Plant-Based Protein Market Synopsis

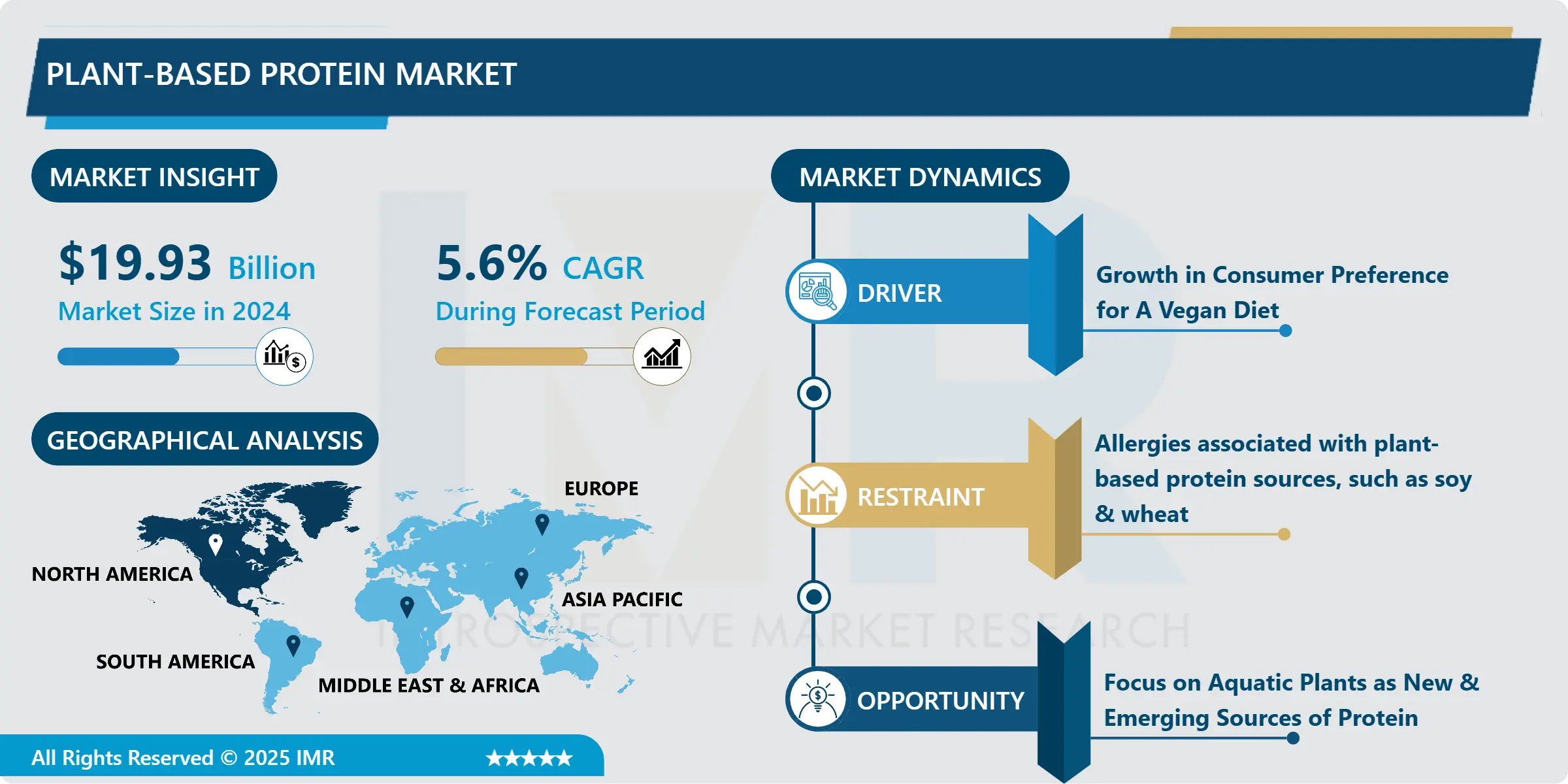

Plant-Based Protein Market Size Was Valued at USD 19.93 Billion in 2024, and is Projected to Reach USD 30.82 Billion by 2032, Growing at a CAGR of 5.6% From 2025-2032.

