Electric Vehicle Fast-Charging System Market Overview

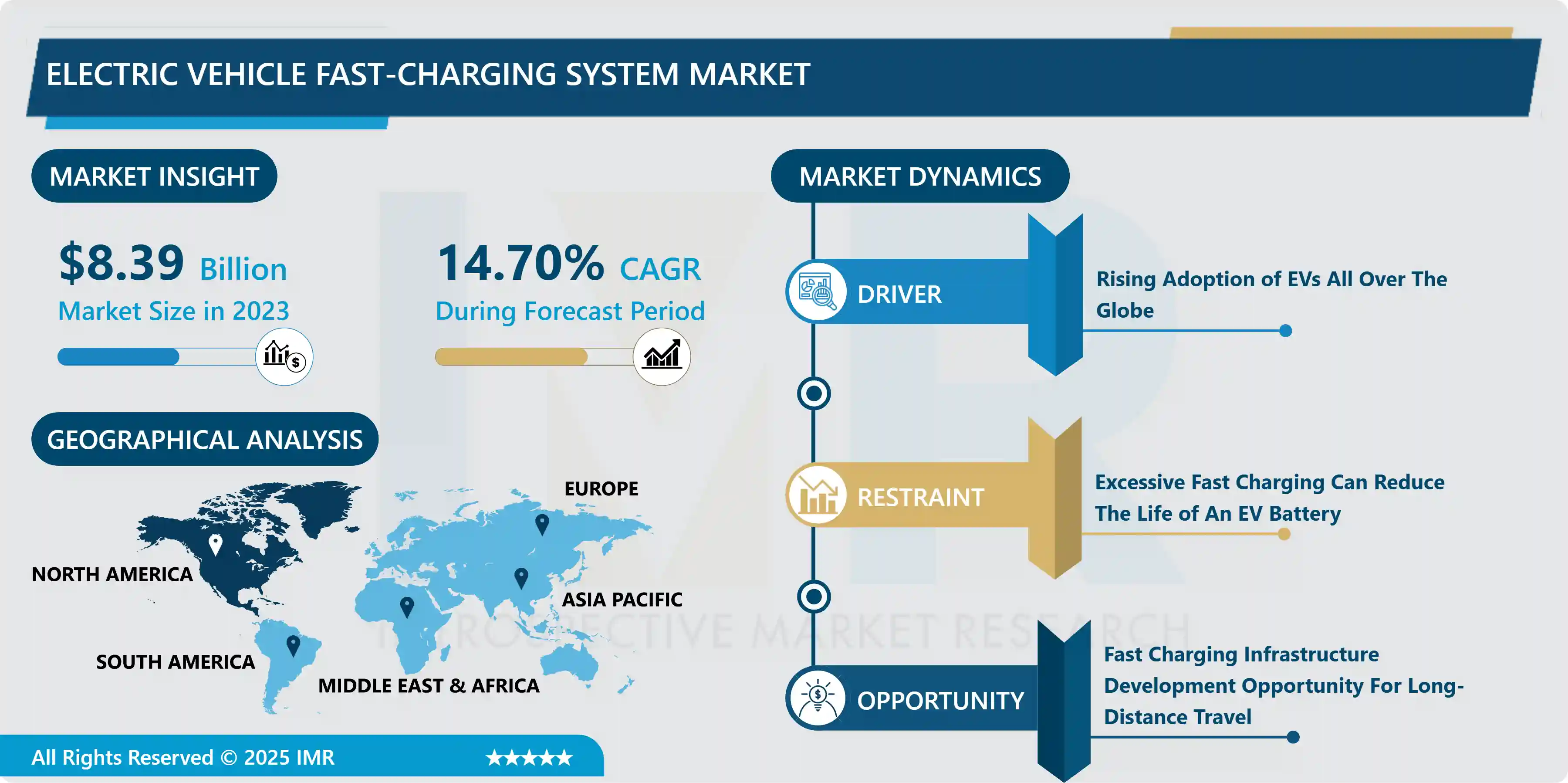

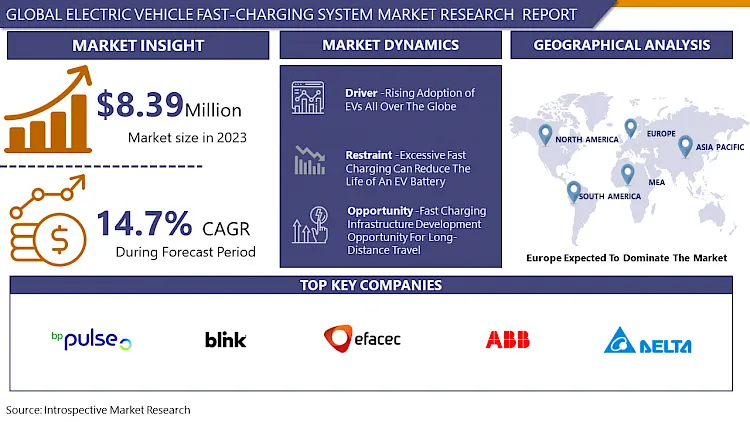

Electric Vehicle Fast-Charging System Market Size Was Valued at USD 8.39 Billion in 2023, and is Projected to Reach USD 33.15 Billion by 2032, Growing at a CAGR of 14.7% From 2024-2032.

Electric vehicles have the possibility to reduce carbon emissions in the transportation industry. The main obstacle to the widespread use of electric vehicles is the amount of time it takes to charge them. It takes just 15 minutes or less to refuel a vehicle that runs on fuel. To promote the adoption of EVs, it is anticipated that the charging time will be on par with that of traditional fuel-powered cars. Quick charging is crucial for easing concerns about range anxiety related to electric vehicles. Different trends can be seen in the rapid charging of electric vehicles, including ultra-rapid charging, increased battery capacity, and designs for ultra-rapid charging stations.

There will be a significant increase in the energy requirements for electric vehicles soon. The energy demand in three developing economies is being considered, which will encourage the use of EVs. The image highlights the significance of rapid charging in the upcoming years. Every developing country includes fast charging in their plans to increase electric vehicle adoption. Over time, there will be an increase in the proportion of total energy demand taken up by level 2 and DC fast charging. DC fast chargers are the most powerful chargers available for electric vehicles. They are frequently employed to extend the range on long journeys along main travel routes and in city settings to assist drivers who do not have access to home charging or drive long distances. They are perfect for locations like restaurants, recreational areas, and shopping centres, where people typically stay for 30 minutes to an hour, given the current charging speeds. The establishment of fast-charging infrastructure has been crucial in building consumer

The current industry is defined by an expanding web of rapid-charging stations, close relationships between car manufacturers, charging service providers, and governments, and a clear direction towards worldwide standardization and compatibility of charging systems. This transformation demonstrates how the market is reacting to the increased interest in EVs and the crucial requirement for infrastructure that enables fast and easy charging of electric vehicles, signalling a noteworthy change from the inception of the market to becoming a vital part of the worldwide effort to electrify transportation.

