Micro Data Center Market Synopsis

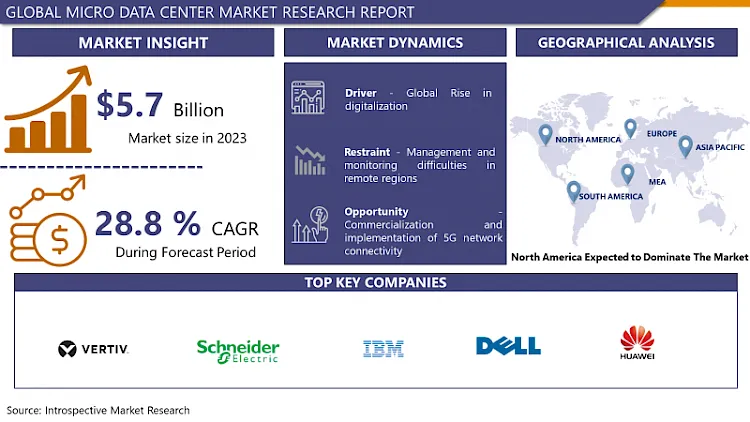

Micro Data Center Market Size Was Valued at USD 5.7 Billion in 2023, and is Projected to Reach USD 55.3 Billion by 2032, Growing at a CAGR of 28.80% From 2024-2032.

A micro data center consists of an independent, self-contained, secure “box” containing the fundamental building blocks necessary to provide the heat dissipation, power, rack, and uninterruptible power supply for all of the necessary Critical IT components together with any Management and Monitoing Software. Micro data centers allows industries to reduce their capital expenditures, the size of real estate while using only the required amount of energy as well as they can quickly deploy the systems. With the help of micro facilities that are mobile and efficient in terms of cost-effective network deployments, connectivity and power efficiency, more organizations are encouraged to adopt micro data centers in remote areas. Hence, not only speedy provisioning, but also infrastructure agility as containers or microdata centers can be quickly up for organizations to increase the business activities is enabled during computing demand booms. Changing of the location of conventional IT facilities at network sites needs more than a month of time, but the installation of micro data centers at the final facilities may take only a week. In addition to being an industry facilitator, they also initiate the growth of this market.

Also in places that are traditionally considered remote or where the infrastructure seems to warrant small data storage centers, a modern approach allowing you to benefit from capabilities of the full-blown data centers is widely available. A standalone data center provides vendors with an excellent possibility to anonymous to any spot and at any corner of the world, regardless of the network’s abilities. The backup data centers therefore receive the positive characteristics which consequently increase their rate on the international market. Usually they are crammed with an entire package of power unit, ventilation systems, and network infrastructure that permit installation as well as maintenance to take place with ease and comfort.

The strong growth of cloud services in various business sectors and the technological breakthroughs that pave the way for continued demand for micro mobile data centers are the driving media for the market. Further development of an array of such kinds of factors too, cyber security for industrial applications, energy efficiency of data centers and peripheral computing devices, will help to the market keep on growing.

Micro Data Center Market Trend Analysis

Organizations are increasingly adopting micro data centers.

- One the most important way to mitigate the environmental issues caused by space exploration is by making the architecture and technology as energy-efficient as possible. To do that, organizations have to implement modular solutions that could be used at the network periphery in order to decrease the latency and improve the connection for transferring and processing data. Micro facilities leave businesses to opt for mobility and deployment of micro data center solutions across peripheral locations in which their headquarters are located due to the many benefits they bring—mobility, cost effectiveness, improved networking and connectivity, and power efficiency. Moreover, the quick setup process of a Micro Data Centre helps clients across the board grow their operations on-demand to fit the spikes in their computing when necessary, and hence consequently this stimulates the Micro Data Centre market.

The communications industry's growing demand for microdata centers

- Provider of data transmission must have designs which are capable of low latency and scaling to help upgrade networks connectivity provided to customers. As 5G technology adoption become popular, the main issue is to keep happy the internet bandwidth and networking connectivity. Telecom companies are spending about 40% of the total cost to buy new cellular site/tower and install new 5G compatible network infrastructure. The application of the top-notch computing solutions will give a possibility to the organizations to make their network connection villagers much closer while reducing the issue of latency; such a scenario will stimulate the increase of demand of micro data center among business owners over the next years.

Micro Data Center Market Segment Analysis:

Micro Data Center Market is Segmented based on Component, and Application.

