Sweet Dark Chocolate Market Synopsis

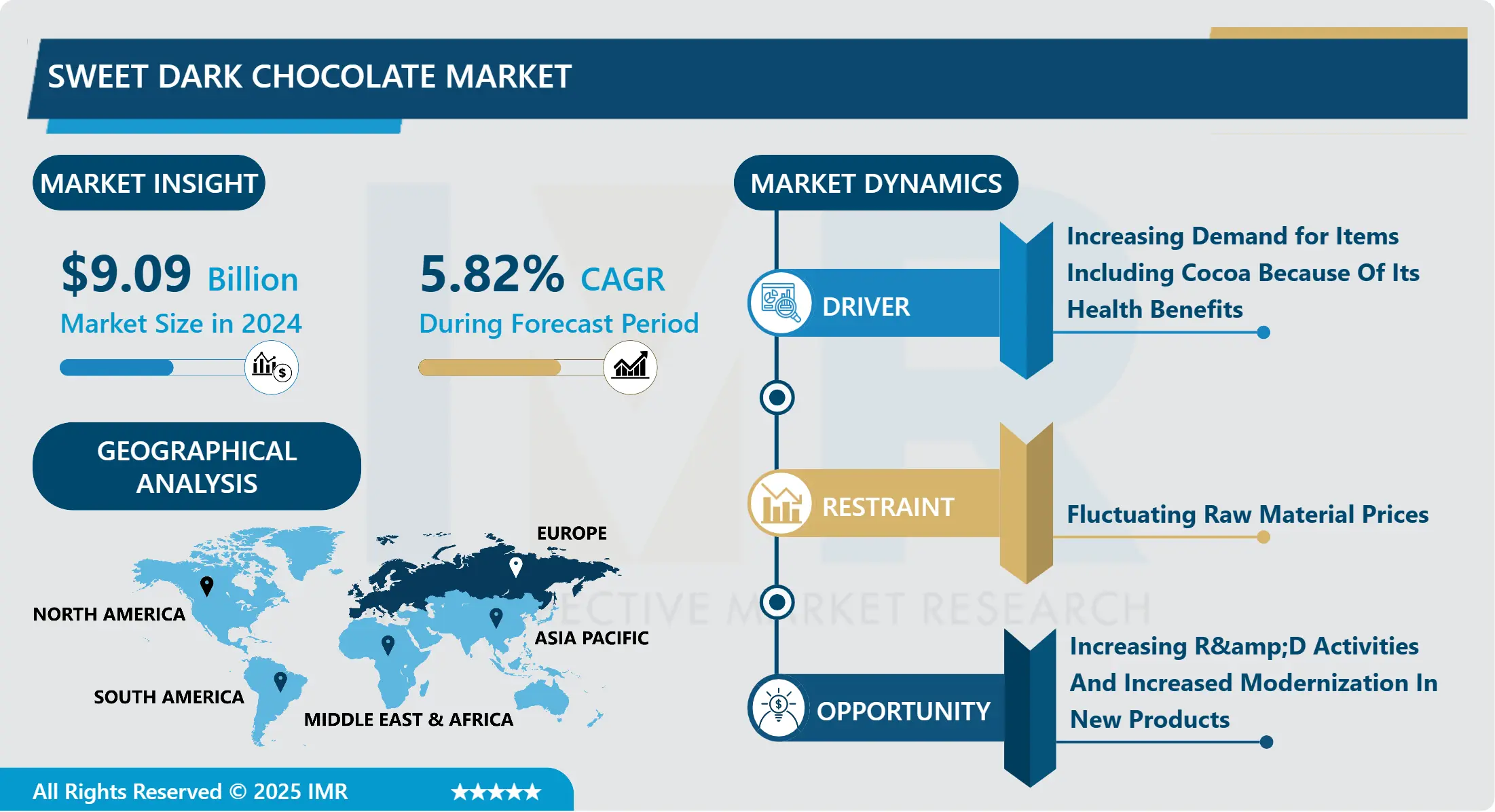

The Global Sweet Dark Chocolate Market size was reasonably estimated to be approximately USD 9.09 Billion in 2024 and is poised to generate revenue over USD 14.29 Billion by the end of 2032, projecting a CAGR of around 5.82% from 2025 to 2032.

