Retort Packaging Market Overview

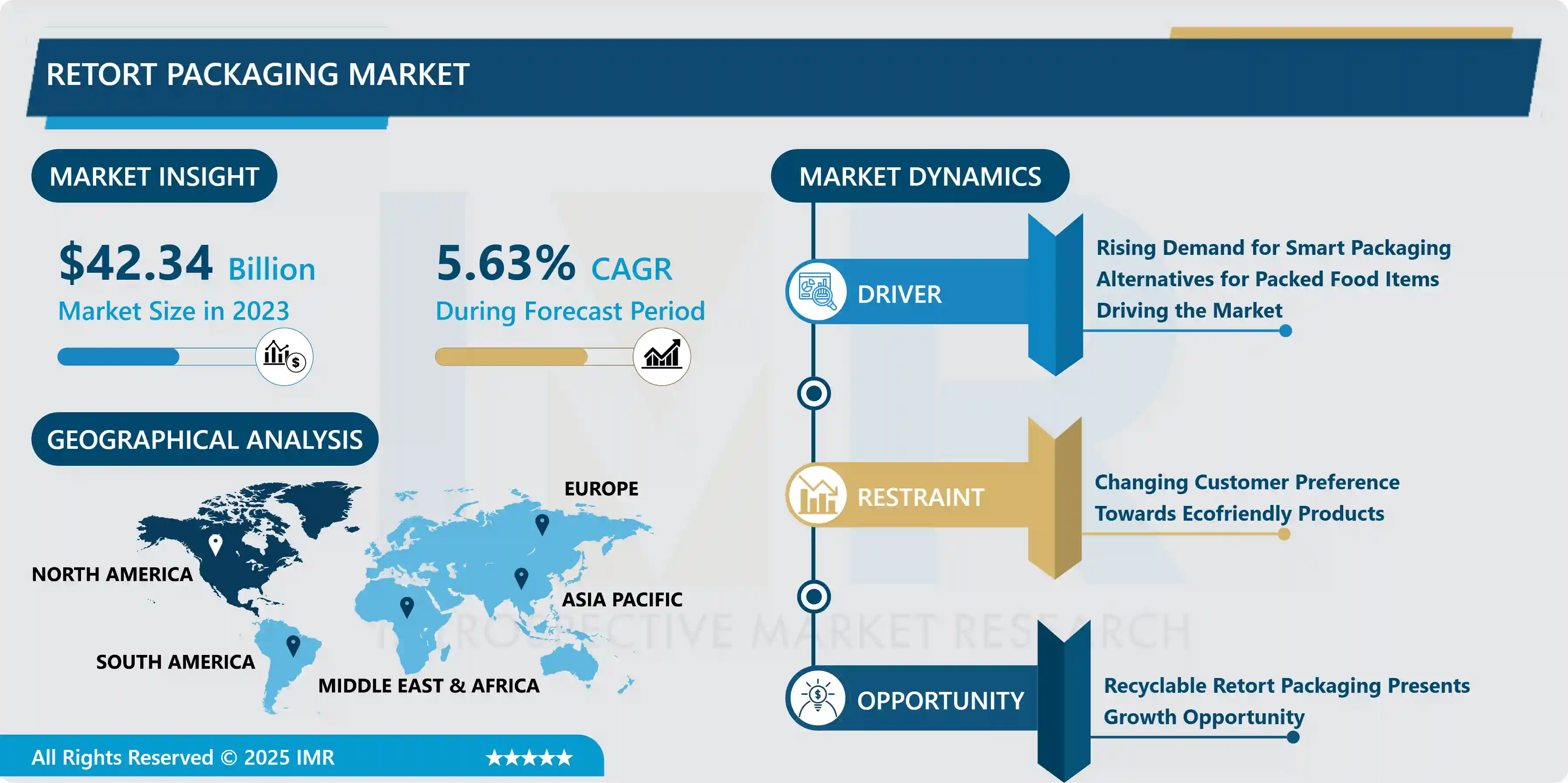

Global Retort Packaging Market Size Was Valued at USD 42.34 Billion In 2023 And Is Projected to Reach USD 69.32 Billion By 2032, Growing at A CAGR of 5.63% From 2024 To 2032.

Retort packaging is an advanced food sterilization method that involves heating food and its packaging to high temperatures inside a pressure vessel, or retort. This process typically reaches 240–250°F (115–121°C), effectively sterilizing the contents and creating a shelf-stable product that can be stored at room temperature for one to two years. The technique is designed to preserve food quality while ensuring safety and extending shelf life.

