Luxury Goods Market Synopsis

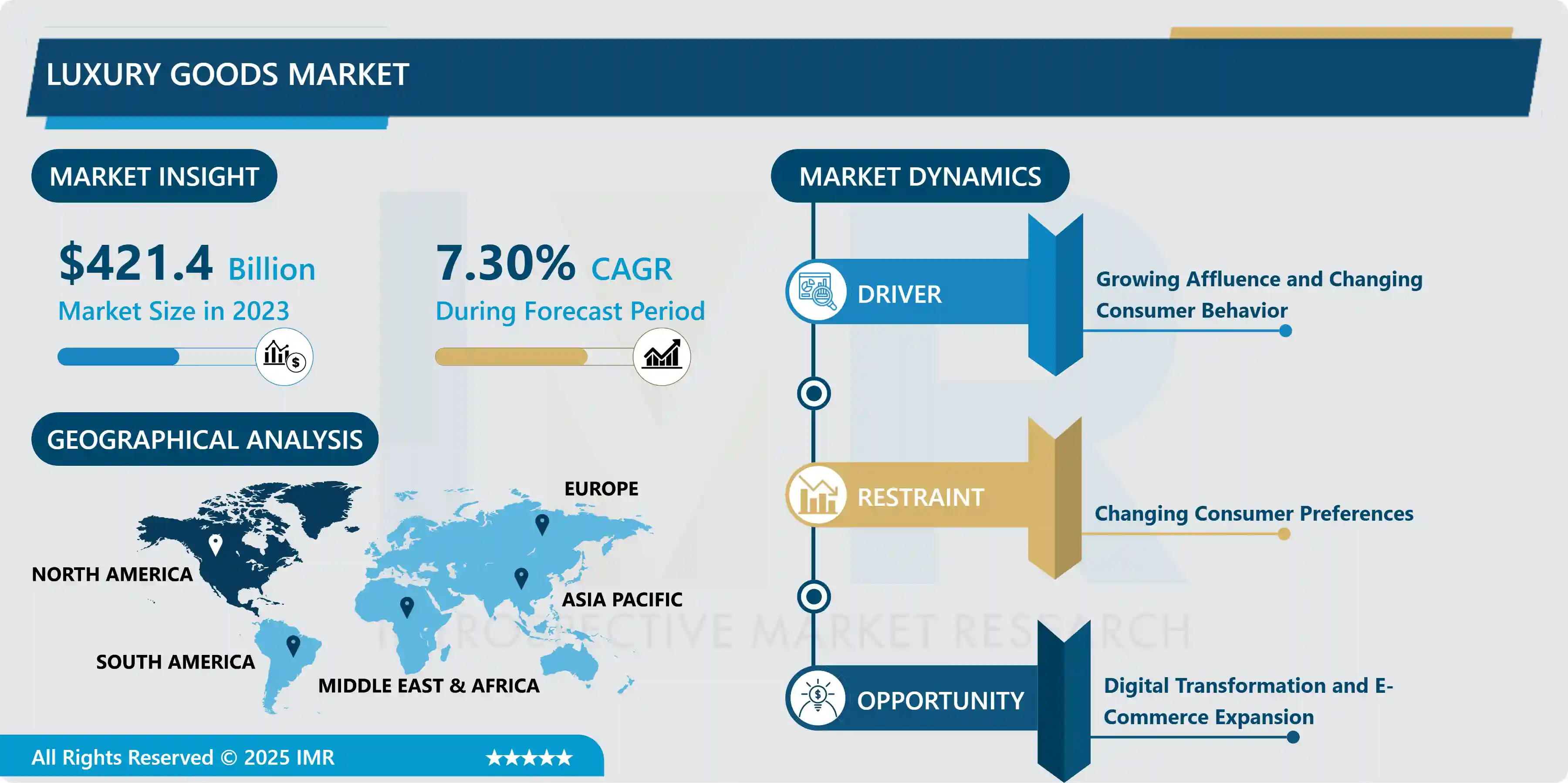

Luxury Goods Market Size Was Valued at USD 421.4 Billion in 2023, and is Projected to Reach USD 794.50 Billion by 2032, Growing at a CAGR of 7.3% From 2024-2032.