Plant-based protein refers to the protein derived from plant sources such as legumes (beans, lentils), nuts, seeds, grains, and certain vegetables. It serves as an essential dietary component for individuals opting for a vegetarian or vegan lifestyle and also forms a significant part of diverse diets worldwide. These proteins are rich in nutrients like fiber, vitamins, minerals, and antioxidants, providing a holistic nutritional package.

Plant-based proteins offer a wide variety of options, enabling individuals to meet their protein requirements without relying on animal products. They contribute to sustainable food choices by reducing the environmental impact associated with animal agriculture. Additionally, incorporating a diverse range of plant-based proteins in one's diet can offer numerous health benefits, including lower risks of certain chronic diseases like heart disease and type 2 diabetes, while promoting overall well-being.

The global plant-based protein market has experienced remarkable growth in recent years, driven by a surge in consumer interest in sustainable, ethical, and healthier food choices. This market encompasses a wide array of plant-derived protein sources, including soy, pea, wheat, canola, and others, catering to various dietary preferences such as vegetarian, vegan, and flexitarian lifestyles. This surge in demand has been fuelled by increasing awareness of the environmental impact of animal agriculture, coupled with a growing emphasis on personal health and wellness.

Several factors contribute to the expansion of the plant-based protein market, including innovative product development, technological advancements in food processing, and a shift in consumer attitudes toward more plant-centric diets. Notably, food companies and manufacturers are investing heavily in research and development to create appealing plant-based alternatives to meat, dairy, and other animal-based products. This expansion has led to a broader availability of plant-based protein options in supermarkets, restaurants, and food service establishments worldwide. As consumer preferences continue to evolve and the focus on sustainability intensifies, the plant-based protein market is expected to maintain its upward trajectory, offering diverse and accessible alternatives to traditional animal-based proteins.

Global Plant-Based Protein Market Trend Analysis

Growth in Consumer Preference for a Vegan Diet

- The burgeoning consumer preference for a vegan diet has emerged as a significant driving force behind the exponential growth of the global plant-based protein market. A fundamental shift in dietary choices is being witnessed worldwide, with an increasing number of individuals opting for plant-based lifestyles for various reasons. Concerns about animal welfare, environmental sustainability, and personal health are pivotal factors propelling this shift. The vegan diet, which abstains from all animal products, including meat, dairy, eggs, and other animal-derived ingredients, relies heavily on plant-based proteins to meet nutritional needs.

- This growing consumer inclination towards veganism has led to an upsurge in demand for plant-based protein alternatives. Consumers are actively seeking protein-rich plant sources such as soy, pea, lentils, and nuts to replace or reduce their consumption of animal-based proteins. This shift in dietary habits is reflected in the increased availability and diversity of plant-based protein products in the market, including plant-based meat substitutes, dairy alternatives, and protein-enriched snacks. As the awareness of the ethical, environmental, and health benefits associated with a vegan diet continues to spread, the demand for plant-based protein is projected to soar, further propelling the growth and expansion of the global plant-based protein market.

Focus on Aquatic Plants as New & Emerging Sources of Protein

- The exploration of aquatic plants as novel and emerging sources of protein has garnered significant attention in recent years. With rising concerns about food sustainability and the need for alternative protein sources, aquatic plants present a promising avenue due to their nutritional value and efficient resource utilization. Species like seaweed, algae, water lentils, and duckweed are gaining traction as they offer high protein content along with essential vitamins, minerals, and omega-3 fatty acids.

- Aquatic plants have the advantage of requiring minimal land, water, and resources for cultivation compared to traditional crops. Their rapid growth rates and ability to thrive in diverse aquatic environments make them a sustainable and eco-friendly protein source. Additionally, ongoing research and technological advancements are focusing on refining extraction methods and enhancing the palatability of these aquatic plants to make them more appealing for consumption. As interest and investment in alternative protein sources continue to grow, the potential for aquatic plants to contribute significantly to the global protein market is becoming increasingly evident, positioning them as a compelling and viable option for meeting future nutritional demands.

Global Plant-Based Protein Market Segment Analysis:

Global Plant-Based Protein Market Segmented on the basis of Source, Type, Form, Nature, Application and Region.

