Smart Data Center Market Synopsis

Smart Data Center Market Size Was Valued at USD 241.16 Billion in 2024 and is Projected to Reach USD 502.11 Billion by 2032, Growing at a CAGR of 9.6 % From 2025-2032.

A Smart Data Center is a facility equipped with advanced technologies and infrastructure to optimize energy usage, improve operational efficiency, enhance security, and enable remote monitoring and management of data center operations. It leverages various technologies such as Internet of Things (IoT), artificial intelligence (AI), and cloud computing to automate tasks, improve resource allocation, and provide real-time insights for better decision-making.

A Smart Data Center is a facility that uses advanced technologies like IoT sensors, artificial intelligence, and automation to optimize data center operations. These centers use techniques like real-time temperature and humidity data to reduce energy consumption, optimize server usage, and use renewable energy sources. They also use predictive maintenance to prevent equipment failures and minimize maintenance costs. They use advanced analytics and machine learning algorithms to optimize resource allocation, ensuring efficient computing.

Smart Data Center also incorporate enhanced security features like biometric authentication and intrusion detection systems. They enable real-time monitoring and management, enabling faster response times and effective resource allocation. They are highly scalable, allowing organizations to expand their infrastructure without significant costs or complexity. They also monitor environmental factors to ensure optimal equipment performance and longevity.

The rise of digital technologies has led to a surge in data generation, necessitating the development of Smart Data Centers. These centers provide efficient, scalable infrastructure for data storage, processing, and analysis. They minimize energy consumption and environmental impact, making them attractive for organizations. As IT infrastructure shifts to the cloud, there's a growing demand for data center services with high availability, scalability, and security.

Smart Data Centers offer real-time monitoring, predictive maintenance, and automated resource allocation, making them ideal for supporting cloud-based applications. They also prioritize data security, incorporating features like biometric authentication, encryption, and intrusion detection systems. These centers offer agility and scalability, enabling organizations to adapt to changing needs and market dynamics.

.webp)

Smart Data Center Market Trend Analysis

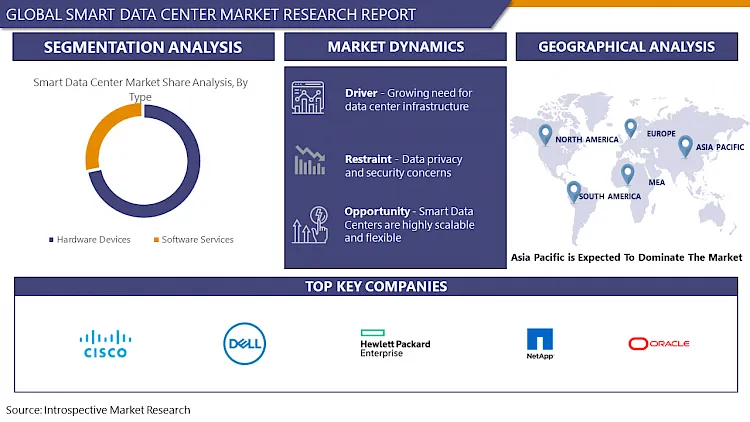

Growing Need for Data Center Infrastructure

- 3D printing materials are extensively used in the automotive industry to manufacture scaled models for testing. They are also used for components, such as bellows, front bumper, air conditioning ducting, suspension wishbone, dashboard interface, alternator mounting bracket, battery cover, etc. Automotive OEM manufacturers are using 3D printing materials for rapid prototyping. ?

- Owing to the advantages of the 3D printing process, such as low cost, less manufacturing time, reduced material wastage, etc., automotive manufacturers are moving toward the usage of this process. Some of the largest automotive manufacturers in the world, such as AUDI, Rolls Royce, Porsche, Hackrod, and many others, are using these materials for manufacturing spare parts and metal prototypes.

- The current slowdown in global automotive production has affected the market for polyester staple fiber because of the decreased demand for automotive fibers. Additionally, the current slowdown in automotive sales in countries such as China is further expected to hinder the demand for 3D printing materials. ?

