Food Grade Alginate Market Synopsis

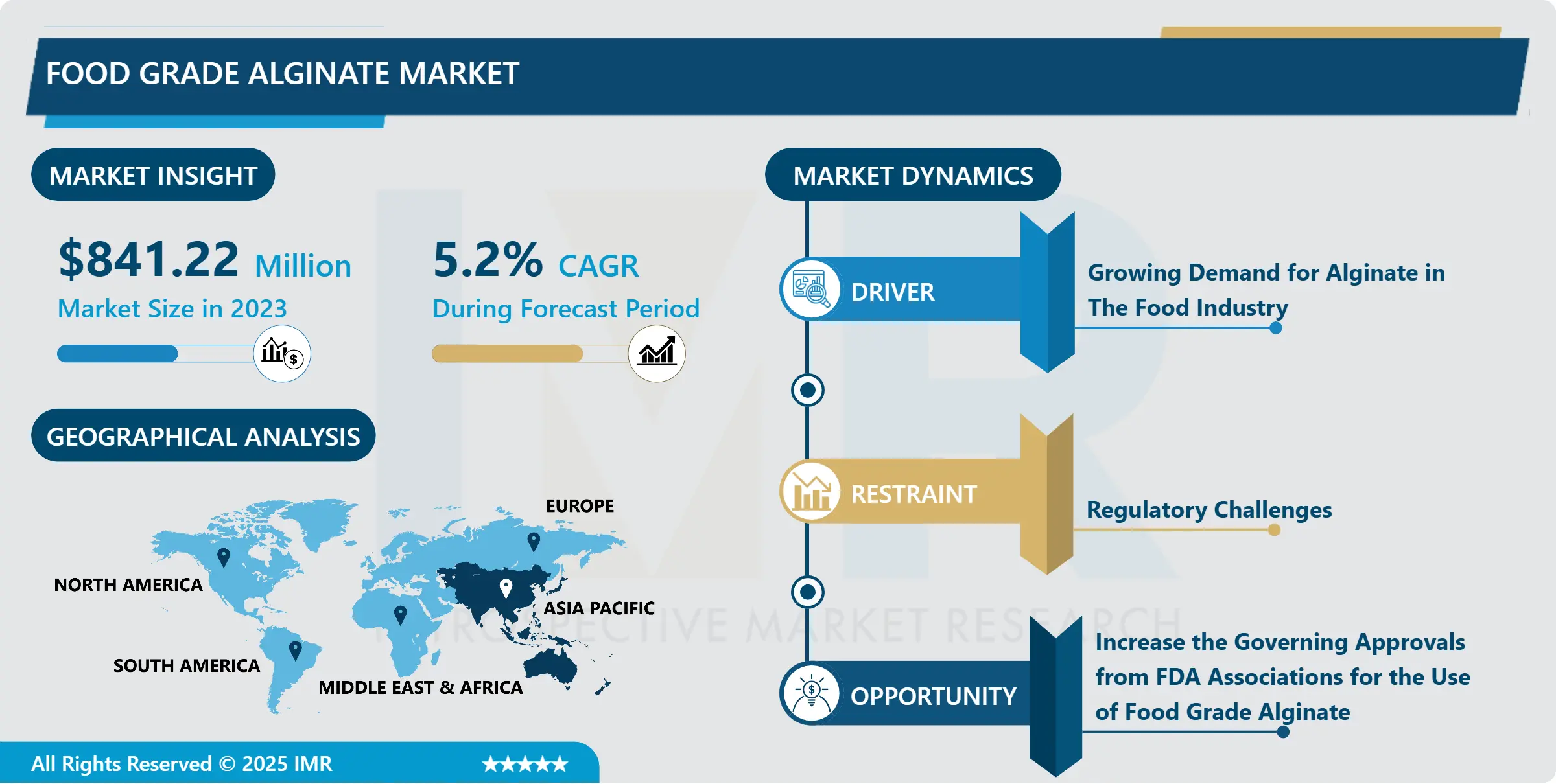

Global Food Grade Alginate Market size is expected to grow from USD 884.96 Million in 2024 to USD 1327.55 Million by 2032, at a CAGR of 5.2% during the forecast period (2025-2032)

The food-grade alginate market refers to the segment of the food industry focused on the production, distribution, and consumption of alginate, a natural polysaccharide derived primarily from seaweed. Food-grade alginate is utilized as a versatile additive, valued for its unique gelling, thickening, and stabilizing properties in a wide range of food products. It is commonly employed in food processing to enhance texture, improve mouthfeel, and extend shelf life. With its ability to form gels in the presence of calcium ions, food-grade alginate finds applications in various food products such as dairy, bakery, confectionery, and processed meats, among others. As consumer preferences for clean-label and natural ingredients continue to drive product innovation, the demand for food-grade alginate as a safe, plant-derived ingredient is expected to witness steady growth in the global food market.

