Global Plastic Rigid IBC Market Overview

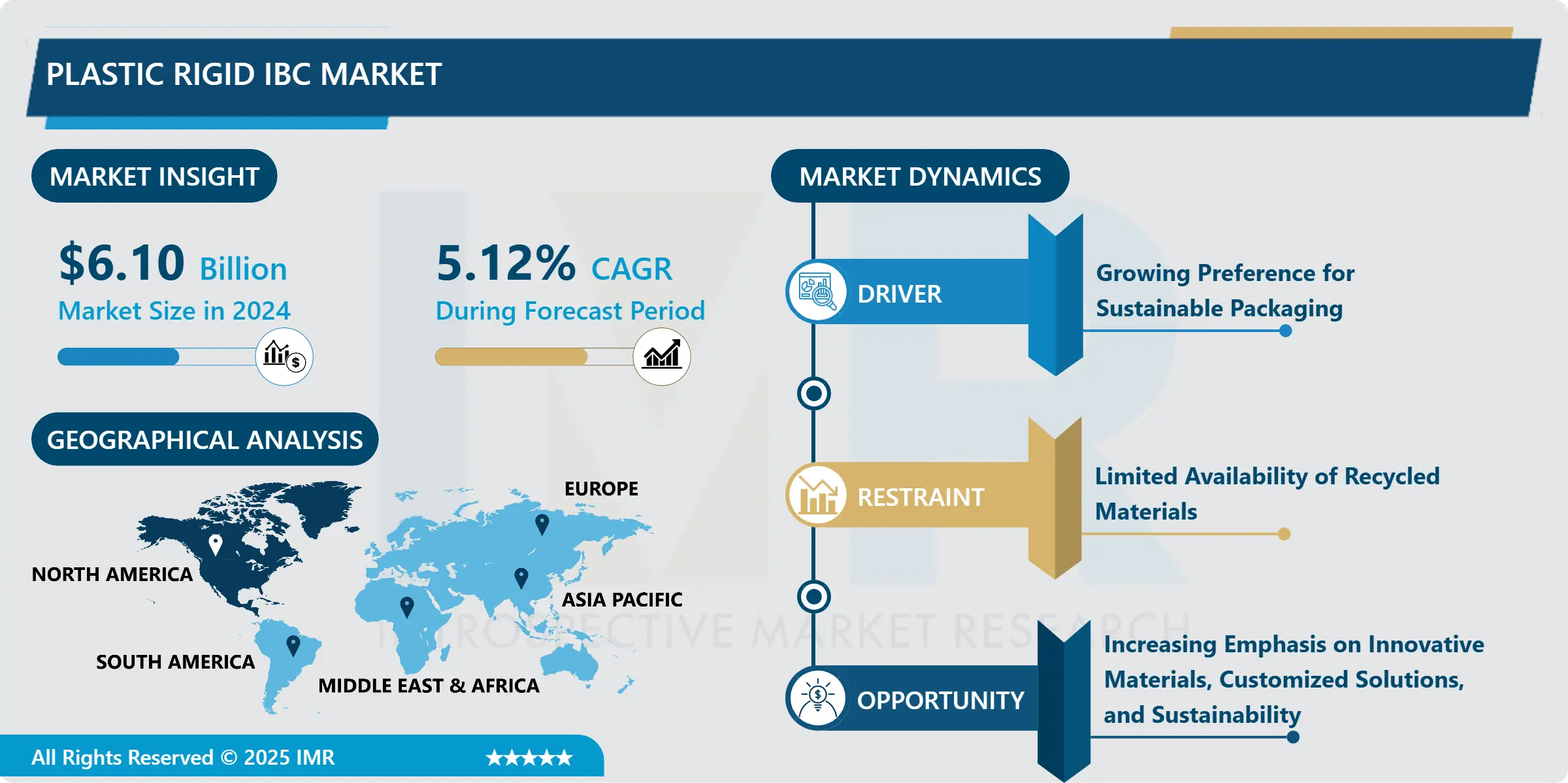

Plastic Rigid IBC Market Size Was Valued at USD 6.10 Billion in 2024, and is Projected to Reach USD 10.56 Billion by 2035, Growing at a CAGR of 5.12 % From 2025-2035.

A plastic rigid IBC, also known as an Intermediate Bulk Container, is a large, industrial-grade container used for storing, transporting, and handling various liquids and solids. They are typically made from high-density polyethylene (HDPE), a strong, durable, and chemically resistant material that can withstand the rigors of industrial environments. Plastic rigid IBCs are reusable and come in a variety of sizes and capacities to meet the specific needs of different industries.