- The pandemic has severely impacted the automotive sector globally; according to OICA (International Organization of Motor Vehicle Manufacturers), global production of vehicles in the third quarter of 2020 was around 50 million, a significant decrease compared to the production in the third quarter of 2019, which was around 65 million.

Restraints

Data Privacy and Security Concerns

- Data privacy and security concerns are arising from the collection, storage, processing, and transmission of sensitive information within Smart Data Centers. These concerns arise from the handling of vast amounts of sensitive data, such as customer data, intellectual property, and proprietary business information, which can result in financial losses, reputational damage, and legal liabilities.

- Smart Data Centers are also vulnerable to cyber-attacks, such as malware, ransomware, phishing, and insider threats. Organizations must comply with regulations and standards related to data privacy and security, such as GDPR, HIPAA, PCI DSS, and SOC. Insider threats can pose a risk, and organizations must implement robust access controls, monitoring, and training programs to mitigate these risks.

- Data encryption is also crucial, ensuring data remains unintelligible to unauthorized parties. Physical security measures, such as biometric authentication, surveillance cameras, access control systems, and perimeter fencing, are also essential.

Opportunity

Smart Data Centres Are Highly Scalable and Flexible

- Smart Data Centers enable organizations to quickly adjust their computing resources to accommodate demand fluctuations, ensuring optimal performance and user experience during high-demand periods. They also enable cost optimization by only paying for the resources they need when needed, avoiding overprovisioning hardware and capacity for future growth.

- The dynamic resource allocation ensures cost efficiency without sacrificing performance or reliability. Smart Data Centers also support business growth and innovation by enabling rapid deployment of new applications, services, and features, allowing businesses to experiment with new ideas, enter new markets, and respond quickly to changing customer needs and competitive pressures.

- Smart Data Centers are designed to seamlessly integrate with hybrid and multi-cloud environments, allowing organizations to leverage resources across on-premises data centers, private clouds, and public clouds, ensuring optimal performance, scalability, and cost efficiency.

Challenge

Legacy Infrastructure and Systems

- Organizations adopting Smart Data Center technologies face significant challenges due to outdated infrastructure and systems. These systems may not be compatible with advanced technologies like virtualization, cloud computing, and software-defined networking, leading to complexity and additional investment in retrofitting or upgrading.

- Legacy systems may lack the performance and scalability needed for modern workloads, resulting in bottlenecks, downtime, and reduced agility. They may also have outdated security features, making them vulnerable to cyber-attacks and data breaches. Maintaining and supporting legacy infrastructure can be costly and time-consuming, especially when vendors discontinue support for older products.

- Legacy systems may not meet current regulatory requirements and industry standards for data privacy, security, and environmental sustainability. Addressing these challenges requires careful planning, investment, and migration strategies. Prioritizing legacy modernization, retiring obsolete systems, and transitioning to more agile and scalable architectures aligned with Smart Data Center goals can help organizations navigate these complexities while minimizing risks and disruptions to business operations.

Smart Data Center Market Segment Analysis:

Smart Data Center Market Segmented on the basis of type, application, and end-users.

By Type, Software Services segment is expected to dominate the market during the forecast period

- The demand for software services to manage and optimize cloud-based data center environments is on the rise as organizations transition to cloud-based systems. Smart Data Center software services offer features like resource provisioning, monitoring, and optimization, which are crucial for efficient cloud-based operations.

- These services provide centralized management and automation capabilities, enabling organizations to streamline operations, improve efficiency, and reduce complexity across diverse IT environments. They also focus on efficiency and optimization, providing real-time insights into data center operations and automating routine tasks. Data analytics is also crucial in Smart Data Center operations, enabling organizations to identify trends, forecast demand, and make data-driven decisions.

- Software Services also emphasize security and compliance, offering features like encryption, threat detection, and access controls. As digital transformation initiatives continue, these services help organizations modernize their data center infrastructure, improve agility, and accelerate innovation by providing scalable, flexible, and automated solutions for managing IT resources.

