Bottled Water Market Synopsis

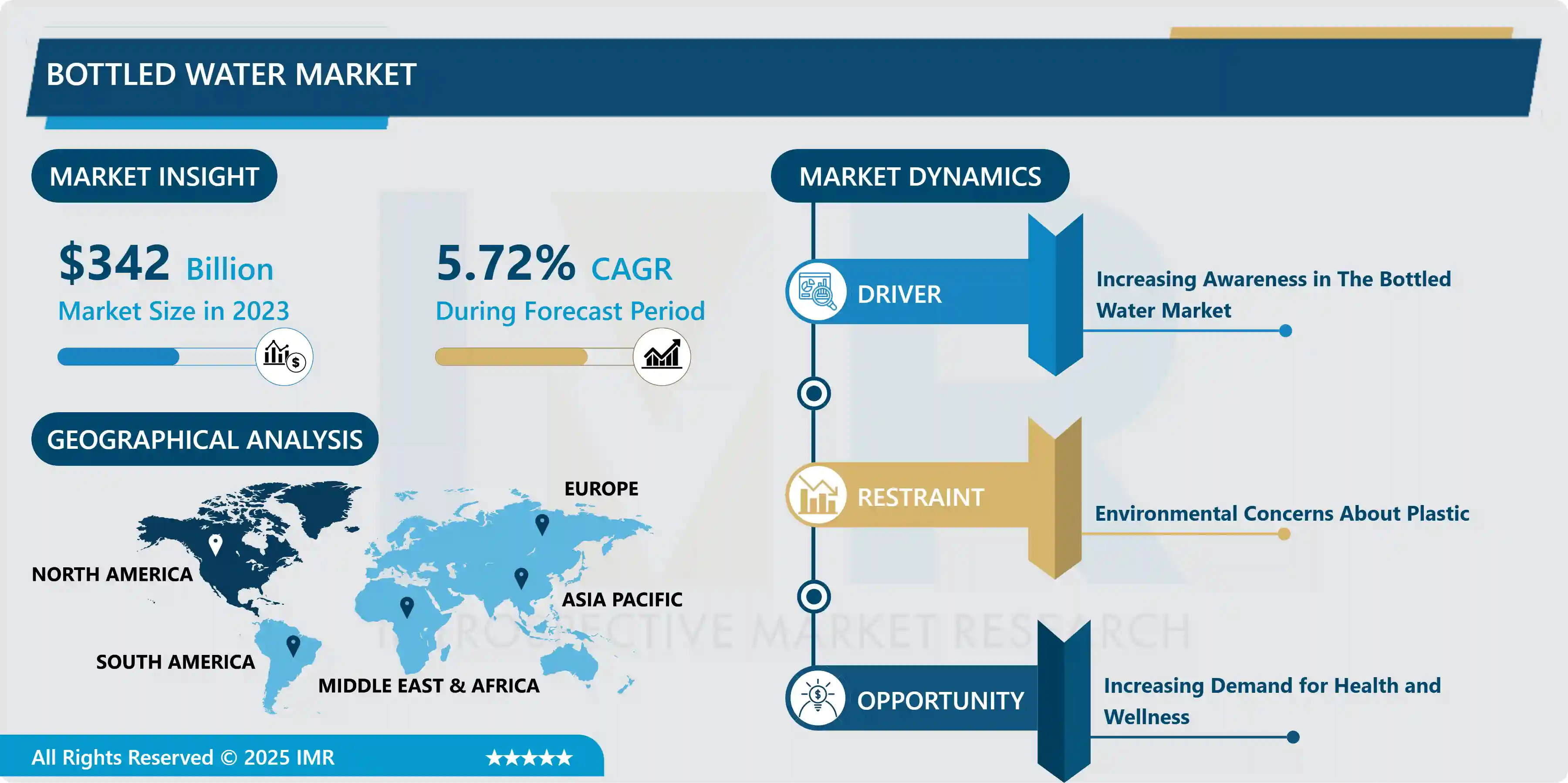

Global Bottled Market size was valued at USD 342 billion in 2023 and is projected to reach USD 564.21 Billion by 2032, growing at a CAGR of 5.72%from 2024 to 2032.

The bottled water industry originated in the late 18th century with mineral water sales in Europe, evolving now with eco-friendly packaging, advanced purification, and a consumer focus on sustainability and tap water awareness.

