Sugar Market Synopsis

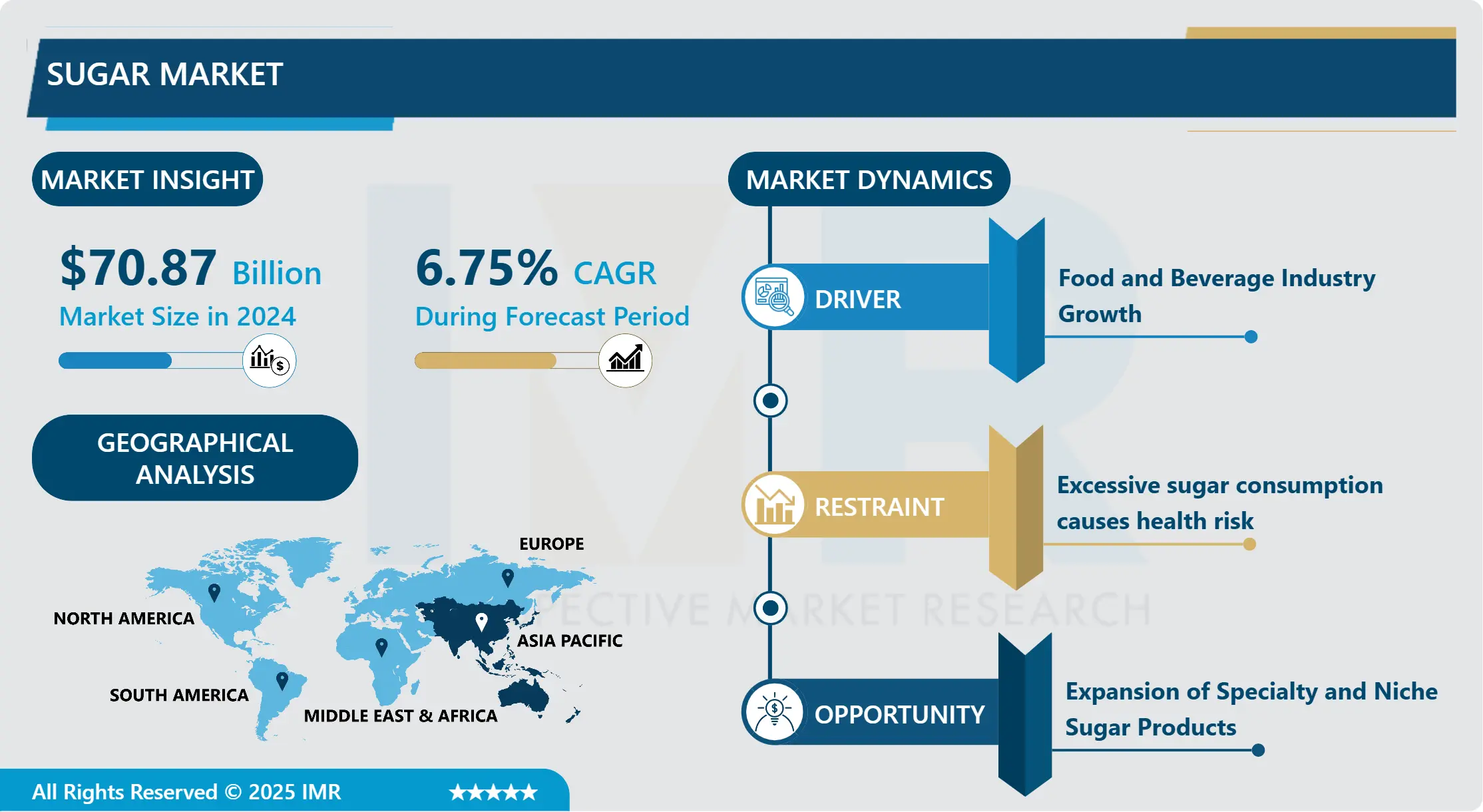

Sugar Market Size Was Valued at USD 70.87 Billion in 2024, and is Projected to Reach USD 119.51 Billion by 2032, Growing at a CAGR of 6.75% From 2025-2032.

