Electric Vehicle Drive System Market Synopsis

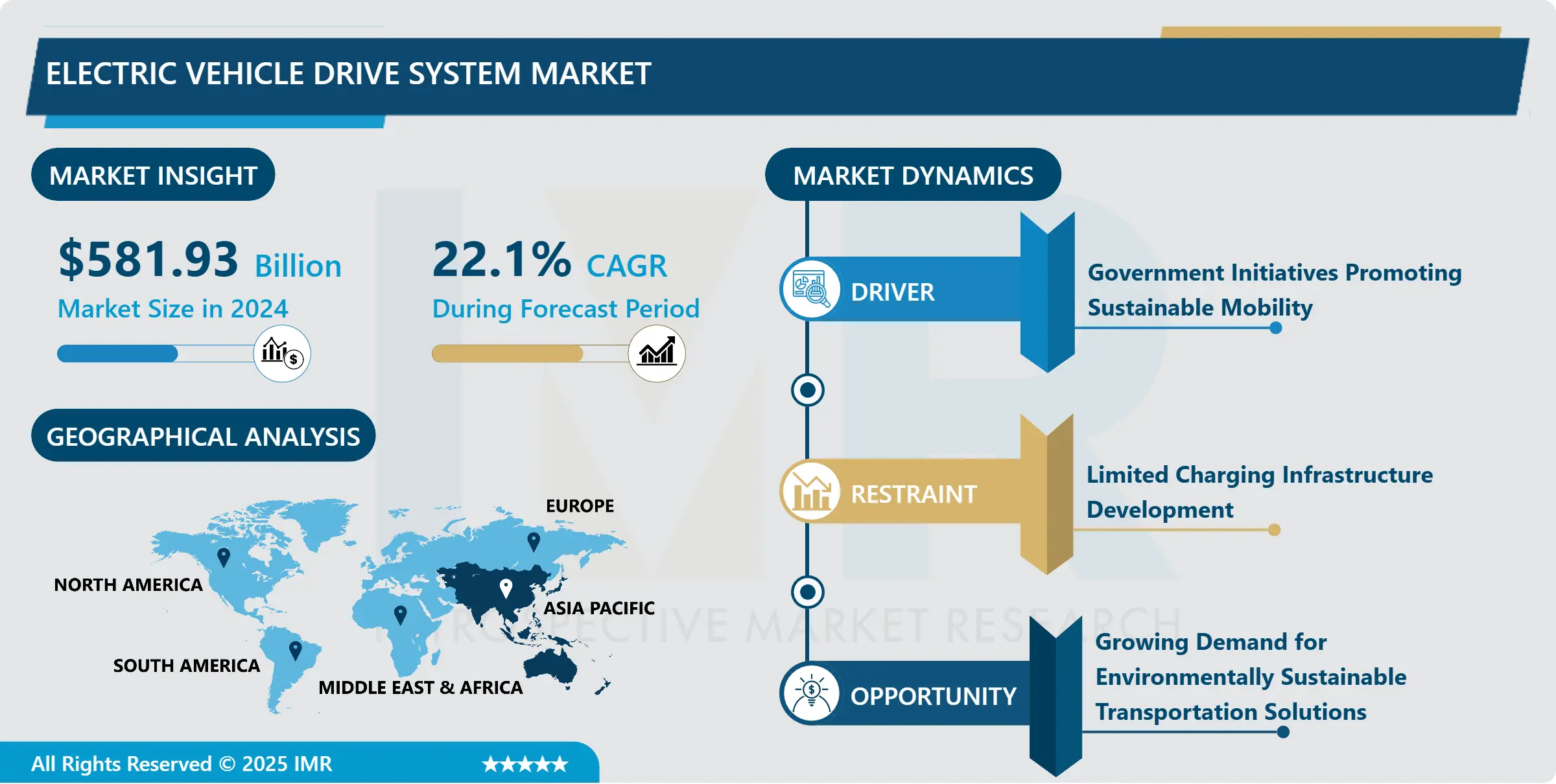

Electric Vehicle Drive System Market Size Was Valued at USD 581.93 Million in 2024, and is Projected to Reach USD 2874.72 Million by 2032, Growing at a CAGR of 22.1 % From 2025-2032.

An EV drive system is a subsystem that comprises the components that are used to power an electric vehicle. It usually comprises an electric motor, power electronics (inverters/converters), a battery pack for energy storage, and a transmission mechanism. The electric motor propels the vehicle by transforming electrical energy from the battery into mechanical energy. Power electronics regulate the power transfer between the battery and the motor. These components are at the core of an EV and are responsible for delivering propulsion in a clean and efficient manner without the use of internal combustion engines.

