Surgical Scissors Market Synopsis

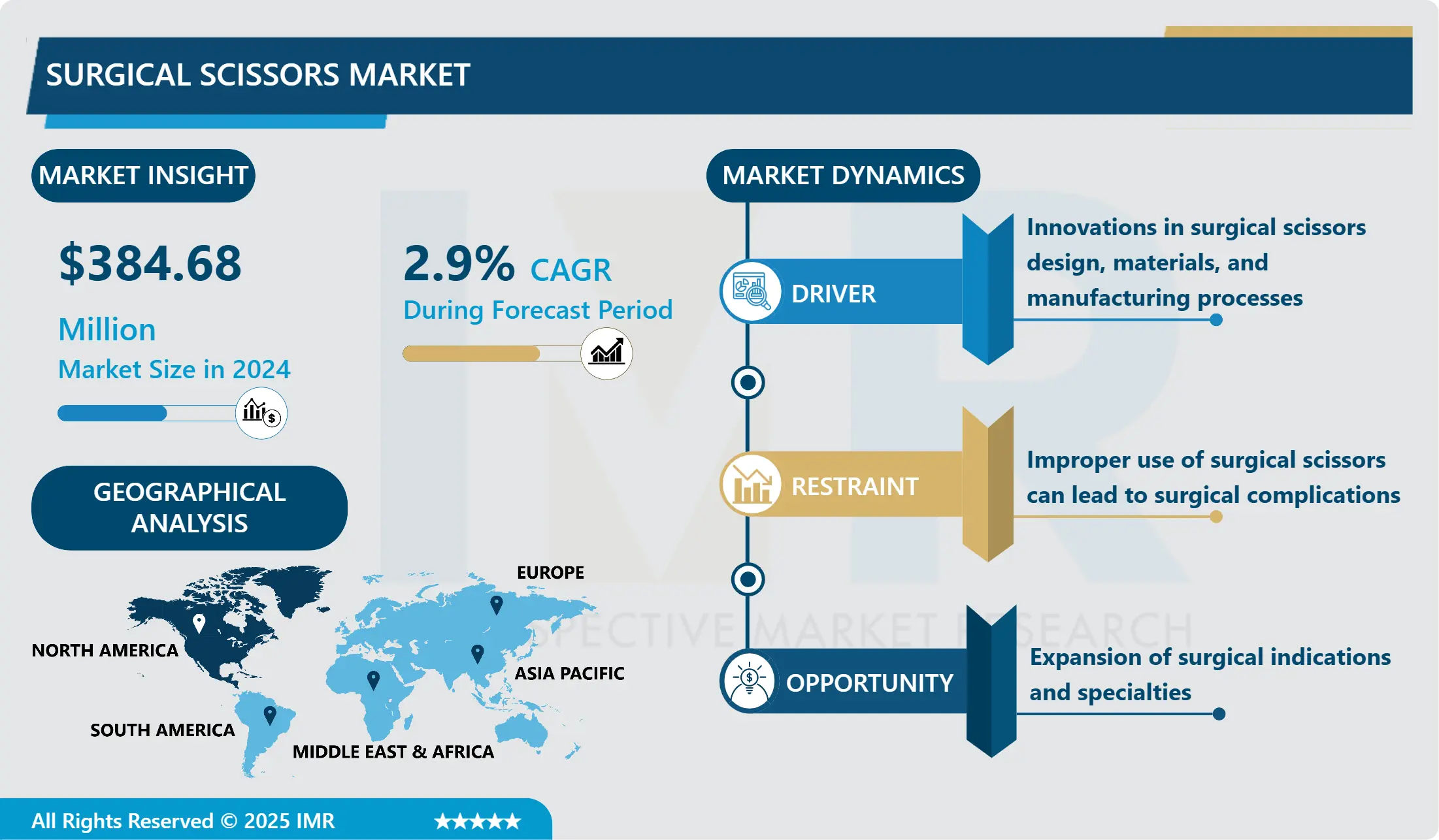

Surgical Scissors Market Size Was Valued at USD 384.68 Million in 2024, and is Projected to Reach USD 526.83 Million by 2035, Growing at a CAGR of 2.9% From 2025-2035.