The food grade alginate market is experiencing robust growth driven by an increasing demand for natural, plant-based ingredients in the food and beverage industry. Alginate, derived from seaweed, offers a versatile solution for food manufacturers seeking alternatives to synthetic additives.

Its unique properties, including thickening, gelling, and stabilizing capabilities, make it a valuable ingredient in various food products such as dairy, bakery, and confectionery. The market is also buoyed by growing consumer awareness regarding clean label products and health-conscious eating habits, further propelling the adoption of food grade alginate.

Additionally, the expanding applications of alginate in the pharmaceutical and healthcare sectors contribute to the market's growth trajectory. However, challenges such as fluctuating seaweed availability and regulatory constraints may hinder market expansion to some extent. Overall, the food grade alginate market is poised for steady growth, driven by increasing consumer preference for natural and sustainable ingredients in food and beverage formulations.

Food Grade Alginate Market Trend Analysis

The Surging Popularity of Alginate in the Food Industry

- In recent years, there has been a discernible shift in consumer preferences towards natural and plant-based ingredients in the realm of food production. This trend stems from a growing awareness among consumers regarding the health and environmental implications of their dietary choices. As individuals become more attuned to the source and composition of the foods they consume, there has been an increasing demand for ingredients that are derived from natural sources and align with sustainable practices. In this context, alginate, extracted from seaweed, has emerged as a highly sought-after ingredient due to its natural origin and versatile functionality as a thickening and gelling agent in food products. Its inherent properties not only cater to the desire for natural ingredients but also resonate with consumers' preferences for sustainable and eco-friendly options.

- Moreover, the surge in the popularity of alginate as a food additive can be attributed to its numerous benefits and applications within the food industry. Beyond its role as a thickener and gelling agent, alginate offers functional advantages such as stability, texture enhancement, and even health benefits. Its ability to improve the mouthfeel and consistency of food products without the need for artificial additives aligns perfectly with the clean label movement, which advocates for simpler and more transparent ingredient lists. As consumers increasingly seek out products with cleaner labels and fewer synthetic additives, alginate presents itself as a natural solution that meets these evolving preferences. Thus, the growing demand for natural and plant-based ingredients has not only propelled the popularity of alginate but has also underscored its relevance and importance in meeting the changing needs of today's discerning consumers.

Alginate's Versatility Reshaping Food Industry Trends

- The versatility of alginate within the food industry is indeed a driving force behind its market growth. Alginate's unique properties make it a highly adaptable ingredient that can be seamlessly integrated into a wide array of food applications. From dairy products to bakery items, confectionery treats, and beverages, alginate offers functional benefits that enhance both the texture and shelf-life of various food products. Its ability to form stable gels without the need for heat is particularly noteworthy, as it allows for the creation of indulgent treats like gummy candies, fruit jellies, and desserts with precise texture and consistency.

- Food manufacturers are increasingly recognizing the value of alginate as a versatile ingredient that enables them to innovate and differentiate their products in a competitive market landscape. By leveraging alginate's unique properties, manufacturers can develop new formulations or improve existing recipes to meet evolving consumer preferences and market trends. Whether it's enhancing the creaminess of dairy products, improving the structure of baked goods, or creating visually appealing confectionery items, alginate offers a versatile solution that enables food manufacturers to push the boundaries of culinary creativity. As a result, the adoption of alginate across various food applications continues to rise, driving its market growth and solidifying its position as a key ingredient in the food industry's quest for innovation and differentiation.

Food Grade Alginate Market Segment Analysis:

Food Grade Alginate Market is segmented based on Form, Packaging and Application

By Form, Powders segment is expected to dominate the market during the forecast period

- Powders stand as the cornerstone of numerous industries, wielding a dominant share owing to their unparalleled versatility and convenience across diverse applications. In the realm of food and beverage, powders reign supreme as essential ingredients, flavorings, and additives, seamlessly integrating into formulations while offering extended shelf life and ease of handling. Whether it's enhancing taste profiles, fortifying nutritional content, or ensuring product consistency, powders provide a flexible canvas for innovation, driving their dominance in this sector. Likewise, in pharmaceuticals, powders emerge as indispensable components in drug formulation and manufacturing processes. Their precise dosing, easy dispersibility, and compatibility with various delivery systems make them pivotal in producing tablets, capsules, and suspensions, where accuracy and efficacy are paramount. With stringent quality standards and regulatory requirements, powders command the lion's share in pharmaceutical applications, underpinning the foundation of medicinal advancements and therapeutic breakthroughs.

