Metal Alloy Market Synopsis

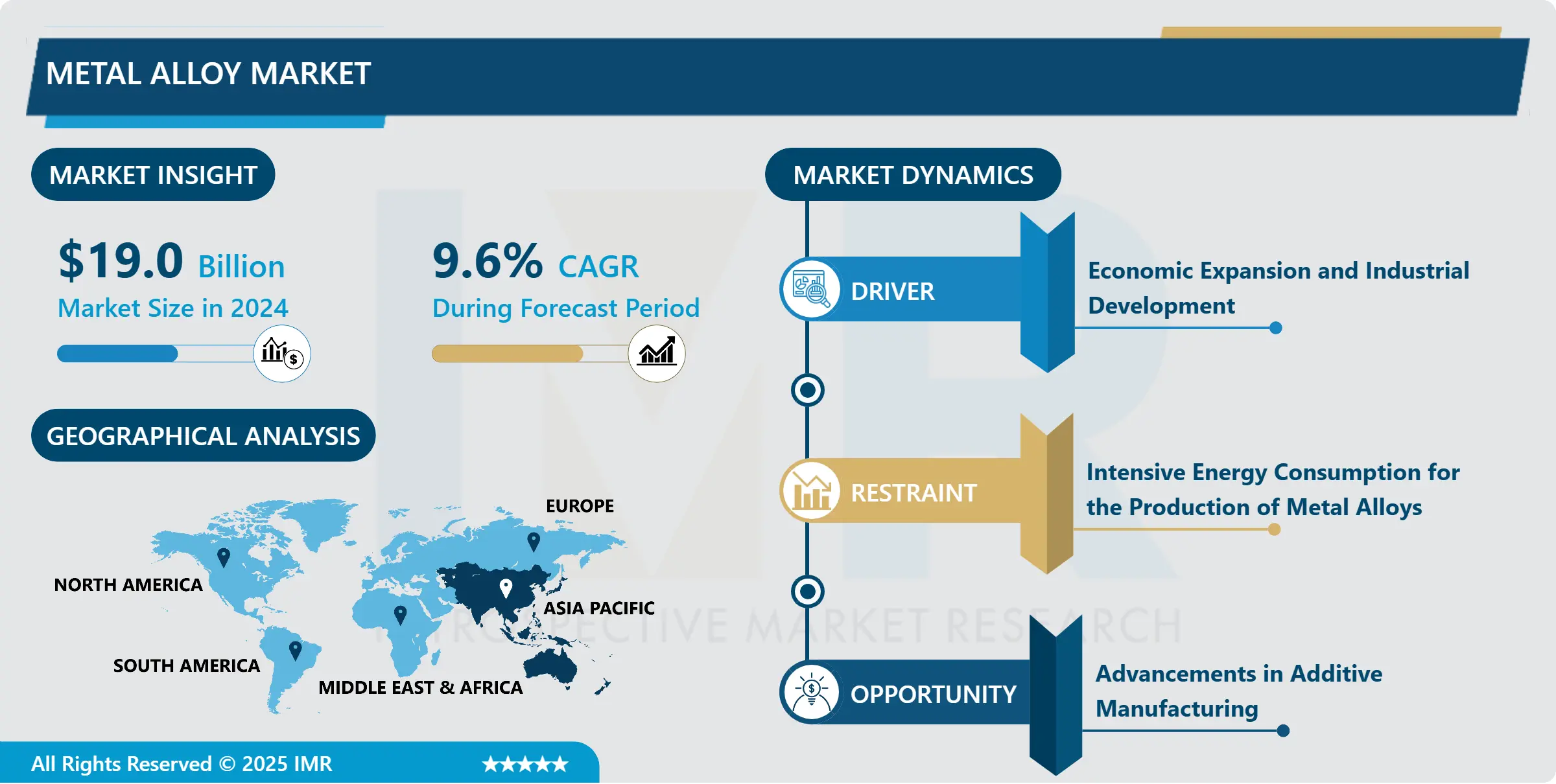

Metal Alloy Market Size Was Valued at USD 19.0 Billion in 2024, and is Projected to Reach USD 52.08 Billion by 2035, Growing at a CAGR of 9.6 % From 2025-2035.