Surgical scissors are medical instruments used by healthcare professionals, particularly surgeons, during surgical procedures to cut tissues, sutures, or other materials. They are typically made of high-quality stainless steel and come in various shapes and sizes, each designed for specific purposes. Surgical scissors have sharp blades that enable precise cutting and are an essential tool in any surgical setting.

Surgical scissors are specialized medical instruments used in a variety of surgical procedures for cutting tissues, sutures, bandages, and other materials. They are designed with precision blades and handles to provide surgeons and medical professionals with control, accuracy, and ease of use. It is also used to dissect and separate tissues during surgical procedures. They are commonly employed in procedures such as incisions, excisions, and tissue removal.

Surgical scissors are used to cut the sutures. This helps to complete the surgical closure and ensures that the sutures are properly trimmed. Surgical scissors are used to trim excess tissue or to shape tissues as needed during surgical procedures. This may be necessary to achieve proper wound closure or to remove diseased or damaged tissue. Surgical scissors are used for hemostasis, which involves cutting blood vessels to control bleeding.

Surgical scissors may be used for both sharp and blunt dissection techniques. Microsurgical scissors are designed for fine and delicate procedures, such as ophthalmic surgery, neurosurgery, and microvascular surgery. Surgical scissors may also be used in orthopedic surgery for procedures such as tendon repair, ligament reconstruction, and bone cutting. In plastic and reconstructive surgery, surgical scissors are used for procedures such as tissue grafting, scar revision, and cosmetic surgery.

Performing fine dissection, cutting through tough tissues, or trimming sutures, surgical scissors offer versatility and control for surgeons. Surgical scissors are manufactured to meet stringent quality standards and undergo rigorous testing to ensure their reliability and durability in surgical settings. They are typically made from high-grade stainless steel or other medical-grade materials to withstand repeated sterilization processes and maintain sharpness over time.

High-quality surgical scissors are designed to minimize tissue trauma, reduce the risk of infections, and enhance surgical outcomes. The demand for surgical scissors is driven by the growing prevalence of surgical procedures worldwide due to factors such as population growth, aging populations, advancements in medical technology, and increasing healthcare access. As surgical volumes continue to rise, the need for surgical instruments, including scissors, also increases to meet the demands of healthcare facilities and surgical teams.

Healthcare spending and investment in medical infrastructure and equipment contribute to the demand for surgical instruments, including scissors, in both developed and developing regions. Government healthcare initiatives, private sector investments, and technological advancements in healthcare systems drive the adoption of surgical procedures and the need for high-quality surgical instruments.

Surgical Scissors Market Trend Analysis

Driver

Innovations in surgical scissors design, materials, and manufacturing processes

- Innovations in ergonomic handle design aim to improve the comfort and usability of surgical scissors for healthcare professionals. Ergonomically designed handles reduce hand fatigue and discomfort during prolonged surgical procedures, enhancing surgeon efficiency and precision. These advancements make surgical scissors more user-friendly, leading to increased adoption and demand among medical professionals. Precision cutting edges are a key feature of modern surgical scissors. Advancements in cutting-edge design, such as sharper blade profiles and finer cutting tips, enable surgeons to achieve more accurate and controlled tissue dissection. Enhanced cutting performance reduces tissue trauma, minimizes blood loss, and improves surgical outcomes.

- Specialized coatings applied to surgical scissors offer several benefits, including improved durability, corrosion resistance, and ease of cleaning. Coatings such as titanium nitride or diamond-like carbon enhance the hardness and wear resistance of scissor blades, extending their lifespan and reducing the need for frequent replacements. However, antimicrobial coatings help prevent bacterial contamination and reduce the risk of surgical site infections, enhancing patient safety and reducing healthcare costs. Surgeons prefer surgical scissors with advanced coatings for their superior performance and long-term reliability.

- Advances in materials science have led to the development of new materials for surgical scissors, such as high-grade stainless-steel alloys, titanium, and medical-grade polymers. These materials offer superior strength, durability, and biocompatibility compared to traditional materials, improving the overall quality and performance of surgical scissors. Lightweight and corrosion-resistant materials enhance surgeon comfort and instrument longevity, driving the adoption of innovative surgical scissors in healthcare facilities worldwide.