An indulgence is thought to be dark chocolate. It is richer than milk chocolate and frequently combined with cheese and wine to provide a mouth-watering experience. Due to its dryness, harsh aftertaste, and gritty texture, dark chocolate has a deeper chocolate flavor than milk chocolate and does not include milk solids. It covers numerous health-promoting capabilities bioactive components polyphenols, flavonoids, procyanidins, theobromines, and nutrients and minerals that control the immune system of humans. It consults safeguards against cardiovascular diseases, certain forms of cancers, and other mind-associated disorders like Alzheimer’s disease, Parkinson’s disease. Dark chocolate is measured as a useful meal because of its anti-diabetic, anti-inflammatory, and anti-microbial properties. It additionally has a properly hooked-up function in weight management and the alteration of a lipid profile in a healthy way.

The main components of dark chocolate are sugar, cocoa beans, and emulsifiers like lecithin to maintain texture and flavors like vanilla. Dark chocolate is chocolate that doesn't have any additional milk solids.

Cacao beans, sugar, an emulsifier such as soy lecithin to maintain texture, and flavorings like vanilla make up the basic ingredients. Dark chocolate will taste harsh and have a higher cocoa content and lower sugar content; a small amount is regarded as a healthy snack.

Its flavor makes it a favorite kind of chocolate for melting and baking a range of sweets. Finding sweet dark chocolate will let you enjoy a superlative experience, even if dark chocolate is typically meant to be bitter compared to milk chocolate. A bar of darker chocolate that has been sweetened can help you satisfy your sweet tooth's yearning and avoid any guilt.

Sweet Dark Chocolate Market Trend Analysis

Sweet Dark Chocolate Market ?Growth Driver- Increasing Demand for Items Including Cocoa Because Of Its Health Benefits

- Cocoa is the primary ingredient used in the production of chocolate. The segment of society that prioritizes health is against eating chocolate. A nutritionist suggests refraining from chocolate to prevent obesity, and anxious mothers restrict their kids' access to it to prevent dental caries. They are true yet cocoa is one of the foods that are good for your health if you eat chocolate in moderation. Polyphenols, particularly flavonoids with their high antioxidant activity, are abundant in cocoa.

- According to reports, the dry weight percentage of polyphenols in cocoa ranges between 6 and 8%. These flavonoids are thought to be responsible for the positive health effects of cocoa and chocolate. More flavonoids are found in cocoa than in red wine or tea. In many related health conditions, including heart disease, cancer, stroke, disorders of the insulin system, vascular diseases, and many others, high levels of flavonoids improve their benefits.

- Although fine-flavored cocoa only makes up a small percentage of total cocoa production, its demand has recently increased. This is mostly due to end users' increasing preference for specialty or premium chocolate.

- In North America and Western Europe, there is a particularly high demand for premium chocolate. Despite the fact that only a small proportion of customers presently purchase these expensive chocolates due to their high prices, market penetration is increasing steadily. Leading chocolate manufacturers like Ferrero and Mars have invested in expanding their product lines as a result.

- The contents of the dark cholate help to give benefits to the body. The protein, fat and higher amount of energy are provided through dark chocolate so the consumption of dark chocolate increasing and thus increasing the consumption due to protein, fat, and Energy demand for dark chocolate increasing so these are the factor driving the growth of the Dark chocolate Market.

Sweet Dark Chocolate Market Opportunity- Increasing R&D Activities and Increased Modernization In New Products

- Manufacturers are focusing on combining natural sugars, such as stevia and coconut sugar, in order to pitch their product to a customer base that is very aware of the food choices they make. The stated emphasis on quality has suggested that manufacturers are currently focusing on including distinctive chocolate beans from Latin American countries.

- Although obtaining these premium ingredients from far-off locations raises the price of the completed product, growing consumer interest in gourmet chocolate is creating profitable market prospects. In the past, the demand for dried fruits used in the production of dark chocolate—such as blueberries and cranberries—has steadily expanded.

- Citrus flavors, vegetables, nuts, cereals, unique fruits, rare cocoa, flowers, flavor combinations, and others are among the latest, cutting-edge components employed in the chocolate industry. The diabetic population has been drawn to chocolate products because they contain healthful ingredients like stevia, honey, lactose-free chocolate ingredients, non-hydrogenated fats, and others. These developments significantly contribute to increasing opportunities in the market for different chocolate products. Innovative new products and consumers attract to new innovations in dark chocolate so expecting major opportunities for the Sweet Dark Chocolate Market.