- Beyond consumables, powders exert their dominance in industrial landscapes, serving as fundamental materials in manufacturing, construction, and chemical processing. From powdered metals facilitating precise casting and molding in automotive and aerospace industries to powdered polymers revolutionizing additive manufacturing and 3D printing, their adaptability fuels innovation and drives efficiency. Moreover, in chemical processing and catalyst production, powders offer unrivaled surface area and reactivity, catalyzing reactions and accelerating processes in petrochemicals, environmental remediation, and beyond. With their inherent advantages of ease of storage, handling, and transport, powders emerge as the preferred choice across industrial sectors, commanding the lion's share in material sourcing and production workflows. In essence, the dominance of powders transcends boundaries, permeating through diverse industries and applications, where their versatility and utility serve as the cornerstone of progress and innovation.

By Application, Food & Beverage segment held the largest share in 2024

- Within the global economic landscape, few sectors wield as significant a presence as the food and beverage industry, commanding the largest share of market consumption worldwide. With a burgeoning population and evolving consumer preferences, this sector stands as a cornerstone of sustenance and indulgence, catering to diverse tastes and cultural palettes across the globe. From the bustling aisles of supermarkets to the quaint corners of local eateries, the pervasive influence of the food and beverage industry underscores its dominance in the market realm. Moreover, its expansive reach extends beyond mere sustenance, encompassing a myriad of products and applications that cater to varying dietary needs, culinary preferences, and lifestyle choices.

- The allure of the food and beverage industry lies not only in its sheer volume of consumption but also in its inherent adaptability and innovation. From traditional staples to avant-garde creations, this dynamic sector continually evolves to meet the ever-changing demands of consumers, driving growth and market expansion. Whether it's the convenience of powdered additives revolutionizing food processing or the indulgence of liquid flavorings enhancing culinary experiences, the versatility of products within this category solidifies its position as the largest shareholder in the market landscape. Moreover, with the rise of health-conscious consumers and sustainability initiatives, the food and beverage industry stands poised to maintain its dominance by embracing trends such as clean labeling, plant-based alternatives, and eco-friendly packaging solutions. In essence, as a testament to its pervasive influence and enduring appeal, the food and beverage industry stands tall as the unrivaled titan of market share, navigating the complexities of global consumption with innovation, resilience, and culinary delight.

Food Grade Alginate Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast period

- In the Asia Pacific region, the demand for food-grade alginate is propelled by several factors that collectively contribute to its dominance in the market. China, Japan, and India stand out as key players in this landscape, each experiencing rapid growth in their food and beverage industries. The rising urbanization and evolving consumer lifestyles in these countries have led to an increased preference for convenience foods, ranging from ready-to-eat meals to packaged snacks. Alginate's versatility as a stabilizer and texturizing agent makes it indispensable for manufacturers seeking to meet the demands of this burgeoning market segment. Moreover, the region's abundant seaweed resources offer a significant cost advantage for alginate production, as compared to other regions reliant on imported raw materials. This local availability not only ensures a stable supply chain but also reduces production costs, enabling manufacturers to offer competitive pricing in a highly price-sensitive market environment.

- Despite these opportunities, navigating the varied food regulations across different countries in the Asia Pacific region presents a notable challenge for market players. Each country has its own set of regulations governing food additives, labeling requirements, and permissible usage levels, necessitating a thorough understanding of local compliance standards. Managing compliance across multiple jurisdictions demands considerable resources and expertise, adding complexity to supply chain operations and product development processes. To maintain a dominant share in this diverse market landscape, companies must invest in robust regulatory affairs capabilities and establish strong partnerships with local regulatory authorities. By proactively addressing regulatory challenges and ensuring compliance with evolving standards, market leaders can sustain their competitive edge and capitalize on the immense growth potential offered by the Asia Pacific food-grade alginate market.

Active Key Players in the Food Grade Alginate Market:

- KIMICA

- IRO Alginate Industry Co., Ltd.

- Ceamsa Algae

- SNAP Natural & Alginate Product Pvt. Ltd.

- Algaia

- Marine Biopolymers Limited (MBL)

- DuPont de Nemours, Inc.