Luxury Goods may be defined as the products which meet with quality, availability, and price as compared to the other general products and services where the latter refers to the goods or services of better quality, scarce in supply and costs than the common goods. They are considered as being luxurious, fashionable, well made and are target at the consumers that look for the brands that are unique and have historical backing and are known for their designs. These are things such as designer wears, jewelries, exotic car manufactures and high end accessories among others.

Luxury personal accessories’ market has been growing at a very significant rate in the last few years boosted by inflationary incomes, shifting consumer trends, and the achievement of wealth thresholds in the developing world. Luxury product market can be described as a broad category of products such as apparel and accessories, leather products, fashion accessories, timepieces, and jewelry, cosmetics and fragrances. Another key tendency common with the market is what can be called experiential luxury, which means that consumers are interested within the product not only as an object but as an experience. Luxury travel, food and beverages, and, luxury entertainment and social activities have become core components of luxurious possessions and services turning luxurious products to luxury experiences. However, because of an enhanced awareness in the aspect of sustainable development, some of the luxurious brands have been applying sustainable methods in sourcing for raw materials, production and even the supply chain. Companies no longer sell products and services to the millennials and generation Z without the company being held accountable for environmental and social implications. As a result, Luxe brands are creating sustainable markets as they add vegan leather accessories and organic beauty products to CSR initiatives.

The industry of luxury products has continued evolved Digitization, here the use of online tools and media in the marketing of luxury brands. Whereas earlier luxury products could be availed only through the department store format, today the world of luxury retail has been opened up to the internet. As of today, most luxury firms have adapted omnichannel marketing, which can be described as the shopping experience between the physical and the virtual world to consumers. The following are some of the marketing strategies that have reached the market to the target consumers; social marketing, influence marketing and digital marketing to the affluent consumers. Other technologies that are also assisting in changing the image of luxury shopping are Augmented reality and virtual reality in which the client can be feel the feel of the luxury goods such as jewelries or apparels even they cannot afford the original item. However the current position has been made especially by the increase in technological factor since it brings issues like fake luxury products in the online shop. To ensure that customers are shielded from substandard goods and patent rights protected most luxury firms have adopted innovative solutions such as blockchain.

The region of Asia-Pacific continues to play significant roles in defining the future direction of the luxury products market especially in the new economies. China is as well among the leading consumers in luxury products that accounts for a considerable portion of luxury sales around the world. L2 A rapidly growing-middle income population in mega cities like Shanghai and Beijing and trends of rapid urbanization and branded goods has put China as one of the favourite hunting grounds for luxurious brands. The Chinese authorities’ actions both for promoting the purchase of domestic luxury goods and the quarantine measures that limited the travel to other countries because of COVID-19 pandemic also contributed to this process. India which is the second largest consumer in luxury products is not behind, in fact it is experiencing a very high growth due to parameters like; the extent of the premiumization, the growing middle-class size and the inherent inclination towards premium merchandise. Asian specific tastes are being incorporated into plans of globalization of luxury brands and elements of Asian culture being used in products and advertisements. Also, travel retail, especially in airport, is gradually gaining its importance and effectiveness for luxury brands in the Asian market as more and more high-end consumers are likely to buy luxury products during their trip.

Therefore, the threats include the following; volatilities of the international market, change of customer perception and tastes, and possibly gradual expansion of some economies leading to slow growth of sales. A higher inflation rate and the costs of raw material have also escalated production costs and this will deeply impact the pricing processes and the consumers spending on luxury goods. Moreover, COVID-19 altered the consumer behaviour and how it makes an entry to come out as ‘low profile luxury’ or ‘stealth luxury’, which is the act of incorporating some luxury into plain things without using brands and logos as markers. Due to such a shift, there has been an observed improvement as customer shifted to the traditional branded products that are believed to be of high quality and related to excellence. Those brands that have been able to divine and follow the new consumer trends while retaining the values have been able to stay relevant. Three drivers which it is considered they will affect the future trends within Luxury market at the global are technology, sustainability as well as consumer trend. Nonetheless, these developments have made it difficult for brands in the luxury goods sector to capture the complicated and dynamic market they have to deal with.