The bottled water market to the industry segment that involves the production, packaging, and distribution of drinking water that is intended for consumption and sold in sealed containers, typically made of plastic, glass, or other materials. Types of bottled drinking water in the market are Spring water bottled drinking water, Mineral water, Purified water bottled, Alkaline water bottled, Sparkling water bottled, and Electrolyte-enhanced water bottled. this packaged water is sold to consumers through various retail channels such as supermarkets, convenience stores, vending machines, and online platforms.

The global bottled water market increases health consciousness, changing lifestyles, the convenience of on-the-go hydration, concerns about tap water quality in some regions, and aggressive marketing strategies by bottled water companies. Bottled water offers several benefits. It provides a reliable and pure source of hydration, free from the chlorine taste often found in tap water. This makes bottled water a reliable choice, especially when on the go or outside, ensuring a safe, refreshing, and high-quality drinking experience. Additionally, the convenience of bottled water allows you to stay hydrated effortlessly throughout the day.

The significant impact of the market is demonstrated through its substantial revenue generation, creation of employment opportunities, and its influence on shaping consumer preferences within the domains of Health and Wellness, Urbanization, and Changing Lifestyles. The market is expanding its scope from conventional still and sparkling water products to incorporate functional and enhanced waters that contain vitamins, minerals, electrolytes, and other advantageous additives, and health wellness requirements.

Bottled Water Market Trend Analysis

Bottled Water Market Trend Analysis

Increasing awareness in the Bottled Water Market

- The growing focus on health and well-being among consumers is a key factor in the bottled water market forward. This shift in consumer preferences is leading people to choose healthier drink alternatives such as purified and ultra-purified bottled water. the increasing desire for water enriched with nutrients is becoming a trend, among travelers, professionals, and those looking for convenient at-home hydration. These are fueling the expansion of the bottled water market and are anticipated to sustain its growth in the future.

- Rapid population growth and the expansion of urban areas’ roles in water supplies across various regions globally. there is a rising trend in allocating more resources toward enhancing water infrastructure, including the construction of dams, reservoirs, and facilities for water purification and treatment. ?

- The growing popularity of sustainable packaging. Consumers are becoming more concerned about the environmental impact of plastic bottles, and manufacturers are responding with more sustainable packaging options, such as glass and aluminum bottles. Some consumers are looking for bottled water that is infused with vitamins or minerals.

- Bottled water companies have expanded their product offerings to encompass a diverse range of options, encompassing flavored variations and functional enhancements. This strategic diversification is particularly attractive to consumers with greater choices and additional advantages from their bottled water selections. This trend reflects a proactive approach by manufacturers to cater to evolving consumer preferences, capitalizing on the growing demand for innovative and health-oriented beverages.

Growing Demand in Health and Wellness

- As consumers become more health-conscious, there's a growing demand for healthier beverages. Bottled water is perceived as a better alternative to sugary soft drinks and juices. Brands that highlight the health benefits of their water, such as natural mineral content or pH balance.

- Urbanization is leading to a decline in the quality of tap water in many areas. This is driving demand for bottled water. Tourists prefer to drink bottled water, as they do not trust the quality of tap water in the places they are visiting.

- Companies are introducing various types of bottled water with added functional benefits, such as electrolytes, vitamins, minerals, and other additives that cater to specific health needs. Concerns about the environmental impact of single-use plastics have also contributed to the growth of the bottled water market.

This global preference for bottled water is a move by a shared aspiration for healthier lifestyles. As individuals around the world become increasingly conscious of their well-being, they choices that align with their health goals. Bottled water, often perceived as a cleaner and safer option compared to tap water, has gained popularity as a convenient means of hydration while avoiding potential contaminants. This perception, by the rigorous purification processes that many bottled water brands emphasize, reinforces the demand for this product on a global scale.

Segmentation Analysis of the Bottled Water Market

Bottle Market segments cover the Type, Application, and, Distribution Channel. By Type, The Mineral Water and Sparkling Water segment is Anticipated to Dominate the Market Over the Forecast period.

- Mineral water is sourced from natural springs or wells and contains minerals and trace elements that are naturally present. It is marketed as a healthier alternative to regular tap water due to its potential health benefits.

- Sparkling water is water that has been artificially carbonated to create bubbles or fizz. It has gained popularity as a low-calorie and refreshing beverage option in the market.