- Ingredients Solutions, Inc

- Shandong Jiejing Group Corporation

- Other Active Players

|

Food Grade Alginate Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 884.96 Mn. |

|

Forecast Period 2024-32 CAGR: |

5.2 % |

Market Size in 2032: |

USD 1327.55 Mn. |

|

Segments Covered: |

By Form |

|

|

|

By Packaging |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Food Grade Alginate Market by Form (2018-2032)

4.1 Food Grade Alginate Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Powders

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Liquid forms

4.5 Crystals

Chapter 5: Food Grade Alginate Market by Packaging (2018-2032)

5.1 Food Grade Alginate Market Snapshot and Growth Engine

5.2 Market Overview

5.3 Paper Bags

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 Fiber Drums

5.5 FIBC Bulk

5.6 Pails

Chapter 6: Food Grade Alginate Market by Application (2018-2032)

6.1 Food Grade Alginate Market Snapshot and Growth Engine

6.2 Market Overview

6.3 Food & Beverage

6.3.1 Introduction and Market Overview

6.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

6.3.3 Key Market Trends, Growth Factors, and Opportunities

6.3.4 Geographic Segmentation Analysis

6.4 Feed Additives

6.5 Pharmaceuticals

6.6 Others (such as industrial)

Chapter 7: Company Profiles and Competitive Analysis

7.1 Competitive Landscape

7.1.1 Competitive Benchmarking

7.1.2 Food Grade Alginate Market Share by Manufacturer (2024)

7.1.3 Industry BCG Matrix

7.1.4 Heat Map Analysis

7.1.5 Mergers and Acquisitions

7.2 MATTHEWS SPECIALTY VEHICLE

7.2.1 Company Overview

7.2.2 Key Executives

7.2.3 Company Snapshot

7.2.4 Role of the Company in the Market

7.2.5 Sustainability and Social Responsibility

7.2.6 Operating Business Segments

7.2.7 Product Portfolio

7.2.8 Business Performance

7.2.9 Key Strategic Moves and Recent Developments

7.2.10 SWOT Analysis

7.3 MOBILE SPECIALTY VEHICLES

7.4 SUMMIT BODYWORKS

7.5 LDV

7.6 STARTRACKS.ORG?INC

7.7 LEGACY

7.8 TOUTENKAMION

7.9 ADI MOBILE HEALTH

7.10 ODULAIR

7.11 IMAGI-MOTIVE

7.12 MOBILE HEALTHCARE FACILITIE

7.13 OTHER KEY PLAYERS

Chapter 8: Global Food Grade Alginate Market By Region

8.1 Overview

8.2. North America Food Grade Alginate Market

8.2.1 Key Market Trends, Growth Factors and Opportunities

8.2.2 Top Key Companies

8.2.3 Historic and Forecasted Market Size by Segments

8.2.4 Historic and Forecasted Market Size by Form

8.2.4.1 Powders

8.2.4.2 Liquid forms

8.2.4.3 Crystals

8.2.5 Historic and Forecasted Market Size by Packaging

8.2.5.1 Paper Bags

8.2.5.2 Fiber Drums

8.2.5.3 FIBC Bulk

8.2.5.4 Pails

8.2.6 Historic and Forecasted Market Size by Application

8.2.6.1 Food & Beverage

8.2.6.2 Feed Additives

8.2.6.3 Pharmaceuticals

8.2.6.4 Others (such as industrial)

8.2.7 Historic and Forecast Market Size by Country

8.2.7.1 US

8.2.7.2 Canada

8.2.7.3 Mexico

8.3. Eastern Europe Food Grade Alginate Market

8.3.1 Key Market Trends, Growth Factors and Opportunities

8.3.2 Top Key Companies

8.3.3 Historic and Forecasted Market Size by Segments

8.3.4 Historic and Forecasted Market Size by Form

8.3.4.1 Powders

8.3.4.2 Liquid forms

8.3.4.3 Crystals

8.3.5 Historic and Forecasted Market Size by Packaging

8.3.5.1 Paper Bags

8.3.5.2 Fiber Drums

8.3.5.3 FIBC Bulk

8.3.5.4 Pails

8.3.6 Historic and Forecasted Market Size by Application

8.3.6.1 Food & Beverage

8.3.6.2 Feed Additives

8.3.6.3 Pharmaceuticals

8.3.6.4 Others (such as industrial)

8.3.7 Historic and Forecast Market Size by Country

8.3.7.1 Russia

8.3.7.2 Bulgaria

8.3.7.3 The Czech Republic

8.3.7.4 Hungary

8.3.7.5 Poland

8.3.7.6 Romania

8.3.7.7 Rest of Eastern Europe