Luxury Goods Market Trend Analysis

Rise of Sustainable and Ethical Luxury

- Sustainable ethical luxury product is playing a role in changing the conventional luxury market since people are conscious about their environment and the standard practice affecting the social livelihoods of people. Today, most of the great major luxury brands indeed set out various attempts in different measures of lowering their carbon emission, going green, and sourcing their material responsibly. For instance, high end fashion line producers and accessory brands are using organic cotton and recycled fabric and ethically sourced leather. However, far more circular systems that extend the useful life of an item constantly are getting consideration due to their benefits in cutting out waste and scale. Today this initiative is being led by the consumers especially the millennials and Gen Z who want the brands and companies that they invest in and the businesses that they buy their products from, to be transparent and sustainable.

- Ethical luxury therefore also goes a notch higher than the green-dimension followed by the company and also has the social-dimension where by the concerns are generated from issues of fairness towards the workers and the public. Most brands are trying to make sure that their supply chain meets fair trade requirements which means that workers are paid properly and conditions in which they operate are safe. Several firms that have embraced this cause include Gucci and Stella McCartney since they are at the frontline of anti sensitivity the fight whereby they have volunteered their supply information chain thereby making it available to the public and hence responsible. In particular, it demonstrates that people are ready to spend more on luxury goods, keeping the sustainability issue in mind, so this trend contributes to the improvement in the luxury industry. Hence, the sustainable and ethical luxury market’s future is promising because luxury brands have stepped up to such changes.

Digital Transformation and E-Commerce Expansion

- The technology disruption observed for luxury product markets is drastically altering consumer touch points and brand communications. With more luxury brands incorporating more digital devices, they are improving their online visibility, improving ERDS and gaining better insights about the consumers’ behavior. It has lead to things like virtual fitting and personalized recommendations that are very appropriately enticing to the luxury as well as the tech savvy segment. Influencers and Instagram or TikTok have also played their part in raising awareness and gaining consumer engagement to turn it into a boon for luxury brands to gain a foothold in the new, generations of youth seeking to build a personal connection with brands they prefer.

- The luxury segment has shown impressive advancement in e-commerce because of the new behavioral changes among the consumers that came from the COVID-19 outbreak. The sales of luxury products grew online; e-commerce could contribute significantly to the total luxury sales in the future. This is also backed by the increased social buying among the well-off group of people who have taken to the comfort and symbiotic shopping. They stress the formation of a reliable network for delivering products and services concurrently with the communication process with the buyer in an efficient pursuit of ideal level of satisfaction regarding the shopping experience. Thus, luxury products themselves are not only changing their selling techniques from the traditional trade to modernity including the internet selling but also introducing the new traditional way of purchasing luxury products that is much more commons and accesible yet they do not forget the status of luxury product.

Luxury Goods Market Segment Analysis:

Luxury Goods Market is segmented based on Product Type, Mode of sale , and Gender.

By Product Type, Designer Apparels segment is expected to dominate the market during the forecast period

- The luxury good industry consists various segments because of product variety and market target and consumer trends that are available in the markets. Designer apparels remains the most prominent ones due to brand status, fashion bloggers and rise in use of social media platform. Purchasers are paying more attention to quality, unique and elegant apparels that also carry on status symbol. Jewellery and timepieces are another related category because people buy accessories that can be ornaments and assets at the same time. The high craftsmanship and the recreation of emotional dear values create the desirability and expanding the luxury goods market, in general.

- But besides fashion accessories other sub sectors such as beauty and fragrances, wine and champagne and liquor are gaining popularity. The improvement of quality consciousness and sophistication among the people has compelled them to search for the better quality beauty products like the luxury skin care and make up products. This is so especially because consumers which would prefer to enjoy various aspects of consumption by consuming specialty drinks hence making the overall trend. Other sectors that have high sales include the traveling accessory particularly the luxury luggage that is expected to benefit from the measures gradually being taken to open up borders across the world. These two types of luxury products are not only a reflection of shifting values of consumers but also reflect the current general trend towards experiential luxury where the quality of the luxurious product is very crucial and the lifestyle enhancement plays a key role in the buying decision in the market.