By End User, IT and Telecommunications segment held the largest share

- The IT and telecommunications industries are increasingly utilizing Smart Data Centers to manage and optimize data center operations, addressing the growing volume of data generated by these networks. Rapid technological advancements, such as cloud computing, edge computing, 5G networks, IoT devices, and AI, drive the need for Smart Data Centers for real-time data processing, low-latency applications, and intelligent network management.

- The proliferation of digital services like streaming video, social media, e-commerce, and online gaming is driving exponential data traffic and consumption, making Smart Data Centers crucial for supporting these services. They offer opportunities for optimizing resource utilization, energy efficiency, and streamlining operations, helping organizations achieve business objectives while remaining competitive.

- Smart Data Centers meet regulatory compliance and security standards, providing advanced security features, compliance tools, and monitoring capabilities to ensure data integrity, confidentiality, and availability.

Smart Data Center Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast Period

- The Asia Pacific region is experiencing rapid digital transformation due to increasing internet penetration, smartphone adoption, and demand for digital services. This is driving the need for advanced data center infrastructure to support the growing volume of data generated and consumed by businesses and consumers.

- The region's largest IT and telecommunications markets, are investing in data center infrastructure to support the expansion of cloud computing, 5G networks, IoT devices, and other emerging technologies. The increasing adoption of cloud computing is driving demand for Smart Data Center solutions to help organizations manage and optimize their cloud-based infrastructure more effectively.

- Governments and enterprises in the region are making substantial investments in data center infrastructure to support economic growth, innovation, and digital transformation initiatives. The region is also focusing on energy efficiency and sustainability, offering Smart Data Center solutions that optimize energy usage, reduce carbon footprint, and meet regulatory requirements.

Smart Data Center Market Top Key Players:

- Cisco Systems, Inc. (US)

- Dell Technologies Inc. (US)

- Hewlett Packard Enterprise (HPE) Company (US)

- Hitachi Vantara Corporation (US)

- Oracle Corporation (US)

- NetApp, Inc. (US)

- Vertiv Co. (US)

- Nutanix, Inc. (US)

- Equinix, Inc. (US)

- CommScope Holding Company, Inc. (US)

- Dell EMC (US)

- Flexential Corporation (US)

- Digital Realty Trust, Inc. (US)

- Western Digital Corporation (US)

- IBM Corporation (US)

- Siemens AG (Germany)

- Rittal GmbH & Co. KG (Germany)

- Schneider Electric SE (France)

- Eaton Corporation plc (Ireland)

- Johnson Controls International plc (Ireland)

- Huawei Technologies Co., Ltd. (China)

- Lenovo Group Limited (China)

- Fujitsu Limited (Japan)

- NTT Ltd. (Japan)

- Quanta Computer Inc. (Taiwan), and Other Active Player

Key Industry Developments in the Smart Data Center Market:

- In February 2024, Siemens to unveil new products and partnerships to advance transformation to sustainable infrastructure.

- In July 2023, Dell Technologies introduced new offerings to help customers quickly and securely build generative AI (GenAI) models on-premises to accelerate improved outcomes and drive new levels of intelligence. New Dell Generative AI Solutions, expanding Helix announcement, span IT infrastructure, PCs and professional services to simplify the adoption of full-stack GenAI with large language models (LLM), meeting organizations wherever they are in their GenAI journey.

|

Global Smart Data Center Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

241.16 Bn |

|

Forecast Period 2024-32 CAGR: |

9.6 % |

Market Size in 2032: |

502.11 Bn |

|

Segments Covered: |

By Type |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Smart Data Center Market by Type (2018-2032)

4.1 Smart Data Center Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Hardware Devices

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Software Services

Chapter 5: Smart Data Center Market by End User (2018-2032)

5.1 Smart Data Center Market Snapshot and Growth Engine

5.2 Market Overview

5.3 BFSI

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 IT and Telecommunications

5.5 Transportation and Logistics

5.6 Manufacturing

5.7 Government and Defence

5.8 E-commerce

5.9 Healthcare

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Smart Data Center Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 GENERAL MILLS INC (U.S.)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 CONAGRA FOODS INC. (U.S.)