- The sparkling water segment will take a leading role in the market and could suggest a change in consumer preferences toward beverages that are both health-conscious and enjoyable, while still retaining the satisfying fizz.

- Polyethylene terephthalate (PET) is known for its clarity and transparency, making it an excellent choice for products like beverages and food items. PET is highly recyclable and can be reprocessed into new PET products or other materials, reducing waste and resource consumption.

Bottled Water Market Regional Analysis:

Asia Pacific region is dominating the Market Over the Forecast period.

- The Asia Pacific region is specified as a growth in the middle-class population. As people move up the economic ladder, their preferences shift toward products that provide safety, hygiene, and convenience. Bottled water, being a packaged and regulated product, fits well within this preference, as it offers an assurance of clean and safe drinking water.

- Asia Pacific regions (China, India, Indonesia, Japan, and Vietnam) are among the most popular in the region bottled water market. Rapid economic growth, urbanization, and an increasing middle class in these countries have led to a surge in the demand for bottled water. factors such as industrialization and pollution in some of these countries might contribute to concerns about tap water quality, driving consumers towards bottled alternatives.

- Middle-income customers tend to prioritize their health and are ready to invest extra in items they perceive as secure and beneficial. In numerous areas of the Asia Pacific, where water quality can be an issue, bottled water is considered to be pure and more dependable compared to tap water. bottled water has the advantages of convenience and portability.

- North America is the 2nd largest market for bottles, the region is driven by the increasing demand for bottled water, beverages, and personal care products.

Active Key Players in the Bottled Water Market:

- Bisleri International(India)

- Nestlé(Switzerland)

- PepsiCo (United States)

- The Coca-Cola Company (United States)

- DANONE (France)

- Primo Water Corporation (United States)

- Gerolsteiner Brunnen (Germany)

- Tata Consumer Products (India)

- VOSS WATER (US)

- Nongfu Spring (China)

- National Beverage Corp. (US)

- Kinley (India)

- Aquafina (India)

- Bailey (India)

- Himalayan Mineral Water (India)

- Kingfisher Mineral Water (India)

- Qua Mineral Water (India)

- Tata Water Plus (India)

- Rail Neer (India)

- Ferrarelle Spa (Italy)

- Keurig Dr Pepper Inc. (US) and Other Major Player.

Key Industry Developments in the Bottled Water Market

- In April 2023, Nestlé Waters North America announced a new partnership with PepsiCo to expand its presence in the premium bottled water market. Nestlé Waters North America will be acquiring PepsiCo's premium bottled water brands, including Aquafina, Propel, and Smartwater, for a total of $4.3 billion.

- In April 2023, PepsiCo announced a new partnership with Constellation Brands to expand its presence in the alcoholic beverage market. PepsiCo will be acquiring Constellation Brands' wine and spirits brands, including Svedka vodka, Corona Extra beer, and Robert Mondavi wine, for a total of $41 billion.

- In May 2023, Coca-Cola announced an investment of $50 million in plant-based packaging company Aseptic Packaging. Aseptic Packaging's technology allows for the production of shelf-stable bottled water without the use of preservatives or artificial flavors.

- In May 2023, Danone announced a new partnership with Evian to expand its presence in the bottled water market in China. Danone will be acquiring Evian's Chinese bottling and distribution operations for an undisclosed amount.

|

Bottled Water Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 342 Bn. |

|

Forecast Period 2024-32 CAGR: |

5.72 % |

Market Size in 2032: |

USD 564.21 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Packaging |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the Report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Bottled Water Market by Type (2018-2032)

4.1 Bottled Water Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Mineral water

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Spring water

4.5 Sparkling water

4.6 Flavoured water.

Chapter 5: Bottled Water Market by Packaging (2018-2032)

5.1 Bottled Water Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Polyethylene terephthalate

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 High-density polyethylene

5.5 Polycarbonate

5.6 Cans.

Chapter 6: Bottled Water Market by Distribution Channel (2018-2032)

6.1 Bottled Water Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Supermarkets

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Convenience Stores

6.5 Hypermarkets.

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Bottled Water Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 SURTEX INSTRUMENTS LIMITED. (UK)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 NEW MED INSTRUMENTS (UAE)