A metal alloy is a material made by combining two or more metallic elements or a metal with a non-metallic element. This combination alters the properties of the original metals, often resulting in enhanced characteristics such as increased strength, durability, or corrosion resistance.

Metal alloys are versatile materials used in various industries, including automotive, construction, architecture, electronics, healthcare, consumer goods, and jewellery. They are used in engine components, chassis and body structures, exhaust systems, aircraft structures, jet engines, fasteners, infrastructure, printed circuit boards, connectors and housings, medical devices, diagnostic equipment, and consumer goods. Steel and aluminum alloys are used for engine blocks, pistons, and cylinder heads due to their strength and heat resistance. Stainless steel and nickel alloys are used for corrosion resistance and durability in exhaust systems. In the aerospace industry, titanium, aluminum, and composite materials are used in aircraft frames, wings, turbine blades, and fasteners.

Copper alloys are used for electrical wiring, plumbing, and roofing. In the healthcare industry, titanium, stainless steel, and cobalt-chromium alloys are used for implants, surgical instruments, and medical devices due to their biocompatibility, corrosion resistance, and mechanical properties. Copper and aluminum alloys are used in diagnostic equipment housings and components due to their electrical conductivity and lightweight properties. Precious metal alloys like gold, silver, and platinum are used in jewellery making. Alloys can be customized to meet specific performance requirements for different applications, offering a cost-effective solution compared to pure metals or alternative materials.

Metal alloys are in high demand due to their unique properties and diverse industries. They offer enhanced properties such as strength, durability, and lightweight, making them suitable for various applications. Aluminum and magnesium alloys are also prized for their lightweight properties, making them ideal for the automotive, aerospace, and transportation industries. High-temperature alloys, like nickel-based superalloys, retain their strength and integrity at elevated temperatures, making them ideal for applications in aerospace, power generation, and industrial processing. They also possess excellent electrical and thermal conductivity, making them essential in electrical wiring, electronic components, heat exchangers, and thermal management systems.

Metal Alloy Market Trend Analysis

Economic Expansion and Industrial Development

- Economic expansion and industrial development significantly impact the metal alloy market, driving demand and supply dynamics. Increased construction activity, infrastructure projects, manufacturing output, and consumer spending drive demand for metal alloys across various industries. For instance, the construction industry experiences increased demand for structural steel and aluminum alloys.

- The automotive and aerospace industries see higher demand for automobiles and aircraft, leading to increased demand for metal alloys used in manufacturing these vehicles. The electronics sector sees a greater demand for electronic devices, driving the need for specialized metal alloys with properties like conductivity, thermal management, and corrosion resistance. Investment in industrial infrastructure stimulates demand for metal alloys in machinery and equipment development.

- Technological advancements and innovation in materials science and manufacturing processes drive market growth. Globalization and trade facilitate international trade, allowing metal alloy producers to access new markets and supply chains. Government policies, such as tax incentives and infrastructure investments, can stimulate demand for metal alloys and support market growth.

Restraint

Intensive Energy Consumption for the Production of Metal Alloys

- The production of metal alloys is a highly energy-intensive process, causing high production costs and environmental impact. This can affect the competitiveness of producers, particularly in markets where cost efficiency is crucial. The combustion of fossil fuels in these processes can result in greenhouse gas emissions and environmental pollution, which is increasingly important due to climate change and sustainability concerns.

- The extraction and processing of raw materials like iron ore and bauxite also require significant energy inputs, contributing to resource depletion and industry sustainability concerns. Energy prices can significantly impact production costs, straining profit margins for alloy manufacturers. Technological challenges include developing more energy-efficient processes, and a competitive disadvantage in regions with high energy costs, impacting market share and investment decisions.