Segmentation Analysis Of Sweet Dark Chocolate Market

Sweet Dark Chocolate Market segments cover the Type, Product, Application, Distribution Channel, and Region.

By Type, 70% Cocoa Dark Chocolate segment is Anticipated to Dominate the Market Over the Forecast period.

- A dark chocolate bar with a 70% cocoa content means that the cocoa bean alone provided 70% of the components used to create the chocolate. The remaining 30% will be made up of additional ingredients, mostly sugar, but they could also contain extremely minor amounts of vanilla flavouring.

- Generally speaking, dark chocolate that contains a larger percentage of cacao solids has fatter than sugar. It is advisable to choose dark chocolate that contains at least 70% cacao solids or more because more cacao also means more flavanols.

- This chocolate bar magically mixes all of your favourite salty, nutty, and sweet flavours into one delicious package. In Boulder, Colorado, in the United States, Chocolove's chocolate is produced using the traditional methods used by the best chocolatiers in Europe. Each Chocolove bar comes with a love poem enclosed in its wrapper and is made "with love" from all-natural ingredients.

Regional Analysis of the Sweet Dark Chocolate Market

Europe is Expected to Dominate the Market Over the Forecast Period.

- Europe dominated the global market in 2021, with a value of USD 19.95 billion. Belgium, the Netherlands, Germany, and Switzerland are home to several of the world's largest industrial chocolate producers, making Europe a center for the manufacturing of industrial chocolate.

- The region is the top producer and consumer of chocolate and chocolate-related goods. Because European consumers source cocoa beans of varied quality and origins to satisfy the need of the cocoa and chocolate industries, the European cocoa market is extremely diverse.

- Europe is the leading importer of cocoa beans worldwide, with 61% of global imports. The Center for the Promotion of Imports from Developing Countries (CBI) estimates that Europe imported 2.3 million tonnes of cocoa beans overall in 2020. Between 2016 and 2020, direct imports to Europe from nations that produce chocolate climbed by 1.4%.

- The demand for chocolate made with responsibly sourced cocoa has also increased as consumers' understanding of sustainable cocoa production has grown. The regional sustainability platforms are working more closely together to increase transparency.

Top Key Players Covered in Sweet Dark Chocolate Market

- Cemoi Chocolatier (France)

- Republica del Cacao (Ecuador)

- Nestlé S.A. (Switzerland)

- Mars Incorporated (U.S.)

- Fuji Oil Holdings Inc. (Japan)

- Guittard Chocolate Co. (U.S.)

- Ghirardelli Chocolate Co. (U.S.)

- Varihona Inc. (France)

- Barry Callebaut AG (Switzerland)

- Alpezzi Chocolate SA De CV (Mexico)

- Kerry Group Plc (Ireland)

- Olam International Ltd. (Singapore)

- Tcho Ventures Inc. (U.S.)

- The Hershey Company (U.S.)

- Cargill Incorporated (U.S.)

- Blommer Chocolate Company (U.S.)

- Foley's Candies LP (Canada)

- Puratos Group Nv (Belgium)

- Ferrero International S.A. (Italy)

- Mars, Inc, (U.S.)

- Mondelez International (U.S.)

- Meiji Co Ltd (Japan)

- Lindt, Ritter Sport (Switzerland)

- Amul, Blommer Chocolate Company (India)

- Brookside Foods (Canada)

- Chocolate Frey (Switzerland)

- Ezaki Glico (Japan)

- Other Active Players

Key Industry Developments in the Sweet Dark Chocolate Market

- In July 2023, Nestlé acquired Van Mouten, a Dutch cocoa processor known for its high-quality dark chocolate ingredients. This acquisition gives Nestlé greater control over its supply chain and allows it to develop new dark chocolate products with unique flavors and textures.

- In June 2023, Hershey's, a major American chocolate company, launched its Special Dark Crafted Collection. This line features three dark chocolate bars infused with unique ingredients like sea salt and almonds, targeting consumers seeking gourmet dark chocolate experiences.

- In May 2023, Swiss chocolate giant Lindt & Sprüngli announced the acquisition of Russel Stover Chocolates, an American confectionery company known for its dark chocolate offerings. This move strengthens Lindt's presence in the North American market and expands its dark chocolate portfolio.