The EV drive system market has witnessed significant growth in recent years due to factors like rising environmental pollution, government subsidies/fiscal policies to support electric vehicles, and progress in battery technology. This market includes a variety of components such as electric motors, power electronics, and transmission systems that are all essential to the functioning of EVs. The growing popularity of EVs globally has also led to increased competition among automobile manufacturers and technology firms to provide effective drive system solutions to improve vehicle performance, increase range, and lower costs for consumers.

The demand for sustainability and strict emissions standards are fueling R&D to further increase the efficiency and innovation of EV drive systems. The EV drive system market looks promising due to the increasing electrification of the automotive industry.

Other growth factors The EV drive system market is also shaped by the increasing number of charging stations for electric vehicles. Governments and private businesses invest in infrastructure to construct both charging stations and networks; range anxiety decreases, enticing consumers to purchase electric vehicles.

The future development of autonomous driving technology is influencing the development of EV drive systems because these systems need more powerful and effective powertrains to support the advanced functions of EVs. Strategic partnerships among carmakers, tech companies, and utilities are emerging and advancing the development and connectivity of the EV value chain.

The shift towards decarbonization and addressing climate change is accelerating the focus on electric mobility – both in terms of legislation requirements and rising customer demand.

Electric Vehicle Drive System Market Trend Analysis

Electric Vehicle Drive System Market- Government Initiatives Promoting Sustainable Mobility

-

Electric Drive Systems with V2G: The Vehicle-to-Grid Revolution in Sustainable Transportation and Energy Management. This unique collaboration enables EVs not only to charge from the grid but also to discharge electricity back into it when required thus making them ‘mobile batteries’. With V2G functionalities, EVs can support grid stability through demand shaping, energy time-shifting, and load shifting. This integration has great potential to improve the grid’s ability to withstand disturbances, lower greenhouse gas emissions, and better manage energy use.

- This creates new opportunities for EV owners to earn additional income by taking part in demand response programs and energy markets. The potential of V2G technology and the role of Electric Drive Systems in its implementation are expected to significantly contribute to the development of the transportation and energy sectors in the future.

- Electric Drive Systems with Vehicle-to-Grid (V2G) offers not only the potential to transform the transportation and energy industries but also provides several avenues for addressing critical issues like climate change and grid instability. In addition to its application in grid regulation and energy management, V2G integration contributes to the creation of a more responsive and sustainable energy system by enabling the connection of distributed renewable energy systems to the grid. This relationship between EVs and the grid allows for more efficient utilization of renewable energy resources by utilizing excess generation and storing it in EV batteries for future use, addressing the intermittency challenges of renewables.

- The ability to supply energy from the car to the grid makes consumers of the electricity market and gives the opportunity to reduce electricity prices not only for an individual owner of the car but also for the entire community. As more infrastructure for V2G is developed and the use of EVs grows exponentially, the integration of Electric Drive Systems and V2G will become a driving force behind the shift towards renewable and distributed energy systems.

Electric Vehicle Drive System Market- Growing Demand for Environmentally Sustainable Transportation Solutions

- The shift towards cleaner and more sustainable mobility has led to a major increase in the EV drive system market. Due to rising concerns about climate change and air pollution, many governments, consumers, and industries are switching to the use of electric vehicles to replace traditional internal combustion engine cars. This shift is not only due to increased environmental awareness but also due to the development of EV technology such as more efficient batteries, more charging stations, and better overall performance.

- The government policies and incentives favoring EV adoption also help to further expand the market. Consequently, manufacturers and suppliers within the electric vehicle drive system market are facing increased demand, which is bringing innovation and investment in the production of further efficient and cost-effective electric drive systems to respond to the growing needs of the global transportation market.

- Other factors such as the governmental policies and technological advancements also contribute to the increasing demand for electric vehicle drive systems. High fuel and oil prices encourage consumers to opt for EVs because they cost less to operate and maintain over their entire life cycle.

- The growing number of electric vehicle options with different price ranges and body styles widens the customer base by attracting a broader range of potential buyers. Strategic partnerships between auto makers, tech firms and energy utilities also support market development, promote innovation and reduce barriers to the incorporation of EVs into conventional systems. In addition, the increasing emphasis on sustainability and corporate social responsibility among companies and fleet owners further promotes the development of EVs and the consumption of high-performance ED systems.