By Mode of Sale , Online segment held the largest share in 2023

- The Luxury Goods Market has presented a new trend in their consumption mainly due to the trend that is associated with online selling in the market. Retail is still relevant, as most of the luxurious brands were discovered in large retail outlets where it was possible to initially concentrate efforts on history and distinctiveness. Luxury accessories and clothes are also sold through product promotion sales exhibitions, product display, and one-to-one services in luxury specialty stores and department stores. However, with the invention of e-business, strategies on how to sell these classy products changed as the brands have the opportunity to market their products worldwide. One thing that has aided luxury brands to reach the millennials online is the ease of doing business online coupled with the aspect and efficiency of digital media marketing.

- The luxury product segment’s sales through the internet have significantly increased due to the effects of COVID-19, which enhanced the use of technology. There has been more emphasis from Luxury brands that have upped their online presence, given very convenient easy use interfaces in cases where the client interfaces are direct to consumer, and having very efficient supply chains in cases where the interfaces are retailer to consumer. : This shift not only meets the increasing popularity of online shopping more than offline shopping, but also enables emerging marketing communication innovation practices including virtual reality showrooms and personalized online consultations. Thus, the position of the online channel is increasing in the context of the luxury goods sector, and companies are attempting to create experiences on digital channels congruent with modern culture. This indicates that fluctuations between retail and online sales will probably persist as customers and supply networks adapt to provide products.

Luxury Goods Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- The Luxury Goods Market in North America is expected to maintain its dominance up to the end of the forecast period due to rising consumers’ demand in addition to availability of numerous luxury brands. This has has been due to the enhanced standard of living, high tendency of individuals in these continents to adopt the use of luxuries, and the large market for the consument in these continents. Some of the product categories among the listed exotic products are readymade garments, fashion accessories, personal products among others in which people are willing to spent a lot on quality products. Furthermore, the continuous evolution of internet retailing has increased its sales since people have begun to access luxury products easily.

- consumers, especially, millennials, and Generation Z, who pay attention to the message and the environment of brands and goods. This demographic change rising from the young generation is putting pressure on the luxury brands to search for a new model for conducting their business and embracing sustainable business strategies. Another example could be a luxury consumption via tourism, because people who arrive to another country temporarily are likely to spend their money on some other durable products during their spare time. Thus, the further aggressive marketing investments, along with increasing attention to customers’ needs and experiences, guarantees North America’s leading position in the luxury goods industry in the forthcoming years.

Active Key Players in the Luxury Goods Market

- LVHM (France)

- Compagnie Financière Richemont SA (Switzerland)

- Kering SA (France)

- Chow Tai Fook Jewellery Group Limited (Hong Kong)

- The Estée Lauder Companies Inc. (U.S.)

- Luxottica Group SpA (Italy)

- The Swatch Group Ltd. (Switzerland)

- L’Oréal Group (France)

- Ralph Lauren Corporation (U.S.)

- Shiseido Company, Limited (Japan)

- Others Key Player

Key Industry Developments in the Luxury Goods Market

- In January 2024, Miu Miu (Prada) launched its fourth limited edition collection of upcycled bags, named “Miu Miu Upcycled: Denim and Patch” bags.

- In December 2023, Kering has announced that it has finalised the acquisition of a 30% stake in Valentino. The luxury group paid 1.7 billion euros (1.75 billion USD) to Valentino’s owner, the investment equity firm Mayhoola, with an option to buy 100% of the Italian brand’s capital until 2028.

- In September 2023, Richemont SA launched a new beauty division named Laboratoire de Haute Parfumerie et Beauté.

|

Luxury Goods Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 421.4 Bn. |

|

Forecast Period 2024-32 CAGR: |

7.3% |

Market Size in 2032: |

USD 794.50 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Mode of Sale |

|

||

|

By Gender |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Luxury Goods Market by Product Type (2018-2032)

4.1 Luxury Goods Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Designer Apparels

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Jewelry & Timepieces

4.5 Accessories

4.6 Cosmetics

4.7 Fine Wines/Champagne And Spirits

4.8 Travel Goods

4.9 Others

Chapter 5: Luxury Goods Market by Mode of Sale (2018-2032)

5.1 Luxury Goods Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Retail

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Online

Chapter 6: Luxury Goods Market by Gender (2018-2032)

6.1 Luxury Goods Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Male

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Female

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Luxury Goods Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ADIDAS AG