- In February 2023, Tony Chocolonely, a Dutch ethical chocolate brand, launched its first oat milk chocolate bar. This move caters to the growing demand for plant-based alternatives in the dark chocolate market.

|

Sweet Dark Chocolate Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 9.09 Bn. |

|

Forecast Period 2025-32 CAGR: |

5.82% |

Market Size in 2032: |

USD 14.29 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Product |

|

||

|

By Application |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Sweet Dark Chocolate Market by Type (2018-2032)

4.1 Sweet Dark Chocolate Market Snapshot and Growth Engine

4.2 Market Overview

4.3 70% Cocoa Dark Chocolate

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 75% Cocoa Dark Chocolate

4.5 80% Cocoa Dark Chocolate

4.6 90% Cocoa Dark Chocolate

Chapter 5: Sweet Dark Chocolate Market by Product (2018-2032)

5.1 Sweet Dark Chocolate Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Bitter Chocolate

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Pure Bitter Chocolate

5.5 Semi-Sweet Chocolate

5.6 Organic Dark Chocolates

5.7 Inorganic Dark Chocolates

Chapter 6: Sweet Dark Chocolate Market by Application (2018-2032)

6.1 Sweet Dark Chocolate Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Beverages

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Food And bakery

6.5 Personal Care & Cosmetics

6.6 Pharmaceuticals

6.7 Others

Chapter 7: Sweet Dark Chocolate Market by Distribution Channel (2018-2032)

7.1 Sweet Dark Chocolate Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Supermarket/Hypermarket

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Speciality Store

7.5 Convenience Store

7.6 Others

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Sweet Dark Chocolate Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 CVS HEALTH(US)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 ALBERTSONS COMPANIES (US)

8.4 AHOLD DELHAIZE (NETHERLANDS)

8.5 THE JEAN COUTU GROUP (PJC) INC (CANADA)

8.6 WALGREENS BOOTS ALLIANCE INC (US)

8.7 WELLNESS FOREVER PHARMACY (INDIA)

8.8 DIRK ROSSMANN GMBH (GERMANY)

8.9 RITE AID CORP (US)

8.10 MEDPLUS HEALTH SERVICES PRIVATE LIMITED (INDIA)

8.11

Chapter 9: Global Sweet Dark Chocolate Market By Region

9.1 Overview

9.2. North America Sweet Dark Chocolate Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Type

9.2.4.1 70% Cocoa Dark Chocolate

9.2.4.2 75% Cocoa Dark Chocolate

9.2.4.3 80% Cocoa Dark Chocolate

9.2.4.4 90% Cocoa Dark Chocolate

9.2.5 Historic and Forecasted Market Size by Product

9.2.5.1 Bitter Chocolate

9.2.5.2 Pure Bitter Chocolate

9.2.5.3 Semi-Sweet Chocolate

9.2.5.4 Organic Dark Chocolates

9.2.5.5 Inorganic Dark Chocolates

9.2.6 Historic and Forecasted Market Size by Application

9.2.6.1 Beverages

9.2.6.2 Food And bakery

9.2.6.3 Personal Care & Cosmetics

9.2.6.4 Pharmaceuticals

9.2.6.5 Others

9.2.7 Historic and Forecasted Market Size by Distribution Channel

9.2.7.1 Supermarket/Hypermarket

9.2.7.2 Speciality Store

9.2.7.3 Convenience Store

9.2.7.4 Others

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Sweet Dark Chocolate Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Type

9.3.4.1 70% Cocoa Dark Chocolate

9.3.4.2 75% Cocoa Dark Chocolate

9.3.4.3 80% Cocoa Dark Chocolate

9.3.4.4 90% Cocoa Dark Chocolate

9.3.5 Historic and Forecasted Market Size by Product

9.3.5.1 Bitter Chocolate

9.3.5.2 Pure Bitter Chocolate

9.3.5.3 Semi-Sweet Chocolate

9.3.5.4 Organic Dark Chocolates

9.3.5.5 Inorganic Dark Chocolates

9.3.6 Historic and Forecasted Market Size by Application

9.3.6.1 Beverages

9.3.6.2 Food And bakery

9.3.6.3 Personal Care & Cosmetics

9.3.6.4 Pharmaceuticals

9.3.6.5 Others

9.3.7 Historic and Forecasted Market Size by Distribution Channel

9.3.7.1 Supermarket/Hypermarket

9.3.7.2 Speciality Store

9.3.7.3 Convenience Store

9.3.7.4 Others

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Sweet Dark Chocolate Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Type