Electric Vehicle Drive System Market Segment Analysis:

Electric Vehicle Drive System Market is Segmented on the basis of Vehicle type and application.

By Type, Hybrid Electric Vehicles (HEVs) segment is expected to dominate the market during the forecast period

- Hybrid Electric Vehicles (HEVs):HEVs utilize both an ICE drivetrain and an electric drivetrain. It helps the internal combustion engine in driving the vehicle and enhances fuel economy and emissions. An HEV does not require being plugged into charge the battery as the regenerative braking and the ICE charge the battery.

- Plug-in Hybrid Electric Vehicles (PHEVs):Some PHEVs also have an internal combustion engine and an electric motor. Yet, PHEVs have larger battery packs than HEVs and can be charged by connecting to an external source. They provide higher all-electric range and longer periods of pure electric driving before the internal combustion engine is utilized.

By Application, E-Axle segment held the largest share in 2024

- E-Axle: This refers to an electric drive that incorporates the motor, power electronics and transmission components into a single assembly which is usually mounted on the axle of the vehicle. E-Axles are the emerging solution for electric vehicles because of their compactness, enhanced efficiency, and straightforward adaptability to conventional vehicle architectures. They are a convenient solution for car manufacturers who want to add electric vehicles to their fleet without major changes in design.

- E-Wheel Drive: In contrast to E-Axle, E-Wheel Drive implies the use of a separate electric motor in every wheel of the car. The following are some of the benefits of this configuration; better traction control, handling, and possibly efficiency through the right degree of torque vectoring. E-Wheel Drive systems may be coupled with all-wheel-drive (AWD) or four-wheel-drive (4WD) and enhance the vehicle performance in different driving situations..

Electric Vehicle Drive System Market Regional Insights:

The Asia-Pacific region is currently leading the charge in the electric vehicle drive system market.

- Asia-Pacific EV Drive System Market: Emerging as the Global Leader. Countries such as China, Japan, and South Korea are at the forefront, and the region has a well-established ecosystem with technological advances, favorable government policies, and growing EV consumer markets. China for instance has established itself as one of the leading manufacturers not only of EVs but also of other crucial components such as batteries and electric motors.

- Japan and South Korea have emerged as pioneers in the innovation of advanced automotive technologies that have attracted major investments in EV infrastructure and research. This regional leadership signifies the commitment of the Asia-Pacific to cut carbon emissions and promote clean energy for sustainable mobility.

- Other countries in the Asia-Pacific region such as China and Japan along with South Korea are also making great progress in the electric vehicle drive system market. For example, India is experiencing a significant growth in the EV market due to the government’s initiatives for promoting environmentally-friendly transportation and energy independence.

- Countries in Southeast Asia are gradually acknowledging the economic and environmental advantages of adopting electric vehicles and are thus putting in place favorable policies and building charging stations. Industrial might, technological advancements, and changes in customer preferences have led to considerable opportunities for the growth of the EV drive system market in the Asia-Pacific region and consolidated its position as a global leader in sustainable mobility. With further investments in research and development and manufacturing facilities, this region has the potential to define the future of the automotive industry globally.

Active Key Players in the Electric Vehicle Drive System Market

- ABB

- Aisin Corporation

- Allison Transmission

- Borgwarner, Bosch, Continental Ag

- Dana

- Denso

- GKN (Melrose)

- Hexagon AB

- Hitachi

- Huayu Automotive Electric System

- Hyundai Mobis

- Infineon Technologies

- Jatco

- Jing-Jin Electric Technologies

- LG Electronics

- Magna International

- Mahle

- Meidensha Corporation

- Meritor

- Nidec Corporation

- Shanghai Automotive Smart Electric Drive

- Siemens AG

- Smesh E-Axle

- ZF Group

- Other Active Players

Key Industry Developments in the Electric Vehicle Drive System Market:

- In January of 2024, Magna has revealed its latest 800V eDrive solution and has announced the arrival of a product on the market which, according to the company itself, sets a range of new standards for efficiency, power-to-weight ratio, and torque density.