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 NIKE INCPUMA SE

7.4 FILA INCNEW BALANCE ATHLETICS INCKNOLL INCSAMSONITE INTERNATIONAL S.AVIP INDUSTRIES LTDTIMBERLAND LLC

7.5 JOHNSTON & MURPHY

7.6 WOODLAND WORLDWIDE

7.7 HERMÈS INTERNATIONAL S.ALOUIS VUITTON MALLETIER

7.8 VF CORPCOLLAR COMPANY

7.9 LUCRIN GENEVA

7.10 NAPPA DORI

7.11 SADDLES INDIA PVT. LTDLEAR CORP

Chapter 8: Global Luxury Goods Market By Region

8.1 Overview

8.2. North America Luxury Goods Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Product Type

8.2.4.1 Designer Apparels

8.2.4.2 Jewelry & Timepieces

8.2.4.3 Accessories

8.2.4.4 Cosmetics

8.2.4.5 Fine Wines/Champagne And Spirits

8.2.4.6 Travel Goods

8.2.4.7 Others

8.2.5 Historic and Forecasted Market Size by Mode of Sale

8.2.5.1 Retail

8.2.5.2 Online

8.2.6 Historic and Forecasted Market Size by Gender

8.2.6.1 Male

8.2.6.2 Female

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Luxury Goods Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Product Type

8.3.4.1 Designer Apparels

8.3.4.2 Jewelry & Timepieces

8.3.4.3 Accessories

8.3.4.4 Cosmetics

8.3.4.5 Fine Wines/Champagne And Spirits

8.3.4.6 Travel Goods

8.3.4.7 Others

8.3.5 Historic and Forecasted Market Size by Mode of Sale

8.3.5.1 Retail

8.3.5.2 Online

8.3.6 Historic and Forecasted Market Size by Gender

8.3.6.1 Male

8.3.6.2 Female

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Luxury Goods Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Product Type

8.4.4.1 Designer Apparels

8.4.4.2 Jewelry & Timepieces

8.4.4.3 Accessories

8.4.4.4 Cosmetics

8.4.4.5 Fine Wines/Champagne And Spirits

8.4.4.6 Travel Goods

8.4.4.7 Others

8.4.5 Historic and Forecasted Market Size by Mode of Sale

8.4.5.1 Retail

8.4.5.2 Online

8.4.6 Historic and Forecasted Market Size by Gender

8.4.6.1 Male

8.4.6.2 Female

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Luxury Goods Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Product Type

8.5.4.1 Designer Apparels

8.5.4.2 Jewelry & Timepieces

8.5.4.3 Accessories

8.5.4.4 Cosmetics

8.5.4.5 Fine Wines/Champagne And Spirits

8.5.4.6 Travel Goods

8.5.4.7 Others

8.5.5 Historic and Forecasted Market Size by Mode of Sale

8.5.5.1 Retail

8.5.5.2 Online

8.5.6 Historic and Forecasted Market Size by Gender

8.5.6.1 Male

8.5.6.2 Female

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Luxury Goods Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Product Type

8.6.4.1 Designer Apparels

8.6.4.2 Jewelry & Timepieces

8.6.4.3 Accessories

8.6.4.4 Cosmetics

8.6.4.5 Fine Wines/Champagne And Spirits

8.6.4.6 Travel Goods

8.6.4.7 Others

8.6.5 Historic and Forecasted Market Size by Mode of Sale

8.6.5.1 Retail

8.6.5.2 Online

8.6.6 Historic and Forecasted Market Size by Gender

8.6.6.1 Male

8.6.6.2 Female

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Luxury Goods Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Product Type

8.7.4.1 Designer Apparels

8.7.4.2 Jewelry & Timepieces

8.7.4.3 Accessories

8.7.4.4 Cosmetics

8.7.4.5 Fine Wines/Champagne And Spirits

8.7.4.6 Travel Goods

8.7.4.7 Others

8.7.5 Historic and Forecasted Market Size by Mode of Sale

8.7.5.1 Retail

8.7.5.2 Online

8.7.6 Historic and Forecasted Market Size by Gender

8.7.6.1 Male

8.7.6.2 Female

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Luxury Goods Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 421.4 Bn. |

|

Forecast Period 2024-32 CAGR: |

7.3% |

Market Size in 2032: |

USD 794.50 Bn. |

|

Segments Covered: |

By Product Type |

|

|

|

By Mode of Sale |

|

||

|

By Gender |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||