Plastic rigid IBCs are durable and impact-resistant, made of HDPE, and compatible with a wide range of liquids and solids, including chemicals, solvents, and hazardous materials. They are reusable, reducing waste and environmental impact, and stackable, saving space during storage and transportation. These cost-effective options are commonly used in various industries, such as chemicals, food and beverage, pharmaceuticals, agriculture, and manufacturing.

The benefits of using plastic rigid IBCs include improved safety, reduced costs, reduced environmental impact, and increased efficiency. The durable and leak-proof design prevents spills and accidents, while the reusable nature reduces material handling costs. The reusability of plastic rigid IBCs also helps reduce waste and environmental impact. The stackable design also saves space, improving efficiency. Overall, plastic rigid IBCs are a versatile and cost-effective solution for storing, transporting, and handling various materials, making them a valuable asset for businesses in various industries.

Plastic Rigid IBC Market Trend Analysis:

Growing Preference for Sustainable Packaging

- This suggests that tastes in the business and among consumers are shifting in favour of ecologically friendly packaging options. Packaging that is considered sustainable usually uses resources that are renewable, recyclable, or biodegradable, among other practices that have a lower negative influence on the environment. Large, reusable industrial containers called plastic rigid intermediate bulk containers, or IBCs, are used for bulk and liquid material storage and transportation. Usually constructed of sturdy plastic, these containers support environmental objectives and are recyclable.

- The implies that the market for plastic rigid IBCs is expanding due in large part to consumers' increasing inclination toward sustainable packaging. The result is that, as part of their sustainable packaging plans, companies and industries are increasingly using plastic rigid IBCs. The claimed environmental benefits and compatibility with sustainability programs of plastic rigid IBCs may be driving greater demand for them. Businesses looking for environmentally friendly packaging solutions might discover greater opportunities in the plastic rigid IBC market. As sustainability continues to be a significant focus across various industries, the Plastic Rigid IBC Market stands to benefit from its alignment with the growing preference for sustainable packaging solutions.

Increasing Emphasis on Innovative Materials, Customized Solutions, and Sustainability

- Sustainability is gaining prominence in consumer preferences and corporate strategies, with businesses recognizing the importance of eco-friendly practices. This shift aligns with ethical considerations, opens new market segments, and enhances brand reputation, as there is a rising demand for sustainable products and services. Advanced materials are driving innovation and reshaping industries, with lightweight, high-strength, and environmentally friendly materials influencing manufacturing processes and product design. Companies investing in research and development to incorporate these materials gain a competitive edge by delivering improved performance, durability, and reduced environmental impact.

- The demand for customized solutions is transforming the market, as consumers seek products and services that cater to their unique needs across various sectors like technology, healthcare, and manufacturing. Offering tailored solutions enhances customer satisfaction and creates a competitive market niche for businesses. The increasing emphasis on sustainability, advanced materials, and customized solutions is not just a trend but a fundamental shift in business operations. Companies that integrate these principles into their strategies can capitalize on this market opportunity, addressing consumer expectations and fostering long-term resilience in an evolving economic landscape where sustainable and innovative practices are becoming synonymous with market leadership.

Plastic Rigid IBC Market Segment Analysis:

Plastic Rigid IBC Market Segmented on the basis of type, Capacity, and end-users.

By Type, HDPE Rigid IBC segment is expected to dominate the market during the forecast period

- High-density polyethylene intermediate bulk containers are popular due to their high melting temperature of 120-140 degrees Celsius, making them ideal for durability and temperature resistance, ensuring safe storage and transport of various materials in applications requiring temperature resistance. High-density polyethylene (HDPE IBCs) are popular due to their high density, enhancing their structural integrity and durability. HDPE IBCs offer superior tensile strength, making them suitable for handling substantial loads and providing reliable containment for a variety of products, making them suitable for handling diverse loads. High-density polyethylene intermediate bulk containers are known for their chemical resistance, making them ideal for storing and transporting various substances, ensuring material integrity and protecting against potential chemical interactions.

Plastic Rigid IBC Market Regional Insights:

North America is Expected to Dominate the Market Over the Forecast period

- North America is driving the growth of the Plastic Rigid Intermediate Bulk Container (IBC) Market due to its economic strength, technological advancements, and robust industrial landscape. Industries like chemicals, pharmaceuticals, and manufacturing demand IBCs for efficient bulk material storage and transportation. Advanced infrastructure and stringent quality standards in these sectors make durable and reliable packaging solutions a preferred choice. The region's regulatory environment prioritizes safety and environmental sustainability, promoting high-quality IBCs like Plastic Rigid IBCs for durability, reusability, and compliance with stringent safety regulations. North America's commitment to sustainability is driving growth in the market for Plastic Rigid IBCs, driven by the preference for eco-friendly packaging solutions and the preference for recyclable materials, shaping the future of sustainable industrial packaging.