The sugar market refers to the global industry involved in the production, processing, and distribution of sugar. It encompasses various types of sugar, including white, brown, and liquid sugars, derived from sources such as sugarcane, sugar beets, and alternative sweeteners. The market serves diverse end-use sectors such as food and beverage, pharmaceuticals, and industrial applications.

Sugar is a versatile ingredient used in various industries, including food and beverage, pharmaceuticals, healthcare, cosmetics, and the chemical industry. It serves as a sweetening agent, a preservative, and a binding agent in food processing. It also contributes to the texture, mouthfeel, and flavor profile of food products, enhancing their sensory appeal. Sugar undergoes browning reactions when heated, adding color, flavor, and aroma to baked goods. In food processing, it acts as a binding agent, holding ingredients together in cereal bars and granola.

In pharmaceuticals, it provides bulk, stability, and palatability to medications. Sugar-based lozenges and cough syrups are commonly used to soothe sore throats. In the industrial sector, sugar is used as a natural exfoliant in scrubs and body polishes, and as a renewable fuel source in biofuel production. It also finds use in art and craft projects and chemical industry processes. Sugar is a versatile ingredient in the food and beverage industry, used in various products such as baked goods, confectionery, beverages, dairy, and processed foods. Despite health concerns, consumer demand for sweetened products persists due to their familiar taste, affordability, and versatility.

Emerging markets' economic growth, urbanization, and changing lifestyles drive increased consumption of processed foods and beverages. Sugar also serves as a raw material in industries like pharmaceuticals, cosmetics, biofuels, and chemicals. As the global population grows, demand for sugar-containing products is expected to grow. The sugar industry invests in research and innovation to address consumer preferences, improve efficiency, and reduce environmental impact. Despite concerns about health implications, the sugar market remains resilient due to its widespread use across multiple industries and adaptability to changing consumer preferences.

Sugar Market Trend Analysis

Food and Beverage Industry Growth

- The food and beverage industry is a major global consumer of sugar, used in various products such as soft drinks, baked goods, confectionery, sauces, and dressings. The demand for these products is increasing due to factors like population growth, urbanization, and changing consumer lifestyles. Sugar plays multiple roles in food and beverage formulations, including as a sweetener, texture, and preservative. Its versatility makes it essential for developing new products to meet evolving consumer preferences and market trends.

- The growing demand for convenience foods and ready-to-drink beverages fuels sugar consumption. Processed and packaged foods often contain added sugars to enhance taste and appeal. Globalization and market expansion have led to increased production and distribution of sugar-containing products worldwide. The demand for sugar as a key ingredient remains strong across different regions and demographics.

- The food and beverage industry is characterized by continuous innovation and product development to meet changing consumer demands, health concerns, and regulatory requirements. Despite growing interest in reducing sugar content and exploring alternative sweeteners, sugar remains a staple ingredient in many formulations due to its unique functional properties and consumer acceptance.

Restraint

Excessive Sugar Consumption Causes Health Risk

- The sugar market is facing restraint due to health concerns linked to excessive sugar consumption. Consumers are increasingly seeking healthier alternatives to sugar, leading to regulatory measures such as sugar taxes and labeling requirements. As awareness of sugar's health risks grows, consumer preferences are shifting towards products with lower sugar content or alternative sweeteners.

- This trend is driving demand for sugar-free or reduced-sugar products in various food and beverage categories. Food manufacturers are responding by reformulating their products to reduce sugar content or introducing new products with alternative sweeteners, reshaping the sugar market landscape and driving competition.

- Sugar producers face market challenges, such as diversifying product offerings, investing in research and development, or exploring new markets. However, the growing awareness of health risks has created opportunities for sugar alternatives like stevia, erythritol, and monk fruit, which offer sweetness without the health risks associated with sugar.