Opportunity

Advancements in Additive Manufacturing

- Additive manufacturing, also known as 3D printing, offers numerous benefits for the metal alloy market. It allows for the production of complex geometries and intricate designs, enabling lightweight, improved performance, and innovative product designs. This process reduces material waste, leading to cost savings and environmental benefits. Additive manufacturing also enables cost-effective production of customized metal alloy components, particularly in industries like healthcare, aerospace, and automotive.

- Rapid prototyping and iteration enable manufacturers to develop and test new components without expensive tooling or long lead times, accelerating the product development cycle and increasing innovation. Advanced additive manufacturing techniques like selective laser melting and electron beam melting enable the production of metal alloy components with complex material compositions, opening up new opportunities for high-performance alloys.

- On-demand production and localized manufacturing facilitate on-demand production, reducing supply chain complexity and inventory costs. Integrating additive manufacturing with digital technologies like AI, machine learning, and digital twin simulations enhances efficiency, reliability, and scalability, further driving the adoption of additive manufacturing in the metal alloy market.

Challenge

Interruptions in the Supply Chain can Lead to Shortages

- The metal alloy market faces significant challenges due to supply chain disruptions, which can occur due to factors such as natural disasters, labor strikes, regulatory changes, or resource depletion. These disruptions can lead to scarcity, price volatility, and increased production costs. Transportation delays can also occur due to congested ports, infrastructure limitations, adverse weather conditions, accidents, and labor disputes.

- Geopolitical tensions, such as trade disputes, sanctions, tariffs, and geopolitical conflicts, can disrupt the flow of raw materials and finished alloys across international borders, affecting the availability and pricing of alloys. This instability can undermine investor confidence, hinder long-term planning, and create uncertainty in the metal alloy industry.

Metal Alloy Market Segment Analysis:

Metal Alloy Market Segmented on the basis of type, application, form, and end-users.

By Type, Non- Ferrous Alloys segment is expected to dominate the market during the forecast period

- Non-ferrous alloys are widely used in various industries, including automotive, aerospace, electronics, construction, and healthcare. They offer unique properties like lightweightness, corrosion resistance, electrical conductivity, and thermal conductivity, making them suitable for various applications. The growing demand for lightweight materials, particularly aluminum and titanium alloys, is driven by fuel efficiency and environmental sustainability. These alloys are also highly corrosion resistant, making them ideal for harsh environments like marine and offshore structures.

- Emerging economies, such as China, India, and Brazil, are experiencing rapid industrialization and urbanization, driving the demand for these alloys in infrastructure development, consumer electronics, and automotive manufacturing. Technological advancements have also made high-performance non-ferrous alloys more attractive, making them more attractive in industries with critical performance requirements. Additionally, their high recycling rate offers environmental and economic benefits.

By Application, Structural Components segment held the largest share of 39.6% in 2023

- Metal alloy structural components are crucial in various industries like automotive, aerospace, construction, and machinery due to their high strength, durability, and reliability. They offer superior strength-to-weight ratios, making them ideal for lightweight applications. Metal alloys can be customized to meet specific performance requirements, allowing manufacturers to achieve desired properties like strength, stiffness, corrosion resistance, and fatigue resistance.

- Advancements in material science and manufacturing technologies have led to the development of advanced metal alloys with enhanced properties, expanding the range of applications and driving market growth. Regulatory standards and quality assurance requirements in safety-critical industries like aerospace and automotive also drive the demand for high-quality alloy structural components. Therefore, metal alloys that meet or exceed these standards are preferred by manufacturers.

Metal Alloy Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast Period

- APAC is experiencing rapid industrialization and urbanization, leading to a significant demand for metal alloys across various sectors. Countries like China, India, Japan, South Korea, and Southeast Asia are thriving in industries like automotive, aerospace, construction, electronics, and machinery manufacturing. APAC's diverse manufacturing base includes mass production of commodity alloys and specialized high-performance alloys for critical applications. The automotive and aerospace industries are expanding rapidly due to rising consumer demand, infrastructure development, and government initiatives.