Key Players Covered in Plastic Rigid IBC Market:

- Hoover Ferguson Group (United States)

- Greif (United States)

- Mauser Packaging Solutions (United States)

- Myers Industries (United States)

- Snyder Industries (United States)

- ACO Container Systems (Canada)

- SCHUTZ (Germany)

- Mauser Group (Germany)

- WERIT AG (Switzerland)

- MaschioPack GmbH (Italy)

- Pyramid Technoplast (Italy)

- Sotralentz (France)

- FACH-PAK Sp. z o.o. (Poland)

- Shijiheng (China)

- ZhenJiang JinShan Packing Factory (China)

- Shanghai Fujiang Plastic Industry Group (China)

- Jielin (China)

- NOVAX (China)

- Time Technoplast Limited (Hong Kong)

- Chuang Xiang (Taiwan)

- Sintex (India), and Other Major Players

Key Industry Developments in the Plastic Rigid IBC Market:

- In March 2024, Greif, Inc. completed its acquisition of Ipackchem Group SAS, a move anticipated to bolster its position as a global leader in industrial packaging. With a transaction value totaling $538 million plus additional fees, Greif now aims to leverage synergies and new market opportunities. The acquisition, funded through existing credit facilities, is expected to immediately enhance EBITDA margins.

- In November 2023, Mauser Packaging Solutions announced its definitive agreement to acquire Taenza, S.A. de C.V., a Mexico-based manufacturer specializing in tin-steel aerosol cans and steel pails. The acquisition aims to broaden Mauser's capabilities in rigid metal packaging. With Taenza's five manufacturing facilities across Mexico and over 850 employees, the deal positions Mauser to better serve customers in industries such as paint, coatings, and chemicals. Mark Burgess, CEO of Mauser, highlighted the alignment of values between the two companies.

|

Global Plastic Rigid IBC Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 6.10 Bn. |

|

Forecast Period 2025-35 CAGR: |

5.12% |

Market Size in 2035: |

USD 10.56 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Capacity |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Plastic Rigid IBC Market by Type (2018-2032)

4.1 Plastic Rigid IBC Market Snapshot and Growth Engine

4.2 Market Overview

4.3 HDPE Rigid IBC

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 LLDPE Rigid IBC

4.5 LDPE Rigid IBC

Chapter 5: Plastic Rigid IBC Market by Capacity (2018-2032)

5.1 Plastic Rigid IBC Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Up To 500 Liters

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 501 To 1000 Liters

5.5 1001 To 2000 Liters

5.6 Above 2000 Liters

Chapter 6: Plastic Rigid IBC Market by End User (2018-2032)

6.1 Plastic Rigid IBC Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Industrial Chemicals

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Petroleum & Lubricants

6.5 Paints Inks & Dyes

6.6 Food & Beverages

6.7 Building & Construction

6.8 Pharmaceuticals

6.9 Others

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Plastic Rigid IBC Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 MOTHER DIRT (U.S.)

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 ESTEE LAUDER INC. (U.S)

7.4 AMYRIS INC (U.S.)

7.5 PROCTER & GAMBLE CO. (U.S.)

7.6 TOO FACED COSMETICS

7.7 LLC (U.S.)

7.8 TULA LIFE INC (U.S.)

7.9 CLINIQUE LABORATORIES

7.10 LLC (U.S)

7.11 GLOWBIOTICS INC (U.S.)

7.12 THE CLOROX COMPANY (U.S.)

7.13 LAFLORE PROBIOTIC SKINCARE (U.S.)

7.14 BEBE & BELLA (U.S)

7.15 BURT'S BEES INC. (U.S.)

7.16 NUDE BRANDS (U.S.)

7.17 EMINENCE ORGANIC SKINCARE (CANADA)

7.18 AURELIA PROBIOTIC SKINCARE (UK)

7.19 UNILEVER PLC (UK)

7.20 L’OREAL S.A. (FRANCE)

7.21 LA ROCHE-POSAY (FRANCE)

7.22 ESSE SKINCARE (SOUTH AFRICA)

7.23 BIORE (JAPAN)

7.24

Chapter 8: Global Plastic Rigid IBC Market By Region

8.1 Overview

8.2. North America Plastic Rigid IBC Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Type

8.2.4.1 HDPE Rigid IBC

8.2.4.2 LLDPE Rigid IBC

8.2.4.3 LDPE Rigid IBC

8.2.5 Historic and Forecasted Market Size by Capacity

8.2.5.1 Up To 500 Liters

8.2.5.2 501 To 1000 Liters

8.2.5.3 1001 To 2000 Liters

8.2.5.4 Above 2000 Liters

8.2.6 Historic and Forecasted Market Size by End User

8.2.6.1 Industrial Chemicals

8.2.6.2 Petroleum & Lubricants

8.2.6.3 Paints Inks & Dyes

8.2.6.4 Food & Beverages

8.2.6.5 Building & Construction

8.2.6.6 Pharmaceuticals

8.2.6.7 Others

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Plastic Rigid IBC Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Type