By Source, Soy segment is expected to dominate the market during the forecast period

- The dominance of soy within this segment is also propelled by its extensive cultivation and global availability. Its adaptability to different climates and regions, coupled with efficient farming practices, has ensured a consistent and substantial supply chain. Moreover, the innovations in soy-based products, such as tofu, soy milk, and meat substitutes, have significantly contributed to its market stronghold. While wheat and pea also play significant roles in various sectors, soy's widespread use and adaptability have positioned it as the primary source within this particular market segment.

By Type, isolates segment held the largest share in 2024

- Isolates have emerged as the go-to choose within the plant-based protein market, owing to their exceptional purity and versatility. These concentrated protein sources are prized for their pivotal role as primary ingredients in the creation of an array of products, including meat substitutes, dairy alternatives, and sports nutrition offerings. Their appeal lies not only in their high protein content but also in their neutral flavour profile and remarkable solubility, attributes that enable seamless integration into various food and beverage formulations

Global Plant-Based Protein Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- The North American market has been a pioneer in driving the plant-based protein industry. The United States and Canada have witnessed a surge in consumer demand for plant-based products due to health consciousness, environmental concerns, and animal welfare considerations.

- Major players in this region have introduced a wide array of plant-based protein products, including soy-based, pea-based, and others, targeting both retail and foodservice sectors.

Global Plant-Based Protein Market Top Key Players:

- ADM (US)

- Cargill, Incorporated (US)

- International Flavors & Fragrances Inc. (US)

- Ingredion (US)

- AMCO Proteins (US)

- Axiom Foods, Inc (US)

- The Green Labs LLC. (US)

- Nutraferma, Inc. (US)

- MycoTechnology (US)

- The Green Labs LLC. (US)

- PURIS (US)

- AGT Food and Ingredients (Canada)

- Burcon NutraScience Corporation (Canada)

- Roquette Frères (France)

- Biopress SAS (France)

- Glanbia plc (Ireland)

- Kerry Group PLC (Ireland)

- BENEO GmbH (Germany)

- Emsland Group (Germany)

- Südzucker AG (Germany)

- European Protein A/S (Denmark)

- Australian Plant Proteins Pty Ltd (Australia)

- Wilmar International Ltd. (Singapore)

- Crown Soya Protein Group (China)

- Biopress SAS (France)

- Other Active Players

Key Industry Developments in the Global Plant-Based Protein Market:

- In April 2022, ADM made an investment of USD 300 million to boost the production of alternative proteins at its plant in Decatur, Illinois, which will double the facility’s soy extrusion capacity. ADM, as part of the investment, is also building a Protein Innovation Center, including labs, test kitchens, and pilot-scale production capabilities, which will boost the company’s R&D capabilities.

- In April 2022, Ingredion expanded its production capacity by setting up a new manufacturing plant at Vanscoy, Canada, through the acquisition of Verdient Foods (Canada). This strategic initiative would vastly increase the company’s production capacity to produce plant-based protein.

|

Plant-Based Protein Market |

||||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 19.93 Bn. |

|

|

CAGR (2025-2032) : |

5.6% |

Market Size in 2032: |

USD 30.82 Bn. |

|

|

Segments Covered: |

By Source |

|

|

|

|

By Type |

|

|

||

|

By Form |

|

|

||

|

By Region |

|

|

||

|

Key Market Drivers: |

|

|||

|

Key Market Restraints: |

|

|||

|

Key Opportunities: |

|

|||

|

Companies Covered in the Report: |

|

|||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Plant-Based Protein Market by Source (2018-2032)

4.1 Plant-Based Protein Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Soy

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Wheat

4.5 Pea

Chapter 5: Plant-Based Protein Market by Type (2018-2032)

5.1 Plant-Based Protein Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Concentrates

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Isolates

5.5 Texture

Chapter 6: Plant-Based Protein Market by Form (2018-2032)

6.1 Plant-Based Protein Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Dry

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Liquid

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Plant-Based Protein Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 CISCO SYSTEMS INC. (UNITED STATES)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 NOTION. (UNITED STATES)