Market Dynamics And Factors For Electric Vehicle Fast-Charging System Market

Drivers:

Rising Adoption of Evs All Over The Globe

- E-mobility has reached a fork in the road. Over 250 new battery-electric automobiles (BEV) and plug-in hybrid electric vehicles (PHEV) will be produced in the next two years, with up to 130 million EVs on the road worldwide by 2030. To maintain these figures, far more price will be required—and it will not be cheap. According to Mckinsey, an estimated $110 billion to $180 billion will be required between 2020 and 2030 to accommodate global demand for EV charging stations in both public and private settings. By the end of 2020, 10 million electric cars would be on the road around the world, following a decade of rapid growth. Despite a global downturn in automotive sales due to the pandemic, which saw global car sales drop by 16 percent in 2020, electric car registrations increased by 41%. Europe overtook the People's Republic of China ("China") as the world's largest electric vehicle (EV) market for the first time, selling about 3 million vehicles (a 4.6 percent market share). In important markets, electric bus and truck registrations also climbed, reaching 600,000 and 31,000 global stocks, respectively. As a result, such a figure shows that the adoption rate of electric vehicles is increasing, which is projected to boost the market for Electric Vehicle Fast-Charging systems.

Restraints:

Excessive Fast Charging Can Reduce The Life of An EV Battery

- One major disadvantage of fast charging technology is that it frequently falls to the manufacturer to put up a charging infrastructure. Companies like Ola Electric have the capital to build a large network, but smaller businesses will find it difficult. Furthermore, the charging mechanism must be standardized to allow several manufacturers to use the same charging method. In places with intense heat, fast charging may not be possible, especially if the batteries are passively cooled. This will have a detrimental impact on the battery's entire life cycle. Fast charging tends to shorten the life of a battery faster than slow charging, so frequent use of this technology may be harmful to the battery's health. As a result, those who usually use slow charging may need to replace the battery pack sooner.