- APAC countries are investing heavily in research and development to enhance metal alloy performance. Government policies support domestic industries, encourage innovation, and attract foreign investment. As disposable incomes rise and living standards improve, there is a growing demand for automobiles, consumer electronics, and infrastructure reliant on metal alloys. APAC countries play a crucial role in global supply chains, serving as manufacturing hubs and export destinations for metal alloys and finished products.

Metal Alloy Market Top Key Players:

- United States Steel Corporation (USA)

- AK Steel Holding Corporation (USA)

- Alcoa Corporation (USA)

- Nucor Corporation (USA)

- Novelis Inc. (USA)

- Allegheny Technologies Incorporated (USA)

- Novolipetsk Steel (Russia)

- Rusal (Russia)

- Thyssenkrupp AG (Germany)

- Outokumpu Oyj (Finland)

- SSAB AB (Sweden)

- China Baowu Steel Group Corporation Limited (China)

- Aluminum Corporation of China Limited (CHALCO) (China)

- Jiangsu Shagang Group Company Limited (China)

- Tata Steel Group (India)

- Nippon Steel Corporation (Japan)

- JFE Steel Corporation (Japan)

- Kobe Steel, Ltd. (Japan)

- Hyundai Steel Company (South Korea)

- POSCO (South Korea)

- Voestalpine AG (Austria)

- Vale S.A. (Brazil)

- Gerdau S.A. (Brazil)

- ArcelorMittal (Luxembourg)

- Tenaris S.A. (Luxembourg), and other major players

Key Industry Developments in the Metal Alloy Market:

- In December 2023, Nippon Steel Corporation (NSC) acquired U. S. Steel, Moving Forward Together as the Best Steelmaker with World-Leading Capabilities, Bringing together two storied companies with rich histories of providing excellent products and services and contributing to the development of society Combining world-leading technologies and manufacturing capabilities to better serve customers in the United States and globally Strengthens a diversified and competitive steel industry in the United States to the benefit of customers through investment collaboration between two global steel innovators

- In September 2022, Alcoa Corporation announced innovations in alloy development and deployment, further strengthening its position as a supplier of advanced aluminum alloys. The Company’s innovations include the introduction of a new high-strength, 6000 series alloy, A210 ExtruStrongTM, that delivers benefits across a wide range of extruded applications, including transport, construction, industrial, and consumer goods. Alcoa also announced that its C611 EZCastTM alloy, a high-performance alloy that does not require a dedicated heat treatment is being recognized this week.

- In July 2022, Novelis Inc., a leading sustainable aluminum solutions provider and the world leader in aluminum rolling and recycling, announced a strategic partnership with Sortera Alloys, Inc., an innovative industrial scrap metal sorting and recycling company. Novelis will take advantage of Sortera's advanced sorting technologies, including data analytics and advanced sensors, to recycle and reuse higher amounts of both automotive post-production and post-consumer scrap. With the use of the Sortera technology, Novelis will be able to effectively separate the mixed scrap into individual alloys and recycle them back into the same product, closing the loop. This will allow Novelis to meet original equipment makers' exacting needs for performance, durability, safety, and design.

|

Global Metal Alloy Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 19.0 Bn |

|

Forecast Period 2025-35 CAGR: |

9.6% |

Market Size in 2035: |

USD 52.08 Bn |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Form |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Metal Alloy Market by Type (2018-2035)

4.1 Metal Alloy Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Ferrous Alloys

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Non- Ferrous Alloys

4.5 Specialty Alloys

Chapter 5: Metal Alloy Market by Application (2018-2035)

5.1 Metal Alloy Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Structural Components

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Electrical Conductors

5.5 Heat Exchangers

5.6 Fasteners and Fittings

5.7 Consumer Goods

Chapter 6: Metal Alloy Market by Form (2018-2035)