8.4. Western Europe Food Grade Alginate Market

8.4.1 Key Market Trends, Growth Factors and Opportunities

8.4.2 Top Key Companies

8.4.3 Historic and Forecasted Market Size by Segments

8.4.4 Historic and Forecasted Market Size by Form

8.4.4.1 Powders

8.4.4.2 Liquid forms

8.4.4.3 Crystals

8.4.5 Historic and Forecasted Market Size by Packaging

8.4.5.1 Paper Bags

8.4.5.2 Fiber Drums

8.4.5.3 FIBC Bulk

8.4.5.4 Pails

8.4.6 Historic and Forecasted Market Size by Application

8.4.6.1 Food & Beverage

8.4.6.2 Feed Additives

8.4.6.3 Pharmaceuticals

8.4.6.4 Others (such as industrial)

8.4.7 Historic and Forecast Market Size by Country

8.4.7.1 Germany

8.4.7.2 UK

8.4.7.3 France

8.4.7.4 The Netherlands

8.4.7.5 Italy

8.4.7.6 Spain

8.4.7.7 Rest of Western Europe

8.5. Asia Pacific Food Grade Alginate Market

8.5.1 Key Market Trends, Growth Factors and Opportunities

8.5.2 Top Key Companies

8.5.3 Historic and Forecasted Market Size by Segments

8.5.4 Historic and Forecasted Market Size by Form

8.5.4.1 Powders

8.5.4.2 Liquid forms

8.5.4.3 Crystals

8.5.5 Historic and Forecasted Market Size by Packaging

8.5.5.1 Paper Bags

8.5.5.2 Fiber Drums

8.5.5.3 FIBC Bulk

8.5.5.4 Pails

8.5.6 Historic and Forecasted Market Size by Application

8.5.6.1 Food & Beverage

8.5.6.2 Feed Additives

8.5.6.3 Pharmaceuticals

8.5.6.4 Others (such as industrial)

8.5.7 Historic and Forecast Market Size by Country

8.5.7.1 China

8.5.7.2 India

8.5.7.3 Japan

8.5.7.4 South Korea

8.5.7.5 Malaysia

8.5.7.6 Thailand

8.5.7.7 Vietnam

8.5.7.8 The Philippines

8.5.7.9 Australia

8.5.7.10 New Zealand

8.5.7.11 Rest of APAC

8.6. Middle East & Africa Food Grade Alginate Market

8.6.1 Key Market Trends, Growth Factors and Opportunities

8.6.2 Top Key Companies

8.6.3 Historic and Forecasted Market Size by Segments

8.6.4 Historic and Forecasted Market Size by Form

8.6.4.1 Powders

8.6.4.2 Liquid forms

8.6.4.3 Crystals

8.6.5 Historic and Forecasted Market Size by Packaging

8.6.5.1 Paper Bags

8.6.5.2 Fiber Drums

8.6.5.3 FIBC Bulk

8.6.5.4 Pails

8.6.6 Historic and Forecasted Market Size by Application

8.6.6.1 Food & Beverage

8.6.6.2 Feed Additives

8.6.6.3 Pharmaceuticals

8.6.6.4 Others (such as industrial)

8.6.7 Historic and Forecast Market Size by Country

8.6.7.1 Turkiye

8.6.7.2 Bahrain

8.6.7.3 Kuwait

8.6.7.4 Saudi Arabia

8.6.7.5 Qatar

8.6.7.6 UAE

8.6.7.7 Israel

8.6.7.8 South Africa

8.7. South America Food Grade Alginate Market

8.7.1 Key Market Trends, Growth Factors and Opportunities

8.7.2 Top Key Companies

8.7.3 Historic and Forecasted Market Size by Segments

8.7.4 Historic and Forecasted Market Size by Form

8.7.4.1 Powders

8.7.4.2 Liquid forms

8.7.4.3 Crystals

8.7.5 Historic and Forecasted Market Size by Packaging

8.7.5.1 Paper Bags

8.7.5.2 Fiber Drums

8.7.5.3 FIBC Bulk

8.7.5.4 Pails

8.7.6 Historic and Forecasted Market Size by Application

8.7.6.1 Food & Beverage

8.7.6.2 Feed Additives

8.7.6.3 Pharmaceuticals

8.7.6.4 Others (such as industrial)

8.7.7 Historic and Forecast Market Size by Country

8.7.7.1 Brazil

8.7.7.2 Argentina

8.7.7.3 Rest of SA

Chapter 9 Analyst Viewpoint and Conclusion

9.1 Recommendations and Concluding Analysis

9.2 Potential Market Strategies

Chapter 10 Research Methodology

10.1 Research Process

10.2 Primary Research

10.3 Secondary Research

|

Food Grade Alginate Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 884.96 Mn. |

|

Forecast Period 2024-32 CAGR: |

5.2 % |

Market Size in 2032: |

USD 1327.55 Mn. |

|

Segments Covered: |

By Form |

|

|

|

By Packaging |

|

||

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||