Restraints

Improper use of surgical scissors can lead to surgical complications

- Improper use or mishandling of surgical scissors can lead to several adverse outcomes, including tissue damage, bleeding, and infections. Surgical scissors are designed to cut through various types of tissue during surgical procedures. However, if used improperly or with excessive force, they can cause unintended damage to surrounding tissues, including organs, blood vessels, nerves, and muscles. Tissue damage can prolong healing time, increase the risk of postoperative complications, and necessitate additional surgical interventions to repair the damage.

- Improper use of surgical scissors can result in unintended cuts or lacerations to blood vessels, leading to bleeding during surgery. Inadequate sterilization or contamination of surgical scissors can introduce microorganisms into the surgical site, increasing the risk of surgical site infections. Healthcare providers must adhere to strict infection control protocols and ensure proper sterilization of surgical instruments to minimize the risk of SSIs.

Opportunity

Expansion of surgical indications and specialties

- The expansion of surgical indications and specialties presents a significant opportunity for the diversification of the surgical scissors market. This opportunity arises from advances in medical technology, demographic trends, and evolving healthcare needs, which have led to the development of new surgical procedures and specialties. Ongoing advancements in medical technology have revolutionized surgical practices and expanded the scope of surgical interventions. New imaging modalities, surgical techniques, and medical devices have enabled healthcare providers to perform a broader range of surgical procedures with greater precision and efficacy.

- The evolving landscape of healthcare, coupled with demographic shifts such as an aging population and the increasing prevalence of chronic diseases, led to the emergence of new surgical specialties and subspecialties. These specialties address specialized healthcare needs and require specialized instruments tailored to their unique requirements. The expansion of surgical indications and specialties has resulted in the diversification of surgical procedures performed across various medical disciplines. From cardiovascular surgery and orthopedic surgery to plastic surgery and oncologic surgery, there is a wide spectrum of surgical procedures that require specific instruments, including scissors, optimized for their unique anatomical considerations and technical requirements.

- The diversification creates opportunities for manufacturers to develop and market specialized scissors tailored to different surgical procedures and specialties. The increasing specialization and complexity of surgical procedures necessitate customization and innovation in surgical instrumentation, including scissors. Manufacturers can leverage advances in materials science, design engineering, and manufacturing technology to develop innovative scissors with enhanced features, functionalities, and performance characteristics. Customized scissors designed for specific surgical indications and techniques can improve surgical outcomes, reduce intraoperative complications, and enhance patient safety and satisfaction.

Challenges

The surgical scissors market is highly competitive

- Surgical scissors, particularly standard models used in general surgical procedures, may lack significant differentiation in terms of design, features, or performance. companies struggle to differentiate their products from those of competitors, making it harder to attract and retain customers based on unique selling points. In a competitive market, building brand loyalty can be difficult, especially when customers perceive little difference between competing brands. Without strong brand recognition or loyalty, companies may find it challenging to retain customers or command premium pricing for their products.

- Companies must continually innovate and introduce new features or advancements in their surgical scissors. However, innovation can be costly and time-consuming, particularly for smaller manufacturers with limited resources. Moreover, rapid technological advancements may necessitate frequent updates to product offerings to remain competitive. Compliance with quality standards and regulatory guidelines is essential for market entry and maintaining competitiveness. However, these requirements add an additional layer of challenge, particularly for smaller companies with limited resources.

Surgical Scissors Market Segment Analysis:

Surgical Scissors Market Segmented based on Product type, Material Type, End User application, End-users, and Region.

By Product Type, Reusable segment is expected to dominate the market during the forecast period

- One of the key drivers of market growth is the cost-effectiveness of reusable Surgical Scissors. Compared to disposable alternatives, reusable scissors can be sterilized and used in multiple procedures, reducing the overall procedural costs for hospitals and surgical centers. This cost advantage has led to the widespread adoption of reusable instruments, especially in healthcare systems aiming to optimize healthcare expenditures.

- Technological advancements have also contributed to the growth of the reusable Surgical Scissors market. Instrument manufacturers have focused on improving the design, ergonomics, and functionality of reusable instruments to enhance surgical precision and patient outcomes.

- The growing prevalence of chronic diseases, such as obesity, gastrointestinal disorders, and gynecological conditions, drive the demand for laparoscopic procedures. These conditions often require surgical intervention, and laparoscopy offers a less invasive option with shorter recovery times.