6.1 Metal Alloy Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Sheets

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Bars and Rods

6.5 Powders

6.6 Foils

6.7 Tubes and Pipes

Chapter 7: Metal Alloy Market by End User (2018-2035)

7.1 Metal Alloy Market Snapshot and Growth Engine

7.2 Market Overview

7.3 Automotive

7.3.1 Introduction and Market Overview

7.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

7.3.3 Key Market Trends, Growth Factors, and Opportunities

7.3.4 Geographic Segmentation Analysis

7.4 Aerospace

7.5 Construction

7.6 Electronics

7.7 Healthcare

Chapter 8: Company Profiles and Competitive Analysis

8.1 Competitive Landscape

8.1.1 Competitive Benchmarking

8.1.2 Metal Alloy Market Share by Manufacturer (2024)

8.1.3 Industry BCG Matrix

8.1.4 Heat Map Analysis

8.1.5 Mergers and Acquisitions

8.2 UNITED STATES STEEL CORPORATION (USA)

8.2.1 Company Overview

8.2.2 Key Executives

8.2.3 Company Snapshot

8.2.4 Role of the Company in the Market

8.2.5 Sustainability and Social Responsibility

8.2.6 Operating Business Segments

8.2.7 Product Portfolio

8.2.8 Business Performance

8.2.9 Key Strategic Moves and Recent Developments

8.2.10 SWOT Analysis

8.3 AK STEEL HOLDING CORPORATION (USA)

8.4 ALCOA CORPORATION (USA)

8.5 NUCOR CORPORATION (USA)

8.6 NOVELIS INC. (USA)

8.7 ALLEGHENY TECHNOLOGIES INCORPORATED (USA)

8.8 NOVOLIPETSK STEEL (RUSSIA)

8.9 RUSAL (RUSSIA)

8.10 THYSSENKRUPP AG (GERMANY)

8.11 OUTOKUMPU OYJ (FINLAND)

8.12 SSAB AB (SWEDEN)

8.13 CHINA BAOWU STEEL GROUP CORPORATION LIMITED (CHINA)

8.14 ALUMINUM CORPORATION OF CHINA LIMITED (CHALCO) (CHINA)

8.15 JIANGSU SHAGANG GROUP COMPANY LIMITED (CHINA)

8.16 TATA STEEL GROUP (INDIA)

8.17 NIPPON STEEL CORPORATION (JAPAN)

8.18 JFE STEEL CORPORATION (JAPAN)

8.19 KOBE STEEL LTD. (JAPAN)

8.20 HYUNDAI STEEL COMPANY (SOUTH KOREA)

8.21 POSCO (SOUTH KOREA)

8.22 VOESTALPINE AG (AUSTRIA)

8.23 VALE S.A. (BRAZIL)

8.24 GERDAU S.A. (BRAZIL)

8.25 ARCELORMITTAL (LUXEMBOURG)

8.26 TENARIS S.A. (LUXEMBOURG)

8.27

Chapter 9: Global Metal Alloy Market By Region

9.1 Overview

9.2. North America Metal Alloy Market

9.2.1 Key Market Trends, Growth Factors and Opportunities

9.2.2 Top Key Companies

9.2.3 Historic and Forecasted Market Size by Segments

9.2.4 Historic and Forecasted Market Size by Type

9.2.4.1 Ferrous Alloys

9.2.4.2 Non- Ferrous Alloys

9.2.4.3 Specialty Alloys

9.2.5 Historic and Forecasted Market Size by Application

9.2.5.1 Structural Components

9.2.5.2 Electrical Conductors

9.2.5.3 Heat Exchangers

9.2.5.4 Fasteners and Fittings

9.2.5.5 Consumer Goods

9.2.6 Historic and Forecasted Market Size by Form

9.2.6.1 Sheets

9.2.6.2 Bars and Rods

9.2.6.3 Powders

9.2.6.4 Foils

9.2.6.5 Tubes and Pipes

9.2.7 Historic and Forecasted Market Size by End User

9.2.7.1 Automotive

9.2.7.2 Aerospace

9.2.7.3 Construction