The materials used in retort packaging are specialized laminates combining flexible plastic and metal foils. Common components include polyester for durability, aluminum foil for a moisture and oxygen barrier, and polypropylene as a sealing layer. This multi-layered structure provides the necessary strength, heat resistance, and protection to withstand the high-pressure sterilization process.

Retort packaging is widely used as a modern alternative to traditional canning. It accommodates various processed foods, such as meat products, soups, sauces, and ready-to-eat meals. The flexible and compact design of retort pouches enhances portability and convenience, making them popular in the food service industry, military rations, and consumer markets for packaged meals.

In terms of sustainability, retort packaging offers significant advantages. It requires less heat and energy for sterilization compared to conventional canning, reducing the environmental footprint. The lightweight structure also minimizes transportation costs and emissions, while certain materials are recyclable, contributing to a eco-friendlier packaging solution.

Market Dynamics And Factors For Retort Packaging Market

Drivers:

Rising Demand For Smart Packaging Alternatives For Packed Food Items Driving The Market

- Because cans and jars are large and bulky, retort packaging is a superior alternative to traditional canning processes. They take up a lot of shelf space, which raises storage and shipping expenses, whereas retort pouches are light and take up less room. The packed items are sterilized using a fast heat transfer method. The retort pouches' small shape helps to speed up the sterilizing process. These characteristics of retort pouches may help them gain traction as food storage alternatives to cans and jars. These factors are expected to enhance demand for retort pouches in the food and beverage sector, which will support the retort packaging market's growth in the future years. Globally, the demand for packaged food that is either raw or cooked inside a retort pouch is rapidly increasing. Customers' lives are changing as a result of their demanding schedules, and an increasing number of consumers do not want to spend much time cooking. These factors are likely to boost demand for processed foods, resulting in increased demand and favorable growth for the retort packaging market throughout the forecast period.

Restraints:

- Changing preference of customers towards eco-friendly packaging alternatives as a sustainable product which are either made from recycled material or bio-degradable solutions. As developed economies focus on the sustainable goals to meet the environmental pact, plastic-free products including sustainable packaging and polyamide free products taking the grip on the market, which is a restraining factor for the retort packaging market, Although eco-friendly reusable packaging material is being introduced by companies such as Mondi Inc and Amcor. Therefore, such factors are expected to restrain the growth of the Retort Packaging Market.

Opportunities:

- Recyclable Retort Packaging possesses bright growth opportunities as sustainability norm is getting popular in the market. Many of the market leaders are pumping the money into a recyclable product lineup. The cyclos-HTP Institute, an independent testing lab, has certified AmLite HeatFlex Recyclable as ecological, and it complies with the CEFLEX Consortium's recently issued packaging requirements for a circular economy. It may be readily recycled in numerous European nations, including Germany, Austria, Italy, Norway, and the Netherlands, where plastic collecting systems already exist. With recyclable products are getting popular, related raw material selection has become crucial. Because aluminum was not a possibility and paper couldn't endure the steam retort process, companies are switching to a complete polyolefin construction. PP and PE are polyolefins, and bags and pouches constructed of these materials are recycled in many countries nowadays. The challenge in switching to polyolefins for retort processing is that only PP has a melting point greater than 130 degrees Celsius, which is easily attained for retort processing. Therefore, the use of PP and PE with recyclable products creates major opportunities for Retort Packaging Market.

Challenges:

- Initial machinery costs and process complexity are two main hurdles in retort packing. Filling, heat treatment, and tensile strength testing equipment are all required. These devices are both expensive to buy and to keep running. Another possible stumbling block is production complexity. Manufacturers must consider various factors when heat treating sealed pouches, including residual air and package thickness. Slower filling speeds and the necessity for additional protection while transportation is two other possible issues. Filling procedures are slower than those used in canning. You may need to give extra wrapping during distribution depending on the type of container you choose to reduce the risks of unintentional puncture.

Segmentation Analysis of Retort Packaging Market

- By Type, Pouches segment dominating the Retort Packaging Market. Because of various advantages such as aesthetics, performance, and cost, the pouch packaging type is expected to increase at the fastest pace throughout the projection period. The overall design and aesthetics of pouches make them a fantastic product promotion tool, and demand is projected to grow in the future years. Pouches help to differentiate products by providing wide surfaces on which high-quality images may be printed, enticing customers, particularly in supermarkets and convenience stores where people make rapid purchase decisions. These pouches also have convenience and usefulness elements such as spouts, rip notches, and zippers. Flat retort pouches come in a variety of shapes and sizes, including pillow pouches, four-side-seal pouches, and three-side-seal pouches.