Opportunity

Expansion of Specialty and Niche Sugar Products

- The sugar market is experiencing a significant opportunity due to the growth of specialty and niche sugar products. These products cater to health-conscious consumers who are seeking alternatives to traditional sugars due to concerns about processed ingredients, additives, and refined carbohydrates. They offer natural, minimally processed options with distinctive flavors, textures, and nutritional profiles.

- Manufacturers can diversify their product portfolios by offering organic, raw, unrefined, natural sweeteners, and exotic sugars. These products are often positioned as premium or gourmet offerings, commanding higher prices and margins. They can capitalize on health and wellness trends, targeting specific dietary preferences like paleo, keto, and vegan diets.

- The expansion of specialty and niche sugar products encourages ingredient innovation in the food and beverage industry, allowing manufacturers to create unique and functional sugar products tailored to consumer preferences. This targeted marketing approach can enhance brand loyalty and foster connections with niche consumer communities.

Challenge

Competition from Alternative Sweeteners

- The sugar market faces competition from alternative sweeteners, which offer sweetness without the calories or blood sugar spikes associated with traditional sugar. These sweeteners are marketed as healthier alternatives, appealing to consumers seeking to reduce calorie intake, manage weight, or control blood sugar levels.

- The food and beverage industry is constantly innovating to meet consumer demand for healthier products, with manufacturers reformulating products to reduce sugar content or replace sugar with alternative sweeteners. The growing popularity of alternative sweeteners has the potential to disrupt the sugar market by reducing demand for traditional sugar products, impacting producers, processors, and distributors.

- Regulatory agencies worldwide scrutinize the use of sugar and alternative sweeteners in food and beverage products, affecting market competition and consumer perceptions. Building trust and acceptance for alternative sweeteners requires education, transparency, and communication from manufacturers and regulatory authorities.

Sugar Market Segment Analysis:

Sugar Market is Segmented based on type, source, distribution channel, and end-users.

By Type, White Sugar segment is expected to dominate the market during the forecast period

- White sugar is a versatile sweetener used in various food and beverage products, including baked goods, confectionery, beverages, dairy products, and processed foods. Its neutral flavor makes it suitable for various recipes and culinary applications. White sugar is popular for its sweetness, texture, and ability to enhance flavors without adding distinct colors or flavor profiles.

- It is widely available in both developed and developing markets at relatively affordable prices, making it a preferred choice for manufacturers and consumers. White sugar is extensively used in the food processing industry due to its functional properties, such as preservatives, texture improvement, and bulk. Its well-established global production and distribution infrastructure ensures steady availability.

By Source, the Sugarcane segment held the largest share of 82.16% in 2024

- Sugarcane, a widely cultivated crop, is a reliable source of sugar due to its high yield potential and adaptability to diverse climates. Its high sugar content, high sucrose content, and well-established infrastructure support efficient extraction, processing, and distribution of sugarcane-derived sugar products. Sugarcane cultivation and production are crucial for many countries, providing employment opportunities and agricultural revenues.

- Governments often provide support and incentives to promote sugarcane cultivation and sugar production. Sugarcane-derived sugar is used in various industries, including food and beverage, pharmaceuticals, and cosmetics, contributing to its market dominance. Its cultural and historical significance has made it a staple ingredient in many cuisines and food traditions.

Sugar Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast Period

- The Asia-Pacific region, including China, India, Indonesia, and Pakistan, is experiencing significant population growth and increased demand for sugar. This growth is driven by economic development, urbanization, and the expansion of the food and beverage industry. Urban populations tend to have higher sugar consumption compared to rural areas.

- Sugar is a key ingredient in processed foods and beverages, contributing to the overall demand in the region. Major sugarcane producers in the region, such as India, Thailand, China, and Indonesia, support local sugar production and contribute to the region's dominance in the global sugar market. Government policies and subsidies in countries like India, which is one of the world's largest sugar producers, also influence sugar production and trade dynamics in the region.