6.4 THE KRAFT HEINZ COMPANY (U.S.)

6.5 MARS INCORPORATED (U.S.)

6.6 TYSON FOODS INC. (U.S.)

6.7 KELLOGG COMPANY (U.S.)

6.8 CAMPBELL SOUP COMPANY (U.S.)

6.9 MCCAIN FOODS (CANADA)

6.10 BAKKAVOR FOODS LTD (UK)

6.11 NOMAD FOODS LTD. (UK)

6.12 JBS S.A. (BRAZIL)

6.13 PREMIER FOODS GROUP LTD. (UK)

6.14 GREENCORE GROUP PLC. (IRELAND)

6.15 UNILEVER (NETHERLANDS)

6.16 ORKLA ASA (NORWAY)

6.17 ITC LIMITED (INDIA)

6.18

Chapter 7: Global Smart Data Center Market By Region

7.1 Overview

7.2. North America Smart Data Center Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Type

7.2.4.1 Hardware Devices

7.2.4.2 Software Services

7.2.5 Historic and Forecasted Market Size by End User

7.2.5.1 BFSI

7.2.5.2 IT and Telecommunications

7.2.5.3 Transportation and Logistics

7.2.5.4 Manufacturing

7.2.5.5 Government and Defence

7.2.5.6 E-commerce

7.2.5.7 Healthcare

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Smart Data Center Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Type

7.3.4.1 Hardware Devices

7.3.4.2 Software Services

7.3.5 Historic and Forecasted Market Size by End User

7.3.5.1 BFSI

7.3.5.2 IT and Telecommunications

7.3.5.3 Transportation and Logistics

7.3.5.4 Manufacturing

7.3.5.5 Government and Defence

7.3.5.6 E-commerce

7.3.5.7 Healthcare

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Smart Data Center Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Type

7.4.4.1 Hardware Devices

7.4.4.2 Software Services

7.4.5 Historic and Forecasted Market Size by End User

7.4.5.1 BFSI

7.4.5.2 IT and Telecommunications

7.4.5.3 Transportation and Logistics

7.4.5.4 Manufacturing

7.4.5.5 Government and Defence

7.4.5.6 E-commerce

7.4.5.7 Healthcare

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Smart Data Center Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Type

7.5.4.1 Hardware Devices

7.5.4.2 Software Services

7.5.5 Historic and Forecasted Market Size by End User

7.5.5.1 BFSI

7.5.5.2 IT and Telecommunications

7.5.5.3 Transportation and Logistics

7.5.5.4 Manufacturing

7.5.5.5 Government and Defence

7.5.5.6 E-commerce

7.5.5.7 Healthcare

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Smart Data Center Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Type

7.6.4.1 Hardware Devices

7.6.4.2 Software Services

7.6.5 Historic and Forecasted Market Size by End User

7.6.5.1 BFSI

7.6.5.2 IT and Telecommunications

7.6.5.3 Transportation and Logistics

7.6.5.4 Manufacturing

7.6.5.5 Government and Defence

7.6.5.6 E-commerce

7.6.5.7 Healthcare

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Smart Data Center Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Type

7.7.4.1 Hardware Devices

7.7.4.2 Software Services

7.7.5 Historic and Forecasted Market Size by End User

7.7.5.1 BFSI

7.7.5.2 IT and Telecommunications

7.7.5.3 Transportation and Logistics

7.7.5.4 Manufacturing

7.7.5.5 Government and Defence

7.7.5.6 E-commerce

7.7.5.7 Healthcare

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Global Smart Data Center Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

241.16 Bn |

|

Forecast Period 2024-32 CAGR: |

9.6 % |

Market Size in 2032: |

502.11 Bn |

|

Segments Covered: |

By Type |

|

|

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||