- By Material, Polypropylene is expected to be dominating the retort packaging market. As companies are opting for more sustainable alternatives to use raw materials. Polypropylene acts as a sealing layer and provides flexibility and strength to the pouch. Polypropylene is a tough and robust plastic material that assists in retaining the freshness of various food items owing to which it is widely used in manufacturing retort pouches. On the inside of the pack, PP film is in direct contact with the food product and provides an exceptionally strong heat seal that can withstand all of the pressure and temperature demands of retorting, flexibility, strength, and inertness on the packaged cooked meat product in contact contributing to a product shelf-life at least equal to that of retorted cans, and packages.

- By End User, the Food segment is dominating the Retort Packaging Market. The packaging market has grown significantly in the food sector. Soups, sauces, infant food, dry-ready meals, frozen ready meals, chilled ready meals, meal replacement products, and dairy products are among the many foods packaged in retort pouches. The application of pet food is also widely employed in the market. The rising popularity of the notion of "humanizing" pets has increased the number of individuals who own pets and provide them high-quality food. Furthermore, the growing trend of pet adoption, particularly among households with one kid and working parents, is expected to boost demand for pet food, favouring market expansion.

Regional Analysis of Retort Packaging Market:

- North America is dominating the retort packaging market. Increased urbanization, hectic work lives, rising single-household populations, and rising consumer buying power have accelerated the expansion of pre-packaged products, which are often packaged in stand-up retort pouches, hence acting as significant drivers for the retort pouch sector. Because it is a highly handy and portable packaging option, retort packaging is quickly gaining favor. Many consumers in the nation prefer flexible, stand-up pouches to rigid packaging. Whether for snack food, beverage, baby food, or industrial oils and lubricants, consumers have increased demand for stand-up pouches tremendously over the last decade. Food, pharmaceutical, and nutraceutical goods ingested by people and animals are regulated by the Department of Health and Human Services in the United States. The Food and Drug Administration (FDA) or the United States Department of Agriculture (USDA) is in charge of this (USDA). Under the most extreme temperatures, the retort package regulation is fairly stringent, requiring the components and procedures to be listed under FDA rule 21 CFR 177.1390. The usage of retort pouches is increasing in Canada because of the growing acceptance of flexible packaging techniques in a variety of industries, including retail, pharmaceuticals, food and beverage, and pet food. Approximately 75% of the country's food supply is made up of packaged, processed foods. There has also been a shift in eating patterns, with a rise in the intake of ultra-processed, ready-to-eat meals, which are often energy-dense and rich in fat, sugar, and salt. These meals are commonly packaged in retort pouches, which are an efficient method of packaging food goods with a long shelf life.

- The Asia Pacific is the fastest-growing region in retort packaging due to the strong demand from countries such as China, Australia, South Korea, and Japan. The region has more than half of the world's population and there has been an increase in the demand for convenient products due to hectic work life and increasing per capita income. The Indian market has seen a sudden boost in the demand for retort packaging as the growing urban population creates significant demand for packaged food items for which local food manufacturers opt the retort packaging to give high standard products. Floeter, Foodpropack is the local Indian retort packaging company that satisfies the regional demand and is expected to contribute the market growth. Consumers in the region are looking for ready meal products that can be consumed without much work; hence the demand for retort packages is growing in the region.

Key Players Covered In Retort Packaging Market:

- Amcor plc.

- Mondi Group

- Huhtamaki Oyj

- Sealed Air Corporation

- Winpak Ltd

- Sonoco Products Company

- Coveris Holdings S.A.

- Proampac LLC

- Tredegar Corporation

- Avonflex

- ALLIEDFLEX Technologies Inc.

- DNP America LLC.

- Clifton Packaging Group Ltd

- Printpack Inc.

- Paharpur 3P

- Constantia Flexibles Group GmbH

- Flair Flexible Packaging Corporation

- HPM Global Inc.

- LD PACK Co. Ltd and other major players.

Key Industry Developments In Retort Packaging Market

- In April 2023, Huhtamäki Oyj launched three innovative mono-material flexible packaging solutions, emphasizing eco-friendly design and improved recyclability. These packaging solutions were developed to reduce resource consumption during production, aligning with sustainability goals and addressing the growing demand for environmentally conscious packaging. By focusing on recyclability, the company aimed to enhance the circular economy and minimize environmental impact. This initiative demonstrated Huhtamäki’s commitment to advancing sustainable packaging technologies and providing effective, resource-efficient alternatives for retort packaging applications.

|

Global Retort Packaging Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 42.34 Bn. |

|

Forecast Period 2024-32 CAGR: |

5.63% |

Market Size in 2032: |

USD 69.32 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Material |

|

||

|

By End-Use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Retort Packaging Market by Type (2018-2032)

