. With market value projected to rise from $196.46 million in 2024 to $240.87 million by 2029, initiatives like the 2021-2025 Pharmaceutical Manufacturing Strategy and Zimbabwe's membership in the African Medicines Agency are set to drive innovation and self-sufficiency.

|

Zimbabwe Pharmaceutical Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 265.94 Mn. |

|

Forecast Period 2025-35 CAGR: |

4.5% |

Market Size in 2035: |

USD 431.58 Mn. |

|

Segments Covered: |

By Drug Type |

|

|

|

By Therapeutic Category |

|

||

|

By Distribution Channel |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Zimbabwe Pharmaceutical Market by Drug Type (2018-2035)

4.1 Zimbabwe Pharmaceutical Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Prescription Drugs

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 OTC Drugs

Chapter 5: Zimbabwe Pharmaceutical Market by Therapeutic Category (2018-2035)

5.1 Zimbabwe Pharmaceutical Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Cardiovascular Disorders

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Anti-viral

5.5 Respiratory Diseases

5.6 Others

Chapter 6: Zimbabwe Pharmaceutical Market by Distribution Channel (2018-2035)

6.1 Zimbabwe Pharmaceutical Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospital Pharmacies

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Retail Pharmacies

6.5 Online Pharmacies

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Zimbabwe Pharmaceutical Market Share by Manufacturer (2023)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 HEXCEL CORPORATION

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 ALCOA CORPORATION

7.4 ALUCOIL

7.5 3A COMPOSITES

7.6 FAIRFIELD METAL LLC

7.7 ALUBOND U.S.AALPOLIC MATERIALS

7.8 ALCOTEX INCARCONIC INC. (USA)

7.9 3A COMPOSITES USA (USA)

7.10 ALUCOBOND USA (USA)

7.11 MITSUBISHI CHEMICAL CORPORATION (ALPOLIC) (USA)

7.12 KINGERTAI GROUP (USA)

7.13 JYI SHYANG INDUSTRIAL COLTD. (TAIWAN)

7.14 ALUCOIL (USA)

7.15 SISTEMALUX S.A. (USA)

7.16 EUROBOND (USA)

7.17 ACM PANEL INC. (USA)

7.18 ALUMAX INDUSTRIAL COLTD. (USA)

7.19 SHANGHAI ALUBOND USA (USA)

7.20 VITRABOND (USA)

7.21 OTHER MAJOR PLAYERS.

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Zimbabwe Pharmaceutical Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 265.94 Mn. |

|

Forecast Period 2025-35 CAGR: |

4.5% |

Market Size in 2035: |

USD 431.58 Mn. |

|

Segments Covered: |

By Drug Type |

|

|

|

By Therapeutic Category |

|

||

|

By Distribution Channel |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||