|

Global Electric Vehicle Drive System Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 581.93 Mn. |

|

Forecast Period 2024-32 CAGR: |

22.1 % |

Market Size in 2032: |

USD 2874.72 Mn. |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||

Chapter 1: Introduction

1.1 Scope and Coverage

Chapter 2:Executive Summary

Chapter 3: Market Landscape

3.1 Market Dynamics

3.1.1 Drivers

3.1.2 Restraints

3.1.3 Opportunities

3.1.4 Challenges

3.2 Market Trend Analysis

3.3 PESTLE Analysis

3.4 Porter's Five Forces Analysis

3.5 Industry Value Chain Analysis

3.6 Ecosystem

3.7 Regulatory Landscape

3.8 Price Trend Analysis

3.9 Patent Analysis

3.10 Technology Evolution

3.11 Investment Pockets

3.12 Import-Export Analysis

Chapter 4: Electric Vehicle Drive System Market by Type (2018-2032)

4.1 Electric Vehicle Drive System Market Snapshot and Growth Engine

4.2 Market Overview

4.3 Hybrid electric vehicles (HEVs)

4.3.1 Introduction and Market Overview

4.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

4.3.3 Key Market Trends, Growth Factors, and Opportunities

4.3.4 Geographic Segmentation Analysis

4.4 Plug-in hybrid electric vehicles (PHEVs)

Chapter 5: Electric Vehicle Drive System Market by Application (2018-2032)