Sugar Market Top Key Players:

- Cargill, Incorporated (US)

- Archer Daniels Midland Company (US)

- Bunge Limited (US)

- United Sugars Corporation (US)

- American Crystal Sugar Company (US)

- Sudzucker AG (Germany)

- Nordzucker AG (Germany)

- Associated British Foods plc (UK)

- Tereos (France)

- Louis Dreyfus Company (Netherlands)

- COFCO International (China)

- Guangxi Nanning Sugar Industry Co., Ltd. (China)

- E.I.D. Parry (India) Limited (India)

- Shree Renuka Sugars Limited (India)

- Dhampur Sugar Mills Ltd. (India)

- Tully Sugar Limited (Australia)

- Cosan Limited (Brazil)

- Raízen (Brazil)

- Biosev (Brazil)

- Tongaat Hulett (South Africa)

- Illovo Sugar Africa (South Africa), and other active players

Key Industry Developments in the Sugar Market:

- In August 2023, Sugar Refinery Sdn Bhd (CSR) launched its latest product, Better White Clear White Sugar, aiming to reinforce its position as Malaysia's premier sugar specialist. This introduction follows the success of CSR's Better Brown variant, which was introduced in 2018 to promote healthier sugar consumption and has since dominated 78% of the brown sugar segmentation in Malaysia. Better White aims to meet rising consumer expectations by offering high-quality sugar products at fair prices.

- In September 2023, British Sugar, and Sidel announced a groundbreaking partnership to introduce an innovative end-of-line solution. British Sugar, a subsidiary of Associated British Foods plc and a leading sugar producer in the Irish and British food and beverage markets, stands to benefit from this collaboration. Demonstrating a firm commitment to meeting market demands and exceeding retailer expectations, British Sugar processes approximately 8 million tonnes of sugar beet annually, resulting in up to 1.2 million tonnes of sugar production. The objective of this initiative is to replace British Sugar's outdated end-of-line system, which has been operational for over 38 years, with a cutting-edge solution. This new system will be equipped to manage high levels of complexity and automation, ensuring efficient handling of multiple SKUs.

|

Global Sugar Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

70.87 Bn |

|

Forecast Period 2025-32 CAGR: |

6.75% |

Market Size in 2032: |

119.51 Bn |

|

Segments Covered: |

By Type |

|

|

|

By Source |

|

||

|

By Distribution Channel |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Sugar Market by Type (2018-2032)

4.1 Sugar Market Snapshot and Growth Engine

4.2 Market Overview

4.3 White Sugar

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Brown Sugar

4.5 Liquid Sugar

Chapter 5: Sugar Market by Source (2018-2032)

5.1 Sugar Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Sugarcane

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Sugar Beets

Chapter 6: Sugar Market by Distribution Channel (2018-2032)

6.1 Sugar Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Supermarkets/Hypermarkets

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Convenience Stores

6.5 E-Commerce

Chapter 7: Sugar Market by End User (2018-2032)

7.1 Sugar Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Food and Beverage Industry

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Industrial Applications

7.5 Pharmaceuticals

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Sugar Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 INTERNATIONAL FLAVORS AND FRAGRANCE INC

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 DSM

8.4 INGREDION INCORPORATED

8.5 KERRY GROUP

8.6 CARGILL INCORPORATED

8.7 LYCORED GROUP

8.8 BALCHEM CORPORATION

8.9 AVEKA GROUP

8.10 ENCAPSYS

8.11 CLEXTRAL

8.12 VITASQUARE

8.13 TASTETECH ENCAPSULATION SOLUTION

8.14 DUPONT

8.15 SYMRISE

8.16 FRIESLAND CAMPINA

8.17 BASF SE

8.18 ADVANCED BIO NUTRITION CORPORATION

8.19 SPHERA ENCAPSULATION

Chapter 9: Global Sugar Market By Region

9.1 Overview

9.2. North America Sugar Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Type

9.2.4.1 White Sugar

9.2.4.2 Brown Sugar

9.2.4.3 Liquid Sugar

9.2.5 Historic and Forecasted Market Size by Source

9.2.5.1 Sugarcane

9.2.5.2 Sugar Beets

9.2.6 Historic and Forecasted Market Size by Distribution Channel

9.2.6.1 Supermarkets/Hypermarkets

9.2.6.2 Convenience Stores

9.2.6.3 E-Commerce

9.2.7 Historic and Forecasted Market Size by End User

9.2.7.1 Food and Beverage Industry

9.2.7.2 Industrial Applications

9.2.7.3 Pharmaceuticals

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Sugar Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Type