7.4 CLH HEALTHCARE (UK)

7.5 ROCIALLE (UK)

7.6 SUZHOU TEXNET CO. LTD. (UK)

7.7 WUHAN LANYUAN PROTECTIVE CO. LTD. (CHINA)

7.8 GUANGZHOU JIUYUEKANG MEDICAL EQUIPMENT CO. LTD. (CHINA)

7.9 SHANGHAI JIAYU MEDICAL EQUIPMENT CO. LTD (CHINA)

7.10 NINGBO FINER MEDICAL INSTRUMENTS COLIMITED (CHINA)

7.11 GREEN VITALITY INDUSTRY LTD. (CHINA)

7.12 FUSION BIOTECH (INDIA)

7.13 MEDILIVESCARE MANUFACTURING PVT. LTD. (INDIA)

7.14

Chapter 8: Global Bottled Water Market By Region

8.1 Overview

8.2. North America Bottled Water Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 Mineral water

8.2.4.2 Spring water

8.2.4.3 Sparkling water

8.2.4.4 Flavoured water.

8.2.5 Historic and Forecasted Market Size by Packaging

8.2.5.1 Polyethylene terephthalate

8.2.5.2 High-density polyethylene

8.2.5.3 Polycarbonate

8.2.5.4 Cans.

8.2.6 Historic and Forecasted Market Size by Distribution Channel

8.2.6.1 Supermarkets

8.2.6.2 Convenience Stores

8.2.6.3 Hypermarkets.

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Bottled Water Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 Mineral water

8.3.4.2 Spring water

8.3.4.3 Sparkling water

8.3.4.4 Flavoured water.

8.3.5 Historic and Forecasted Market Size by Packaging

8.3.5.1 Polyethylene terephthalate

8.3.5.2 High-density polyethylene

8.3.5.3 Polycarbonate

8.3.5.4 Cans.

8.3.6 Historic and Forecasted Market Size by Distribution Channel

8.3.6.1 Supermarkets

8.3.6.2 Convenience Stores

8.3.6.3 Hypermarkets.

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Bottled Water Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 Mineral water

8.4.4.2 Spring water

8.4.4.3 Sparkling water

8.4.4.4 Flavoured water.

8.4.5 Historic and Forecasted Market Size by Packaging

8.4.5.1 Polyethylene terephthalate

8.4.5.2 High-density polyethylene

8.4.5.3 Polycarbonate

8.4.5.4 Cans.

8.4.6 Historic and Forecasted Market Size by Distribution Channel

8.4.6.1 Supermarkets

8.4.6.2 Convenience Stores

8.4.6.3 Hypermarkets.

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Bottled Water Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 Mineral water

8.5.4.2 Spring water

8.5.4.3 Sparkling water

8.5.4.4 Flavoured water.

8.5.5 Historic and Forecasted Market Size by Packaging

8.5.5.1 Polyethylene terephthalate

8.5.5.2 High-density polyethylene

8.5.5.3 Polycarbonate

8.5.5.4 Cans.

8.5.6 Historic and Forecasted Market Size by Distribution Channel

8.5.6.1 Supermarkets

8.5.6.2 Convenience Stores

8.5.6.3 Hypermarkets.

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Bottled Water Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 Mineral water

8.6.4.2 Spring water

8.6.4.3 Sparkling water

8.6.4.4 Flavoured water.

8.6.5 Historic and Forecasted Market Size by Packaging

8.6.5.1 Polyethylene terephthalate

8.6.5.2 High-density polyethylene

8.6.5.3 Polycarbonate

8.6.5.4 Cans.

8.6.6 Historic and Forecasted Market Size by Distribution Channel

8.6.6.1 Supermarkets

8.6.6.2 Convenience Stores

8.6.6.3 Hypermarkets.

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Bottled Water Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 Mineral water

8.7.4.2 Spring water

8.7.4.3 Sparkling water

8.7.4.4 Flavoured water.

8.7.5 Historic and Forecasted Market Size by Packaging

8.7.5.1 Polyethylene terephthalate

8.7.5.2 High-density polyethylene

8.7.5.3 Polycarbonate

8.7.5.4 Cans.

8.7.6 Historic and Forecasted Market Size by Distribution Channel

8.7.6.1 Supermarkets

8.7.6.2 Convenience Stores

8.7.6.3 Hypermarkets.

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Bottled Water Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 342 Bn. |

|

Forecast Period 2024-32 CAGR: |

5.72 % |

Market Size in 2032: |

USD 564.21 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Packaging |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the Report: |

|

||