5.1 Electric Vehicle Drive System Market Snapshot and Growth Engine

5.2 Market Overview

5.3 E-Axle

5.3.1 Introduction and Market Overview

5.3.2 Historic and Forecasted Market Size in Value USD and Volume Units

5.3.3 Key Market Trends, Growth Factors, and Opportunities

5.3.4 Geographic Segmentation Analysis

5.4 E-Wheel Drive

Chapter 6: Company Profiles and Competitive Analysis

6.1 Competitive Landscape

6.1.1 Competitive Benchmarking

6.1.2 Electric Vehicle Drive System Market Share by Manufacturer (2024)

6.1.3 Industry BCG Matrix

6.1.4 Heat Map Analysis

6.1.5 Mergers and Acquisitions

6.2 BESPOKE COMPOSITE PANELS

6.2.1 Company Overview

6.2.2 Key Executives

6.2.3 Company Snapshot

6.2.4 Role of the Company in the Market

6.2.5 Sustainability and Social Responsibility

6.2.6 Operating Business Segments

6.2.7 Product Portfolio

6.2.8 Business Performance

6.2.9 Key Strategic Moves and Recent Developments

6.2.10 SWOT Analysis

6.3 DANA LIMITED

6.4 ESTRA AUTOMOTIVE

6.5 HELLA GMBH & CO. KGAA

6.6 KOHSAN CO.LTD

6.7 MAHLE GMBH

6.8 MODINE MANUFACTURING COMPANY

6.9 NIPPON LIGHT METALS

6.10 PRIATHERM

6.11 LEONI AG (GERMANY)

6.12 ROGERS CORPORATION (USA)

6.13 SCHUNK CARBON TECHNOLOGY (GERMANY)

6.14 TE CONNECTIVITY (SWITZERLAND)

6.15 SUMITOMO ELECTRIC INDUSTRIES LTD. (JAPAN)

6.16 SANHUA AUTOMOTIVE

6.17 AND OTHER KEY PLAYERS

Chapter 7: Global Electric Vehicle Drive System Market By Region

7.1 Overview

7.2. North America Electric Vehicle Drive System Market

7.2.1 Key Market Trends, Growth Factors and Opportunities

7.2.2 Top Key Companies

7.2.3 Historic and Forecasted Market Size by Segments

7.2.4 Historic and Forecasted Market Size by Type

7.2.4.1 Hybrid electric vehicles (HEVs)

7.2.4.2 Plug-in hybrid electric vehicles (PHEVs)

7.2.5 Historic and Forecasted Market Size by Application

7.2.5.1 E-Axle

7.2.5.2 E-Wheel Drive

7.2.6 Historic and Forecast Market Size by Country

7.2.6.1 US

7.2.6.2 Canada

7.2.6.3 Mexico

7.3. Eastern Europe Electric Vehicle Drive System Market

7.3.1 Key Market Trends, Growth Factors and Opportunities

7.3.2 Top Key Companies

7.3.3 Historic and Forecasted Market Size by Segments

7.3.4 Historic and Forecasted Market Size by Type

7.3.4.1 Hybrid electric vehicles (HEVs)

7.3.4.2 Plug-in hybrid electric vehicles (PHEVs)

7.3.5 Historic and Forecasted Market Size by Application

7.3.5.1 E-Axle

7.3.5.2 E-Wheel Drive

7.3.6 Historic and Forecast Market Size by Country

7.3.6.1 Russia

7.3.6.2 Bulgaria

7.3.6.3 The Czech Republic

7.3.6.4 Hungary

7.3.6.5 Poland

7.3.6.6 Romania

7.3.6.7 Rest of Eastern Europe

7.4. Western Europe Electric Vehicle Drive System Market

7.4.1 Key Market Trends, Growth Factors and Opportunities

7.4.2 Top Key Companies

7.4.3 Historic and Forecasted Market Size by Segments

7.4.4 Historic and Forecasted Market Size by Type

7.4.4.1 Hybrid electric vehicles (HEVs)

7.4.4.2 Plug-in hybrid electric vehicles (PHEVs)

7.4.5 Historic and Forecasted Market Size by Application

7.4.5.1 E-Axle

7.4.5.2 E-Wheel Drive

7.4.6 Historic and Forecast Market Size by Country

7.4.6.1 Germany

7.4.6.2 UK

7.4.6.3 France

7.4.6.4 The Netherlands

7.4.6.5 Italy

7.4.6.6 Spain

7.4.6.7 Rest of Western Europe

7.5. Asia Pacific Electric Vehicle Drive System Market

7.5.1 Key Market Trends, Growth Factors and Opportunities

7.5.2 Top Key Companies

7.5.3 Historic and Forecasted Market Size by Segments

7.5.4 Historic and Forecasted Market Size by Type

7.5.4.1 Hybrid electric vehicles (HEVs)

7.5.4.2 Plug-in hybrid electric vehicles (PHEVs)

7.5.5 Historic and Forecasted Market Size by Application

7.5.5.1 E-Axle

7.5.5.2 E-Wheel Drive

7.5.6 Historic and Forecast Market Size by Country

7.5.6.1 China

7.5.6.2 India

7.5.6.3 Japan

7.5.6.4 South Korea

7.5.6.5 Malaysia

7.5.6.6 Thailand

7.5.6.7 Vietnam

7.5.6.8 The Philippines

7.5.6.9 Australia

7.5.6.10 New Zealand

7.5.6.11 Rest of APAC

7.6. Middle East & Africa Electric Vehicle Drive System Market

7.6.1 Key Market Trends, Growth Factors and Opportunities

7.6.2 Top Key Companies

7.6.3 Historic and Forecasted Market Size by Segments

7.6.4 Historic and Forecasted Market Size by Type

7.6.4.1 Hybrid electric vehicles (HEVs)

7.6.4.2 Plug-in hybrid electric vehicles (PHEVs)

7.6.5 Historic and Forecasted Market Size by Application

7.6.5.1 E-Axle

7.6.5.2 E-Wheel Drive

7.6.6 Historic and Forecast Market Size by Country

7.6.6.1 Turkiye

7.6.6.2 Bahrain

7.6.6.3 Kuwait

7.6.6.4 Saudi Arabia

7.6.6.5 Qatar

7.6.6.6 UAE

7.6.6.7 Israel

7.6.6.8 South Africa

7.7. South America Electric Vehicle Drive System Market

7.7.1 Key Market Trends, Growth Factors and Opportunities

7.7.2 Top Key Companies

7.7.3 Historic and Forecasted Market Size by Segments

7.7.4 Historic and Forecasted Market Size by Type

7.7.4.1 Hybrid electric vehicles (HEVs)

7.7.4.2 Plug-in hybrid electric vehicles (PHEVs)

7.7.5 Historic and Forecasted Market Size by Application

7.7.5.1 E-Axle

7.7.5.2 E-Wheel Drive

7.7.6 Historic and Forecast Market Size by Country

7.7.6.1 Brazil

7.7.6.2 Argentina

7.7.6.3 Rest of SA

Chapter 8 Analyst Viewpoint and Conclusion

8.1 Recommendations and Concluding Analysis

8.2 Potential Market Strategies

Chapter 9 Research Methodology

9.1 Research Process

9.2 Primary Research

9.3 Secondary Research

|

Global Electric Vehicle Drive System Market |

|||

|

Base Year: |

2024 |

Forecast Period: |

2025-2032 |

|

Historical Data: |

2018 to 2023 |

Market Size in 2024: |

USD 581.93 Mn. |

|

Forecast Period 2024-32 CAGR: |

22.1 % |

Market Size in 2032: |

USD 2874.72 Mn. |

|

Segments Covered: |

By Type |

|

|

|

By Application |

|

||

|

By Region |

|

||

|

Key Market Drivers: |

|

||

|

Key Market Restraints: |

|

||

|

Key Opportunities: |

|

||

|

Companies Covered in the report: |

|

||