4.1 Retort Packaging Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Pouches

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Trays

4.5 Cartons

Chapter 5: Retort Packaging Market by Material (2018-2032)

5.1 Retort Packaging Market Snapshot and Growth Engine

5.2 Market Overview

5.3 PET

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Polypropylene

5.5 Aluminum Foil

5.6 PA

5.7 PE

5.8 Paperboard

Chapter 6: Retort Packaging Market by End-Use (2018-2032)

6.1 Retort Packaging Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Food

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Beverages

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Retort Packaging Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 NETZSCH PUMPS & SYSTEMS

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 SEEPEX GMBH

7.4 HALLIBURTON

7.5 WEATHERFORD INTERNATIONAL

7.6 VIKING PUMP INCSULZER LTDGEA GROUP

7.7 PSG DOVER

7.8 NATIONAL OILWELL VARCO (NOV)

7.9 TUTHILL CORPORATION

7.10 BAKER HUGHES

7.11 HUNAN OIL PUMP COLTDXYLEM INCKRACHT GMBH

7.12 WANGEN PUMPS

7.13 SPX FLOW

7.14 INGERSOLL RAND

7.15 ITT INCEMERSON ELECTRIC COGRUNDFOS PUMPS CORPORATION

7.16 AND OTHER ACTIVE PLAYER.

Chapter 8: Global Retort Packaging Market By Region

8.1 Overview

8.2. North America Retort Packaging Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Pouches

8.2.4.2 Trays

8.2.4.3 Cartons

8.2.5 Historic and Forecasted Market Size by Material

8.2.5.1 PET

8.2.5.2 Polypropylene

8.2.5.3 Aluminum Foil

8.2.5.4 PA

8.2.5.5 PE

8.2.5.6 Paperboard

8.2.6 Historic and Forecasted Market Size by End-Use

8.2.6.1 Food

8.2.6.2 Beverages

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Retort Packaging Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Pouches

8.3.4.2 Trays

8.3.4.3 Cartons

8.3.5 Historic and Forecasted Market Size by Material

8.3.5.1 PET

8.3.5.2 Polypropylene

8.3.5.3 Aluminum Foil

8.3.5.4 PA

8.3.5.5 PE

8.3.5.6 Paperboard

8.3.6 Historic and Forecasted Market Size by End-Use

8.3.6.1 Food

8.3.6.2 Beverages

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Retort Packaging Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Pouches

8.4.4.2 Trays

8.4.4.3 Cartons

8.4.5 Historic and Forecasted Market Size by Material

8.4.5.1 PET

8.4.5.2 Polypropylene

8.4.5.3 Aluminum Foil

8.4.5.4 PA

8.4.5.5 PE

8.4.5.6 Paperboard

8.4.6 Historic and Forecasted Market Size by End-Use

8.4.6.1 Food

8.4.6.2 Beverages

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Retort Packaging Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Pouches

8.5.4.2 Trays

8.5.4.3 Cartons

8.5.5 Historic and Forecasted Market Size by Material

8.5.5.1 PET

8.5.5.2 Polypropylene

8.5.5.3 Aluminum Foil

8.5.5.4 PA

8.5.5.5 PE

8.5.5.6 Paperboard

8.5.6 Historic and Forecasted Market Size by End-Use

8.5.6.1 Food

8.5.6.2 Beverages

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Retort Packaging Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Pouches

8.6.4.2 Trays

8.6.4.3 Cartons

8.6.5 Historic and Forecasted Market Size by Material

8.6.5.1 PET

8.6.5.2 Polypropylene

8.6.5.3 Aluminum Foil

8.6.5.4 PA

8.6.5.5 PE

8.6.5.6 Paperboard

8.6.6 Historic and Forecasted Market Size by End-Use

8.6.6.1 Food

8.6.6.2 Beverages

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Retort Packaging Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Pouches

8.7.4.2 Trays

8.7.4.3 Cartons

8.7.5 Historic and Forecasted Market Size by Material

8.7.5.1 PET

8.7.5.2 Polypropylene

8.7.5.3 Aluminum Foil

8.7.5.4 PA

8.7.5.5 PE

8.7.5.6 Paperboard

8.7.6 Historic and Forecasted Market Size by End-Use

8.7.6.1 Food

8.7.6.2 Beverages

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Retort Packaging Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 42.34 Bn. |

|

Forecast Period 2024-32 CAGR: |

5.63% |

Market Size in 2032: |

USD 69.32 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Material |

|

||

|

By End-Use |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||