9.3.4.1 White Sugar

9.3.4.2 Brown Sugar

9.3.4.3 Liquid Sugar

9.3.5 Historic and Forecasted Market Size by Source

9.3.5.1 Sugarcane

9.3.5.2 Sugar Beets

9.3.6 Historic and Forecasted Market Size by Distribution Channel

9.3.6.1 Supermarkets/Hypermarkets

9.3.6.2 Convenience Stores

9.3.6.3 E-Commerce

9.3.7 Historic and Forecasted Market Size by End User

9.3.7.1 Food and Beverage Industry

9.3.7.2 Industrial Applications

9.3.7.3 Pharmaceuticals

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Sugar Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Type

9.4.4.1 White Sugar

9.4.4.2 Brown Sugar

9.4.4.3 Liquid Sugar

9.4.5 Historic and Forecasted Market Size by Source

9.4.5.1 Sugarcane

9.4.5.2 Sugar Beets

9.4.6 Historic and Forecasted Market Size by Distribution Channel

9.4.6.1 Supermarkets/Hypermarkets

9.4.6.2 Convenience Stores

9.4.6.3 E-Commerce

9.4.7 Historic and Forecasted Market Size by End User

9.4.7.1 Food and Beverage Industry

9.4.7.2 Industrial Applications

9.4.7.3 Pharmaceuticals

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Sugar Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Type

9.5.4.1 White Sugar

9.5.4.2 Brown Sugar

9.5.4.3 Liquid Sugar

9.5.5 Historic and Forecasted Market Size by Source

9.5.5.1 Sugarcane

9.5.5.2 Sugar Beets

9.5.6 Historic and Forecasted Market Size by Distribution Channel

9.5.6.1 Supermarkets/Hypermarkets

9.5.6.2 Convenience Stores

9.5.6.3 E-Commerce

9.5.7 Historic and Forecasted Market Size by End User

9.5.7.1 Food and Beverage Industry

9.5.7.2 Industrial Applications

9.5.7.3 Pharmaceuticals

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Sugar Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Type

9.6.4.1 White Sugar

9.6.4.2 Brown Sugar

9.6.4.3 Liquid Sugar

9.6.5 Historic and Forecasted Market Size by Source

9.6.5.1 Sugarcane

9.6.5.2 Sugar Beets

9.6.6 Historic and Forecasted Market Size by Distribution Channel

9.6.6.1 Supermarkets/Hypermarkets

9.6.6.2 Convenience Stores

9.6.6.3 E-Commerce

9.6.7 Historic and Forecasted Market Size by End User

9.6.7.1 Food and Beverage Industry

9.6.7.2 Industrial Applications

9.6.7.3 Pharmaceuticals

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Sugar Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Type

9.7.4.1 White Sugar

9.7.4.2 Brown Sugar

9.7.4.3 Liquid Sugar

9.7.5 Historic and Forecasted Market Size by Source

9.7.5.1 Sugarcane

9.7.5.2 Sugar Beets

9.7.6 Historic and Forecasted Market Size by Distribution Channel

9.7.6.1 Supermarkets/Hypermarkets

9.7.6.2 Convenience Stores

9.7.6.3 E-Commerce

9.7.7 Historic and Forecasted Market Size by End User

9.7.7.1 Food and Beverage Industry

9.7.7.2 Industrial Applications

9.7.7.3 Pharmaceuticals

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Sugar Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

70.87 Bn |

|

Forecast Period 2025-32 CAGR: |

6.75% |

Market Size in 2032: |

119.51 Bn |

|

Segments Covered: |

By Type |

|

|

|

By Source |

|

||

|

By Distribution Channel |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||