By Material Type, Stainless Steel segment held the largest share in 2024

- Stainless steel is widely favored in surgical instruments, including scissors, due to its excellent properties such as corrosion resistance, durability, and strength. Surgical scissors made from stainless steel can withstand repeated sterilization cycles without rusting or corroding, ensuring long-term reliability and performance. Stainless steel is relatively cost-effective compared to alternative materials such as titanium or tungsten carbide. The cost-effectiveness makes stainless steel scissors more accessible and affordable for healthcare facilities, contributing to their widespread adoption and market dominance.

- Stainless steel is readily available and widely used in the manufacturing of surgical instruments worldwide. Its widespread availability ensures easy access to stainless steel scissors for healthcare providers and facilitates seamless integration into surgical procedures across various specialties and settings. Stainless steel surgical scissors have a long history of use in surgical settings and have established a proven track record of reliability, safety, and efficacy. Surgeons and healthcare professionals are familiar with stainless steel instruments and trust their performance and durability, leading to their continued preference and widespread adoption.

- Stainless steel surgical scissors are compatible with various sterilization methods, including steam autoclaving, ethylene oxide sterilization, and gamma irradiation. Stainless steel surgical scissors are manufactured by stringent regulatory standards and guidelines governing medical devices.

Surgical Scissors Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast Period

- North America, particularly the United States boasts advanced healthcare infrastructure with well-established healthcare systems, state-of-the-art medical facilities, and high standards of patient care. This robust healthcare infrastructure drives demand for surgical instruments, including scissors, to support a wide range of surgical procedures across various medical specialties. North America is a hub for medical technology innovation and research, with numerous companies investing in the development of advanced surgical instruments and equipment.

- The region's sizable healthcare market creates significant demand for medical devices and surgical instruments, including scissors, to meet the needs of healthcare facilities, surgeons, and patients. North America's high surgical procedure volumes are driven by factors such as the aging population, the prevalence of chronic diseases, and advancements in surgical techniques. Surgical scissors are essential tools used in a wide range of surgical procedures, including general surgery, orthopedic surgery, cardiovascular surgery, and minimally invasive procedures, contributing to their strong demand in the region.

Surgical Scissors Market Top Key Players:

- Ethicon, Inc. (US)

- Becton, Dickinson and Company (BD) (US)

- Integra LifeSciences Corporation (US)

- Stryker Corporation (US)

- Zimmer Biomet Holdings, Inc. (US)

- CONMED Corporation (US)

- CooperSurgical, Inc. (US)

- Aspen Surgical Products, Inc. (US)

- KARL STORZ Endoscopy-America, Inc. (US)

- Scanlan International, Inc. (US)

- Wexler Surgical (US)

- Roboz Surgical Instrument Co. (US)

- Fine Science Tools (US)

- Millennium Surgical Corp. (US)

- Sklar Surgical Instruments (US)

- GermedUSA Inc. (US)

- B. Braun Melsungen AG (Germany)

- Karl Storz GmbH & Co. KG (Germany)

- Reda Instrumente GmbH (Germany)

- KLS Martin Group (Germany)

- Medtronic plc (Ireland)

- Smith & Nephew plc (UK)

- Surgical Holdings (UK)

- Olympus Corporation (Japan)

- Terumo Corporation (Japan)

- Other Active Players

Key Industry Developments in the Surgical Scissors Market:

- In January 2024, Stryker a global leader in medical technologies, announced the launch of Prophecy Footprint, an expansion of the Prophecy Surgical Planning system, offering comprehensive surgical planning across the entire foot. The system will be demonstrated at the American College of Foot and Ankle. its launch in 2014, the Infinity Total Ankle System has been featured in multiple studies, with the largest series demonstrating 98.8% survivorship at the two-year mark.