9.4.4.1 70% Cocoa Dark Chocolate

9.4.4.2 75% Cocoa Dark Chocolate

9.4.4.3 80% Cocoa Dark Chocolate

9.4.4.4 90% Cocoa Dark Chocolate

9.4.5 Historic and Forecasted Market Size by Product

9.4.5.1 Bitter Chocolate

9.4.5.2 Pure Bitter Chocolate

9.4.5.3 Semi-Sweet Chocolate

9.4.5.4 Organic Dark Chocolates

9.4.5.5 Inorganic Dark Chocolates

9.4.6 Historic and Forecasted Market Size by Application

9.4.6.1 Beverages

9.4.6.2 Food And bakery

9.4.6.3 Personal Care & Cosmetics

9.4.6.4 Pharmaceuticals

9.4.6.5 Others

9.4.7 Historic and Forecasted Market Size by Distribution Channel

9.4.7.1 Supermarket/Hypermarket

9.4.7.2 Speciality Store

9.4.7.3 Convenience Store

9.4.7.4 Others

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Sweet Dark Chocolate Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Type

9.5.4.1 70% Cocoa Dark Chocolate

9.5.4.2 75% Cocoa Dark Chocolate

9.5.4.3 80% Cocoa Dark Chocolate

9.5.4.4 90% Cocoa Dark Chocolate

9.5.5 Historic and Forecasted Market Size by Product

9.5.5.1 Bitter Chocolate

9.5.5.2 Pure Bitter Chocolate

9.5.5.3 Semi-Sweet Chocolate

9.5.5.4 Organic Dark Chocolates

9.5.5.5 Inorganic Dark Chocolates

9.5.6 Historic and Forecasted Market Size by Application

9.5.6.1 Beverages

9.5.6.2 Food And bakery

9.5.6.3 Personal Care & Cosmetics

9.5.6.4 Pharmaceuticals

9.5.6.5 Others

9.5.7 Historic and Forecasted Market Size by Distribution Channel

9.5.7.1 Supermarket/Hypermarket

9.5.7.2 Speciality Store

9.5.7.3 Convenience Store

9.5.7.4 Others

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Sweet Dark Chocolate Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Type

9.6.4.1 70% Cocoa Dark Chocolate

9.6.4.2 75% Cocoa Dark Chocolate

9.6.4.3 80% Cocoa Dark Chocolate

9.6.4.4 90% Cocoa Dark Chocolate

9.6.5 Historic and Forecasted Market Size by Product

9.6.5.1 Bitter Chocolate

9.6.5.2 Pure Bitter Chocolate

9.6.5.3 Semi-Sweet Chocolate

9.6.5.4 Organic Dark Chocolates

9.6.5.5 Inorganic Dark Chocolates

9.6.6 Historic and Forecasted Market Size by Application

9.6.6.1 Beverages

9.6.6.2 Food And bakery

9.6.6.3 Personal Care & Cosmetics

9.6.6.4 Pharmaceuticals

9.6.6.5 Others

9.6.7 Historic and Forecasted Market Size by Distribution Channel

9.6.7.1 Supermarket/Hypermarket

9.6.7.2 Speciality Store

9.6.7.3 Convenience Store

9.6.7.4 Others

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Sweet Dark Chocolate Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Type

9.7.4.1 70% Cocoa Dark Chocolate

9.7.4.2 75% Cocoa Dark Chocolate

9.7.4.3 80% Cocoa Dark Chocolate

9.7.4.4 90% Cocoa Dark Chocolate

9.7.5 Historic and Forecasted Market Size by Product

9.7.5.1 Bitter Chocolate

9.7.5.2 Pure Bitter Chocolate

9.7.5.3 Semi-Sweet Chocolate

9.7.5.4 Organic Dark Chocolates

9.7.5.5 Inorganic Dark Chocolates

9.7.6 Historic and Forecasted Market Size by Application

9.7.6.1 Beverages

9.7.6.2 Food And bakery

9.7.6.3 Personal Care & Cosmetics

9.7.6.4 Pharmaceuticals

9.7.6.5 Others

9.7.7 Historic and Forecasted Market Size by Distribution Channel

9.7.7.1 Supermarket/Hypermarket

9.7.7.2 Speciality Store

9.7.7.3 Convenience Store

9.7.7.4 Others

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Sweet Dark Chocolate Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 9.09 Bn. |

|

Forecast Period 2025-32 CAGR: |

5.82% |

Market Size in 2032: |

USD 14.29 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Product |

|

||

|

By Application |

|

||

|

By Distribution Channel |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||