Opportunities:

Fast Charging Infrastructure Development Opportunity For Long-Distance Travel

- Although fast-charging stations presently play a significant role in meeting long-distance recharging needs, future increases in charging speeds may alter their utility. In China's major cities, such as Beijing, as many fast-charging stations as level 2 charging stations have already been installed. This is an attempt to meet the needs of urban EV drivers who do not have access to a private parking space and consequently a dedicated charging station. Although the limited charging speeds imply that such an alternative is not currently favored by EV drivers, such preferences may change in the future. Most automobiles can only charge at speeds of up to 100 kW, resulting in charging periods of more than 30 minutes to fill the car to 80% capacity. These longer charging durations have led to a preference for charging when parked. With increased battery capacity and improved battery management systems, it is expected that EVs would be able to charge at faster rates. If charging times are reduced dramatically, EV drivers may shift their preferences toward fast charging.

Challenges:

Limited Fast Charging System/Infrastructure

- The number of charging sessions required by an electric car is influenced by its battery technology. While some electric vehicles have long ranges, others may only be able to travel a short distance on a single charge. The number of public charging stations required in a given location is determined by this. The capacity of charging stations, on the other hand, determines the charging time for electric vehicles. Regular AC charging outlets can supply Level 1 (equivalent to a US household plug) or Level 2 charging capacity (240 volts). However, it takes longer when compared to a rapid Level 3 DC charging outlet. Integrating several types of chargers into a one-stop solution on a wide scale can be difficult for Electric Vehicle Fast-Charging System providers.

Segmentation Analysis of Electric Vehicle Fast-Charging System Market

- By Power, >200 KW segment is expected to be dominating in the Electric Vehicle Fast-Charging System Market. The fast-charging system above 200 KW is also referred to as high-power charging. HPC allows for faster charging with more power, typically up to 100, 150, or 200 kilowatts, depending on the vehicle. Audi e-Tron, Tesla Model 3, and Porsche Taycan have the highest charging power. In ideal conditions, charging time for 100 kilometers of driving distance is about 5-10 minutes. Depending on the vehicle and charging parameters such as battery temperature, HPC reduces charging time by 20%–70%. The charging port is a standard CC. The cables are liquid-cooled, and the connectors are frequently marked "HPC." Because HPC is backward compatible, it may charge any electric vehicle with a CCS plug, including older models. HPC chargers use RFID tags and mobile apps in the same manner that conventional chargers do. HPC is available in two voltages: 400 volts and 800 volts. Only the Porsche Taycan can charge utilizing a new 800-volt system with up to 270 kilowatts, which is compatible with all vehicles. Current HPC installations have a maximum capacity of 350 kilowatts, with considerably higher powers anticipated for future EVs.

- By Connector Type, CHADeMO dominates the EV fast-charging system market. The CHAdeMO charging system was developed by Tokyo Electric Power Co. Between 2006 and 2009, TEPCO worked on several EV infrastructure initiatives with Nissan, Mitsubishi, and Subaru (amongst others). CHAdeMO was the first in the world to offer a standardized DC rapid charge solution as the public infrastructure on the roadside that could be shared by EVs of all brands and models. Newer CHAdeMO units have a lower footprint and may be placed with minimal civil engineering work in many existing parking lots. Furthermore, CHAdeMO chargers have grown significantly more inexpensive in recent years. In comparison to other options, the CHAdeMO fast-charging system provides an excellent cost-to-performance ratio.

- By Application, the Public segment is likely to dominate the Electric Vehicle Fast-Charging System Market. Governments all over the world are promoting electric vehicles by investing extensively in the expansion of EV charging infrastructure to attract more people to them. By 2020, there will be 1.3 million publicly available slow and rapid chargers. Slow charger (charging power below 22 kW) installations climbed by 65 percent in China in 2020, to around 500 000 publicly accessible slow chargers. In Europe, fast chargers are being adopted at a faster rate than slow chargers. Around 38 000 public fast chargers are now available, up 55% from 2020, with over 7,500 in Germany and 6,200 in the United States. There are 4,000 in the United Kingdom, 4,000 in France, and 2,000 in the Netherlands. In the United States, there are 17 000 fast chargers, with Tesla accounting for roughly 60%, and 9800 fast chargers and superchargers in Korea.