9.2.7.4 Electronics

9.2.7.5 Healthcare

9.2.8 Historic and Forecast Market Size by Country

9.2.8.1 US

9.2.8.2 Canada

9.2.8.3 Mexico

9.3. Eastern Europe Metal Alloy Market

9.3.1 Key Market Trends, Growth Factors and Opportunities

9.3.2 Top Key Companies

9.3.3 Historic and Forecasted Market Size by Segments

9.3.4 Historic and Forecasted Market Size by Type

9.3.4.1 Ferrous Alloys

9.3.4.2 Non- Ferrous Alloys

9.3.4.3 Specialty Alloys

9.3.5 Historic and Forecasted Market Size by Application

9.3.5.1 Structural Components

9.3.5.2 Electrical Conductors

9.3.5.3 Heat Exchangers

9.3.5.4 Fasteners and Fittings

9.3.5.5 Consumer Goods

9.3.6 Historic and Forecasted Market Size by Form

9.3.6.1 Sheets

9.3.6.2 Bars and Rods

9.3.6.3 Powders

9.3.6.4 Foils

9.3.6.5 Tubes and Pipes

9.3.7 Historic and Forecasted Market Size by End User

9.3.7.1 Automotive

9.3.7.2 Aerospace

9.3.7.3 Construction

9.3.7.4 Electronics

9.3.7.5 Healthcare

9.3.8 Historic and Forecast Market Size by Country

9.3.8.1 Russia

9.3.8.2 Bulgaria

9.3.8.3 The Czech Republic

9.3.8.4 Hungary

9.3.8.5 Poland

9.3.8.6 Romania

9.3.8.7 Rest of Eastern Europe

9.4. Western Europe Metal Alloy Market

9.4.1 Key Market Trends, Growth Factors and Opportunities

9.4.2 Top Key Companies

9.4.3 Historic and Forecasted Market Size by Segments

9.4.4 Historic and Forecasted Market Size by Type

9.4.4.1 Ferrous Alloys

9.4.4.2 Non- Ferrous Alloys

9.4.4.3 Specialty Alloys

9.4.5 Historic and Forecasted Market Size by Application

9.4.5.1 Structural Components

9.4.5.2 Electrical Conductors

9.4.5.3 Heat Exchangers

9.4.5.4 Fasteners and Fittings

9.4.5.5 Consumer Goods

9.4.6 Historic and Forecasted Market Size by Form

9.4.6.1 Sheets

9.4.6.2 Bars and Rods

9.4.6.3 Powders

9.4.6.4 Foils

9.4.6.5 Tubes and Pipes

9.4.7 Historic and Forecasted Market Size by End User

9.4.7.1 Automotive

9.4.7.2 Aerospace

9.4.7.3 Construction

9.4.7.4 Electronics

9.4.7.5 Healthcare

9.4.8 Historic and Forecast Market Size by Country

9.4.8.1 Germany

9.4.8.2 UK

9.4.8.3 France

9.4.8.4 The Netherlands

9.4.8.5 Italy

9.4.8.6 Spain

9.4.8.7 Rest of Western Europe

9.5. Asia Pacific Metal Alloy Market

9.5.1 Key Market Trends, Growth Factors and Opportunities

9.5.2 Top Key Companies

9.5.3 Historic and Forecasted Market Size by Segments

9.5.4 Historic and Forecasted Market Size by Type

9.5.4.1 Ferrous Alloys

9.5.4.2 Non- Ferrous Alloys

9.5.4.3 Specialty Alloys

9.5.5 Historic and Forecasted Market Size by Application

9.5.5.1 Structural Components

9.5.5.2 Electrical Conductors

9.5.5.3 Heat Exchangers

9.5.5.4 Fasteners and Fittings

9.5.5.5 Consumer Goods

9.5.6 Historic and Forecasted Market Size by Form

9.5.6.1 Sheets

9.5.6.2 Bars and Rods

9.5.6.3 Powders

9.5.6.4 Foils

9.5.6.5 Tubes and Pipes

9.5.7 Historic and Forecasted Market Size by End User

9.5.7.1 Automotive