8.3.4.1 HDPE Rigid IBC

8.3.4.2 LLDPE Rigid IBC

8.3.4.3 LDPE Rigid IBC

8.3.5 Historic and Forecasted Market Size by Capacity

8.3.5.1 Up To 500 Liters

8.3.5.2 501 To 1000 Liters

8.3.5.3 1001 To 2000 Liters

8.3.5.4 Above 2000 Liters

8.3.6 Historic and Forecasted Market Size by End User

8.3.6.1 Industrial Chemicals

8.3.6.2 Petroleum & Lubricants

8.3.6.3 Paints Inks & Dyes

8.3.6.4 Food & Beverages

8.3.6.5 Building & Construction

8.3.6.6 Pharmaceuticals

8.3.6.7 Others

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Plastic Rigid IBC Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Type

8.4.4.1 HDPE Rigid IBC

8.4.4.2 LLDPE Rigid IBC

8.4.4.3 LDPE Rigid IBC

8.4.5 Historic and Forecasted Market Size by Capacity

8.4.5.1 Up To 500 Liters

8.4.5.2 501 To 1000 Liters

8.4.5.3 1001 To 2000 Liters

8.4.5.4 Above 2000 Liters

8.4.6 Historic and Forecasted Market Size by End User

8.4.6.1 Industrial Chemicals

8.4.6.2 Petroleum & Lubricants

8.4.6.3 Paints Inks & Dyes

8.4.6.4 Food & Beverages

8.4.6.5 Building & Construction

8.4.6.6 Pharmaceuticals

8.4.6.7 Others

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Plastic Rigid IBC Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Type

8.5.4.1 HDPE Rigid IBC

8.5.4.2 LLDPE Rigid IBC

8.5.4.3 LDPE Rigid IBC

8.5.5 Historic and Forecasted Market Size by Capacity

8.5.5.1 Up To 500 Liters

8.5.5.2 501 To 1000 Liters

8.5.5.3 1001 To 2000 Liters

8.5.5.4 Above 2000 Liters

8.5.6 Historic and Forecasted Market Size by End User

8.5.6.1 Industrial Chemicals

8.5.6.2 Petroleum & Lubricants

8.5.6.3 Paints Inks & Dyes

8.5.6.4 Food & Beverages

8.5.6.5 Building & Construction

8.5.6.6 Pharmaceuticals

8.5.6.7 Others

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Plastic Rigid IBC Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Type

8.6.4.1 HDPE Rigid IBC

8.6.4.2 LLDPE Rigid IBC

8.6.4.3 LDPE Rigid IBC

8.6.5 Historic and Forecasted Market Size by Capacity

8.6.5.1 Up To 500 Liters

8.6.5.2 501 To 1000 Liters

8.6.5.3 1001 To 2000 Liters

8.6.5.4 Above 2000 Liters

8.6.6 Historic and Forecasted Market Size by End User

8.6.6.1 Industrial Chemicals

8.6.6.2 Petroleum & Lubricants

8.6.6.3 Paints Inks & Dyes

8.6.6.4 Food & Beverages

8.6.6.5 Building & Construction

8.6.6.6 Pharmaceuticals

8.6.6.7 Others

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Plastic Rigid IBC Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Type

8.7.4.1 HDPE Rigid IBC

8.7.4.2 LLDPE Rigid IBC

8.7.4.3 LDPE Rigid IBC

8.7.5 Historic and Forecasted Market Size by Capacity

8.7.5.1 Up To 500 Liters

8.7.5.2 501 To 1000 Liters

8.7.5.3 1001 To 2000 Liters

8.7.5.4 Above 2000 Liters

8.7.6 Historic and Forecasted Market Size by End User

8.7.6.1 Industrial Chemicals

8.7.6.2 Petroleum & Lubricants

8.7.6.3 Paints Inks & Dyes

8.7.6.4 Food & Beverages

8.7.6.5 Building & Construction

8.7.6.6 Pharmaceuticals

8.7.6.7 Others

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Global Plastic Rigid IBC Market |

|||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 6.10 Bn. |

|

Forecast Period 2025-35 CAGR: |

5.12% |

Market Size in 2035: |

USD 10.56 Bn. |

|

Segments Covered: |

By Type |

|

|

|

By Capacity |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||