Regional Analysis of Electric Vehicle Fast-Charging System Market

- The European region is dominating the Electric Vehicle Fast-Charging System Market. Electric car sales in Europe were much greater as a result of current legislative support programs. Global market conditions were dramatically different in the second half of 2020 when lockdowns were eased for a time and the automobile sector began to recover. Electric vehicle sales in all major markets, including China, India, the European Union, Korea, the United States, and the United Kingdom, exceeded monthly sales every month between July and December 2019. Certain countries, such as Canada, Japan, and others, experienced a loss in income as demand for new autos and manufacturing were badly impacted. During pandemics and lockdowns, the deployment of electric vehicle charging infrastructure has been delayed. Since the prohibition has been lifted, several countries have begun to expand their charging infrastructures in collaboration with corporate and public entities, resulting in a surge in the Electric Vehicle Fast-Charging System market.

- The Electric Vehicle Fast-Charging System Market is predicted to develop at the quickest rate in North America. With the rising number of service providers such as Tesla (Superchargers & Destination), ChargePoint, Blink (CarCharging), SemaConnect / SemaCharge, EVgo, GE WattStation, and Electrify America / Electrify Canada, North America, Canada, and the United States have seen tremendous growth in EV charging infrastructure. In terms of cost, charging at home is roughly 30% less expensive than charging at a public charger, and traveling 100 km (62 miles) on electricity is 6 times less expensive than driving on gas in Quebec. Charging at home costs about 65 percent less than charging at a public charger in Ontario, and traveling 100 km (62 miles) on electricity costs 5 times less than driving on gasoline. Everything in the United States is determined by the price of oil and gas. The consumption of an electric vehicle in kWh/100 miles multiplied by the cost of a kWh vs the consumption of a gas automobile in gallons/100 miles multiplied by the price of a gallon of gas. As a result, North America is projected to see a significant increase in Electric Vehicle Fast-Charging System Market.

Players Covered in Electric Vehicle Fast-Charging System Market are

- ABB

- Blink Charging Co.

- BP Chargemaster Ltd

- Broadband TelCom Power Inc.

- ChargePoint Inc.

- Delta Electronics Inc.

- Efacec Electric Mobility

- Signet EV Inc.

- EVBox

- ShenZhen SETEC Power Co. Ltd.

- Siemens

- Star Charge

- Tesla Inc.

- Tritium Pty Ltd

- Xi'an TGOOD Intelligent Charging Technology Co Ltd and other major players.

Key Industry Developments In Electric Vehicle Fast-Charging System Market

- In June 2024, ChargePoint, a leading provider of networked charging solutions for electric vehicles (EVs), and global innovator LG Electronics (LG) have formed a strategic partnership to leverage their respective strengths for future innovations in EV charging

- In January 2024,Blink Charging Co. ?is thrilled to announce a collaboration that’s sure to electrify El Salvador. Teaming up with Grupo Q, Porsche’s official dealer throughout El Salvador, the Company will be launching five advanced EV charging stations in select premium retail and restaurant locations in the Santa Tecla, Costa del Sol, Santa Ana, San Miguel, and Playa La Libertad regions. The launch of Blink’s chargers is part of Porsche’s Destination Charging Program Porsche’s global initiative to expand and ensure EV charging infrastructure worldwide.

|

Electric Vehicle Fast-Charging System Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data : |

2017 to 2023 |

Market Size in 2023: |

USD 8.39 Bn. |

|

Forecast Period 2024-32 CAGR: |

14.7 % |

Market Size in 2032: |

USD 33.15 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Connector Type |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Electric Vehicle Fast-Charging System Market by Type (2018-2032)

4.1 Electric Vehicle Fast-Charging System Market Snapshot and Growth Engine

4.2 Market Overview

4.3 <100 KW

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 100-200 KW

4.5 >200 KW

Chapter 5: Electric Vehicle Fast-Charging System Market by Connector Type (2018-2032)