7.4 HELIUM SYSTEM INC. (UNITED STATES)

7.5 SAMSARA NETWORKS INC. (UNITED STATES)

7.6 BEEP INC. (UNITED STATES)

7.7 DELL TECHNOLOGIES INC. (UNITED STATES)

7.8 HEWLETT PACKARD ENTERPRISE DEVELOPMENT LP (UNITED STATES)

7.9 UBIQUITI INC. (UNITED STATES)

7.10 INTEL CORPORATION (UNITED STATES)

7.11 TEXAS INSTRUMENTS INCORPORATED (UNITED STATES)

7.12 MICROCHIP TECHNOLOGY INC. (UNITED STATES)

7.13 HUAWEI TECHNOLOGIES COLTD. (CHINA)

7.14 NXP SEMICONDUCTORS N.V. (NETHERLANDS)

7.15 QUECTEL WIRELESS SOLUTIONS COLTD. (CHINA)

7.16 SIERRA WIRELESS INC. (CANADA)

7.17 STMICROELECTRONICS N.V. (SWITZERLAND)

7.18 TELIT COMMUNICATIONS PLC (UNITED KINGDOM)

7.19 TOSHIBA CORPORATION (JAPAN)

7.20 TE CONNECTIVITY LTD. (SWITZERLAND)

7.21 ESTIMOTE INC. (POLAND)

7.22 ADVANTECH COLTD. (TAIWAN)

7.23 AAEON TECHNOLOGY INC. (TAIWAN)

7.24 NEXCOM INTERNATIONAL CO. LTD. (TAIWAN)

7.25 EUROTECH S.P.A. (ITALY)

7.26 ADLINK TECHNOLOGY INC. (TAIWAN)

Chapter 8: Global Plant-Based Protein Market By Region

8.1 Overview

8.2. North America Plant-Based Protein Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Source

8.2.4.1 Soy

8.2.4.2 Wheat

8.2.4.3 Pea

8.2.5 Historic and Forecasted Market Size by Type

8.2.5.1 Concentrates

8.2.5.2 Isolates

8.2.5.3 Texture

8.2.6 Historic and Forecasted Market Size by Form

8.2.6.1 Dry

8.2.6.2 Liquid

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Plant-Based Protein Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Source

8.3.4.1 Soy

8.3.4.2 Wheat

8.3.4.3 Pea

8.3.5 Historic and Forecasted Market Size by Type

8.3.5.1 Concentrates

8.3.5.2 Isolates

8.3.5.3 Texture

8.3.6 Historic and Forecasted Market Size by Form

8.3.6.1 Dry

8.3.6.2 Liquid

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Plant-Based Protein Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Source

8.4.4.1 Soy

8.4.4.2 Wheat

8.4.4.3 Pea

8.4.5 Historic and Forecasted Market Size by Type

8.4.5.1 Concentrates

8.4.5.2 Isolates

8.4.5.3 Texture

8.4.6 Historic and Forecasted Market Size by Form

8.4.6.1 Dry

8.4.6.2 Liquid

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Plant-Based Protein Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Source

8.5.4.1 Soy

8.5.4.2 Wheat

8.5.4.3 Pea

8.5.5 Historic and Forecasted Market Size by Type

8.5.5.1 Concentrates

8.5.5.2 Isolates

8.5.5.3 Texture

8.5.6 Historic and Forecasted Market Size by Form

8.5.6.1 Dry

8.5.6.2 Liquid

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Plant-Based Protein Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Source

8.6.4.1 Soy

8.6.4.2 Wheat

8.6.4.3 Pea

8.6.5 Historic and Forecasted Market Size by Type

8.6.5.1 Concentrates

8.6.5.2 Isolates

8.6.5.3 Texture

8.6.6 Historic and Forecasted Market Size by Form

8.6.6.1 Dry

8.6.6.2 Liquid

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Plant-Based Protein Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Source

8.7.4.1 Soy

8.7.4.2 Wheat

8.7.4.3 Pea

8.7.5 Historic and Forecasted Market Size by Type

8.7.5.1 Concentrates

8.7.5.2 Isolates

8.7.5.3 Texture

8.7.6 Historic and Forecasted Market Size by Form

8.7.6.1 Dry

8.7.6.2 Liquid

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Plant-Based Protein Market |

||||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 19.93 Bn. |

|

|

CAGR (2025-2032) : |

5.6% |

Market Size in 2032: |

USD 30.82 Bn. |

|

|

Segments Covered: |

By Source |

|

|

|

|

By Type |

|

|

||

|

By Form |

|

|

||

|

By Region |

|

|

||

|

Key Market Drivers: |

|

|||

|

Key Market Restraints: |

|

|||

|

Key Opportunities: |

|

|||

|

Companies Covered in the Report: |

|

|||