By Application, IT and telecommunications segment is expected to dominate the market during the forecast period

- This market of micro data center is represented as carbon dioxide emission into atmosphere consider BFSI, colocation, energy, government, healthcare, industrial, IT and telecom and other sectors. The IT and Telecommunication sector became undoubtedly the biggest part-holder in the year of 2022. The providers of telecommunications companies are, in this newly changed environment with smartphones and internet connectivity proliferative, more likely to invest heavily and use new solutions to upgrade their services. This is mainly attributed to the huge resident population among other countries and more bandwidth utilization which makes China and India the major nations in the field of internet penetration and telecom muscle. Via micro data centers telecom providers can enhance the : (a) broader application of compute functions (b) reduced network congestion and latency. As 5G network infrastructure is installed in rapid pace, telecommunication companies have concentrated on upgrading networks reliability and performance.

By Component, Solution segment held the largest share in 2023

- The micro data center market is segmented into complimentary services & solutions based on macro data constituent part belonging to them. According to forecasts, the solutions sector will expand its market share from 32% of the current estimated share of 2022 to 37% by 2032. The marketing of power solutions for a diverse range of requirements are rapidly improving with the developments of the new UPS series. Designed to instantly meet specific needs of micro data centers, the UPS systems provide improved efficiency, expandability, and adaptability thanks to these features. The examples the iCube 2 brings to my mind are the electronic library or an electronic classroom. and for the 9PX lithium-ion UPS, Eaton, which is one of the leading global companies for power management solutions, released them as part of the 9PX UPS series and the micro data center line in June 2021.

- Keeping Asian organizations to make their data center infrastructures last for the long term in view, these offerings were purposefully developed so they address unique needs and concerns of the Asia. The unceasing progress of UPS inventions in refueling the micro data center industry to get better is key for the industry to keep competitive while edge computing becomes mainstream.

Micro Data Center Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- In 2021, the leadership in global micro data centers was taken by North America, which took approximately 37% share. U. S. -based telecommunications firms are building microdata centers to provide infrastructure and aid for improving 5G coverage. Small data centers are distributed directly or via proximity to network aggregation pools or cellular towers to provide boost network processing and considerably reduce latency. Telecom modernization in the European Union is closely related to changes in the same field in the United States. Severe toll +1 country code proposed with final result number 459. A total of it 48 million connections in 2021. A total of 361. Relatively speaking to the 66 million of them which of course are mobile phones, and each grasping an average of one unit. 1 mobile phones. This through this will make it possible for network towers to have base stations sites which operate in microdata centers.

Active Key Players in the Micro Data Center Market

- Vertiv Co

- Schneider Electric SE

- IBM Corporation

- Dell Inc

- Huawei Technologies Co. Ltd

- Hewlett Packard Enterprise Company

- Eaton Corporation

- Other Key Players

Key Industry Developments in the Micro Data Center Market:

- Dell Inc. integrated liquid cooling technology into the Dell Micro 815 data center in June 2023. It is asserted by the company that its liquid cooling technology accomplishes an energy conservation of 40-50%.

- Supermicro, Inc., an all-encompassing provider of IT solutions for storage, 5G/edge, and cloud and AI/ML applications, expanded its data center offerings in May 2023 with the introduction of liquid-cooled NVIDIA HGX H100 rack-scale solutions. By implementing measures to improve energy efficiency and decrease refrigeration expenses, the organization enhances the suitability of micro data centers for businesses seeking to decrease their environmental impact and operational costs.

|

Micro Data Center Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 5.7 Bn. |

|

Forecast Period 2024-32 CAGR: |

28.80% |

Market Size in 2032: |

USD 55.3 Bn. |

|

Segments Covered: |

By Component |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Micro Data Center Market by Component (2018-2032)

4.1 Micro Data Center Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Solutions

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Power

4.5 Networking

4.6 Cooling

4.7 Rack & Enclosure

4.8 Upto 24U

4.9 24U to 40U

4.10 Above 40U

4.11 DCIM

4.12 Service

Chapter 5: Micro Data Center Market by Application (2018-2032)

5.1 Micro Data Center Market Snapshot and Growth Engine

5.2 Market Overview

5.3 BFSI

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Colocation

5.5 Energy

5.6 Government

5.7 Healthcare

5.8 Industrial

5.9 IT & Telecom

5.10 Others

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Micro Data Center Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 ACE HARDWARE (UNITED STATES)

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 ELECTRONIC CITY INDONESIA (INDONESIA)