5.1 Electric Vehicle Fast-Charging System Market Snapshot and Growth Engine

5.2 Market Overview

5.3 SAE Combo Charging System

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 GB/T

5.5 CHADeMO

5.6 Supercharger

Chapter 6: Electric Vehicle Fast-Charging System Market by Application (2018-2032)

6.1 Electric Vehicle Fast-Charging System Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Public

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Private

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Electric Vehicle Fast-Charging System Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 ALFRED A. TOMATIS

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 DON CAMPBELL

7.4 JONATHAN GOLDMAN

7.5 FABIEN MAMAN

7.6 JOSHUA LEEDS

7.7 MITCHELL L. GAYNOR

7.8 JOHN BEAULIEU

7.9 EILEEN MCKUSICK

7.10 BARRY GOLDSTEIN

7.11 DAVID GIBSON

7.12 SILVIA NAKKACH

7.13 ACAMA

7.14 STEVEN HALPERN

7.15 SUSAN ALEXJANDER

7.16 MARJORIE DE MUYNCK

7.17 WAYNE PERRY

7.18 ANNE H. HEYWOOD

7.19 CHRISTINE STEVENS

7.20 JILL MATTSON

7.21 JEFFREY THOMPSON

Chapter 8: Global Electric Vehicle Fast-Charging System Market By Region

8.1 Overview

8.2. North America Electric Vehicle Fast-Charging System Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 <100 KW

8.2.4.2 100-200 KW

8.2.4.3 >200 KW

8.2.5 Historic and Forecasted Market Size by Connector Type

8.2.5.1 SAE Combo Charging System

8.2.5.2 GB/T

8.2.5.3 CHADeMO

8.2.5.4 Supercharger

8.2.6 Historic and Forecasted Market Size by Application

8.2.6.1 Public

8.2.6.2 Private

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Electric Vehicle Fast-Charging System Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 <100 KW

8.3.4.2 100-200 KW

8.3.4.3 >200 KW

8.3.5 Historic and Forecasted Market Size by Connector Type

8.3.5.1 SAE Combo Charging System

8.3.5.2 GB/T

8.3.5.3 CHADeMO

8.3.5.4 Supercharger

8.3.6 Historic and Forecasted Market Size by Application

8.3.6.1 Public

8.3.6.2 Private

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Electric Vehicle Fast-Charging System Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 <100 KW

8.4.4.2 100-200 KW

8.4.4.3 >200 KW

8.4.5 Historic and Forecasted Market Size by Connector Type

8.4.5.1 SAE Combo Charging System

8.4.5.2 GB/T

8.4.5.3 CHADeMO

8.4.5.4 Supercharger

8.4.6 Historic and Forecasted Market Size by Application

8.4.6.1 Public

8.4.6.2 Private

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Electric Vehicle Fast-Charging System Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 <100 KW

8.5.4.2 100-200 KW

8.5.4.3 >200 KW

8.5.5 Historic and Forecasted Market Size by Connector Type

8.5.5.1 SAE Combo Charging System

8.5.5.2 GB/T

8.5.5.3 CHADeMO

8.5.5.4 Supercharger

8.5.6 Historic and Forecasted Market Size by Application

8.5.6.1 Public

8.5.6.2 Private

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Electric Vehicle Fast-Charging System Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 <100 KW

8.6.4.2 100-200 KW

8.6.4.3 >200 KW

8.6.5 Historic and Forecasted Market Size by Connector Type

8.6.5.1 SAE Combo Charging System

8.6.5.2 GB/T

8.6.5.3 CHADeMO

8.6.5.4 Supercharger

8.6.6 Historic and Forecasted Market Size by Application

8.6.6.1 Public

8.6.6.2 Private

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Electric Vehicle Fast-Charging System Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 <100 KW

8.7.4.2 100-200 KW

8.7.4.3 >200 KW

8.7.5 Historic and Forecasted Market Size by Connector Type

8.7.5.1 SAE Combo Charging System

8.7.5.2 GB/T

8.7.5.3 CHADeMO

8.7.5.4 Supercharger

8.7.6 Historic and Forecasted Market Size by Application

8.7.6.1 Public

8.7.6.2 Private

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Electric Vehicle Fast-Charging System Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data : |

2017 to 2023 |

Market Size in 2023: |

USD 8.39 Bn. |

|

Forecast Period 2024-32 CAGR: |

14.7 % |

Market Size in 2032: |

USD 33.15 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Connector Type |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||