- In June 2023, Becton, Dickinson, and Company a leading

|

Global Surgical Scissors Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 384.68 Mn |

|

Forecast Period 2025-35 CAGR: |

2.9 % |

Market Size in 2035: |

USD 526.83 Mn |

|

Segments Covered: |

By Product Type |

|

|

|

By Material Type |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Surgical Scissors Market by Product Type (2018-2032)

4.1 Surgical Scissors Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Reusable

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Disposable

Chapter 5: Surgical Scissors Market by Material Type (2018-2032)

5.1 Surgical Scissors Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Stainless Steel

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Titanium

Chapter 6: Surgical Scissors Market by End User (2018-2032)

6.1 Surgical Scissors Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Hospitals & Clinics

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Ambulatory surgical centers

6.5 Home care settings

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Surgical Scissors Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 STRYKER (US)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 TRUMPF (GERMANY)

7.4 KARL STORZ (GERMANY)

7.5 MIZUHO OSI (UNITED STATES)

7.6 SKYTRON (UNITED STATES)

7.7 STERIS (UNITED KINGDOM)

7.8 ESCHMANN (INDIA)

7.9 KENSWICK (USA)

7.10 MERIVAARA (EUROPE)

7.11 DRAEGER MEDICAL (INDIA)

7.12 A-DEC INC. (US)

7.13 BIHLERMED (US)

7.14 CV MEDICAL (US)

7.15 GETINGE AB (SWEDEN)

7.16 HERBERT WALDMANN GMBH & CO. KG (GERMANY)

7.17 HILL-ROM SERVICES INC. (US)

7.18 INTEGRA LIFE SCIENCES CORPORATION (ISRAEL)

7.19 KONINKLIJKE PHILIPS NV (NETHERLANDS)

7.20 SIMEON MEDICAL GMBH & CO. KG (GERMANY)

7.21 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS COLTD. (CHINA)

7.22 SUNNEX GROUP (SWEDEN)

7.23 TECHNOMED INDIA (INDIA).

Chapter 8: Global Surgical Scissors Market By Region

8.1 Overview

8.2. North America Surgical Scissors Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Product Type

8.2.4.1 Reusable

8.2.4.2 Disposable

8.2.5 Historic and Forecasted Market Size by Material Type

8.2.5.1 Stainless Steel

8.2.5.2 Titanium

8.2.6 Historic and Forecasted Market Size by End User

8.2.6.1 Hospitals & Clinics

8.2.6.2 Ambulatory surgical centers

8.2.6.3 Home care settings

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Surgical Scissors Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Product Type

8.3.4.1 Reusable

8.3.4.2 Disposable

8.3.5 Historic and Forecasted Market Size by Material Type

8.3.5.1 Stainless Steel

8.3.5.2 Titanium

8.3.6 Historic and Forecasted Market Size by End User

8.3.6.1 Hospitals & Clinics

8.3.6.2 Ambulatory surgical centers

8.3.6.3 Home care settings

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Surgical Scissors Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Product Type

8.4.4.1 Reusable

8.4.4.2 Disposable

8.4.5 Historic and Forecasted Market Size by Material Type

8.4.5.1 Stainless Steel

8.4.5.2 Titanium

8.4.6 Historic and Forecasted Market Size by End User

8.4.6.1 Hospitals & Clinics

8.4.6.2 Ambulatory surgical centers

8.4.6.3 Home care settings

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Surgical Scissors Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Product Type

8.5.4.1 Reusable

8.5.4.2 Disposable

8.5.5 Historic and Forecasted Market Size by Material Type

8.5.5.1 Stainless Steel

8.5.5.2 Titanium

8.5.6 Historic and Forecasted Market Size by End User

8.5.6.1 Hospitals & Clinics

8.5.6.2 Ambulatory surgical centers

8.5.6.3 Home care settings

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Surgical Scissors Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Product Type

8.6.4.1 Reusable

8.6.4.2 Disposable

8.6.5 Historic and Forecasted Market Size by Material Type

8.6.5.1 Stainless Steel

8.6.5.2 Titanium

8.6.6 Historic and Forecasted Market Size by End User

8.6.6.1 Hospitals & Clinics

8.6.6.2 Ambulatory surgical centers

8.6.6.3 Home care settings

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Surgical Scissors Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Product Type

8.7.4.1 Reusable

8.7.4.2 Disposable

8.7.5 Historic and Forecasted Market Size by Material Type

8.7.5.1 Stainless Steel

8.7.5.2 Titanium

8.7.6 Historic and Forecasted Market Size by End User

8.7.6.1 Hospitals & Clinics

8.7.6.2 Ambulatory surgical centers

8.7.6.3 Home care settings

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Surgical Scissors Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 384.68 Mn |

|

Forecast Period 2025-35 CAGR: |

2.9 % |

Market Size in 2035: |

USD 526.83 Mn |

|

Segments Covered: |

By Product Type |

|

|

|

By Material Type |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||