6.4 TRIKOMSEL OKE (INDONESIA)

6.5 ALFAMART (INDONESIA)

6.6 ALIEXPRESS (ALIBABA) (CHINA)

6.7 BEST DENKI (JAPAN)

6.8 PT. ELECTRONIC SOLUTION INDONESIA (INDONESIA)

6.9 OTHER KEY PLAYERS

Chapter 7: Global Micro Data Center Market By Region

7.1 Overview

7.2. North America Micro Data Center Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Component

7.2.4.1 Solutions

7.2.4.2 Power

7.2.4.3 Networking

7.2.4.4 Cooling

7.2.4.5 Rack & Enclosure

7.2.4.6 Upto 24U

7.2.4.7 24U to 40U

7.2.4.8 Above 40U

7.2.4.9 DCIM

7.2.4.10 Service

7.2.5 Historic and Forecasted Market Size by Application

7.2.5.1 BFSI

7.2.5.2 Colocation

7.2.5.3 Energy

7.2.5.4 Government

7.2.5.5 Healthcare

7.2.5.6 Industrial

7.2.5.7 IT & Telecom

7.2.5.8 Others

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Micro Data Center Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Component

7.3.4.1 Solutions

7.3.4.2 Power

7.3.4.3 Networking

7.3.4.4 Cooling

7.3.4.5 Rack & Enclosure

7.3.4.6 Upto 24U

7.3.4.7 24U to 40U

7.3.4.8 Above 40U

7.3.4.9 DCIM

7.3.4.10 Service

7.3.5 Historic and Forecasted Market Size by Application

7.3.5.1 BFSI

7.3.5.2 Colocation

7.3.5.3 Energy

7.3.5.4 Government

7.3.5.5 Healthcare

7.3.5.6 Industrial

7.3.5.7 IT & Telecom

7.3.5.8 Others

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Micro Data Center Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Component

7.4.4.1 Solutions

7.4.4.2 Power

7.4.4.3 Networking

7.4.4.4 Cooling

7.4.4.5 Rack & Enclosure

7.4.4.6 Upto 24U

7.4.4.7 24U to 40U

7.4.4.8 Above 40U

7.4.4.9 DCIM

7.4.4.10 Service

7.4.5 Historic and Forecasted Market Size by Application

7.4.5.1 BFSI

7.4.5.2 Colocation

7.4.5.3 Energy

7.4.5.4 Government

7.4.5.5 Healthcare

7.4.5.6 Industrial

7.4.5.7 IT & Telecom

7.4.5.8 Others

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Micro Data Center Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Component

7.5.4.1 Solutions

7.5.4.2 Power

7.5.4.3 Networking

7.5.4.4 Cooling

7.5.4.5 Rack & Enclosure

7.5.4.6 Upto 24U

7.5.4.7 24U to 40U

7.5.4.8 Above 40U

7.5.4.9 DCIM

7.5.4.10 Service

7.5.5 Historic and Forecasted Market Size by Application

7.5.5.1 BFSI

7.5.5.2 Colocation

7.5.5.3 Energy

7.5.5.4 Government

7.5.5.5 Healthcare

7.5.5.6 Industrial

7.5.5.7 IT & Telecom

7.5.5.8 Others

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Micro Data Center Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Component

7.6.4.1 Solutions

7.6.4.2 Power

7.6.4.3 Networking

7.6.4.4 Cooling

7.6.4.5 Rack & Enclosure

7.6.4.6 Upto 24U

7.6.4.7 24U to 40U

7.6.4.8 Above 40U

7.6.4.9 DCIM

7.6.4.10 Service

7.6.5 Historic and Forecasted Market Size by Application

7.6.5.1 BFSI

7.6.5.2 Colocation

7.6.5.3 Energy

7.6.5.4 Government

7.6.5.5 Healthcare

7.6.5.6 Industrial

7.6.5.7 IT & Telecom

7.6.5.8 Others

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Micro Data Center Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Component

7.7.4.1 Solutions

7.7.4.2 Power

7.7.4.3 Networking

7.7.4.4 Cooling

7.7.4.5 Rack & Enclosure

7.7.4.6 Upto 24U

7.7.4.7 24U to 40U

7.7.4.8 Above 40U

7.7.4.9 DCIM

7.7.4.10 Service

7.7.5 Historic and Forecasted Market Size by Application

7.7.5.1 BFSI

7.7.5.2 Colocation

7.7.5.3 Energy

7.7.5.4 Government

7.7.5.5 Healthcare

7.7.5.6 Industrial

7.7.5.7 IT & Telecom

7.7.5.8 Others

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Micro Data Center Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD 5.7 Bn. |

|

Forecast Period 2024-32 CAGR: |

28.80% |

Market Size in 2032: |

USD 55.3 Bn. |

|

Segments Covered: |

By Component |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||