9.5.7.2 Aerospace

9.5.7.3 Construction

9.5.7.4 Electronics

9.5.7.5 Healthcare

9.5.8 Historic and Forecast Market Size by Country

9.5.8.1 China

9.5.8.2 India

9.5.8.3 Japan

9.5.8.4 South Korea

9.5.8.5 Malaysia

9.5.8.6 Thailand

9.5.8.7 Vietnam

9.5.8.8 The Philippines

9.5.8.9 Australia

9.5.8.10 New Zealand

9.5.8.11 Rest of APAC

9.6. Middle East & Africa Metal Alloy Market

9.6.1 Key Market Trends, Growth Factors and Opportunities

9.6.2 Top Key Companies

9.6.3 Historic and Forecasted Market Size by Segments

9.6.4 Historic and Forecasted Market Size by Type

9.6.4.1 Ferrous Alloys

9.6.4.2 Non- Ferrous Alloys

9.6.4.3 Specialty Alloys

9.6.5 Historic and Forecasted Market Size by Application

9.6.5.1 Structural Components

9.6.5.2 Electrical Conductors

9.6.5.3 Heat Exchangers

9.6.5.4 Fasteners and Fittings

9.6.5.5 Consumer Goods

9.6.6 Historic and Forecasted Market Size by Form

9.6.6.1 Sheets

9.6.6.2 Bars and Rods

9.6.6.3 Powders

9.6.6.4 Foils

9.6.6.5 Tubes and Pipes

9.6.7 Historic and Forecasted Market Size by End User

9.6.7.1 Automotive

9.6.7.2 Aerospace

9.6.7.3 Construction

9.6.7.4 Electronics

9.6.7.5 Healthcare

9.6.8 Historic and Forecast Market Size by Country

9.6.8.1 Turkiye

9.6.8.2 Bahrain

9.6.8.3 Kuwait

9.6.8.4 Saudi Arabia

9.6.8.5 Qatar

9.6.8.6 UAE

9.6.8.7 Israel

9.6.8.8 South Africa

9.7. South America Metal Alloy Market

9.7.1 Key Market Trends, Growth Factors and Opportunities

9.7.2 Top Key Companies

9.7.3 Historic and Forecasted Market Size by Segments

9.7.4 Historic and Forecasted Market Size by Type

9.7.4.1 Ferrous Alloys

9.7.4.2 Non- Ferrous Alloys

9.7.4.3 Specialty Alloys

9.7.5 Historic and Forecasted Market Size by Application

9.7.5.1 Structural Components

9.7.5.2 Electrical Conductors

9.7.5.3 Heat Exchangers

9.7.5.4 Fasteners and Fittings

9.7.5.5 Consumer Goods

9.7.6 Historic and Forecasted Market Size by Form

9.7.6.1 Sheets

9.7.6.2 Bars and Rods

9.7.6.3 Powders

9.7.6.4 Foils

9.7.6.5 Tubes and Pipes

9.7.7 Historic and Forecasted Market Size by End User

9.7.7.1 Automotive

9.7.7.2 Aerospace

9.7.7.3 Construction

9.7.7.4 Electronics

9.7.7.5 Healthcare

9.7.8 Historic and Forecast Market Size by Country

9.7.8.1 Brazil

9.7.8.2 Argentina

9.7.8.3 Rest of SA

Chapter 10 Analyst Viewpoint and Conclusion

10.1 Recommendations and Concluding Analysis

10.2 Potential Market Strategies

Chapter 11 Research Methodology

11.1 Research Process

11.2 Primary Research

11.3 Secondary Research

|

Global Metal Alloy Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2035 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 19.0 Bn |

|

Forecast Period 2025-35 CAGR: |

9.6% |

Market Size in 2035: |

USD 52.08 Bn |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Form |

|

||

|

By End User |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||